444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The North America polycarbonate (PC) market represents a dynamic and rapidly evolving sector within the advanced materials industry, characterized by exceptional growth momentum and technological innovation. Polycarbonate materials have emerged as critical components across diverse industrial applications, from automotive manufacturing to electronics and construction sectors. The region’s market demonstrates robust expansion, driven by increasing demand for lightweight, durable, and high-performance materials that meet stringent safety and environmental standards.

Market dynamics indicate sustained growth at a CAGR of 6.8% through the forecast period, reflecting strong industrial adoption and technological advancement. North American manufacturers are increasingly leveraging polycarbonate’s unique properties, including exceptional impact resistance, optical clarity, and thermal stability, to develop innovative solutions across multiple end-use industries. The market’s resilience stems from polycarbonate’s versatility and superior performance characteristics compared to traditional materials.

Regional leadership in polycarbonate adoption is particularly evident in the United States and Canada, where advanced manufacturing capabilities and strong research infrastructure support continuous innovation. Industrial applications account for approximately 42% of total consumption, while automotive and electronics sectors represent significant growth drivers. The market’s expansion trajectory reflects broader trends toward material lightweighting, energy efficiency, and sustainable manufacturing practices across North American industries.

The North America polycarbonate market refers to the comprehensive ecosystem encompassing the production, distribution, and consumption of polycarbonate thermoplastic polymers across the United States, Canada, and Mexico. Polycarbonate (PC) represents a high-performance engineering plastic characterized by exceptional mechanical properties, optical clarity, and thermal resistance, making it indispensable for demanding industrial applications.

Market scope encompasses various polycarbonate grades and formulations, including standard, flame-retardant, glass-filled, and specialty variants designed for specific applications. Value chain participants include raw material suppliers, polycarbonate manufacturers, processors, distributors, and end-users across automotive, electronics, construction, medical, and consumer goods industries. The market’s definition extends beyond simple material supply to include technical services, application development, and sustainability initiatives.

Geographic coverage spans major industrial centers throughout North America, with concentrated activity in regions with strong automotive, electronics, and manufacturing presence. Market boundaries encompass both commodity and specialty polycarbonate segments, reflecting diverse performance requirements and application-specific needs across different industries and end-use applications.

Strategic analysis reveals the North America polycarbonate market as a high-growth sector driven by technological innovation, industrial expansion, and increasing demand for advanced materials. Market fundamentals demonstrate strong underlying demand across key end-use industries, supported by favorable regulatory environment and continuous product development initiatives. The region’s market position benefits from established manufacturing infrastructure, skilled workforce, and proximity to major consumption centers.

Key growth drivers include automotive lightweighting trends, electronics miniaturization, construction industry expansion, and increasing focus on energy-efficient materials. Automotive applications represent approximately 35% of market demand, driven by requirements for impact-resistant glazing, lightweight components, and aesthetic enhancements. Electronics sector adoption continues expanding, particularly in smartphone housings, LED lighting, and optical components where polycarbonate’s clarity and durability provide competitive advantages.

Market challenges include raw material price volatility, environmental regulations, and competition from alternative materials. However, innovation initiatives in recycling technologies, bio-based polycarbonates, and advanced processing techniques are creating new opportunities for market expansion. Regional competitiveness remains strong due to technological leadership, established supply chains, and strong customer relationships across diverse industries.

Market intelligence reveals several critical insights shaping the North America polycarbonate landscape:

Market trends indicate accelerating adoption of advanced polycarbonate formulations, with specialty grades experiencing growth rates exceeding 8% annually. Innovation focus centers on developing materials with enhanced sustainability profiles while maintaining superior performance characteristics essential for demanding applications.

Primary growth drivers propelling the North America polycarbonate market encompass diverse factors spanning technological advancement, regulatory requirements, and evolving consumer preferences. Automotive industry transformation represents the most significant driver, as manufacturers increasingly adopt polycarbonate materials to achieve lightweighting objectives while maintaining safety and performance standards.

Regulatory mandates for improved fuel efficiency and reduced emissions are accelerating polycarbonate adoption in automotive glazing, interior components, and structural applications. Weight reduction benefits of polycarbonate compared to glass and metal alternatives deliver measurable improvements in vehicle efficiency and performance. Safety enhancements provided by polycarbonate’s impact resistance and shatter-proof characteristics align with stringent automotive safety regulations.

Electronics sector expansion drives substantial demand for high-performance polycarbonate materials in consumer devices, telecommunications equipment, and industrial electronics. Miniaturization trends require materials offering exceptional dimensional stability, optical clarity, and thermal management properties. 5G infrastructure deployment creates new opportunities for specialized polycarbonate applications in antenna housings, equipment enclosures, and optical components.

Construction industry growth supports increasing polycarbonate utilization in architectural glazing, roofing systems, and building envelope applications. Energy efficiency requirements favor polycarbonate’s superior insulation properties and light transmission characteristics. Design flexibility offered by polycarbonate enables innovative architectural solutions while meeting building code requirements and sustainability objectives.

Market constraints affecting North America polycarbonate growth include several interconnected challenges that industry participants must navigate strategically. Raw material price volatility represents a persistent concern, as polycarbonate production depends on petrochemical feedstocks subject to commodity price fluctuations and supply chain disruptions.

Environmental regulations pose increasing compliance challenges, particularly regarding bisphenol A (BPA) content and end-of-life disposal requirements. Regulatory scrutiny of certain polycarbonate formulations has prompted industry investment in alternative chemistries and recycling technologies, though these transitions require significant time and resources. Sustainability pressures from customers and stakeholders demand continuous innovation in eco-friendly polycarbonate solutions.

Competition from alternative materials intensifies as other high-performance plastics and advanced composites improve their property profiles and cost competitiveness. Technological advancement in competing materials challenges polycarbonate’s traditional advantages in specific applications. Market saturation in certain mature applications limits growth potential and intensifies price competition among suppliers.

Processing complexity associated with high-performance polycarbonate grades requires specialized equipment and technical expertise, potentially limiting adoption among smaller manufacturers. Quality requirements for critical applications demand stringent manufacturing controls and quality assurance systems, increasing operational costs and complexity for market participants.

Emerging opportunities within the North America polycarbonate market present substantial potential for growth and innovation across multiple dimensions. Circular economy initiatives are creating new market segments focused on recyclable and bio-based polycarbonate materials, addressing sustainability concerns while opening additional revenue streams for industry participants.

Advanced manufacturing technologies including 3D printing and additive manufacturing are expanding polycarbonate applications into prototyping, custom components, and low-volume production scenarios. Digital transformation in manufacturing enables more precise material utilization and waste reduction, improving overall economics of polycarbonate applications. Industry 4.0 integration facilitates real-time quality monitoring and process optimization in polycarbonate processing operations.

Medical device market expansion offers significant growth potential as healthcare industry demand for biocompatible, sterilizable materials increases. Aging population demographics drive demand for medical equipment and devices utilizing polycarbonate components. Telemedicine growth creates opportunities for polycarbonate applications in remote monitoring devices and portable medical equipment.

Renewable energy sector development presents opportunities for polycarbonate applications in solar panel components, wind turbine parts, and energy storage systems. Infrastructure modernization initiatives across North America create demand for durable, weather-resistant polycarbonate materials in transportation and utility applications. Smart city development incorporates polycarbonate materials in LED lighting systems, communication infrastructure, and urban furniture applications.

Market dynamics shaping the North America polycarbonate sector reflect complex interactions between supply-side capabilities, demand-side requirements, and external environmental factors. Supply chain resilience has emerged as a critical factor following recent global disruptions, prompting industry investments in regional production capacity and diversified sourcing strategies.

Technological innovation cycles drive continuous product development, with manufacturers investing heavily in research and development to create next-generation polycarbonate materials with enhanced properties. Customer collaboration intensifies as end-users seek customized solutions for specific applications, requiring closer partnerships between polycarbonate suppliers and their customers. Application development activities focus on expanding polycarbonate utilization into new market segments and emerging technologies.

Competitive intensity varies across different market segments, with commodity grades experiencing price-based competition while specialty applications command premium pricing based on performance differentiation. Market consolidation trends reflect economies of scale requirements and the need for comprehensive product portfolios to serve diverse customer needs. Strategic partnerships between material suppliers and end-users facilitate joint development of innovative applications and market expansion initiatives.

Regulatory evolution continues influencing market dynamics as environmental standards become more stringent and safety requirements expand across different applications. Sustainability metrics increasingly influence purchasing decisions, with customers prioritizing suppliers demonstrating environmental responsibility and circular economy practices. Market responsiveness to changing regulations requires agile product development and manufacturing capabilities.

Comprehensive research approach employed for analyzing the North America polycarbonate market incorporates multiple data sources, analytical techniques, and validation methods to ensure accuracy and reliability of market insights. Primary research activities include extensive interviews with industry executives, technical specialists, and key stakeholders across the polycarbonate value chain to gather firsthand market intelligence and validate secondary research findings.

Secondary research methodology encompasses systematic analysis of industry publications, company reports, regulatory filings, and technical literature to establish market baseline data and identify emerging trends. Data triangulation techniques ensure consistency and accuracy across different information sources while identifying potential discrepancies requiring further investigation. Market modeling utilizes statistical analysis and forecasting techniques to project future market developments and quantify growth opportunities.

Industry expert consultation provides qualitative insights into market dynamics, competitive positioning, and technology trends that complement quantitative analysis. Supply chain analysis examines raw material availability, production capacity, and distribution networks to assess market supply-demand balance. End-user surveys capture customer preferences, application requirements, and purchasing criteria across different market segments.

Validation processes include cross-referencing multiple data sources, conducting follow-up interviews with key informants, and reviewing findings with industry advisory panels. Analytical rigor ensures research conclusions are supported by robust evidence and reflect actual market conditions rather than theoretical projections. Continuous monitoring of market developments enables real-time updates to research findings and maintains relevance of market intelligence.

United States market dominates North America polycarbonate consumption, accounting for approximately 68% of regional demand, driven by strong automotive, electronics, and construction industries. Manufacturing concentration in the Midwest and Southeast regions benefits from proximity to automotive production centers and established chemical industry infrastructure. Innovation hubs in California and the Northeast drive development of advanced polycarbonate applications in electronics and medical devices.

Canadian market represents approximately 22% of regional consumption, with strong demand from automotive, aerospace, and natural resource industries. Resource availability and established petrochemical infrastructure support domestic polycarbonate production capabilities. Environmental leadership in sustainability initiatives influences market development toward eco-friendly polycarbonate solutions and circular economy practices.

Mexican market shows rapid growth at 8.5% annually, driven by expanding automotive manufacturing and electronics assembly operations. Manufacturing migration from other regions creates new demand centers for polycarbonate materials and processing capabilities. Trade relationships within NAFTA/USMCA framework facilitate regional supply chain integration and market development.

Regional integration strengthens through cross-border supply chains, joint ventures, and technology sharing arrangements among North American polycarbonate industry participants. Competitive advantages of regional production include reduced transportation costs, shorter lead times, and enhanced customer service capabilities. Market development initiatives focus on expanding applications and improving material performance to maintain competitive positioning against global suppliers.

Market leadership in the North America polycarbonate sector is characterized by a mix of global chemical companies and regional specialists, each bringing distinct capabilities and market positioning strategies. Competitive dynamics reflect the industry’s capital-intensive nature and the importance of technological innovation in maintaining market position.

Competitive strategies emphasize product differentiation, technical service capabilities, and sustainable manufacturing practices. Innovation investments focus on developing next-generation polycarbonate materials with enhanced properties and environmental profiles. Market positioning varies from commodity suppliers emphasizing cost competitiveness to specialty producers commanding premium pricing through performance differentiation.

Strategic partnerships between polycarbonate suppliers and major end-users facilitate joint development of innovative applications and long-term supply relationships. Capacity expansion initiatives reflect confidence in long-term market growth and the need to maintain competitive supply capabilities.

Market segmentation analysis reveals distinct patterns of demand and growth across different polycarbonate categories, applications, and end-use industries. Product segmentation encompasses various polycarbonate grades and formulations designed for specific performance requirements and application needs.

By Product Type:

By Application:

Geographic distribution shows concentration in industrial regions with strong automotive and electronics manufacturing presence. End-use segmentation reflects diverse application requirements and varying growth rates across different industries and market segments.

Automotive segment represents the largest polycarbonate application category, driven by industry trends toward lightweighting and improved safety performance. Glazing applications show particularly strong growth as automotive manufacturers adopt polycarbonate alternatives to traditional glass for weight reduction and design flexibility. Interior components utilize polycarbonate’s aesthetic properties and processing versatility to create innovative cabin designs and functional elements.

Electronics category demonstrates rapid expansion, with smartphone housings and consumer device applications driving substantial volume growth. LED lighting applications benefit from polycarbonate’s optical clarity and thermal management properties. 5G infrastructure development creates new opportunities for specialized polycarbonate grades in telecommunications equipment and antenna systems.

Construction applications show steady growth driven by architectural glazing and building envelope systems. Energy efficiency requirements favor polycarbonate’s insulation properties and light transmission characteristics. Hurricane-resistant glazing represents a growing niche market in coastal regions, leveraging polycarbonate’s impact resistance and safety benefits.

Medical device segment exhibits strong growth potential as healthcare industry demand for biocompatible materials increases. Sterilization resistance and optical clarity make polycarbonate ideal for medical equipment housings and disposable components. Regulatory compliance requirements drive demand for specialized medical-grade polycarbonate formulations with documented biocompatibility and performance characteristics.

Material suppliers benefit from diverse market opportunities across multiple end-use industries, providing revenue stability and growth potential. Product differentiation capabilities enable premium pricing for specialty grades while commodity applications provide volume base. Technical service offerings create additional value streams and strengthen customer relationships through application development support.

End-user manufacturers gain access to high-performance materials enabling product innovation and competitive differentiation. Weight reduction benefits in automotive applications translate directly to improved fuel efficiency and regulatory compliance. Design flexibility offered by polycarbonate processing characteristics enables innovative product designs and manufacturing efficiency improvements.

Supply chain participants including distributors and processors benefit from growing market demand and expanding application opportunities. Value-added services such as custom compounding and fabrication create additional revenue streams and customer loyalty. Regional supply chain advantages provide competitive positioning against global competitors through reduced lead times and enhanced service capabilities.

Technology developers find opportunities in advancing polycarbonate formulations, processing technologies, and recycling solutions. Sustainability initiatives create new market segments and competitive advantages for innovative solutions. Application development activities expand market potential and create new revenue opportunities across diverse industries.

Investors and stakeholders benefit from market growth potential and the industry’s resilience across economic cycles. Diversified end-use markets provide risk mitigation and stable returns. Innovation focus supports long-term competitive positioning and market leadership opportunities in emerging applications and technologies.

Strengths:

Weaknesses:

Opportunities:

Threats:

Sustainability transformation represents the most significant trend reshaping the North America polycarbonate market, with industry participants investing heavily in circular economy solutions and bio-based alternatives. Recycling technology advancement enables mechanical and chemical recycling of polycarbonate materials, addressing environmental concerns while creating new business opportunities. Life cycle assessment integration into product development processes ensures environmental considerations are embedded throughout the value chain.

Digital transformation accelerates across polycarbonate manufacturing and processing operations, with Industry 4.0 technologies enabling real-time monitoring, predictive maintenance, and quality optimization. Artificial intelligence applications in material formulation and process control improve efficiency and reduce waste. Digital twin technology facilitates virtual testing and optimization of polycarbonate applications before physical implementation.

Customization demand increases as end-users seek tailored polycarbonate solutions for specific applications and performance requirements. Co-development partnerships between suppliers and customers intensify to create innovative materials and applications. Rapid prototyping capabilities using 3D printing and additive manufacturing enable faster product development cycles and reduced time-to-market.

Supply chain regionalization trends reflect efforts to reduce dependency on global supply chains and improve resilience against disruptions. Near-shoring initiatives bring production closer to end-use markets, reducing transportation costs and lead times. Strategic partnerships within North America strengthen regional supply chain capabilities and competitive positioning.

Performance enhancement continues through development of advanced polycarbonate grades with improved properties such as enhanced UV resistance, better chemical compatibility, and superior processing characteristics. Nanotechnology integration enables creation of polycarbonate nanocomposites with unique properties for specialized applications.

Capacity expansion projects across North America reflect industry confidence in long-term market growth and the need to meet increasing demand. Manufacturing investments focus on advanced production technologies that improve efficiency, reduce environmental impact, and enable production of specialty polycarbonate grades. Facility modernization initiatives incorporate digital technologies and automation to enhance operational performance.

Strategic acquisitions and partnerships reshape the competitive landscape as companies seek to expand capabilities, access new technologies, and strengthen market positions. Vertical integration moves by major players aim to secure raw material supply and capture additional value chain margins. Technology licensing agreements facilitate knowledge transfer and accelerate innovation across the industry.

Product launches of next-generation polycarbonate materials address evolving customer needs and emerging applications. Sustainable product lines incorporate recycled content and bio-based components to meet environmental requirements. Application-specific grades target high-growth market segments such as automotive glazing, medical devices, and electronics.

Research collaborations between industry participants and academic institutions advance fundamental understanding of polycarbonate chemistry and processing. Government partnerships support development of sustainable materials and manufacturing technologies. Industry consortiums address common challenges such as recycling infrastructure and standardization of sustainable practices.

Regulatory developments influence product formulations and manufacturing processes as environmental standards evolve. Certification programs for sustainable polycarbonate materials provide market differentiation and customer assurance. Standards development activities establish performance benchmarks and testing protocols for emerging applications.

Strategic recommendations for North America polycarbonate market participants emphasize the importance of balancing growth opportunities with sustainability requirements and competitive pressures. MarkWide Research analysis suggests that companies should prioritize investment in sustainable technologies and circular economy solutions to maintain long-term competitiveness and regulatory compliance.

Innovation focus should center on developing next-generation polycarbonate materials that combine superior performance with environmental responsibility. Research and development investments in bio-based feedstocks, advanced recycling technologies, and specialty formulations will create competitive differentiation and new market opportunities. Customer collaboration in application development ensures that innovation efforts align with market needs and create mutual value.

Supply chain optimization requires careful balance between cost efficiency and resilience, with emphasis on regional sourcing and strategic partnerships. Capacity planning should consider both current demand and future growth projections while maintaining flexibility to adapt to changing market conditions. Digital transformation investments will improve operational efficiency and enable data-driven decision making.

Market positioning strategies should emphasize unique value propositions and technical capabilities rather than competing solely on price. Specialty applications offer higher margins and growth potential compared to commodity markets. Geographic expansion within North America can capture growth in emerging markets and applications while leveraging existing infrastructure and capabilities.

Sustainability leadership will become increasingly important for market success as customers and regulators demand environmental responsibility. Circular economy initiatives should be integrated into business strategy rather than treated as compliance requirements. Stakeholder engagement across the value chain will facilitate collaborative solutions to sustainability challenges and market development opportunities.

Long-term prospects for the North America polycarbonate market remain highly favorable, supported by continued industrial growth, technological advancement, and expanding applications across diverse end-use sectors. Market evolution will be characterized by increasing sophistication in material properties, processing technologies, and sustainability practices. Growth trajectory is expected to maintain momentum at 6.2% CAGR through the next decade, driven by automotive lightweighting, electronics innovation, and construction industry expansion.

Technology advancement will continue driving market development through improved polycarbonate formulations, processing efficiency, and recycling capabilities. Artificial intelligence and machine learning applications will optimize material design and manufacturing processes. Nanotechnology integration will enable development of polycarbonate materials with unprecedented property combinations and performance characteristics.

Sustainability transformation will accelerate as circular economy principles become mainstream business practices. Bio-based polycarbonates are expected to achieve commercial viability and significant market penetration within the forecast period. Recycling infrastructure development will support closed-loop material flows and reduce environmental impact while creating new business opportunities.

Application expansion into emerging technologies such as autonomous vehicles, renewable energy systems, and advanced medical devices will create substantial new demand. Smart materials incorporating sensors and connectivity features will open entirely new market segments. Additive manufacturing applications will enable customized solutions and distributed production models.

Regional integration within North America will strengthen through continued trade relationships and supply chain optimization. Competitive positioning will increasingly depend on innovation capabilities, sustainability leadership, and customer partnership strength rather than traditional cost advantages. Market maturation will favor companies with comprehensive portfolios, technical expertise, and strong customer relationships across multiple end-use industries.

North America polycarbonate market represents a dynamic and resilient sector positioned for sustained growth and continued innovation. Market fundamentals remain strong, supported by diverse end-use applications, technological advancement, and favorable industry trends toward lightweighting and high-performance materials. The region’s competitive advantages in manufacturing infrastructure, technical expertise, and customer proximity provide solid foundation for long-term market leadership.

Industry transformation toward sustainability and circular economy principles creates both challenges and opportunities for market participants. Successful companies will be those that embrace innovation, invest in sustainable technologies, and develop strong partnerships across the value chain. Market evolution will favor participants with comprehensive capabilities spanning material science, application development, and customer service excellence.

Future success in the North America polycarbonate market will depend on balancing growth ambitions with environmental responsibility, maintaining technological leadership while managing costs, and serving diverse customer needs while building sustainable competitive advantages. Strategic focus on innovation, sustainability, and customer partnership will determine market leadership in this evolving and opportunity-rich sector.

What is Polycarbonate?

Polycarbonate is a durable thermoplastic known for its high impact resistance and optical clarity. It is widely used in applications such as eyewear lenses, automotive components, and electronic devices.

What are the key players in the North America Polycarbonate (PC) Market?

Key players in the North America Polycarbonate (PC) Market include Covestro AG, SABIC, and Teijin Limited, among others. These companies are known for their innovative products and extensive distribution networks.

What are the growth factors driving the North America Polycarbonate (PC) Market?

The North America Polycarbonate (PC) Market is driven by increasing demand from the automotive and electronics industries, as well as the growing need for lightweight and durable materials in construction applications.

What challenges does the North America Polycarbonate (PC) Market face?

Challenges in the North America Polycarbonate (PC) Market include fluctuating raw material prices and environmental concerns related to plastic waste. These factors can impact production costs and regulatory compliance.

What opportunities exist in the North America Polycarbonate (PC) Market?

Opportunities in the North America Polycarbonate (PC) Market include the development of bio-based polycarbonate materials and advancements in recycling technologies. These innovations can enhance sustainability and reduce environmental impact.

What trends are shaping the North America Polycarbonate (PC) Market?

Trends in the North America Polycarbonate (PC) Market include the increasing use of polycarbonate in smart devices and the automotive sector, as well as a shift towards more sustainable production methods. These trends reflect changing consumer preferences and regulatory pressures.

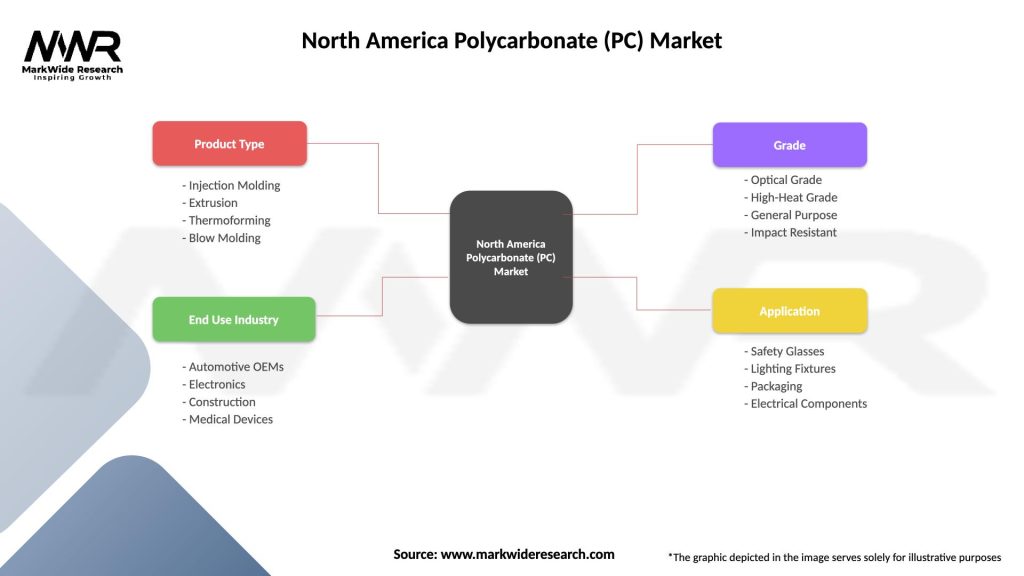

North America Polycarbonate (PC) Market

| Segmentation Details | Description |

|---|---|

| Product Type | Injection Molding, Extrusion, Thermoforming, Blow Molding |

| End Use Industry | Automotive OEMs, Electronics, Construction, Medical Devices |

| Grade | Optical Grade, High-Heat Grade, General Purpose, Impact Resistant |

| Application | Safety Glasses, Lighting Fixtures, Packaging, Electrical Components |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the North America Polycarbonate (PC) Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.