444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Norway property insurance market represents a sophisticated and mature segment of the Nordic insurance landscape, characterized by comprehensive coverage solutions and innovative risk management approaches. Norwegian property insurance encompasses residential, commercial, and industrial property protection, serving a population that values security and comprehensive coverage against natural disasters, theft, and property damage.

Market dynamics in Norway reflect the country’s unique geographical challenges, including extreme weather conditions, flooding risks, and the need for specialized coverage for properties in remote areas. The market demonstrates steady growth with insurance penetration rates reaching approximately 92% of Norwegian households, indicating high consumer awareness and regulatory compliance requirements.

Digital transformation has significantly impacted the Norwegian property insurance sector, with insurtech solutions driving operational efficiency improvements of 35% across major providers. The market benefits from Norway’s advanced digital infrastructure, enabling seamless online policy management, claims processing, and customer service delivery.

Climate change adaptation has become a central focus, with insurers investing heavily in risk assessment technologies and preventive measures. The market shows increasing demand for specialized coverage against climate-related risks, reflecting Norway’s proactive approach to environmental challenges and sustainable insurance practices.

The Norway property insurance market refers to the comprehensive ecosystem of insurance products, services, and providers offering protection for residential, commercial, and industrial properties against various risks including fire, theft, natural disasters, and liability claims within the Norwegian territory.

Property insurance in Norway encompasses multiple coverage types designed to protect property owners from financial losses due to damage, destruction, or liability issues. This includes homeowners insurance, commercial property coverage, landlord insurance, and specialized policies for unique Norwegian property types such as cabins, boats, and seasonal residences.

Norwegian property insurance operates within a highly regulated framework that ensures consumer protection while promoting market competition. The market includes both traditional insurance companies and modern insurtech providers, offering diverse products ranging from basic coverage to comprehensive protection packages with additional services.

Risk assessment in the Norwegian context considers unique factors such as harsh weather conditions, geographical isolation of some properties, and specific building materials and construction methods common in Nordic architecture. This specialized approach ensures appropriate coverage and pricing for Norwegian property owners.

Market leadership in Norway’s property insurance sector is characterized by strong domestic players alongside international insurers, creating a competitive environment that benefits consumers through innovative products and competitive pricing. The market demonstrates resilience and stability with consistent growth patterns and high customer satisfaction rates.

Technological advancement drives market evolution, with artificial intelligence adoption increasing by 28% annually among leading insurers. Digital platforms enable enhanced customer experiences, streamlined claims processing, and improved risk assessment capabilities, positioning Norwegian insurers as regional technology leaders.

Regulatory compliance remains a key market characteristic, with Norwegian insurance regulations ensuring consumer protection while fostering innovation. The market benefits from clear regulatory frameworks that support both traditional insurance models and emerging insurtech solutions.

Climate resilience has become a defining market feature, with insurers developing specialized products for climate-related risks. This proactive approach addresses Norway’s unique environmental challenges while supporting the country’s sustainability goals and climate adaptation strategies.

Consumer behavior in Norway’s property insurance market reflects high awareness levels and sophisticated purchasing decisions. Norwegian consumers typically research multiple options and value comprehensive coverage over lowest-price alternatives, creating opportunities for premium product positioning.

Regulatory requirements serve as a primary market driver, with Norwegian law mandating specific insurance coverage for property owners, particularly in mortgage-related transactions. This regulatory framework ensures consistent market demand while protecting consumers and financial institutions from property-related risks.

Climate change impacts increasingly drive demand for comprehensive property insurance coverage. Norway’s experience with extreme weather events, flooding, and temperature fluctuations creates heightened awareness of property risks, leading to increased insurance adoption and coverage expansion among property owners.

Economic prosperity in Norway supports robust property insurance market growth, with high disposable income levels enabling consumers to invest in comprehensive coverage options. The strong Norwegian economy facilitates property ownership and associated insurance purchases, creating a stable market foundation.

Technological innovation drives market expansion through improved service delivery, enhanced risk assessment, and streamlined customer experiences. Norwegian insurers leverage advanced technologies to offer competitive advantages, attracting tech-savvy consumers who value digital convenience and innovative insurance solutions.

Urbanization trends contribute to market growth as more Norwegians move to urban areas with higher property values and increased insurance requirements. Urban property concentration creates opportunities for specialized coverage products and services tailored to city-specific risks and requirements.

High premium costs in certain regions, particularly areas prone to natural disasters, can limit market accessibility for some consumers. Premium pricing reflects risk levels but may create affordability challenges for property owners in high-risk zones, potentially limiting market penetration in specific geographical areas.

Complex policy structures sometimes deter consumers from purchasing comprehensive coverage, particularly among first-time property owners who may find insurance terms and conditions difficult to understand. This complexity can lead to under-insurance or delayed purchase decisions, impacting market growth potential.

Seasonal property challenges create unique market constraints, as many Norwegians own seasonal cabins and properties that require specialized coverage. These properties often present higher risks and require customized policies, creating operational challenges for insurers and potentially higher costs for consumers.

Regulatory compliance costs impact insurer operations and may be passed on to consumers through higher premiums. While regulations protect consumers, compliance requirements can increase operational expenses for insurance providers, potentially affecting market competitiveness and pricing strategies.

Geographic accessibility challenges in remote areas of Norway can limit service delivery and increase operational costs for insurers. Properties in isolated locations may face higher premiums or limited coverage options due to accessibility constraints and specialized risk factors.

Insurtech innovation presents significant opportunities for market expansion and service enhancement. Norwegian insurers can leverage emerging technologies such as IoT sensors, predictive analytics, and blockchain solutions to offer innovative products, improve risk assessment, and enhance customer experiences while reducing operational costs.

Sustainable insurance products offer growth opportunities as Norwegian consumers increasingly prioritize environmental responsibility. Green building coverage, energy-efficient property discounts, and climate adaptation services align with Norway’s sustainability goals while creating differentiation opportunities for forward-thinking insurers.

Cross-selling opportunities exist through integrated financial services offerings, allowing property insurers to expand into related products such as life insurance, investment services, and financial planning. This approach can increase customer lifetime value while providing comprehensive financial protection solutions.

International expansion opportunities emerge as Norwegian insurers develop expertise in Nordic and cold-climate property insurance. This specialized knowledge can be leveraged in similar markets, creating growth opportunities beyond Norway’s borders while diversifying revenue sources.

Partnership development with construction companies, real estate agencies, and property management firms can create new distribution channels and customer acquisition opportunities. Strategic partnerships can enhance market reach while providing value-added services to property owners throughout the ownership lifecycle.

Competitive intensity in Norway’s property insurance market drives continuous innovation and service improvement. Major players compete on coverage comprehensiveness, customer service quality, digital capabilities, and pricing strategies, creating a dynamic environment that benefits consumers through improved offerings and competitive rates.

Customer expectations continue evolving toward digital-first experiences, personalized coverage options, and proactive risk management services. Norwegian consumers expect seamless online interactions, mobile accessibility, and transparent communication, pushing insurers to invest in technology and customer experience improvements.

Risk landscape changes due to climate change, urbanization, and evolving property types require continuous adaptation of coverage products and pricing models. Insurers must balance risk exposure with market accessibility, developing sophisticated risk assessment capabilities to maintain profitability while serving diverse customer needs.

Regulatory evolution influences market dynamics through changing compliance requirements, consumer protection measures, and market conduct standards. MarkWide Research analysis indicates that regulatory changes typically drive 6-month adaptation cycles among Norwegian insurers, requiring agile operational capabilities and strategic planning.

Technology integration accelerates across all market segments, with artificial intelligence, machine learning, and automation transforming traditional insurance processes. These technological advances enable more accurate risk pricing, faster claims processing, and enhanced fraud detection capabilities, improving overall market efficiency.

Primary research methodologies employed in analyzing Norway’s property insurance market include comprehensive surveys of insurance providers, consumer behavior studies, and in-depth interviews with industry executives and regulatory officials. This approach ensures accurate representation of current market conditions and future trends.

Secondary research incorporates analysis of regulatory filings, financial reports, industry publications, and government statistics to provide comprehensive market understanding. Data sources include Norwegian insurance regulatory authorities, statistical agencies, and industry associations to ensure accuracy and reliability.

Market segmentation analysis examines various coverage types, customer demographics, geographical regions, and distribution channels to identify growth opportunities and market trends. This detailed segmentation approach enables precise market sizing and trend identification across different market components.

Competitive analysis methodology includes evaluation of market share, product offerings, pricing strategies, and customer satisfaction metrics across major insurance providers. This analysis provides insights into competitive positioning and strategic opportunities within the Norwegian market.

Trend analysis incorporates historical data review, current market assessment, and future projection modeling to identify emerging opportunities and potential challenges. This comprehensive approach ensures robust market insights and strategic recommendations for industry participants.

Oslo and surrounding areas represent the largest regional market segment, accounting for approximately 35% of total property insurance premiums due to high property values, population density, and commercial activity concentration. The capital region demonstrates strong demand for comprehensive coverage and premium insurance products.

Bergen and Western Norway show unique market characteristics due to coastal location and weather-related risks. This region demonstrates higher claims frequency related to water damage and storm-related incidents, requiring specialized coverage products and risk assessment approaches tailored to coastal property challenges.

Trondheim and Central Norway represent a balanced market with mixed residential and commercial properties. The region shows steady growth patterns with moderate risk profiles and consistent demand for standard property insurance coverage, making it an attractive market for both established and emerging insurance providers.

Northern Norway presents unique challenges and opportunities due to extreme weather conditions, seasonal accessibility issues, and specialized property types. Despite representing a smaller market share, this region shows premium pricing acceptance for specialized coverage addressing Arctic-specific risks and challenges.

Rural and remote areas across Norway demonstrate distinct insurance needs related to agricultural properties, seasonal residences, and accessibility challenges. These areas often require customized coverage solutions and may show different adoption patterns compared to urban markets, creating niche opportunities for specialized providers.

Market leadership in Norway’s property insurance sector is distributed among several key players, each offering distinct value propositions and serving different customer segments. The competitive environment encourages innovation while maintaining high service standards across the industry.

Competitive strategies focus on digital transformation, customer experience enhancement, and specialized product development. Leading insurers invest heavily in technology infrastructure, data analytics capabilities, and customer service improvements to maintain competitive advantages in the evolving market landscape.

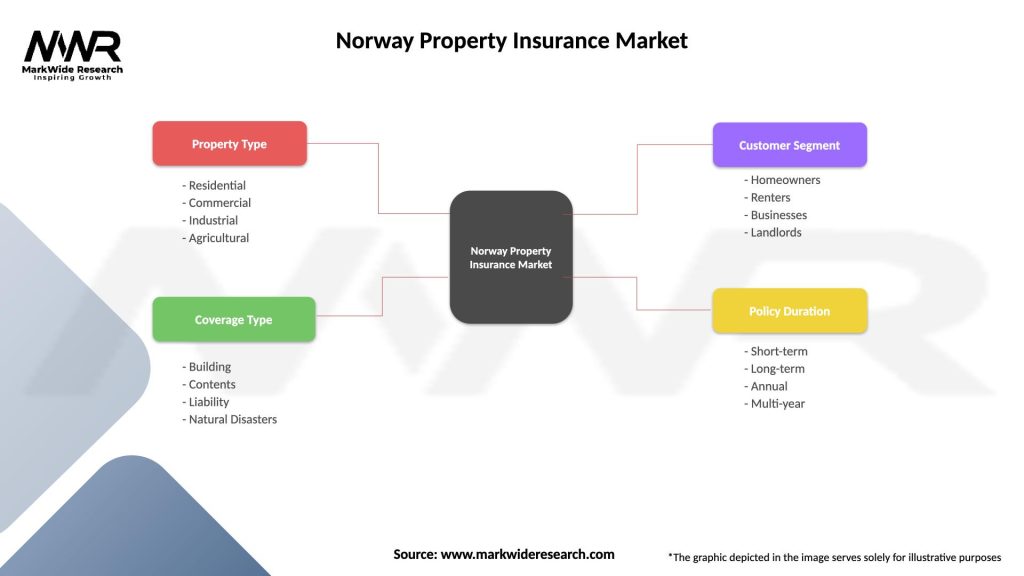

By Coverage Type: The Norwegian property insurance market segments into residential property insurance, commercial property coverage, industrial property protection, and specialized policies for unique property types such as boats, cabins, and seasonal residences.

By Customer Type: Market segmentation includes individual homeowners, landlords and property investors, small and medium enterprises, large corporations, and public sector entities, each requiring tailored coverage solutions and service approaches.

By Distribution Channel: Insurance distribution occurs through direct sales, insurance brokers, bank partnerships, online platforms, and mobile applications, with digital channels showing the strongest growth trends in recent years.

By Property Type: Coverage categories include single-family homes, apartments and condominiums, commercial buildings, industrial facilities, agricultural properties, and recreational properties, each presenting distinct risk profiles and coverage requirements.

By Risk Category: Segmentation based on risk levels includes standard risk properties, high-risk locations prone to natural disasters, premium properties requiring specialized coverage, and unique properties with customized insurance needs.

Residential Property Insurance represents the largest market segment, driven by high homeownership rates and regulatory requirements. This category shows consistent growth with increasing demand for comprehensive coverage including liability protection, temporary accommodation benefits, and personal property coverage.

Commercial Property Insurance demonstrates strong performance due to Norway’s robust business environment and regulatory compliance requirements. Commercial policies typically include business interruption coverage, equipment protection, and liability insurance, creating higher premium values per policy.

Specialized Property Coverage for cabins, boats, and seasonal properties represents a unique Norwegian market characteristic. These policies require specialized risk assessment and coverage terms, often commanding premium pricing due to increased risk factors and seasonal usage patterns.

Landlord Insurance shows growing demand as rental property investment increases in urban areas. This segment requires specialized coverage for rental-specific risks including tenant damage, rental income protection, and landlord liability coverage.

High-Value Property Insurance serves affluent Norwegian consumers with premium properties requiring specialized coverage limits and services. This segment demonstrates strong growth potential with increasing wealth concentration and luxury property development in major urban areas.

Insurance Providers benefit from Norway’s stable regulatory environment, high consumer trust levels, and strong economic fundamentals that support consistent market growth and profitability. The market offers opportunities for innovation, technology adoption, and customer relationship development.

Property Owners gain access to comprehensive protection against various risks, financial security, and peace of mind through reliable insurance coverage. Norwegian consumers benefit from competitive pricing, innovative products, and high-quality customer service standards maintained across the industry.

Financial Institutions benefit from reduced lending risks through mandatory property insurance requirements, enabling more confident mortgage lending and property financing decisions. Insurance coverage protects both lenders and borrowers from property-related financial losses.

Government and Regulators achieve consumer protection objectives while maintaining market competitiveness through effective regulatory frameworks. The insurance market contributes to economic stability and disaster resilience planning at the national level.

Technology Providers find opportunities in the growing demand for insurtech solutions, digital platforms, and innovative risk assessment technologies. The Norwegian market’s technology adoption creates opportunities for specialized service providers and technology partnerships.

Strengths:

Weaknesses:

Opportunities:

Threats:

Digital-first approaches dominate market evolution, with insurers prioritizing mobile applications, online policy management, and digital claims processing. This trend reflects Norwegian consumers’ high digital adoption rates and expectations for seamless online experiences across all service interactions.

Personalization and customization trends drive product development, with insurers offering tailored coverage options based on individual risk profiles, property characteristics, and customer preferences. Advanced data analytics enable more precise risk assessment and personalized pricing strategies.

Preventive services integration becomes increasingly important, with insurers offering risk reduction services, property monitoring solutions, and maintenance recommendations. This proactive approach helps reduce claims frequency while enhancing customer value and satisfaction levels.

Sustainability integration influences product development and business practices, with insurers developing green insurance products, supporting sustainable building practices, and incorporating environmental considerations into risk assessment and pricing models.

Partnership ecosystem development creates new value propositions through collaborations with proptech companies, construction firms, and service providers. These partnerships enable comprehensive property protection solutions extending beyond traditional insurance coverage.

Regulatory modernization initiatives continue shaping market evolution, with Norwegian authorities updating insurance regulations to accommodate technological innovation while maintaining consumer protection standards. Recent regulatory changes support insurtech adoption and digital service delivery improvements.

Technology investments by major insurers focus on artificial intelligence, machine learning, and automation solutions to enhance operational efficiency and customer service quality. MWR research indicates that leading Norwegian insurers allocate 12-15% of annual budgets to technology development and implementation.

Climate adaptation strategies become central to industry planning, with insurers developing specialized products for climate-related risks and investing in predictive modeling capabilities. These initiatives support Norway’s national climate adaptation goals while addressing evolving customer needs.

Market consolidation activities include strategic partnerships, acquisitions, and joint ventures aimed at achieving operational efficiencies and market expansion. These developments reshape competitive dynamics while creating opportunities for enhanced service delivery and innovation.

Customer experience initiatives focus on omnichannel service delivery, personalized communication, and proactive customer engagement. Leading insurers invest in customer relationship management systems and service quality improvements to maintain competitive advantages.

Technology investment priorities should focus on customer-facing digital platforms, automated claims processing, and predictive analytics capabilities. Norwegian insurers should prioritize mobile-first solutions and seamless integration across all customer touchpoints to meet evolving consumer expectations.

Product development strategies should emphasize climate-resilient coverage options, preventive services integration, and personalized policy structures. Insurers should leverage data analytics to develop more precise risk assessment capabilities and offer customized coverage solutions for diverse customer needs.

Market expansion opportunities exist through specialized coverage development for emerging property types, enhanced service offerings for high-value properties, and targeted solutions for underserved market segments. Strategic focus on niche markets can create competitive advantages and premium pricing opportunities.

Partnership development should prioritize collaborations with proptech companies, construction firms, and environmental service providers to create comprehensive property protection ecosystems. These partnerships can enhance value propositions while creating new revenue streams and customer acquisition channels.

Sustainability integration should become a core business strategy, incorporating environmental considerations into all aspects of operations from product development to claims management. This approach aligns with Norwegian values while creating differentiation opportunities in the competitive market.

Market growth prospects remain positive, supported by continued economic stability, regulatory support for innovation, and increasing consumer awareness of property protection needs. The Norwegian property insurance market is expected to maintain steady growth rates of 4-6% annually over the next five years.

Digital transformation acceleration will continue reshaping market dynamics, with artificial intelligence, IoT integration, and blockchain technologies becoming standard components of insurance operations. These technological advances will enable more efficient operations and enhanced customer experiences across the industry.

Climate adaptation focus will intensify as extreme weather events become more frequent, driving demand for specialized coverage and risk management services. Insurers will need to develop sophisticated climate risk models and innovative coverage solutions to address evolving environmental challenges.

Regulatory evolution will likely support continued market modernization while maintaining strong consumer protection standards. Future regulations may address emerging risks such as cyber threats, climate change impacts, and new property types requiring specialized coverage approaches.

Competitive landscape changes may include increased market consolidation, new entrant emergence, and strategic partnership development. MarkWide Research projections suggest that market concentration may increase slightly while maintaining healthy competition levels that benefit consumers through innovation and competitive pricing.

The Norway property insurance market represents a mature, stable, and innovative sector characterized by high consumer awareness, strong regulatory frameworks, and continuous technological advancement. Market participants benefit from Norway’s economic stability, advanced digital infrastructure, and consumer preference for comprehensive coverage solutions.

Key success factors include digital capability development, customer experience excellence, climate risk management, and innovative product development. Norwegian insurers that effectively combine traditional insurance expertise with modern technology solutions and sustainable practices will be best positioned for future growth and market leadership.

Market opportunities exist across multiple dimensions including technology integration, sustainability focus, specialized coverage development, and enhanced service delivery. The evolving risk landscape creates demand for innovative solutions while Norway’s economic strength supports continued market expansion and profitability.

Strategic priorities for market participants should emphasize customer-centric innovation, operational efficiency improvement, and proactive risk management capabilities. Success in Norway’s property insurance market requires balancing traditional insurance principles with modern customer expectations and emerging risk factors in an increasingly complex operating environment.

What is Property Insurance?

Property insurance provides financial protection against risks to property, such as fire, theft, and natural disasters. It covers various types of properties, including residential homes, commercial buildings, and personal belongings.

What are the key players in the Norway Property Insurance Market?

Key players in the Norway Property Insurance Market include Gjensidige, If P&C Insurance, and Storebrand, among others. These companies offer a range of property insurance products tailored to meet the needs of homeowners and businesses.

What are the growth factors driving the Norway Property Insurance Market?

The growth of the Norway Property Insurance Market is driven by increasing property values, a rise in natural disasters, and growing awareness of the importance of insurance coverage. Additionally, urbanization and the expansion of the real estate sector contribute to market growth.

What challenges does the Norway Property Insurance Market face?

The Norway Property Insurance Market faces challenges such as regulatory changes, increasing competition, and the impact of climate change on risk assessment. These factors can affect pricing and the availability of coverage for certain properties.

What opportunities exist in the Norway Property Insurance Market?

Opportunities in the Norway Property Insurance Market include the development of innovative insurance products, the integration of technology for better risk assessment, and the growing demand for sustainable insurance solutions. Insurers can leverage these trends to enhance customer engagement.

What trends are shaping the Norway Property Insurance Market?

Trends in the Norway Property Insurance Market include the increasing use of digital platforms for policy management, the rise of personalized insurance products, and a focus on sustainability in underwriting practices. These trends reflect changing consumer preferences and technological advancements.

Norway Property Insurance Market

| Segmentation Details | Description |

|---|---|

| Property Type | Residential, Commercial, Industrial, Agricultural |

| Coverage Type | Building, Contents, Liability, Natural Disasters |

| Customer Segment | Homeowners, Renters, Businesses, Landlords |

| Policy Duration | Short-term, Long-term, Annual, Multi-year |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Norway Property Insurance Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.