444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Poland property and casualty insurance system market represents a dynamic and rapidly evolving sector within the broader European insurance landscape. Poland’s insurance market has experienced significant transformation following the country’s economic development and integration with European Union regulatory frameworks. The market encompasses comprehensive coverage for property damage, liability protection, motor insurance, and various casualty insurance products tailored to both individual consumers and commercial enterprises.

Market dynamics indicate robust growth driven by increasing consumer awareness, regulatory compliance requirements, and expanding economic activities across various sectors. The Polish insurance sector has demonstrated resilience and adaptability, with property and casualty insurance representing a substantial portion of the overall insurance market. Digital transformation initiatives have revolutionized service delivery, enabling insurers to offer more personalized products and streamlined claims processing.

Economic growth in Poland has directly contributed to increased demand for comprehensive insurance coverage, particularly in the property sector where real estate values have appreciated significantly. The market shows strong potential for continued expansion, supported by favorable demographic trends, urbanization patterns, and growing middle-class purchasing power. Regulatory harmonization with EU standards has enhanced market stability and consumer confidence, creating opportunities for both domestic and international insurance providers.

The Poland property and casualty insurance system market refers to the comprehensive ecosystem of insurance products, services, and regulatory frameworks designed to protect individuals and businesses against financial losses from property damage, liability claims, and various casualty risks within the Polish territory. This market encompasses traditional insurance products such as homeowners insurance, commercial property coverage, motor vehicle insurance, general liability protection, and specialized casualty insurance solutions.

Property insurance components include coverage for residential and commercial buildings, contents protection, business interruption insurance, and specialized property risks. Casualty insurance elements encompass liability coverage, professional indemnity insurance, product liability protection, and various forms of accident insurance. The system operates under strict regulatory oversight to ensure consumer protection, market stability, and compliance with European Union insurance directives.

Market participants include domestic insurance companies, international insurers, reinsurance providers, insurance brokers, agents, and various technology service providers supporting the digital transformation of insurance operations. The system integrates traditional insurance principles with modern risk assessment technologies, data analytics, and customer service innovations to deliver comprehensive protection solutions.

Poland’s property and casualty insurance market demonstrates exceptional growth potential driven by economic expansion, regulatory modernization, and evolving consumer expectations. The market has successfully navigated various economic challenges while maintaining steady growth trajectories across multiple insurance segments. Digital adoption rates have accelerated significantly, with approximately 78% of insurance transactions now incorporating digital elements in the customer journey.

Competitive landscape features a balanced mix of domestic market leaders and international insurance groups, fostering innovation and competitive pricing strategies. The market benefits from strong regulatory frameworks that promote transparency, consumer protection, and market stability. Motor insurance represents the largest segment by premium volume, followed by property insurance and various casualty insurance products.

Emerging trends include increased adoption of usage-based insurance models, integration of Internet of Things (IoT) technologies for risk assessment, and development of specialized insurance products for emerging economic sectors. The market shows resilience against economic volatility and demonstrates consistent growth patterns aligned with Poland’s broader economic development trajectory. Customer satisfaction levels have improved significantly, with 85% of policyholders expressing satisfaction with their insurance providers’ services.

Market penetration rates for property and casualty insurance in Poland continue to expand, driven by mandatory insurance requirements, increased risk awareness, and growing asset values requiring protection. The market demonstrates strong fundamentals with consistent premium growth and improving loss ratios across major insurance segments.

According to MarkWide Research analysis, the market demonstrates exceptional resilience and adaptability, with insurance companies successfully implementing innovative solutions to meet evolving customer needs and regulatory requirements.

Economic growth serves as the primary driver for Poland’s property and casualty insurance market expansion. Rising disposable incomes, increased property ownership, and expanding business activities create substantial demand for comprehensive insurance coverage. Urbanization trends contribute significantly to market growth as more individuals and businesses require sophisticated insurance protection for their assets and operations.

Regulatory requirements mandate specific insurance coverage for various activities, including motor vehicle operation, professional services, and commercial operations. These mandatory insurance requirements provide a stable foundation for market growth while ensuring adequate protection for consumers and businesses. EU integration has harmonized insurance regulations, creating opportunities for cross-border insurance services and enhanced consumer protection standards.

Technological advancement enables insurers to offer more competitive products through improved risk assessment, streamlined operations, and enhanced customer service capabilities. Digital platforms have revolutionized insurance distribution, making products more accessible to consumers while reducing operational costs for insurance providers. Data analytics capabilities allow for more accurate pricing and personalized insurance solutions, driving market competitiveness and customer satisfaction.

Risk awareness among consumers and businesses has increased significantly, driven by education campaigns, media coverage of major losses, and professional risk management advice. This heightened awareness translates into increased demand for comprehensive insurance coverage across various risk categories.

Price sensitivity among consumers represents a significant challenge for the Polish property and casualty insurance market. Economic pressures and budget constraints often lead consumers to seek minimum coverage levels or delay insurance purchases, potentially limiting market growth potential. Competition intensity has resulted in pricing pressures that may impact profitability for insurance providers.

Regulatory complexity creates operational challenges for insurance companies, requiring substantial investments in compliance systems and processes. Frequent regulatory changes necessitate continuous adaptation of products, procedures, and systems, increasing operational costs and complexity for market participants.

Claims inflation poses ongoing challenges as repair costs, medical expenses, and legal settlements continue to rise faster than premium increases. This trend particularly affects motor insurance and property insurance segments where material and labor costs have increased significantly. Fraudulent claims represent an ongoing concern, requiring substantial investments in detection and prevention systems.

Economic uncertainty can impact consumer spending patterns and business investment decisions, potentially affecting demand for non-mandatory insurance products. Market saturation in certain segments may limit growth opportunities, requiring insurers to focus on product innovation and market expansion strategies.

Digital transformation presents substantial opportunities for market expansion through improved customer experience, operational efficiency, and product innovation. Artificial intelligence and machine learning technologies enable more sophisticated risk assessment, fraud detection, and customer service capabilities, creating competitive advantages for early adopters.

Emerging market segments offer significant growth potential, including cyber insurance, environmental liability coverage, and specialized insurance products for new economic sectors. Small and medium enterprises represent an underserved market segment with substantial growth potential as these businesses increasingly recognize the importance of comprehensive insurance protection.

Product customization opportunities exist through advanced data analytics and customer segmentation capabilities, enabling insurers to develop highly targeted insurance solutions. Usage-based insurance models particularly in motor insurance, offer opportunities to attract price-sensitive customers while improving risk selection and pricing accuracy.

Cross-selling opportunities within existing customer bases can drive revenue growth through comprehensive insurance packages and integrated financial services. Partnership strategies with technology companies, automotive manufacturers, and real estate developers can create new distribution channels and product development opportunities.

Competitive dynamics in the Polish property and casualty insurance market reflect a balanced ecosystem of domestic leaders and international players, fostering innovation while maintaining market stability. Market concentration has evolved through strategic mergers and acquisitions, creating stronger entities capable of investing in technology and expanding service capabilities.

Customer expectations continue to evolve, demanding more personalized products, faster service delivery, and transparent pricing structures. Digital-first approaches have become essential for market competitiveness, with customers expecting seamless online experiences throughout the insurance lifecycle. Claims processing efficiency has improved dramatically, with average settlement times reduced by approximately 40% through digital automation.

Pricing dynamics reflect sophisticated risk assessment capabilities and competitive market conditions. Telematics adoption in motor insurance has reached approximately 25% market penetration, enabling more accurate risk pricing and customer engagement. Reinsurance relationships provide market stability and enable insurers to write larger risks while maintaining appropriate capital allocation.

Distribution channel evolution shows increasing importance of digital platforms while maintaining the relevance of traditional agent networks for complex products and customer segments requiring personal service. Omnichannel strategies have become standard practice for leading market participants.

Comprehensive market analysis employs multiple research methodologies to ensure accuracy and reliability of market insights. Primary research includes extensive interviews with industry executives, regulatory officials, insurance brokers, and consumer representatives to gather firsthand market intelligence and trend analysis.

Secondary research encompasses analysis of regulatory filings, industry reports, financial statements, and market data from authoritative sources. Quantitative analysis utilizes statistical modeling and trend analysis to project market developments and identify growth opportunities across various market segments.

Market segmentation analysis examines performance across different product categories, distribution channels, customer segments, and geographic regions within Poland. Competitive intelligence gathering includes analysis of market positioning, product offerings, pricing strategies, and strategic initiatives of major market participants.

Regulatory analysis monitors changes in insurance legislation, EU directives, and supervisory guidance that may impact market dynamics. Consumer behavior studies examine purchasing patterns, satisfaction levels, and emerging preferences to identify market opportunities and challenges.

Warsaw metropolitan area dominates the Polish property and casualty insurance market, accounting for approximately 35% of total premium volume due to high concentration of businesses, elevated property values, and sophisticated insurance needs. The region demonstrates the highest adoption rates for innovative insurance products and digital service delivery channels.

Krakow and surrounding regions represent significant growth markets driven by economic development, technology sector expansion, and increasing foreign investment. Regional insurance penetration has improved substantially, with commercial insurance adoption rates reaching 68% among eligible businesses.

Gdansk and northern regions show strong performance in marine insurance, logistics-related coverage, and industrial property insurance segments. The region benefits from port activities, manufacturing operations, and growing tourism sector requiring specialized insurance solutions.

Wroclaw and western regions demonstrate robust growth in motor insurance and residential property coverage, supported by population growth and economic development. Cross-border insurance activities with neighboring EU countries create additional market opportunities in these regions.

Rural and smaller urban areas present growth opportunities through improved distribution networks and simplified insurance products tailored to local market needs. Agricultural insurance represents a specialized segment with significant potential for expansion and modernization.

Market leadership in Poland’s property and casualty insurance sector features a diverse mix of domestic champions and international insurance groups, creating a dynamic competitive environment that benefits consumers through innovation and competitive pricing.

Strategic partnerships between insurers and technology companies, automotive manufacturers, and financial institutions create competitive advantages through enhanced distribution capabilities and product innovation. Market consolidation continues through selective acquisitions and strategic alliances designed to strengthen market positions and operational capabilities.

By Product Type:

By Distribution Channel:

By Customer Segment:

Motor Insurance Category represents the largest segment with mandatory third-party liability requirements driving consistent demand. Telematics integration has revolutionized this category, enabling usage-based pricing models and improved risk assessment. Electric vehicle insurance represents an emerging subcategory with specialized coverage requirements and growing market potential.

Property Insurance Category demonstrates strong growth driven by increasing property values and enhanced risk awareness. Climate-related risks have become increasingly important, with insurers developing specialized coverage for weather-related damages. Smart home technology integration offers opportunities for risk reduction and premium optimization.

Commercial Liability Category shows robust expansion as businesses increasingly recognize the importance of comprehensive liability protection. Cyber liability insurance has emerged as a critical subcategory with rapid growth potential. Professional indemnity coverage continues to expand across various professional service sectors.

Specialty Insurance Category includes niche products such as marine insurance, aviation coverage, and specialized industrial risks. These segments offer higher margins but require specialized expertise and risk assessment capabilities. Environmental liability represents an emerging area with significant growth potential.

Insurance Companies benefit from market stability, regulatory clarity, and growing demand for sophisticated insurance products. Digital transformation opportunities enable operational efficiency improvements and enhanced customer engagement capabilities. Risk diversification across multiple product lines and customer segments provides stability and growth opportunities.

Consumers gain access to comprehensive protection solutions, competitive pricing, and improved service delivery through digital innovation. Regulatory protection ensures fair treatment and transparent pricing practices. Product customization enables tailored coverage solutions meeting specific individual and business needs.

Brokers and Agents benefit from diverse product portfolios, competitive commission structures, and technology support for enhanced customer service. Professional development opportunities enable specialization in high-value market segments. Digital tools improve efficiency and customer relationship management capabilities.

Reinsurers find attractive opportunities in a stable, well-regulated market with sophisticated risk management practices. Portfolio diversification across various risk categories provides balanced exposure. Technology partnerships enable enhanced risk assessment and pricing capabilities.

Strengths:

Weaknesses:

Opportunities:

Threats:

Digital-First Customer Experience has become the standard expectation, with insurers investing heavily in user-friendly mobile applications, online policy management, and automated claims processing. Artificial intelligence integration enables personalized product recommendations and streamlined underwriting processes.

Usage-Based Insurance Models continue to gain traction, particularly in motor insurance where telematics data enables precise risk assessment and fair pricing. Pay-as-you-drive and pay-how-you-drive models attract price-conscious consumers while improving risk selection for insurers.

Sustainability Integration reflects growing environmental consciousness, with insurers developing green insurance products and incorporating environmental factors into risk assessment. Climate risk modeling has become essential for property insurance underwriting and pricing strategies.

Cyber Insurance Expansion addresses increasing digital risks faced by businesses and individuals. Data breach coverage and cyber liability protection represent rapidly growing market segments with substantial future potential.

Parametric Insurance Solutions offer innovative approaches to traditional coverage challenges, particularly for weather-related risks and business interruption scenarios. These products provide faster claims settlement and reduced administrative costs.

Regulatory modernization initiatives have streamlined insurance operations while maintaining strong consumer protection standards. Solvency II implementation has enhanced risk management practices and capital allocation efficiency across the industry.

Technology partnerships between insurers and fintech companies have accelerated digital transformation initiatives. API integration enables seamless connectivity between insurance systems and third-party platforms, improving customer experience and operational efficiency.

Market consolidation through strategic mergers and acquisitions has created stronger market participants with enhanced capabilities and broader product portfolios. Cross-border partnerships within the EU have expanded service capabilities and market reach.

Product innovation has focused on emerging risks and underserved market segments. Microinsurance products have been developed to serve price-sensitive consumers, while specialized commercial coverage addresses complex business risks.

Distribution channel evolution has emphasized omnichannel approaches combining digital platforms with traditional agent networks. Bancassurance partnerships have expanded significantly, leveraging existing customer relationships for insurance distribution.

MarkWide Research recommends that insurance companies prioritize digital transformation investments to maintain competitive positioning and meet evolving customer expectations. Customer experience enhancement should focus on seamless omnichannel service delivery and personalized product offerings.

Risk management capabilities require continuous enhancement through advanced analytics, artificial intelligence, and predictive modeling technologies. Underwriting excellence will differentiate successful insurers in an increasingly competitive market environment.

Market expansion strategies should target underserved segments including small businesses, emerging risk categories, and specialized industry sectors. Product innovation must address evolving risk landscapes including cyber threats, climate change impacts, and technological disruptions.

Partnership development with technology providers, distribution partners, and complementary service providers can create competitive advantages and expand market reach. Strategic alliances should focus on enhancing customer value propositions and operational efficiency.

Regulatory compliance must remain a priority while seeking opportunities to influence policy development through industry participation and thought leadership. Proactive engagement with regulatory authorities can help shape favorable market conditions.

Market growth prospects remain positive, supported by continued economic development, increasing risk awareness, and expanding insurance penetration across various market segments. Digital transformation will continue driving operational improvements and customer satisfaction enhancements.

Technology integration will accelerate with artificial intelligence adoption reaching approximately 60% of insurance operations within the next five years. Blockchain technology may revolutionize claims processing and policy administration, improving transparency and reducing costs.

Product evolution will focus on emerging risks including cyber security, climate change, and technological disruptions. Parametric insurance solutions are expected to capture 15% market share in specific risk categories by 2028.

Market consolidation may continue selectively, creating stronger entities capable of investing in technology and expanding service capabilities. International expansion opportunities within the EU may drive strategic partnerships and cross-border service development.

Regulatory evolution will likely focus on consumer protection enhancement, digital service standards, and sustainability requirements. ESG considerations will become increasingly important in product development and investment strategies.

Poland’s property and casualty insurance system market demonstrates exceptional resilience and growth potential within the European insurance landscape. The market benefits from strong regulatory frameworks, economic stability, and increasing consumer sophistication driving demand for comprehensive insurance solutions.

Digital transformation has emerged as a critical success factor, enabling insurers to improve operational efficiency, enhance customer experience, and develop innovative products addressing evolving risk landscapes. Market participants who successfully integrate technology capabilities with traditional insurance expertise will capture the greatest opportunities for sustainable growth.

Future success will depend on continued innovation, customer-centric service delivery, and proactive adaptation to changing market conditions. The market’s strong fundamentals, combined with ongoing economic development and regulatory support, position Poland’s property and casualty insurance sector for continued expansion and modernization in the years ahead.

What is Property and Casualty Insurance System?

Property and Casualty Insurance System refers to a type of insurance that provides coverage for property loss and liability for damages to others. This includes various policies such as homeowners, auto, and commercial insurance, which protect individuals and businesses from financial losses due to unforeseen events.

What are the key players in the Poland Property and Casualty Insurance System Market?

Key players in the Poland Property and Casualty Insurance System Market include PZU, Warta, and Allianz, among others. These companies offer a range of insurance products tailored to meet the needs of consumers and businesses in Poland.

What are the growth factors driving the Poland Property and Casualty Insurance System Market?

The growth of the Poland Property and Casualty Insurance System Market is driven by increasing urbanization, rising awareness of insurance products, and the growing need for risk management solutions among businesses and individuals. Additionally, economic growth contributes to higher disposable incomes, leading to greater insurance uptake.

What challenges does the Poland Property and Casualty Insurance System Market face?

The Poland Property and Casualty Insurance System Market faces challenges such as regulatory changes, intense competition among insurers, and the impact of climate change on risk assessment. These factors can complicate pricing strategies and affect profitability for insurance providers.

What opportunities exist in the Poland Property and Casualty Insurance System Market?

Opportunities in the Poland Property and Casualty Insurance System Market include the expansion of digital insurance solutions, the introduction of innovative products tailored to specific consumer needs, and the potential for growth in underinsured segments. Insurers can leverage technology to enhance customer experience and streamline operations.

What trends are shaping the Poland Property and Casualty Insurance System Market?

Trends shaping the Poland Property and Casualty Insurance System Market include the increasing adoption of insurtech solutions, a focus on sustainability in insurance practices, and the rise of personalized insurance products. These trends reflect changing consumer preferences and the need for more efficient service delivery.

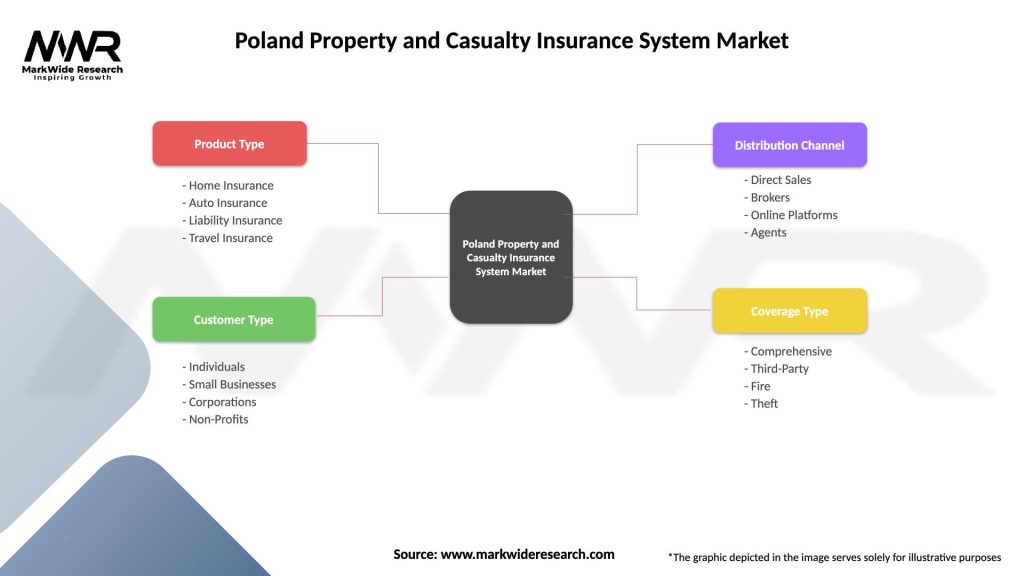

Poland Property and Casualty Insurance System Market

| Segmentation Details | Description |

|---|---|

| Product Type | Home Insurance, Auto Insurance, Liability Insurance, Travel Insurance |

| Customer Type | Individuals, Small Businesses, Corporations, Non-Profits |

| Distribution Channel | Direct Sales, Brokers, Online Platforms, Agents |

| Coverage Type | Comprehensive, Third-Party, Fire, Theft |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Poland Property and Casualty Insurance System Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.