The Quant Fund Market represents a significant segment within the broader investment industry, characterized by the use of quantitative models and algorithms to make investment decisions. Quantitative funds, also known as quant funds or quant strategies, employ mathematical and statistical techniques to analyze market data, identify trading opportunities, and manage investment portfolios. These funds leverage advanced computational tools and data analytics to generate alpha and outperform traditional investment strategies. With the increasing sophistication of quantitative techniques and the growing demand for systematic approaches to investing, the quant fund market has experienced substantial growth and evolution in recent years.

Meaning

Quantitative funds utilize quantitative analysis and computational algorithms to drive investment decisions, rather than relying on subjective judgment or qualitative factors. These funds employ mathematical models to analyze historical market data, identify patterns and trends, and develop predictive models for asset pricing and market behavior. Quantitative strategies encompass a wide range of approaches, including statistical arbitrage, trend-following, factor investing, and machine learning-based strategies. By harnessing the power of data and technology, quant funds aim to generate consistent returns and manage investment risks in an objective and systematic manner.

Executive Summary

The Quant Fund Market has emerged as a prominent force in the investment landscape, offering investors access to sophisticated quantitative strategies and systematic approaches to portfolio management. Quantitative funds leverage advanced mathematical models, statistical analysis, and computational techniques to identify investment opportunities, optimize portfolio allocations, and manage risk exposures. These funds cater to a diverse range of investors, including institutional investors, hedge funds, asset managers, and individual investors seeking enhanced returns and diversification benefits. As the demand for data-driven investment solutions continues to grow, the quant fund market is poised for further expansion and innovation.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Rise of Data Analytics: The proliferation of data analytics tools and techniques has revolutionized the quant fund market, enabling fund managers to access vast amounts of market data, analyze complex relationships, and extract actionable insights. Data-driven approaches, such as machine learning and artificial intelligence, are increasingly being integrated into quantitative strategies to enhance predictive modeling and decision-making capabilities.

Focus on Risk Management: Risk management is a key priority for quant funds, given the inherent complexities and uncertainties of financial markets. These funds employ sophisticated risk models and optimization techniques to manage portfolio exposures, control volatility, and mitigate downside risks. By incorporating risk management into their investment processes, quant funds seek to achieve more stable and consistent returns over time.

Adoption of Factor Investing: Factor investing has gained traction in the quant fund market, with funds utilizing systematic factors such as value, momentum, size, and quality to construct diversified portfolios and capture sources of alpha. Factor-based strategies offer investors a transparent and rules-based approach to investing, allowing them to systematically exploit market anomalies and generate excess returns.

Market Drivers

Technological Advancements: Advances in technology, including computational power, data storage, and cloud computing, have empowered quant funds to analyze larger datasets, develop more sophisticated models, and implement complex trading strategies with greater efficiency and precision.

Demand for Alpha Generation: Investors are increasingly seeking alternative sources of alpha beyond traditional asset classes, leading to growing interest in quantitative strategies that offer differentiated returns and low correlations to traditional market factors.

Regulatory Environment: Regulatory changes and market reforms have created opportunities for quant funds to capitalize on market inefficiencies, adapt to changing market dynamics, and navigate regulatory challenges with greater agility and transparency.

Market Restraints

Data Quality and Availability: The quality and availability of data can pose challenges for quant funds, particularly in accessing timely and accurate datasets, managing data biases and errors, and ensuring data integrity and confidentiality.

Model Risk and Uncertainty: Quantitative models are subject to model risk and uncertainty, including parameter estimation errors, data overfitting, and model misspecification, which can impact the performance and reliability of quant strategies in real-world market conditions.

Liquidity and Market Impact: The execution of quantitative trading strategies can be affected by liquidity constraints, market impact, and transaction costs, particularly in highly liquid or illiquid markets where large trades may move prices and distort market dynamics.

Market Opportunities

Alternative Data Sources: The proliferation of alternative data sources, including satellite imagery, social media sentiment, and internet of things (IoT) data, presents opportunities for quant funds to gain unique insights into market trends, consumer behavior, and economic indicators.

Machine Learning and AI: Machine learning and artificial intelligence (AI) techniques offer new avenues for quant funds to enhance predictive modeling, identify nonlinear patterns, and extract alpha from unstructured datasets, unlocking opportunities for innovation and alpha generation.

Factor-Based Strategies: Factor-based investing continues to evolve, with quant funds exploring novel factors, dynamic factor weighting schemes, and multi-factor strategies to capture sources of alpha, mitigate risk factors, and enhance portfolio diversification.

Market Dynamics

The Quant Fund Market operates in a dynamic and competitive environment shaped by factors such as technological innovation, regulatory developments, market volatility, and investor preferences. Market dynamics such as data availability, model sophistication, risk management practices, and liquidity conditions influence the performance and evolution of quant strategies, driving continuous innovation and adaptation within the industry.

Regional Analysis

The Quant Fund Market exhibits regional variations in terms of market maturity, regulatory frameworks, investor sophistication, and technological infrastructure. While developed markets such as the United States, Europe, and Asia-Pacific have well-established quant fund industries and sophisticated financial ecosystems, emerging markets in Latin America, Africa, and the Middle East present untapped opportunities for market expansion and growth.

Competitive Landscape

Leading Companies in the Quant Fund Market:

Renaissance Technologies LLC

Two Sigma Investments, LP

D.E. Shaw & Co., L.P.

Citadel LLC

AQR Capital Management, LLC

Bridgewater Associates, LP

Millennium Management LLC

Winton Group Ltd.

Man Group plc

WorldQuant LLC

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Segmentation

The Quant Fund Market can be segmented based on various factors, including:

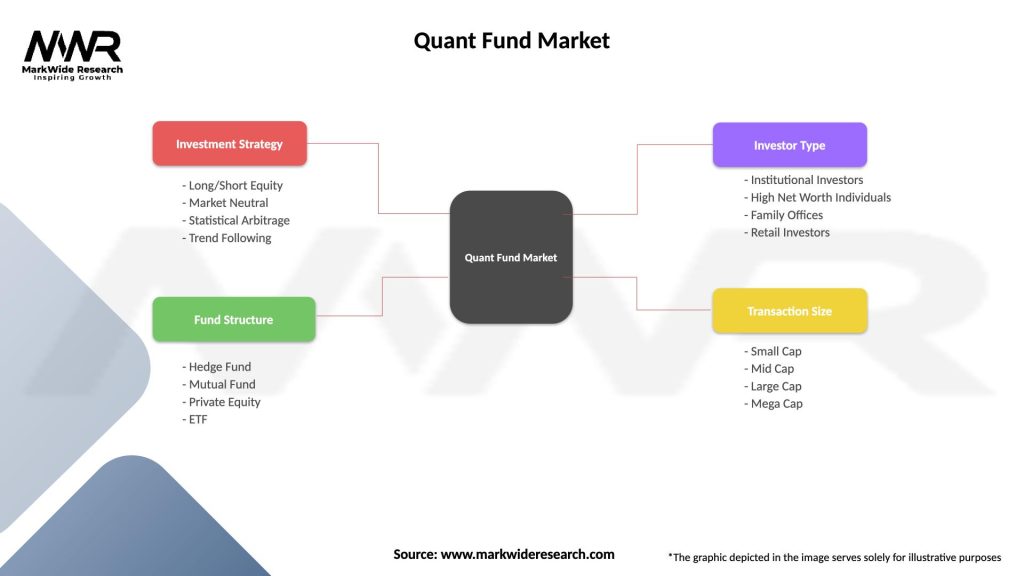

Investment Strategy: Segmentation by investment strategy includes market-neutral strategies, trend-following strategies, mean-reversion strategies, factor-based strategies, and high-frequency trading strategies, each catering to different investment objectives and risk profiles.

Asset Class: Segmentation by asset class includes equity funds, fixed-income funds, commodity funds, currency funds, and multi-asset funds, each focusing on specific asset classes and market segments.

Investor Type: Segmentation by investor type includes institutional investors, such as pension funds, endowments, and sovereign wealth funds, as well as high-net-worth individuals, family offices, and retail investors seeking exposure to quantitative strategies.

Category-wise Insight

Market-Neutral Strategies: Market-neutral strategies seek to generate returns independent of market direction by exploiting relative mispricings and inefficiencies across securities, sectors, or regions. These strategies typically involve long-short equity pairs trading, statistical arbitrage, and merger arbitrage techniques.

Trend-Following Strategies: Trend-following strategies aim to capitalize on momentum and trend persistence in asset prices by systematically buying or selling securities based on their price movements and trend signals. These strategies employ quantitative models to identify and exploit trends across different time frames and asset classes.

Factor-Based Strategies: Factor-based strategies seek to capture sources of risk premia associated with systematic factors such as value, momentum, size, quality, and low volatility. These strategies construct portfolios using factor-based models and risk factors to achieve targeted exposures and enhance risk-adjusted returns.

Key Benefits for Industry Participants and Stakeholders

Diversification: Quantitative strategies offer investors access to diversified investment opportunities and non-traditional return sources, reducing portfolio concentration risk and enhancing overall portfolio diversification.

Transparency: Quantitative strategies provide investors with greater transparency into investment processes, risk factors, and performance attribution, enabling more informed investment decisions and improved risk management practices.

Efficiency: Quantitative strategies leverage automation, scalability, and efficiency to streamline investment processes, reduce operational costs, and enhance portfolio management capabilities, delivering cost-effective solutions for investors.

Risk Management: Quantitative strategies employ rigorous risk management frameworks, quantitative models, and portfolio optimization techniques to manage investment risks, control volatility, and preserve capital in diverse market conditions.

SWOT Analysis

A SWOT analysis of the Quant Fund Market provides insights into its strengths, weaknesses, opportunities, and threats:

Strengths:

Quantitative rigor and systematic approach

Diversified sources of alpha and risk premia

Scalability and efficiency of investment processes

Enhanced risk management and portfolio optimization

Weaknesses:

Model risk and uncertainty

Data limitations and biases

Liquidity and execution risks

Regulatory and compliance challenges

Opportunities:

Technological innovation and data analytics

Emerging markets and untapped investor segments

Alternative data sources and machine learning techniques

Factor-based investing and smart beta strategies

Threats:

Market volatility and systemic risks

Regulatory changes and compliance burdens

Competitive pressures and fee compression

Technological disruptions and cybersecurity threats

Market Key Trends

Quantamental Investing: The convergence of quantitative and fundamental approaches, known as quantamental investing, is gaining popularity among asset managers, combining quantitative models with qualitative insights to enhance investment decision-making and alpha generation.

Machine Learning and AI: Machine learning and artificial intelligence (AI) techniques are revolutionizing the quant fund industry, enabling fund managers to develop predictive models, identify nonlinear patterns, and extract alpha from unstructured datasets with greater accuracy and efficiency.

Alternative Data Adoption: The adoption of alternative data sources, including satellite imagery, social media sentiment, and IoT data, is reshaping the quant fund landscape, providing investors with unique insights into market trends, consumer behavior, and economic indicators.

COVID-19 Impact

The COVID-19 pandemic has had a significant impact on the Quant Fund Market, affecting market volatility, liquidity conditions, and investor sentiment. While the pandemic initially led to increased market volatility and dislocation, quantitative strategies demonstrated resilience and adaptability, with some funds capitalizing on market dislocations and others adjusting their models to navigate evolving market dynamics.

Key Industry Developments

Remote Work and Digital Transformation: The shift to remote work and digital transformation accelerated by the COVID-19 pandemic has prompted quant funds to invest in technology infrastructure, data analytics capabilities, and remote collaboration tools to support remote trading operations and ensure business continuity.

ESG Integration: Environmental, social, and governance (ESG) factors are increasingly being integrated into quantitative investment processes, with quant funds leveraging ESG data and analytics to identify sustainable investment opportunities, manage ESG-related risks, and meet investor demand for responsible investing solutions.

Regulatory Compliance: Regulatory compliance remains a key focus for quant funds, with increasing scrutiny from regulators on algorithmic trading, market manipulation, and investor protection. Quant funds are investing in compliance technology, monitoring tools, and governance frameworks to ensure adherence to regulatory requirements and industry best practices.

Analyst Suggestions

Data Quality and Governance: Quant funds should prioritize data quality and governance processes to ensure the integrity, accuracy, and reliability of data used in quantitative models, mitigating data biases, errors, and inconsistencies that could impact investment decisions and performance outcomes.

Model Validation and Stress Testing: Quant funds should conduct rigorous model validation and stress testing exercises to assess the robustness, stability, and reliability of quantitative models under different market scenarios, identifying potential vulnerabilities and improving risk management practices.

Talent Development and Diversity: Quant funds should invest in talent development and diversity initiatives to attract, retain, and develop a diverse workforce of quantitative analysts, data scientists, and technologists with the skills, expertise, and perspectives needed to drive innovation and resilience in the industry.

Future Outlook

The future outlook for the Quant Fund Market is optimistic, driven by factors such as technological innovation, data analytics, regulatory compliance, and investor demand for systematic investment solutions. Quantitative strategies are expected to continue evolving and expanding, with a focus on machine learning, alternative data, ESG integration, and multi-asset solutions to meet the evolving needs of investors and navigate complex market environments.

Conclusion

The Quant Fund Market represents a dynamic and rapidly evolving segment within the investment industry, characterized by the use of quantitative models and algorithms to drive investment decisions and manage portfolios. Quantitative strategies offer investors access to sophisticated investment approaches, enhanced risk management capabilities, and diversified sources of alpha and risk premia. By embracing technological innovation, regulatory compliance, and talent development, quant funds are well-positioned to navigate market uncertainties, capitalize on emerging opportunities, and deliver long-term value for investors in the evolving landscape of finance and investment management.

What is Quant Fund?

A Quant Fund is an investment fund that uses quantitative analysis and mathematical models to make investment decisions. These funds often rely on algorithms and statistical techniques to identify trading opportunities in various asset classes.

What are the key players in the Quant Fund Market?

Key players in the Quant Fund Market include firms like Renaissance Technologies, Two Sigma Investments, and AQR Capital Management, which utilize advanced data analysis and quantitative strategies to drive their investment processes, among others.

What are the growth factors driving the Quant Fund Market?

The growth of the Quant Fund Market is driven by the increasing availability of big data, advancements in machine learning technologies, and a growing demand for systematic trading strategies among institutional investors.

What challenges does the Quant Fund Market face?

The Quant Fund Market faces challenges such as market volatility, the risk of model overfitting, and regulatory scrutiny, which can impact the performance and operational strategies of these funds.

What opportunities exist in the Quant Fund Market for future growth?

Opportunities in the Quant Fund Market include the expansion of alternative data sources, the integration of artificial intelligence in trading strategies, and the potential for increased retail investor participation in quantitative investing.

What trends are shaping the Quant Fund Market today?

Current trends in the Quant Fund Market include the rise of ESG-focused quantitative strategies, the use of high-frequency trading algorithms, and the growing importance of data privacy and security in quantitative analysis.

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.