The Phased Array RF Front-End IC market represents a pivotal segment within the broader landscape of RF (Radio Frequency) technology. Phased array systems enable the manipulation of electromagnetic signals using multiple antennas, offering enhanced performance and flexibility in diverse applications ranging from communication systems to radar and imaging technologies.

Meaning

Phased Array RF Front-End ICs (Integrated Circuits) are integral components within phased array systems, facilitating the transmission and reception of RF signals. These ICs play a crucial role in beamforming, signal processing, and beam steering, enabling the dynamic control and optimization of electromagnetic waves for various applications.

Executive Summary

The Phased Array RF Front-End IC market is witnessing significant growth driven by burgeoning demand for advanced communication systems, radar technologies, and wireless networks. Key market participants are leveraging technological innovations to enhance IC performance, reduce power consumption, and optimize integration, thereby catering to diverse industry verticals and applications.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Growing Demand for 5G Infrastructure: The proliferation of 5G networks necessitates advanced RF front-end solutions, driving demand for Phased Array RF Front-End ICs capable of supporting high-frequency bands and complex modulation schemes.

Rise of Automotive Radar Systems: The increasing adoption of radar-based driver assistance systems and autonomous vehicles underscores the need for high-performance RF front-end ICs in automotive applications, driving market growth.

Expansion in Satellite Communication: Satellite communication systems rely on phased array antennas for beamforming and signal tracking, fueling demand for RF front-end ICs tailored to satellite communication applications.

Emergence of mmWave Technology: The emergence of millimeter-wave (mmWave) technology in communication and sensing applications necessitates RF front-end ICs capable of operating at higher frequencies with increased bandwidth and linearity.

Market Drivers

Advancements in Wireless Communication: Continuous advancements in wireless communication technologies, including 5G, Wi-Fi 6, and beyond, drive demand for high-performance RF front-end ICs capable of supporting higher data rates and spectral efficiency.

Proliferation of IoT Devices: The proliferation of IoT (Internet of Things) devices and smart sensors necessitates RF front-end ICs optimized for low-power operation, extended range, and connectivity in diverse IoT applications.

Adoption of Phased Array Radar Systems: Phased array radar systems find extensive applications in aerospace, defense, and automotive industries, propelling demand for RF front-end ICs capable of beamforming, beam steering, and signal processing.

Demand for Miniaturization and Integration: The trend towards miniaturization and integration in electronic devices drives demand for compact and highly integrated RF front-end ICs offering reduced footprint, improved performance, and lower cost.

Market Restraints

Complex Design Challenges: Designing RF front-end ICs for phased array systems entails complex engineering challenges related to signal integrity, power consumption, thermal management, and manufacturing yield, posing barriers to market entry and innovation.

Cost Sensitivity in Consumer Electronics: Price sensitivity in consumer electronics markets imposes constraints on the adoption of advanced RF front-end ICs, necessitating cost-effective solutions without compromising performance and quality.

Regulatory Compliance and Standards: Compliance with regulatory standards and spectrum allocations presents challenges for RF front-end IC manufacturers, necessitating adherence to stringent RF emission limits and interoperability requirements.

Supply Chain Disruptions: Global supply chain disruptions, including shortages of critical components and geopolitical uncertainties, pose risks to the production and supply of RF front-end ICs, affecting market stability and growth prospects.

Market Opportunities

Expansion in 5G Infrastructure: The ongoing deployment of 5G networks worldwide presents lucrative opportunities for RF front-end IC manufacturers to capitalize on the demand for high-performance components supporting 5G NR (New Radio) standards.

Rise of Automotive Radar Applications: The proliferation of automotive radar systems for ADAS (Advanced Driver Assistance Systems) and autonomous driving creates opportunities for RF front-end IC suppliers to develop customized solutions tailored to automotive radar requirements.

Deployment of satellite Constellations: The deployment of satellite constellations for global broadband connectivity and remote sensing applications necessitates RF front-end ICs capable of operating in space and harsh environmental conditions.

Investment in mmWave Technology: Investment in mmWave technology for communication, sensing, and imaging applications presents opportunities for RF front-end IC manufacturers to develop innovative solutions for emerging markets and applications.

Market Dynamics

The Phased Array RF Front-End IC market operates within a dynamic ecosystem shaped by technological advancements, regulatory trends, competitive dynamics, and evolving customer requirements. Market participants must navigate these dynamics to capitalize on growth opportunities, mitigate risks, and maintain competitive positioning in the global marketplace.

Regional Analysis

The Phased Array RF Front-End IC market exhibits regional variations driven by factors such as technological innovation, industrialization, regulatory frameworks, and market demand. Notable regional dynamics include:

North America: North America leads in RF technology innovation and adoption, driven by the presence of leading semiconductor companies, defense contractors, and telecommunications providers.

Europe: Europe emphasizes RF front-end ICs for aerospace, automotive, and industrial applications, supported by investments in research and development, standardization, and regulatory compliance.

Asia Pacific: Asia Pacific emerges as a key manufacturing hub for RF front-end ICs, benefiting from the presence of semiconductor foundries, electronics manufacturing services, and a burgeoning consumer electronics market.

Rest of the World: Emerging economies in regions such as Latin America, the Middle East, and Africa offer growth opportunities for RF front-end IC manufacturers, driven by infrastructure development, urbanization, and industrialization.

Competitive Landscape

Leading Companies in the Phased Array RF Front-End IC Market:

Broadcom Inc.

Qualcomm Technologies, Inc.

Skyworks Solutions, Inc.

Qorvo, Inc.

Analog Devices, Inc.

Infineon Technologies AG

Texas Instruments Incorporated

STMicroelectronics NV

NXP Semiconductors N.V.

MACOM Technology Solutions Holdings, Inc.

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

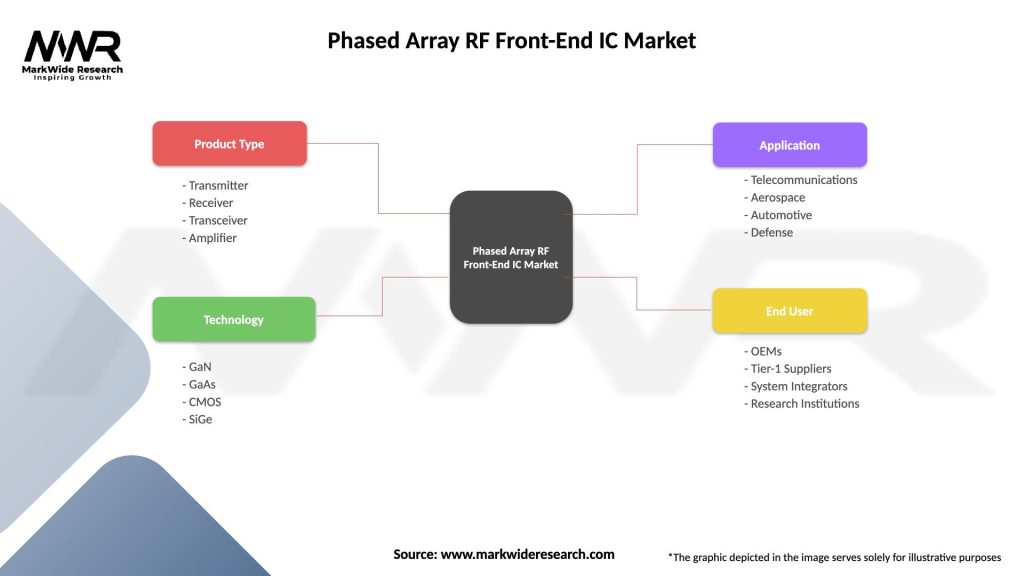

Segmentation

The Phased Array RF Front-End IC market can be segmented based on various factors, including:

Application: Segmentation by application, including communication systems, radar systems, satellite communication, automotive radar, IoT devices, and consumer electronics.

Frequency Band: Segmentation by frequency band, including sub-6 GHz bands, mmWave bands, and terahertz bands, reflecting different application requirements and market dynamics.

Integration Level: Segmentation by integration level, including discrete RF front-end ICs, RF modules, and system-on-chip (SoC) solutions, catering to diverse customer needs and product specifications.

Geography: Segmentation by geography, including North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa, reflecting regional variations in market demand, technology adoption, and regulatory frameworks.

Category-wise Insights

Communication Systems: RF front-end ICs for communication systems enable wireless connectivity in cellular networks, Wi-Fi, Bluetooth, and other wireless standards, supporting high data rates, extended range, and low latency.

Radar Systems: RF front-end ICs for radar systems enable target detection, tracking, and imaging in military, aerospace, automotive, and industrial applications, offering high sensitivity, resolution, and reliability.

Satellite Communication: RF front-end ICs for satellite communication systems facilitate uplink and downlink communications in satellite constellations, offering wide coverage, high throughput, and low latency.

Automotive Radar: RF front-end ICs for automotive radar systems enable collision avoidance, adaptive cruise control, and autonomous driving functionalities, offering high resolution, accuracy, and reliability.

Key Benefits for Industry Participants and Stakeholders

Industry participants and stakeholders stand to benefit from the Phased Array RF Front-End IC market in various ways:

Enabling Advanced Applications: RF front-end ICs enable advanced applications such as 5G communication, automotive radar, satellite communication, and IoT connectivity, fostering innovation and economic growth.

Improving System Performance: High-performance RF front-end ICs enhance system performance in terms of signal quality, range, data rate, and reliability, enabling superior user experiences and operational efficiency.

Optimizing Cost and Power: RF front-end ICs optimized for cost and power consumption enable affordable and energy-efficient solutions for mass-market adoption, driving economies of scale and market penetration.

Accelerating Time-to-Market: Ready-to-use RF front-end IC solutions accelerate product development cycles and time-to-market for OEMs and system integrators, enabling faster innovation and competitive advantage.

SWOT Analysis

A SWOT analysis offers insights into the Phased Array RF Front-End IC market’s strengths, weaknesses, opportunities, and threats:

Strengths: Advanced technology expertise, robust IP portfolio, established customer relationships, and diversified application domains.

Weaknesses: High R&D costs, complex design challenges, long product development cycles, and dependence on semiconductor manufacturing capabilities.

Opportunities: Emerging applications in 5G communication, automotive radar, satellite communication, and IoT connectivity, as well as geographic expansion in emerging markets.

Threats: Intense competition, price pressure, supply chain disruptions, and regulatory uncertainties impacting market growth and profitability.

Market Key Trends

Integration and Miniaturization: Trends towards integration and miniaturization drive demand for highly integrated RF front-end ICs with reduced footprint, improved performance, and lower power consumption.

Advanced Semiconductor Technologies: Adoption of advanced semiconductor technologies, including CMOS, SiGe, GaAs, and GaN, enables higher integration, wider bandwidth, and improved linearity in RF front-end ICs.

Multi-Band and Multi-Standard Support: Demand for RF front-end ICs supporting multi-band and multi-standard operation increases, enabling seamless connectivity across diverse wireless standards and frequency bands.

Software-Defined Radio (SDR): Adoption of SDR architectures in RF front-end ICs enables flexible and reconfigurable radio systems supporting multiple waveforms, protocols, and modulation schemes.

Covid-19 Impact

The Covid-19 pandemic has had both short-term and long-term impacts on the Phased Array RF Front-End IC market:

Short-term Disruptions: Supply chain disruptions, production slowdowns, and demand uncertainties resulting from lockdown measures and travel restrictions affected market growth and profitability in the short term.

Long-term Acceleration: The pandemic accelerated digital transformation initiatives, remote working trends, and investments in 5G infrastructure, driving demand for RF front-end ICs supporting wireless connectivity and communication technologies.

Resilience and Adaptability: Market players demonstrated resilience and adaptability by implementing remote work arrangements, digital collaboration tools, and agile supply chain strategies to mitigate pandemic-related risks and maintain business continuity.

Investments in Healthcare and Telemedicine: Increased investments in healthcare, telemedicine, and remote monitoring technologies spurred demand for RF front-end ICs enabling wireless connectivity and sensing applications in medical devices and IoT solutions.

Key Industry Developments

5G Deployment: Accelerated deployment of 5G networks worldwide drives demand for RF front-end ICs supporting 5G NR standards, mmWave frequencies, and massive MIMO (Multiple-Input Multiple-Output) architectures.

Automotive Radar Integration: Integration of automotive radar systems with ADAS and autonomous driving platforms fuels demand for RF front-end ICs enabling collision detection, object tracking, and adaptive cruise control functionalities.

satellite Constellation Rollout: Deployment of satellite constellations for global broadband connectivity and remote sensing applications creates opportunities for RF front-end ICs supporting satellite communication bands and frequencies.

IoT Connectivity Expansion: Expansion of IoT ecosystems in smart cities, industrial automation, and smart homes drives demand for RF front-end ICs enabling low-power, long-range, and secure wireless connectivity solutions.

Analyst Suggestions

Invest in R&D: Continued investment in R&D is imperative to develop next-generation RF front-end ICs with enhanced performance, integration, and cost-effectiveness, addressing evolving market requirements and technological trends.

Diversify Application Portfolio: Diversification of application portfolios across emerging markets and verticals such as 5G communication, automotive radar, satellite communication, and IoT connectivity mitigates risks and enhances growth opportunities.

Forge Strategic Partnerships: Collaboration with ecosystem partners, including OEMs, foundries, research institutions, and standards bodies, accelerates innovation, expands market reach, and drives adoption of RF front-end IC solutions.

Enhance Supply Chain Resilience: Strengthening supply chain resilience through strategic sourcing, inventory management, and supplier diversification mitigates risks associated with supply chain disruptions and enhances market competitiveness.

Future Outlook

The Phased Array RF Front-End IC market is poised for robust growth driven by accelerating demand for wireless connectivity, communication systems, and sensing applications across diverse industry verticals. Key trends shaping the market’s future outlook include:

5G Revolution: The ongoing deployment of 5G networks worldwide drives demand for RF front-end ICs supporting high-frequency bands, massive MIMO architectures, and advanced modulation schemes.

Automotive Radar Evolution: Integration of automotive radar systems with ADAS and autonomous driving platforms fuels demand for RF front-end ICs enabling collision detection, object tracking, and adaptive cruise control functionalities.

Satellite Communication Expansion: Deployment of satellite constellations for global broadband connectivity and remote sensing applications creates opportunities for RF front-end ICs supporting satellite communication bands and frequencies.

IoT Connectivity Proliferation: Expansion of IoT ecosystems in smart cities, industrial automation, and smart homes drives demand for RF front-end ICs enabling low-power, long-range, and secure wireless connectivity solutions.

Conclusion

In conclusion, the Phased Array RF Front-End IC market represents a dynamic and rapidly evolving segment within the broader RF technology landscape. Market participants must navigate complex engineering challenges, regulatory requirements, and competitive dynamics to capitalize on growth opportunities in emerging applications such as 5G communication, automotive radar, satellite communication, and IoT connectivity. By investing in innovation, forging strategic partnerships, and enhancing supply chain resilience, industry stakeholders can position themselves for sustained growth and leadership in the global marketplace.

What is Phased Array RF Front-End IC?

Phased Array RF Front-End IC refers to integrated circuits designed for phased array radar and communication systems. These ICs enable the electronic steering of beams, enhancing performance in applications such as telecommunications and military radar systems.

What are the key players in the Phased Array RF Front-End IC Market?

Key players in the Phased Array RF Front-End IC Market include companies like Analog Devices, Texas Instruments, and NXP Semiconductors. These companies are known for their innovative solutions and contributions to the development of advanced RF technologies, among others.

What are the growth factors driving the Phased Array RF Front-End IC Market?

The Phased Array RF Front-End IC Market is driven by the increasing demand for advanced communication systems and the growing adoption of radar technologies in defense applications. Additionally, the rise of IoT and smart devices is further propelling market growth.

What challenges does the Phased Array RF Front-End IC Market face?

Challenges in the Phased Array RF Front-End IC Market include the high cost of development and the complexity of integrating these systems into existing technologies. Additionally, competition from alternative technologies can hinder market expansion.

What future opportunities exist in the Phased Array RF Front-End IC Market?

Future opportunities in the Phased Array RF Front-End IC Market include advancements in 5G technology and the increasing use of phased array systems in automotive applications, such as autonomous driving. These trends are expected to create new avenues for growth.

What trends are shaping the Phased Array RF Front-End IC Market?

Trends in the Phased Array RF Front-End IC Market include the miniaturization of components and the integration of AI for enhanced signal processing. Additionally, the shift towards more efficient and compact designs is influencing product development.

Leading Companies in the Phased Array RF Front-End IC Market:

Broadcom Inc.

Qualcomm Technologies, Inc.

Skyworks Solutions, Inc.

Qorvo, Inc.

Analog Devices, Inc.

Infineon Technologies AG

Texas Instruments Incorporated

STMicroelectronics NV

NXP Semiconductors N.V.

MACOM Technology Solutions Holdings, Inc.

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.