444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

Market Overview

The orthopedic power tools market is a rapidly growing segment of the medical device industry, providing surgeons with specialized tools for performing orthopedic surgeries. These power tools offer precision, speed, and efficiency in bone cutting, drilling, and shaping procedures. This market overview provides valuable insights into the orthopedic power tools market, including its meaning, executive summary, key market insights, market drivers, market restraints, market opportunities, market dynamics, regional analysis, competitive landscape, segmentation, category-wise insights, key benefits for industry participants and stakeholders, SWOT analysis, market key trends, COVID-19 impact, key industry developments, analyst suggestions, future outlook, and conclusion.

Meaning

The orthopedic power tools market refers to the manufacturing, distribution, and usage of specialized tools designed to aid surgeons in orthopedic procedures. These power tools are battery-operated or electrically powered and are utilized for bone cutting, drilling, reaming, and shaping. Orthopedic power tools play a vital role in improving surgical precision, reducing operative time, and enhancing patient outcomes in orthopedic surgeries.

Executive Summary

The orthopedic power tools market has witnessed significant growth in recent years, driven by technological advancements, increasing prevalence of orthopedic disorders, and the rising demand for minimally invasive surgical procedures. The market offers a wide range of power tools designed for specific orthopedic procedures, providing surgeons with enhanced capabilities and improved patient care. This executive summary provides a concise overview of the orthopedic power tools market, highlighting key market insights, driving factors, market restraints, opportunities, and the competitive landscape.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Market Drivers

Market Restraints

Market Opportunities

Market Dynamics

The orthopedic power tools market is influenced by various dynamics, including technological advancements, regulatory landscape, market competition, and surgeon preferences. These factors interact to shape the growth and development of the market. Collaboration with surgeons, investment in research and development, and continuous product innovation are crucial for industry participants to meet the evolving needs of orthopedic surgeons and improve patient outcomes.

Regional Analysis

The orthopedic power tools market exhibits regional variations in terms of market size, healthcare infrastructure, regulatory frameworks, and surgical practices. Key regions analyzed in this report include North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. Each region has its specific market characteristics, influenced by factors such as healthcare expenditure, technological advancements, and surgeon preferences.

Competitive Landscape

Leading Companies in the Orthopedic Power Tools Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Segmentation

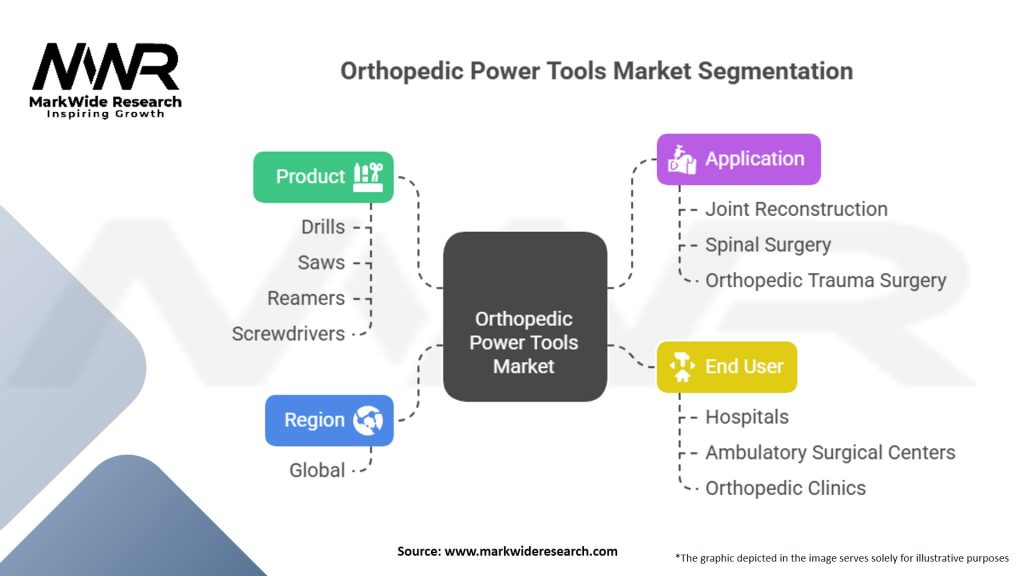

The orthopedic power tools market can be segmented based on various factors, including tool type (drills, saws, reamers, shavers, staplers), power source (electric-powered, battery-powered), and end-user (hospitals, ambulatory surgical centers, orthopedic clinics). The segmentation allows for a better understanding of the market landscape and aids in targeted marketing strategies and product development.

Category-wise Insights

Key Benefits for Industry Participants and Stakeholders

SWOT Analysis

Strengths:

Precision & Control: Advanced ergonomics and torque control improve surgical outcomes.

Broad Product Range: Drills, saws, reamers, and fixation devices cover diverse orthopedic procedures.

OEM Support: Leading device makers offer training, service, and regulatory compliance.

Weaknesses:

High Capital Cost: Premium equipment pricing limits adoption in smaller hospitals and clinics.

Sterilization Requirements: Complex sterilization cycles increase turnaround times.

Technical Learning Curve: Surgeons require specialized training for safe and effective use.

Opportunities:

Minimally Invasive Surgery: Growing MIS procedures drive demand for precision power tools.

Aging Population: Rising incidence of osteoporosis and joint disorders fuels procedural volumes.

Battery Technology Advances: Longer-life, lighter batteries improve portability and OR workflow.

Threats:

Regulatory Hurdles: Stringent device approval processes and evolving standards can delay launches.

Reusable vs. Disposable Debate: Trend toward single-use instrument sets could impact market dynamics.

Price Competition: Generic or lower-cost tool manufacturers may erode margins.

Market Key Trends

COVID-19 Impact

The COVID-19 pandemic has had a significant impact on the orthopedic power tools market. While the pandemic temporarily disrupted elective orthopedic surgeries, the market experienced a gradual recovery as healthcare systems adapted to the new normal. The pandemic highlighted the importance of maintaining a robust supply chain, ensuring patient safety, and adopting infection control measures in surgical settings.

Key Industry Developments

Analyst Suggestions

Future Outlook

The orthopedic power tools market is expected to witness continued growth in the coming years, driven by technological advancements, increasing prevalence of orthopedic disorders, and the demand for minimally invasive surgical procedures. The market’s future outlook appears promising, with opportunities arising from emerging economies, integration of advanced technologies, and surgeon-led innovations.

Conclusion

In conclusion, the orthopedic power tools market plays a crucial role in improving surgical precision, efficiency, and patient outcomes in orthopedic surgeries. The market offers a wide range of power tools designed for specific orthopedic procedures, catering to the unique needs of orthopedic surgeons and patients. By understanding the market dynamics, regional variations, and key trends, industry participants can make informed decisions, contribute to surgical advancements, and meet the evolving demands of orthopedic surgeons worldwide.

What is Orthopedic Power Tools?

Orthopedic power tools are specialized instruments used in orthopedic surgeries to assist in procedures such as bone cutting, drilling, and fixation. These tools enhance precision and efficiency in surgical operations, improving patient outcomes.

What are the key players in the Orthopedic Power Tools Market?

Key players in the Orthopedic Power Tools Market include DePuy Synthes, Stryker Corporation, Medtronic, and Zimmer Biomet, among others. These companies are known for their innovative products and extensive portfolios in orthopedic solutions.

What are the main drivers of growth in the Orthopedic Power Tools Market?

The growth of the Orthopedic Power Tools Market is driven by the increasing prevalence of orthopedic disorders, advancements in surgical technologies, and a rising aging population requiring joint replacement surgeries. Additionally, the demand for minimally invasive procedures is boosting market expansion.

What challenges does the Orthopedic Power Tools Market face?

The Orthopedic Power Tools Market faces challenges such as high costs of advanced surgical tools, stringent regulatory requirements, and the need for continuous training of medical personnel. These factors can hinder market growth and adoption rates.

What opportunities exist in the Orthopedic Power Tools Market?

Opportunities in the Orthopedic Power Tools Market include the development of smart surgical tools, increasing investments in healthcare infrastructure, and the growing trend of outpatient surgeries. These factors are expected to create new avenues for growth and innovation.

What trends are shaping the Orthopedic Power Tools Market?

Current trends in the Orthopedic Power Tools Market include the integration of robotics and automation in surgical procedures, the rise of personalized medicine, and the increasing focus on sustainability in manufacturing practices. These trends are transforming how orthopedic surgeries are performed.

Orthopedic Power Tools Market:

| Segmentation Details | Details |

|---|---|

| Product | Drills, Saws, Reamers, Screwdrivers, Others |

| Application | Joint Reconstruction, Spinal Surgery, Orthopedic Trauma Surgery, Others |

| End User | Hospitals, Ambulatory Surgical Centers, Orthopedic Clinics, Others |

| Region | Global |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading Companies in the Orthopedic Power Tools Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

North America

o US

o Canada

o Mexico

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA