The North America Pipeline Construction Market plays a pivotal role in the region’s energy infrastructure, facilitating the transportation of oil, natural gas, and other petroleum products across vast distances. With the abundance of energy resources in North America and the need to transport them efficiently, the pipeline construction market has experienced significant growth and evolution over the years, contributing to the region’s economic development and energy security.

Meaning

The North America Pipeline Construction Market encompasses the planning, design, engineering, and construction of pipelines for the transportation of oil, natural gas, refined petroleum products, and other fluids. It involves various stakeholders, including pipeline operators, construction companies, engineering firms, regulatory agencies, and landowners. Pipeline construction projects range from small gathering lines to large transmission pipelines spanning hundreds of miles.

Executive Summary

The North America Pipeline Construction Market is driven by the region’s vast energy reserves, increasing demand for reliable energy transportation infrastructure, and ongoing pipeline replacement and expansion projects. Despite regulatory and environmental challenges, the market presents lucrative opportunities for industry participants to capitalize on the region’s energy boom and address evolving energy transportation needs.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Abundant Energy Resources: North America boasts abundant energy resources, including shale oil, natural gas, and tar sands, driving the need for extensive pipeline infrastructure to transport these resources from production areas to refineries, processing plants, and end markets.

Technological Advancements: Technological advancements in pipeline construction techniques, materials, and monitoring systems improve safety, efficiency, and environmental performance in the North America Pipeline Construction Market. Innovations such as horizontal directional drilling, trenchless construction methods, and advanced coating technologies enhance pipeline integrity and longevity.

Environmental and Regulatory Considerations: Environmental and regulatory considerations play a significant role in shaping the North America Pipeline Construction Market. Pipeline projects must adhere to stringent environmental regulations, obtain permits, conduct environmental assessments, and engage with stakeholders to address concerns related to land use, water quality, and wildlife habitat protection.

Economic and Geopolitical Factors: Economic factors, geopolitical dynamics, and energy market trends influence investment decisions and project timelines in the North America Pipeline Construction Market. Factors such as commodity prices, regulatory policies, trade agreements, and geopolitical tensions impact the viability and profitability of pipeline projects.

Market Drivers

Growing Energy Demand: The growing demand for energy resources in North America and global markets drives investments in pipeline construction to transport oil, natural gas, and petroleum products from production areas to consumption centers, power plants, and industrial facilities.

Infrastructure Modernization: Aging pipeline infrastructure, deteriorating assets, and the need for modernization and safety upgrades stimulate demand for pipeline construction services in North America. Replacement projects, integrity management programs, and capacity expansion initiatives support market growth.

Energy Independence and Security: Efforts to enhance energy independence, reduce reliance on foreign imports, and strengthen energy security drive investments in domestic pipeline infrastructure in North America. Pipelines play a critical role in transporting domestically produced energy resources to reduce dependence on overseas suppliers.

Environmental Considerations: Environmental considerations, including greenhouse gas emissions, carbon footprint, and air and water quality impacts, influence the choice of pipeline routes, construction methods, and mitigation measures in North America. Companies prioritize environmental stewardship and sustainability in pipeline construction projects.

Market Restraints

Regulatory Challenges: Regulatory challenges, permitting delays, and legal disputes pose obstacles to pipeline construction projects in North America. Regulatory uncertainty, public opposition, and litigation risk can prolong project timelines, increase costs, and deter investment in new pipeline infrastructure.

Environmental Opposition: Environmental opposition, indigenous rights concerns, and grassroots activism against fossil fuel development and pipeline construction projects pose challenges to industry stakeholders in North America. Protests, blockades, and legal challenges disrupt project planning, construction activities, and social license to operate.

Public Safety and Risk Management: Public safety considerations, risk management practices, and emergency response planning are paramount in pipeline construction projects in North America. Accidents, spills, and incidents have significant financial, reputational, and regulatory implications for pipeline operators and construction companies.

Market Volatility: Market volatility, commodity price fluctuations, and economic uncertainty impact investment decisions and project financing in the North America Pipeline Construction Market. Uncertain market conditions, regulatory changes, and geopolitical events can affect project economics and investor confidence.

Market Opportunities

Expansion of Oil and Gas Infrastructure: The expansion of oil and gas infrastructure, including pipelines, storage facilities, and terminals, presents opportunities for pipeline construction companies in North America. Projects to connect emerging production areas with existing infrastructure and export terminals drive market growth.

Renewable Energy Integration: The transition to renewable energy sources, including wind, solar, and hydroelectric power, requires new transmission lines and interconnections to the grid in North America. Pipeline construction companies diversify into renewable energy infrastructure projects, such as hydrogen pipelines and carbon capture and storage (CCS) networks.

Technology Adoption and Innovation: Technology adoption and innovation, including digitalization, automation, and robotics, enhance productivity, safety, and project execution in the North America Pipeline Construction Market. Companies invest in smart pipeline technologies, remote monitoring systems, and predictive analytics to optimize operations and maintenance.

Economic Recovery and Infrastructure Investment: Economic recovery initiatives, infrastructure stimulus packages, and government funding programs support investments in critical infrastructure projects, including pipeline construction, across North America. Public-private partnerships and infrastructure investment trusts (REITs) finance pipeline development and modernization efforts.

Market Dynamics

The North America Pipeline Construction Market operates within a dynamic environment shaped by economic, political, regulatory, and technological factors. Market dynamics such as energy demand trends, infrastructure investment cycles, regulatory developments, and stakeholder engagement influence project planning, execution, and outcomes in the region.

Regional Analysis

The North America Pipeline Construction Market exhibits regional variations in project activity, market dynamics, and regulatory frameworks across the United States, Canada, and Mexico. Each country has unique energy infrastructure needs, resource endowments, environmental considerations, and socio-economic factors that influence pipeline construction trends and investment priorities.

United States: The United States leads the North America Pipeline Construction Market, with extensive networks of oil, natural gas, and liquids pipelines crisscrossing the country. Shale plays, including the Permian Basin, Bakken Formation, and Marcellus-Utica region, drive pipeline development and expansion projects to connect production areas with refining hubs, export terminals, and demand centers.

Canada: Canada is a major player in the North America Pipeline Construction Market, with vast reserves of oil sands, conventional oil, and natural gas resources. Pipeline projects, such as the Trans Mountain Expansion, Keystone XL, and Line 3 Replacement, face regulatory hurdles, indigenous consultation requirements, and environmental opposition, impacting project timelines and investment decisions.

Mexico: Mexico’s energy reform policies, including privatization of the oil and gas sector, attract investment in pipeline infrastructure projects to modernize and expand the country’s energy transportation network. Projects such as the Los Ramones Pipeline System and the Texas-Mexico natural gas pipelines enhance cross-border connectivity and support Mexico’s energy security objectives.

Competitive Landscape

Leading Companies in North America Pipeline Construction Market:

Bechtel Corporation

TransCanada Corporation (TC Energy)

Kinder Morgan, Inc.

Enbridge Inc.

Michels Corporation

Precision Pipeline, LLC

Pumpco, Inc. (A Subsidiary of Emcor Group)

MasTec, Inc.

Primoris Services Corporation

Quanta Services, Inc.

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

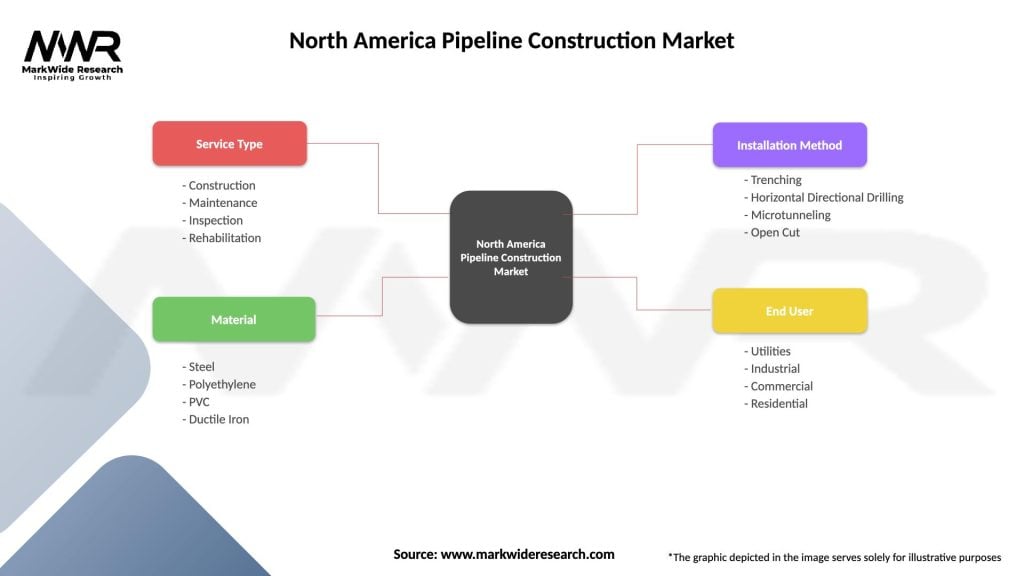

Segmentation

The North America Pipeline Construction Market can be segmented based on various factors, including:

Pipeline Type: Segmentation by pipeline type includes crude oil pipelines, natural gas pipelines, refined products pipelines, water pipelines, and specialty pipelines for chemicals, CO2, and hydrogen transportation.

Project Size: Segmentation by project size includes small diameter pipelines (gathering lines, distribution lines), medium diameter pipelines (interstate pipelines, regional pipelines), and large diameter pipelines (transmission pipelines, export pipelines).

Geography: Segmentation by geography includes regional markets such as the United States, Canada, Mexico, and specific states or provinces with unique pipeline construction trends and regulatory frameworks.

Application: Segmentation by application includes upstream pipelines (from wellhead to processing facilities), midstream pipelines (from processing plants to storage terminals), and downstream pipelines (from refineries to end users).

Segmentation provides insights into market dynamics, project characteristics, and customer requirements, enabling companies to tailor their strategies, products, and services to specific market segments and customer needs.

Category-wise Insights

Crude Oil Pipelines: Crude oil pipelines are a key segment of the North America Pipeline Construction Market, transporting crude oil from production areas to refineries, export terminals, and storage facilities. Projects such as the Keystone XL Pipeline, Dakota Access Pipeline, and Permian Highway Pipeline cater to growing crude oil production and export demand.

Natural Gas Pipelines: Natural gas pipelines play a vital role in the North America energy infrastructure, delivering natural gas from production basins to power plants, industrial facilities, and residential consumers. Projects such as the Atlantic Coast Pipeline, Mountain Valley Pipeline, and LNG export terminals support natural gas supply reliability and market expansion.

Water and Wastewater Pipelines: Water and wastewater pipelines address water resource management, irrigation, municipal water supply, and wastewater treatment needs in North America. Projects such as water transfer pipelines, desalination plants, and sewage conveyance systems enhance water security and environmental sustainability.

Specialty Pipelines: Specialty pipelines cater to specific market niches and applications, including chemical pipelines, CO2 pipelines for enhanced oil recovery (EOR), hydrogen pipelines for fuel cell vehicles, and geothermal pipelines for renewable energy generation. Emerging technologies and sustainability initiatives drive demand for specialty pipeline construction projects.

Key Benefits for Industry Participants and Stakeholders

The North America Pipeline Construction Market offers several benefits for industry participants and stakeholders:

Energy Security: Pipeline construction enhances energy security by providing reliable transportation infrastructure for domestically produced oil, natural gas, and petroleum products, reducing dependence on foreign imports and volatile global markets.

Economic Growth: Pipeline construction projects stimulate economic growth, create jobs, and generate investment opportunities across the supply chain, including engineering, construction, manufacturing, and support services, contributing to regional development and prosperity.

Infrastructure Resilience: Pipeline infrastructure enhances infrastructure resilience, disaster response capabilities, and emergency preparedness by ensuring continuous energy supply, fuel availability, and critical infrastructure connectivity during emergencies and natural disasters.

Environmental Stewardship: Pipeline operators prioritize environmental stewardship, safety, and sustainability in pipeline construction and operations, implementing best practices, technology solutions, and risk management measures to protect ecosystems, water resources, and air quality.

SWOT Analysis

A SWOT analysis of the North America Pipeline Construction Market provides insights into its strengths, weaknesses, opportunities, and threats:

Strengths:

Extensive pipeline network and infrastructure

Abundant energy resources and reserves

Technological expertise and innovation capabilities

Economic contributions and job creation

Weaknesses:

Regulatory hurdles and permitting delays

Environmental opposition and public resistance

Infrastructure vulnerabilities and safety risks

Market volatility and commodity price fluctuations

Opportunities:

Expansion of pipeline infrastructure

Renewable energy integration and diversification

Technology adoption and digital transformation

Economic recovery and infrastructure investment

Threats:

Regulatory uncertainty and policy changes

Environmental litigation and social activism

Geopolitical tensions and trade disputes

Energy market shifts and disruptive technologies

Understanding these factors helps industry stakeholders identify strategic priorities, mitigate risks, and capitalize on growth opportunities in the North America Pipeline Construction Market.

Market Key Trends

Digitalization and Automation: Digitalization and automation technologies, including digital twins, remote monitoring systems, and predictive analytics, optimize pipeline operations, maintenance, and asset management, enhancing safety, efficiency, and reliability.

Decarbonization and Energy Transition: Decarbonization initiatives, renewable energy mandates, and clean energy policies drive investments in low-carbon technologies, hydrogen infrastructure, and carbon capture and storage (CCS) projects, reshaping the energy landscape and pipeline market dynamics.

Infrastructure Resilience and Security: Infrastructure resilience and security measures, including cybersecurity protocols, physical asset protection, and risk mitigation strategies, safeguard critical infrastructure assets, prevent disruptions, and ensure continuous energy supply in the face of emerging threats and vulnerabilities.

Stakeholder Engagement and Social License: Stakeholder engagement, community outreach, and Indigenous consultation efforts foster trust, collaboration, and social license to operate for pipeline projects, addressing environmental, social, and governance (ESG) considerations and enhancing project acceptance and viability.

Covid-19 Impact

The Covid-19 pandemic has had a mixed impact on the North America Pipeline Construction Market, with short-term disruptions and long-term implications for energy demand, project economics, and regulatory dynamics:

Supply Chain Disruptions: The Covid-19 pandemic disrupted global supply chains, affecting the availability of materials, equipment, and skilled labor for pipeline construction projects in North America, leading to project delays and cost overruns.

Demand Fluctuations: The pandemic-induced economic slowdown, travel restrictions, and lockdown measures reduced energy demand, affecting oil and gas prices, drilling activity, and investment decisions in North America, impacting the pace and scale of pipeline development.

Regulatory Challenges: The Covid-19 pandemic intensified regulatory challenges, permitting delays, and legal uncertainties for pipeline projects in North America, as stakeholders grappled with public health concerns, social distancing requirements, and remote engagement processes.

Long-Term Resilience: Despite short-term disruptions, the North America Pipeline Construction Market demonstrated long-term resilience and adaptability, with pipeline operators implementing safety protocols, contingency plans, and remote work arrangements to ensure project continuity and operational continuity.

Key Industry Developments

Economic Recovery Initiatives: Economic recovery initiatives, infrastructure stimulus packages, and government funding programs support investments in critical infrastructure projects, including pipeline construction, across North America, stimulating job creation, economic growth, and industry recovery.

Renewable Energy Integration: Renewable energy integration projects, such as hydrogen pipelines, offshore wind transmission lines, and renewable natural gas (RNG) pipelines, complement traditional oil and gas infrastructure, diversifying revenue streams and addressing sustainability goals in North America.

Energy Transition Strategies: Energy transition strategies, including electrification, decarbonization, and circular economy initiatives, drive investments in clean energy technologies, grid modernization, and energy storage infrastructure, shaping the future landscape of the North America Pipeline Construction Market.

Innovation and Collaboration: Innovation hubs, technology accelerators, and industry collaborations facilitate knowledge sharing, technology transfer, and innovation diffusion in the North America Pipeline Construction Market, accelerating the adoption of digitalization, automation, and sustainability solutions.

Analyst Suggestions

Diversification and Innovation: Pipeline construction companies should diversify into emerging markets, renewable energy sectors, and technology-driven solutions to mitigate risks, capture new growth opportunities, and enhance competitiveness in the evolving North America Pipeline Construction Market.

Regulatory Compliance and ESG Focus: Companies need to prioritize regulatory compliance, environmental stewardship, and social responsibility in pipeline construction projects, engaging with regulators, communities, and stakeholders to address ESG considerations and secure project approvals.

Risk Management and Resilience: Robust risk management practices, contingency planning, and resilience strategies are essential for pipeline operators and construction companies to navigate uncertainties, disruptions, and emergencies in the North America Pipeline Construction Market effectively.

Collaboration and Partnerships: Collaboration among industry stakeholders, government agencies, research institutions, and technology providers fosters innovation, knowledge exchange, and capacity building in the North America Pipeline Construction Market, driving collective action and industry transformation.

Future Outlook

The future outlook for the North America Pipeline Construction Market is influenced by various factors, including energy market trends, regulatory developments, technological advancements, and societal expectations:

Energy Market Dynamics: Energy market dynamics, including oil and gas prices, production trends, supply-demand balance, and geopolitical risks, will shape investment decisions, project economics, and market competitiveness in the North America Pipeline Construction Market.

Regulatory Environment: The regulatory environment, including environmental regulations, permitting requirements, indigenous consultation processes, and social license considerations, will impact the pace and scale of pipeline construction projects in North America, influencing market dynamics and industry behavior.

Technology Adoption: Technology adoption trends, including digitalization, automation, data analytics, and artificial intelligence, will drive innovation, efficiency gains, and operational excellence in the North America Pipeline Construction Market, transforming project delivery and asset management practices.

Sustainability Imperative: The sustainability imperative, including climate change mitigation, carbon reduction goals, and ESG commitments, will drive investments in low-carbon technologies, renewable energy infrastructure, and circular economy solutions, reshaping the energy landscape and pipeline market dynamics.

Conclusion

The North America Pipeline Construction Market plays a vital role in the region’s energy infrastructure, providing essential transportation infrastructure for oil, natural gas, and petroleum products. Despite regulatory challenges, environmental opposition, and market volatility, the pipeline construction industry demonstrates resilience, adaptability, and innovation in meeting evolving energy transportation needs.

By embracing technology, sustainability, and collaboration, pipeline construction companies can navigate market uncertainties, capture growth opportunities, and contribute to the region’s energy security, economic prosperity, and environmental stewardship. With a focus on regulatory compliance, risk management, and stakeholder engagement, the North America Pipeline Construction Market can sustainably meet the energy demands of the future while addressing societal expectations and advancing the transition to a low-carbon economy.

What is Pipeline Construction?

Pipeline construction involves the process of building pipelines for transporting various substances, including oil, gas, and water. This sector is crucial for energy distribution and infrastructure development.

What are the key players in the North America Pipeline Construction Market?

Key players in the North America Pipeline Construction Market include companies like Bechtel, Kinder Morgan, and TransCanada, which are involved in various pipeline projects and infrastructure development, among others.

What are the main drivers of the North America Pipeline Construction Market?

The main drivers of the North America Pipeline Construction Market include the increasing demand for energy, the need for infrastructure upgrades, and the expansion of natural gas distribution networks. These factors contribute to the growth of pipeline projects across the region.

What challenges does the North America Pipeline Construction Market face?

The North America Pipeline Construction Market faces challenges such as regulatory hurdles, environmental concerns, and public opposition to new projects. These factors can delay construction timelines and increase costs.

What opportunities exist in the North America Pipeline Construction Market?

Opportunities in the North America Pipeline Construction Market include advancements in technology for safer and more efficient construction methods, as well as the potential for new projects driven by renewable energy initiatives. These trends can lead to increased investment in pipeline infrastructure.

What trends are shaping the North America Pipeline Construction Market?

Trends shaping the North America Pipeline Construction Market include the integration of digital technologies for project management, a focus on sustainability practices, and the growing importance of pipeline safety measures. These trends are influencing how companies approach pipeline construction.

Leading Companies in North America Pipeline Construction Market:

Bechtel Corporation

TransCanada Corporation (TC Energy)

Kinder Morgan, Inc.

Enbridge Inc.

Michels Corporation

Precision Pipeline, LLC

Pumpco, Inc. (A Subsidiary of Emcor Group)

MasTec, Inc.

Primoris Services Corporation

Quanta Services, Inc.

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.