The Poland property and casualty insurance market refers to the sector that deals with providing insurance coverage for properties and liabilities associated with various risks. Property and casualty insurance, commonly known as general insurance, offers protection against losses or damages to properties and liabilities arising from accidents, natural disasters, or other unforeseen events. It plays a crucial role in safeguarding individuals, businesses, and organizations against financial losses due to property damage, legal liabilities, or personal injuries.

Meaning

Property and casualty insurance in Poland encompasses a wide range of insurance products, including home insurance, car insurance, liability insurance, and commercial property insurance. These policies are designed to provide financial compensation for losses or damages incurred by policyholders due to covered risks. The insurance market in Poland has witnessed significant growth in recent years, driven by factors such as rising awareness of insurance products, increasing disposable income, and the growing importance of risk management.

Executive Summary

The Poland property and casualty insurance market has experienced steady growth over the past decade. The market is characterized by the presence of both domestic and international insurance companies, offering a wide range of insurance products to cater to the diverse needs of individuals and businesses. The industry has been influenced by various factors, including regulatory changes, technological advancements, and shifting consumer preferences.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Growing Demand for Home Insurance: The increasing number of residential properties and the rising awareness of the importance of home insurance have fueled the demand for property insurance policies in Poland.

Rising Automobile Sales: The expanding automotive industry in Poland has led to a surge in the demand for car insurance policies, driving the growth of the property and casualty insurance market.

Emphasis on Risk Management: Both individuals and businesses are recognizing the significance of risk management and are opting for liability insurance policies to protect themselves against potential legal liabilities.

Digital Transformation: The insurance industry in Poland is undergoing digital transformation, with insurers adopting advanced technologies such as artificial intelligence, machine learning, and data analytics to streamline operations, enhance customer experience, and develop innovative products.

Market Drivers

Increasing Awareness of Insurance: The growing awareness of the benefits of insurance coverage, coupled with rising disposable incomes, has led to an increase in the demand for property and casualty insurance policies in Poland.

Regulatory Support: Favorable regulations and government initiatives aimed at promoting insurance penetration and financial security have played a significant role in driving the growth of the market.

Economic Growth: Poland’s robust economic growth and increasing investments in infrastructure projects have created opportunities for the property and casualty insurance market, particularly in the construction and real estate sectors.

Changing Lifestyles and Risk Perception: The evolving lifestyle patterns and changing risk perception among individuals and businesses have contributed to the increased demand for insurance coverage against potential risks and losses.

Market Restraints

Low Insurance Penetration: Despite the growing awareness, the insurance penetration rate in Poland remains relatively low compared to other European countries, posing a challenge for market growth.

Price Competition: Intense competition among insurance providers has resulted in price pressures, affecting profit margins and hindering market growth.

Limited Product Innovation: The property and casualty insurance market in Poland has witnessed limited product innovation, leading to a lack of differentiation among insurers and hindering customer acquisition.

Complex Claims Process: The complex and time-consuming claims settlement process has been a significant challenge for the industry, impacting customer satisfaction and trust in insurers.

Market Opportunities

Untapped Potential in Rural Areas: There is significant untapped potential for property and casualty insurance in rural areas of Poland, where insurance awareness is relatively low compared to urban areas.

Product Customization: Insurers can seize opportunities by offering customized insurance products tailored to the specific needs of individuals and businesses, thereby enhancing customer satisfaction and loyalty.

Technological Advancements: The integration of advanced technologies such as artificial intelligence, telematics, and blockchain presents opportunities for insurers to streamline processes, improve risk assessment, and enhance customer engagement.

Partnerships and Distribution Channels: Collaborations with banks, financial institutions, and other distribution channels can help insurers expand their reach and tap into new customer segments.

Market Dynamics

The property and casualty insurance market in Poland is dynamic and influenced by several factors. Changing consumer behavior, technological advancements, regulatory developments, and competitive landscape significantly impact the industry’s growth and profitability. Insurers must stay agile and adapt to emerging trends to remain competitive and capitalize on market opportunities.

Regional Analysis

The property and casualty insurance market in Poland is geographically diverse, with varying insurance needs and preferences across different regions. Urban areas, such as Warsaw, Krakow, and Wroclaw, have higher insurance penetration rates due to higher population density and greater awareness. However, rural areas offer untapped potential for insurers to expand their customer base and increase market penetration through targeted marketing and awareness campaigns.

Competitive Landscape

leading companies in the Poland Property and Casualty Insurance Market:

PZU S.A.

Allianz Polska S.A.

Warta S.A.

Ergo Hestia S.A.

Aviva Towarzystwo Ubezpieczeń Ogólnych S.A.

Generali T.U. S.A.

UNIQA Towarzystwo Ubezpieczeń S.A.

HDI Global SE (Poland Branch)

Link4 Towarzystwo Ubezpieczeń S.A.

TU Europa S.A.

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

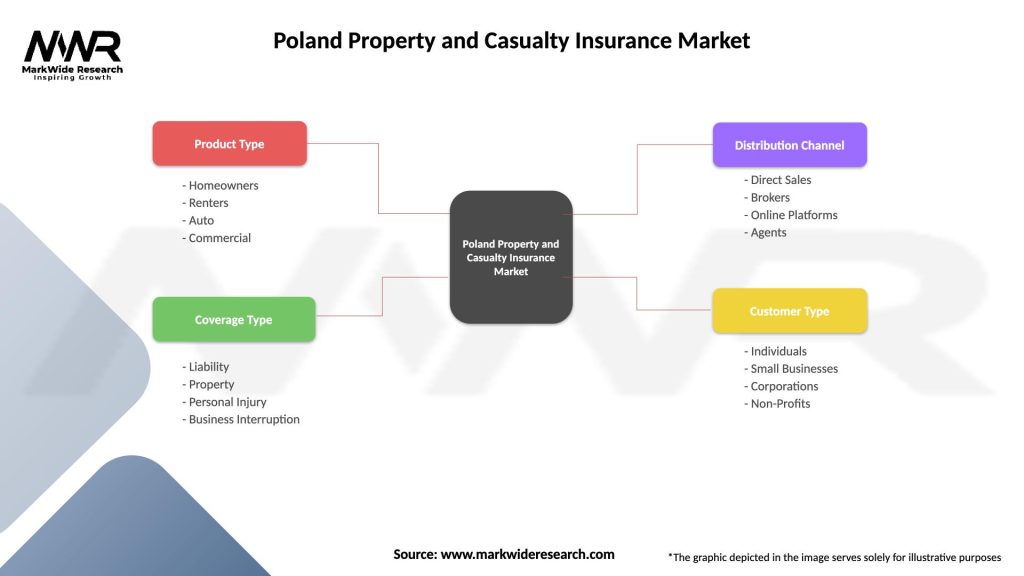

Segmentation

The property and casualty insurance market in Poland can be segmented based on insurance type, distribution channel, and end-user.

The demand for home insurance is driven by the increasing number of residential properties and the need to protect against risks such as fire, theft, and natural disasters.

Insurers can offer additional coverage options such as personal liability, home contents, and temporary accommodation to enhance the value proposition for customers.

Car Insurance:

The car insurance segment is witnessing growth due to the rising number of automobiles on the roads and the mandatory requirement of third-party liability insurance.

Insurers can leverage telematics and usage-based insurance models to offer personalized policies based on driving behavior and usage patterns.

Liability Insurance:

Liability insurance is gaining prominence as individuals and businesses seek protection against potential legal liabilities arising from accidents or third-party claims.

Insurers can provide specialized liability insurance products for different sectors, such as professional liability insurance for doctors or public liability insurance for event organizers.

Commercial Property Insurance:

The commercial property insurance segment caters to businesses and organizations, offering coverage against property damage, business interruption, and other associated risks.

Insurers can develop industry-specific policies and risk management solutions to address the unique needs and challenges faced by different sectors.

Key Benefits for Industry Participants and Stakeholders

Revenue Generation: The property and casualty insurance market offers significant revenue-generation opportunities for insurance providers, brokers, and intermediaries.

Risk Mitigation: Insurance policies help individuals and businesses mitigate financial risks associated with property damage, liabilities, and unforeseen events.

Business Expansion: Insurers can expand their customer base by developing innovative insurance products, entering new geographical markets, and forming strategic partnerships.

Enhanced Customer Experience: Insurers that prioritize customer-centricity and offer seamless digital experiences can attract and retain customers, fostering long-term relationships.

SWOT Analysis

Strengths:

Established insurance companies with a strong market presence

Diverse product portfolio catering to different insurance needs

Growing awareness of insurance products among individuals and businesses

Weaknesses:

Low insurance penetration compared to other European countries

Price competition affecting profit margins

Limited product innovation and differentiation among insurers

Opportunities:

Untapped potential in rural areas and niche insurance segments

Customization of insurance products to cater to specific customer needs

Integration of advanced technologies for process optimization and customer engagement

Threats:

Increasing regulatory requirements and compliance costs

Intense competition from domestic and international insurance providers

Economic volatility and uncertainties impacting insurance demand

Market Key Trends

Digitalization and Insurtech: Insurers are leveraging digital technologies to streamline operations, enhance underwriting processes, and improve customer engagement. Insurtech startups are disrupting the market with innovative solutions and customer-centric approaches.

Usage-Based Insurance: The adoption of telematics and IoT devices enables insurers to offer usage-based insurance policies, where premiums are based on individual behavior, driving patterns, or property usage. This approach promotes risk awareness and rewards responsible behavior.

Personalized Customer Experience: Insurers are investing in customer-centric strategies, providing personalized experiences through digital platforms, chatbots, and mobile applications. Tailored products, automated claims processing, and 24/7 customer support enhance customer satisfaction.

Sustainable and Green Insurance: The increasing focus on sustainability and environmental responsibility has led to the emergence of green insurance products. These policies incentivize eco-friendly practices and provide coverage for renewable energy projects and sustainable businesses.

Covid-19 Impact

The COVID-19 pandemic has had a significant impact on the property and casualty insurance market in Poland. The lockdown measures, business disruptions, and economic uncertainties have resulted in changes in risk profiles, insurance demands, and claim patterns. Insurers have faced challenges in assessing and pricing pandemic-related risks. However, the crisis has also highlighted the importance of insurance coverage and risk management, leading to increased awareness and demand for relevant policies.

Key Industry Developments

Regulatory Reforms: The Polish government has implemented regulatory reforms to enhance insurance penetration and consumer protection. These include measures to simplify insurance contract terms, promote fair competition, and strengthen the supervision of insurers.

Digital Transformation: Insurers are investing in digital transformation initiatives, such as online sales platforms, mobile apps, and digital claims processing systems, to improve operational efficiency and customer experience.

Strategic Partnerships: Insurance companies are forming strategic partnerships with technology firms, insurtech startups, and distribution channels to leverage their expertise, expand market reach, and offer innovative insurance solutions.

Green Initiatives: Insurers in Poland are increasingly focusing on sustainability and green initiatives. They are incorporating environmental, social, and governance (ESG) factors into their business strategies and offering green insurance products to address the growing demand for sustainable solutions.

Analyst Suggestions

Embrace Digital Transformation: Insurers should invest in advanced technologies and digital tools to streamline processes, enhance underwriting accuracy, and deliver personalized customer experiences.

Focus on Customer Centricity: Prioritize customer needs and preferences, offering tailored products, simplified claims processes, and proactive customer support to build trust and loyalty.

Enhance Risk Assessment: Leverage data analytics and artificial intelligence to improve risk assessment and pricing models, enabling insurers to offer more accurate and competitive insurance policies.

Collaborate and Innovate: Form strategic partnerships with insurtech startups, technology firms, and distribution channels to foster innovation, develop new insurance products, and expand market reach.

Future Outlook

The Poland property and casualty insurance market is expected to witness continued growth in the coming years. Factors such as increasing insurance awareness, rising disposable incomes, regulatory support, and technological advancements will drive market expansion. Insurers that embrace digital transformation, focus on customer-centricity, and innovate in product offerings are likely to gain a competitive edge in the evolving market landscape.

Conclusion

The property and casualty insurance market in Poland plays a vital role in protecting individuals, businesses, and organizations against financial losses due to property damage, legal liabilities, and personal injuries. The market has experienced steady growth, driven by factors such as increasing awareness of insurance, regulatory reforms, and changing risk perception. Insurers need to adapt to emerging trends, leverage technology, and offer customized solutions to meet the evolving needs of customers. The future outlook for the market is promising, with opportunities for revenue generation, risk mitigation, and business expansion.

What is Property and Casualty Insurance?

Property and Casualty Insurance refers to a type of insurance that provides coverage for property loss and liability for damages to others. This includes various forms of insurance such as homeowners, auto, and commercial insurance.

What are the key players in the Poland Property and Casualty Insurance Market?

Key players in the Poland Property and Casualty Insurance Market include PZU, Warta, and Allianz, among others. These companies offer a range of products catering to both individual and business needs.

What are the growth factors driving the Poland Property and Casualty Insurance Market?

The growth of the Poland Property and Casualty Insurance Market is driven by increasing urbanization, rising awareness of insurance products, and the growing need for risk management solutions among businesses and individuals.

What challenges does the Poland Property and Casualty Insurance Market face?

Challenges in the Poland Property and Casualty Insurance Market include regulatory changes, intense competition among insurers, and the impact of climate change on risk assessment and pricing.

What opportunities exist in the Poland Property and Casualty Insurance Market?

Opportunities in the Poland Property and Casualty Insurance Market include the expansion of digital insurance solutions, the rise of insurtech companies, and the increasing demand for customized insurance products tailored to specific consumer needs.

What trends are shaping the Poland Property and Casualty Insurance Market?

Trends in the Poland Property and Casualty Insurance Market include the adoption of advanced technologies like AI for underwriting, a shift towards more sustainable insurance practices, and the growing importance of customer-centric service models.

leading companies in the Poland Property and Casualty Insurance Market:

PZU S.A.

Allianz Polska S.A.

Warta S.A.

Ergo Hestia S.A.

Aviva Towarzystwo Ubezpieczeń Ogólnych S.A.

Generali T.U. S.A.

UNIQA Towarzystwo Ubezpieczeń S.A.

HDI Global SE (Poland Branch)

Link4 Towarzystwo Ubezpieczeń S.A.

TU Europa S.A.

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.