P and C Insurance Software Market Analysis- Industry Size, Share, Research Report, Insights, Covid-19 Impact, Statistics, Trends, Growth and Forecast 2025-2034

P and C Insurance Software Market Analysis- Industry Size, Share, Research Report, Insights, Covid-19 Impact, Statistics, Trends, Growth and Forecast 2025-2034

The P and C (Property and Casualty) Insurance Software Market is witnessing significant growth and transformation in recent years. This market is driven by the increasing adoption of digital technologies and the rising need for efficient and streamlined insurance operations. P and C insurance software refers to the specialized software solutions designed to facilitate various processes and tasks related to property and casualty insurance, including policy administration, claims management, underwriting, billing, and customer management.

Meaning

P and C insurance software encompasses a wide range of applications and tools that enable insurance companies to automate and enhance their operations, improve customer service, reduce costs, and mitigate risks. These software solutions are tailored to address the unique needs and challenges of the property and casualty insurance sector, which involves insuring against property damage, liability claims, and other risks.

Executive Summary

The P and C insurance software Market has experienced substantial growth over the past few years and is expected to continue its upward trajectory. The market is driven by the increasing digitization of the insurance industry, the growing adoption of advanced technologies such as artificial intelligence (AI) and machine learning (ML), and the need for efficient and agile insurance operations. Insurance companies are leveraging P and C insurance software to streamline their processes, enhance customer experience, and gain a competitive edge in the market.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Cloud Adoption Surge: Over 60% of new P&C software deals in 2024 involved cloud-native solutions, reversing legacy on-premise dominance.

AI & Automation: Claims automation and predictive analytics are the fastest-growing segments, enabling 24/7 FNOL, automated damage assessment, and fraud detection.

Microservices Architecture: Insurers favor modular, API-first platforms that support rapid product launches and integration with third-party data providers (telematics, IoT).

Customer Experience Focus: Self-service portals and mobile apps rank among top investment areas, as 70% of policyholders expect end-to-end digital journeys.

Regulatory Compliance: Solutions featuring built-in compliance for GDPR, IFRS 17, and local regulatory regimes reduce audit overhead and speed market entry.

Market Drivers

Legacy Modernization: Pressing need to replace brittle, batch-oriented systems with real-time, configurable platforms.

Usage-Based Insurance (UBI): Telematics-driven auto products and parametric offerings for property risks open new underwriting frontiers.

AI-First Claims: Computer vision, NLP, and robotic process automation (RPA) for end-to-end claims servicing reduce cycle times and improve accuracy.

Microservices Marketplaces: Low-code/no-code marketplaces for prebuilt connectors, analytics modules, and regulatory templates.

Emerging Markets: Asia-Pacific and Latin America have strong demand for greenfield digital platforms to leapfrog legacy constraints.

Market Dynamics

Hybrid Modernization: Insurers adopt “bite-sized” modernization—replacing select modules (e.g., billing, claims) before full core transformation.

Insurtech Collaboration: Partnerships and joint ventures with nimble startups accelerate time-to-market for innovative products.

Subscription Models: Shift from perpetual licenses to SaaS subscription pricing aligns vendor incentives with insurer outcomes.

Regulatory Technology (RegTech): Built-in reporting and compliance engines speed adaptation to evolving insurance regulations.

Cloud-Native Trends: Kubernetes, containerization, and serverless computing reduce infrastructure overhead and enable elastic scaling.

Regional Analysis

North America: Leading adoption of advanced analytics, AI, and microservices architectures; large cloud-native deals by major carriers.

Europe: GDPR and Solvency II drive strong demand for compliance-centric platforms; InsurTech hubs in U.K., Germany, and Nordic countries.

Asia-Pacific: Fastest CAGR, with digital-first upstarts and regional giants in China and India investing heavily in core modernization and customer portals.

Latin America: Greenfield digital projects prevail, with mid-market and regional carriers selecting cloud-based platforms to rapidly expand product lines.

Middle East & Africa: Emerging demand tied to regulatory reforms and modernization of national insurers; mobile-first distribution channels prominent.

Competitive Landscape

Leading Companies in the P and C Insurance Software Market:

Applied Systems, Inc.

Guidewire Software, Inc.

Duck Creek Technologies, Inc.

Insurity, Inc.

Majesco

Sapiens International Corporation

EIS Group Ltd.

Accenture plc

PCMS Datafit Inc.

CodeObjects, Inc

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

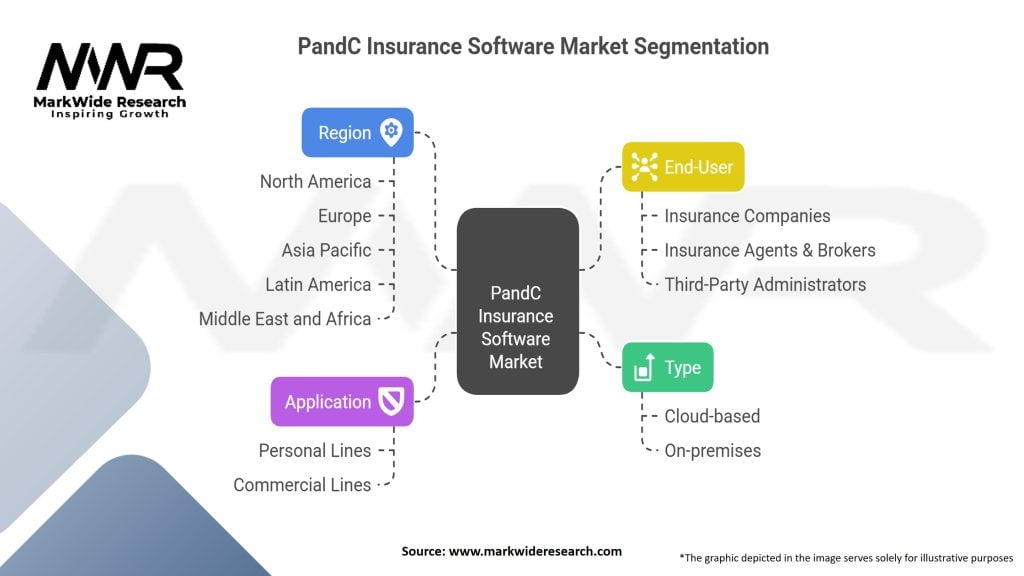

Segmentation

The P and C insurance software Market can be segmented based on:

Deployment Model:

On-premises: This segment includes software solutions installed and operated on the premises of the insurance company.

Cloud-based: This segment comprises software solutions delivered over the cloud, offering scalability, flexibility, and cost savings.

Application:

Policy Administration: This segment includes software solutions for managing policy creation, renewal, endorsements, and other policy-related processes.

Claims Management: This segment covers software solutions for efficient claims processing, including claim registration, assessment, settlement, and fraud detection.

Underwriting: This segment includes software solutions that support risk assessment, pricing, and decision-making in the underwriting process.

Billing and Payment: This segment encompasses software solutions for invoicing, premium collection, and payment processing.

Customer Management: This segment includes software solutions for managing customer data, interactions, and relationship management.

End-User:

Insurance Companies: This segment comprises software solutions designed specifically for insurance companies, including large enterprises and small and medium-sized insurers.

Insurance Agencies and Brokers: This segment includes software solutions tailored for insurance agencies and brokers, enabling them to manage policies, customer interactions, and commissions.

Category-wise Insights

Policy Administration: Highest revenue share; emphasis on end-to-end policy lifecycles and product configuration.

Claims Management: Fastest growth segment; automation, AI triage, and virtual claims handling drive investments.

Billing & Payments: Shift to omnichannel billing platforms and integrated payment gateways for seamless customer experiences.

Underwriting & Rating: Data enrichment and predictive modeling tools empower risk-based pricing and portfolio steering.

Distribution Management: Agent portals and embedded insurance modules expand reach and reduce acquisition costs.

Key Benefits for Industry Participants and Stakeholders

Open Insurance: APIs and developer portals foster innovative third-party integrations and ecosystems.

Embedded & On-Demand Products: Usage-based and event-triggered policies delivered via digital channels.

Low-Code/No-Code Platforms: Democratization of configuration empowers business users to drive change.

Blockchain & Smart Contracts: Pilot use cases in parametric insurance and secure data sharing for reinsurance.

Covid-19 Impact The pandemic accelerated digital transformation in P&C insurance, as carriers faced distributed workforces and surges in claims volume, particularly business-interruption and captive programs. Rapid deployment of cloud-based claims solutions and remote customer engagement tools became strategic imperatives. While IT budgets briefly tightened, carriers reprioritized investments in automation, analytics, and customer portals to build future resilience—fueling the current high-growth trajectory of P&C software adoption.

Key Industry Developments

Guidewire’s Cloud Upgrade (2024): Expanded multi-tenant SaaS offering with embedded AI modules for claim prediction and fraud detection.

Duck Creek’s Marketplace Launch (2023): Introduced low-code app store for third-party connectors, analytics, and digital-engagement widgets.

Sapiens-Solera Partnership (2022): Integrated telematics and claim-management workflows for automated auto damage appraisals.

Majesco’s Acquisition of InsurePay (2021): Enabled integrated billing and payments orchestration within core insurance workflows.

Analyst Suggestions

Adopt a Phased Modernization Approach: Balance quick wins—claims automation and digital distribution—with long-term core replacement roadmaps.

Invest in Data Quality: Ensure strong data governance and master data management to maximize AI/ML return on investment.

Embrace Ecosystem Play: Leverage open APIs to partner with insurtechs, IoT providers, and distribution platforms for integrated offerings.

Prioritize Cybersecurity: Embed security-by-design in every module and maintain continuous compliance with evolving data-privacy standards.

Cultivate Digital Talent: Build in-house capabilities in cloud engineering, data science, and agile delivery to drive sustainable innovation.

Future Outlook The P&C Insurance Software market will continue its rapid evolution as carriers deepen investments in AI, cloud, and ecosystem integrations. The distinction between core systems and digital front ends will blur, giving rise to platform-as-a-service models combining policy, claims, billing, distribution, and analytics in unified environments. Parametric and embedded products will proliferate, challenging incumbents to adapt product-configuration engines swiftly. Insurers and MGAs that align technology adoption with agile operating models and customer-centric strategies will secure competitive advantage in an increasingly digital and data-driven landscape.

Conclusion In summary, the P&C Insurance Software market stands at a pivotal juncture of modernization and innovation. By embracing cloud-native platforms, AI-powered automation, and open-architecture ecosystems, insurers can achieve operational excellence, regulatory compliance, and differentiated customer experiences. Strategic partnerships, phased transformation roadmaps, and a relentless focus on data quality and cybersecurity will underpin success. As market dynamics evolve, carriers that leverage cutting-edge software solutions to respond rapidly to emerging risks and customer needs will lead P&C insurance into its next era of growth and resilience.

What is P and C Insurance Software?

P and C Insurance Software refers to technology solutions designed to support property and casualty insurance operations, including policy management, claims processing, and underwriting. These software systems help insurers streamline their processes and improve customer service.

What are the key players in the P and C Insurance Software Market?

Key players in the P and C Insurance Software Market include Guidewire Software, Duck Creek Technologies, and Insurity. These companies provide a range of solutions that cater to various aspects of property and casualty insurance, among others.

What are the main drivers of growth in the P and C Insurance Software Market?

The growth of the P and C Insurance Software Market is driven by the increasing demand for digital transformation in the insurance sector, the need for enhanced customer experience, and the rising complexity of regulatory compliance. Additionally, the adoption of data analytics and AI technologies is also contributing to market expansion.

What challenges does the P and C Insurance Software Market face?

The P and C Insurance Software Market faces challenges such as the high cost of implementation and integration of new systems, resistance to change from traditional practices, and data security concerns. These factors can hinder the adoption of innovative software solutions.

What opportunities exist in the P and C Insurance Software Market?

Opportunities in the P and C Insurance Software Market include the growing trend of insurtech startups offering innovative solutions, the potential for partnerships between technology firms and insurance companies, and the increasing focus on customer-centric services. These factors are likely to shape the future landscape of the market.

What trends are currently shaping the P and C Insurance Software Market?

Current trends in the P and C Insurance Software Market include the rise of cloud-based solutions, the integration of artificial intelligence for claims processing, and the emphasis on data-driven decision-making. These trends are transforming how insurers operate and interact with their customers.

Leading Companies in the P and C Insurance Software Market:

Applied Systems, Inc.

Guidewire Software, Inc.

Duck Creek Technologies, Inc.

Insurity, Inc.

Majesco

Sapiens International Corporation

EIS Group Ltd.

Accenture plc

PCMS Datafit Inc.

CodeObjects, Inc

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.