444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

Market Overview

Norway Property and Casualty Insurance Market refers to the sector that provides insurance coverage for various types of properties and liabilities in Norway. Property and casualty insurance, also known as general insurance, offers protection against losses and damages to properties such as homes, vehicles, businesses, and other assets, as well as coverage for legal liabilities arising from accidents or injuries.

Meaning

Property and casualty insurance, commonly known as P&C insurance, is a type of coverage that provides financial protection against damage or loss to property, such as homes, vehicles, and businesses, as well as liability for injuries or damages caused to others. The Norway Property and Casualty Insurance Market refers to the sector within the insurance industry that focuses on providing these types of insurance policies to individuals and businesses in Norway.

Executive Summary

The Norway Property and Casualty Insurance Market has experienced significant growth in recent years. This can be attributed to various factors, such as the increasing awareness of the importance of insurance coverage, the rising number of high-value assets, and the evolving regulatory landscape. This executive summary provides a brief overview of the market, highlighting key insights, market drivers, restraints, and opportunities.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Market Drivers

Market Restraints

Market Opportunities

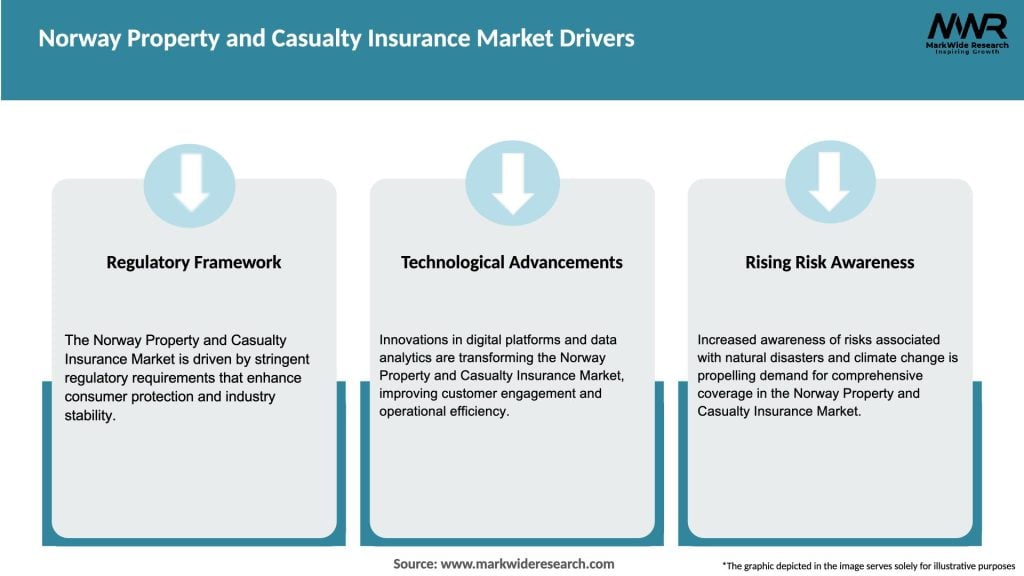

Market Dynamics

The Norway Property and Casualty Insurance Market is dynamic and influenced by various factors. These dynamics include changing customer preferences, technological advancements, regulatory developments, and macroeconomic conditions. Insurance companies need to adapt and innovate to stay competitive in this ever-evolving market landscape.

Regional Analysis

The Norway Property and Casualty Insurance Market exhibits regional variations, with certain areas experiencing higher insurance penetration than others. Urban centers, such as Oslo, Bergen, and Stavanger, have a higher concentration of insurance buyers due to the higher population density and greater asset values. However, there is potential for growth in rural areas, as insurance awareness and demand continue to rise.

Competitive Landscape

Leading Companies in Norway Property and Casualty Insurance Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

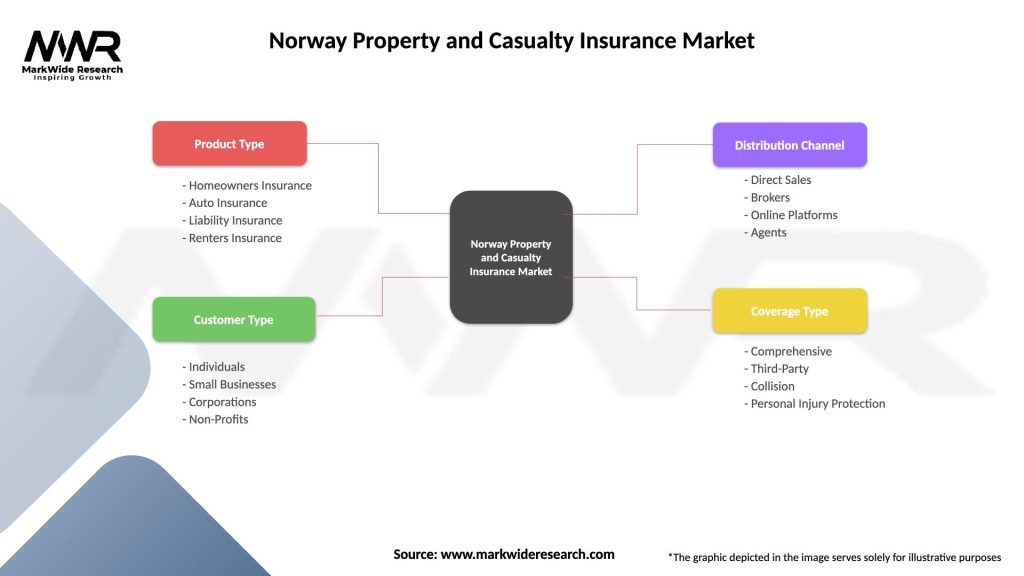

Segmentation

The Norway Property and Casualty Insurance Market can be segmented based on insurance type, including home insurance, auto insurance, commercial property insurance, liability insurance, and others. Each segment has its own unique characteristics and customer requirements, offering opportunities for insurance providers to tailor their products and services accordingly.

Category-wise Insights

Key Benefits for Industry Participants and Stakeholders

SWOT Analysis

Market Key Trends

Covid-19 Impact

The Covid-19 pandemic has had a significant impact on the Norway Property and Casualty Insurance Market. While the overall market remained resilient, there were shifts in customer behavior and insurance requirements. The pandemic highlighted the importance of coverage for business interruption, travel cancellations, and cyber risks. Insurance companies responded by introducing new policies and providing support to policyholders affected by the pandemic.

Key Industry Developments

Analyst Suggestions

Future Outlook

The future outlook for the Norway Property and Casualty Insurance Market is positive. The market is expected to continue growing due to factors such as increasing insurance awareness, evolving customer needs, and the integration of technology. Insurance companies that can adapt to the changing landscape, innovate their offerings, and provide excellent customer service will be well-positioned for success.

Conclusion

The Norway Property and Casualty Insurance Market offers significant growth potential for insurance providers. The market is driven by factors such as increasing awareness, rising natural disasters, and technological advancements. However, intense competition, regulatory challenges, and economic fluctuations pose obstacles. Insurance companies can capitalize on opportunities through innovation, expansion into untapped regions, and strategic partnerships. By embracing digital transformation, focusing on customer needs, and staying abreast of industry trends, insurance companies can navigate the market dynamics and secure a competitive advantage in the future.

What is Property and Casualty Insurance?

Property and Casualty Insurance refers to a type of insurance that provides coverage for property loss and liability for damages to others. It encompasses various policies, including homeowners, auto, and commercial insurance, protecting individuals and businesses from financial losses due to unforeseen events.

What are the key players in the Norway Property and Casualty Insurance Market?

Key players in the Norway Property and Casualty Insurance Market include Gjensidige, If P&C Insurance, and DNB Insurance. These companies offer a range of products, including personal and commercial insurance solutions, catering to diverse customer needs.

What are the growth factors driving the Norway Property and Casualty Insurance Market?

The growth of the Norway Property and Casualty Insurance Market is driven by increasing awareness of risk management, a rise in property ownership, and the growing demand for comprehensive coverage solutions. Additionally, advancements in technology are enabling insurers to offer more tailored products.

What challenges does the Norway Property and Casualty Insurance Market face?

The Norway Property and Casualty Insurance Market faces challenges such as regulatory changes, increasing competition, and the impact of climate change on risk assessment. These factors can complicate underwriting processes and affect profitability for insurers.

What opportunities exist in the Norway Property and Casualty Insurance Market?

Opportunities in the Norway Property and Casualty Insurance Market include the expansion of digital insurance solutions, the integration of artificial intelligence for claims processing, and the potential for new products addressing emerging risks. Insurers can leverage these trends to enhance customer engagement and operational efficiency.

What trends are shaping the Norway Property and Casualty Insurance Market?

Trends shaping the Norway Property and Casualty Insurance Market include the increasing adoption of insurtech solutions, a focus on sustainability in underwriting practices, and the rise of personalized insurance products. These trends reflect changing consumer preferences and the need for more flexible coverage options.

Norway Property and Casualty Insurance Market

| Segmentation Details | Description |

|---|---|

| Product Type | Homeowners Insurance, Auto Insurance, Liability Insurance, Renters Insurance |

| Customer Type | Individuals, Small Businesses, Corporations, Non-Profits |

| Distribution Channel | Direct Sales, Brokers, Online Platforms, Agents |

| Coverage Type | Comprehensive, Third-Party, Collision, Personal Injury Protection |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading Companies in Norway Property and Casualty Insurance Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.