444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The North America LiDAR service market represents a rapidly expanding sector within the geospatial technology industry, driven by increasing demand for high-precision mapping and surveying solutions across multiple industries. LiDAR technology has emerged as a critical component in applications ranging from autonomous vehicle development to infrastructure planning, environmental monitoring, and urban development projects. The market encompasses various service offerings including aerial LiDAR surveys, terrestrial scanning services, mobile mapping solutions, and specialized data processing and analysis services.

Market dynamics indicate robust growth potential, with the sector experiencing a compound annual growth rate (CAGR) of approximately 12.8% over the forecast period. This growth trajectory is supported by technological advancements in laser scanning technology, decreasing equipment costs, and expanding applications across diverse industry verticals. The integration of artificial intelligence and machine learning capabilities into LiDAR data processing workflows has significantly enhanced the value proposition of these services.

Regional distribution shows the United States commanding approximately 78% market share, followed by Canada with substantial growth in mining and forestry applications. The market benefits from strong government support for infrastructure modernization initiatives and increasing adoption of digital twin technologies in smart city development projects.

The North America LiDAR service market refers to the comprehensive ecosystem of professional services that utilize Light Detection and Ranging technology to capture, process, and analyze three-dimensional spatial data for various commercial, industrial, and governmental applications across the United States and Canada.

LiDAR services encompass multiple specialized offerings that transform raw laser scanning data into actionable intelligence for decision-making processes. These services include data acquisition through various platforms such as aircraft, drones, vehicles, and stationary equipment, followed by sophisticated data processing, analysis, and visualization services. The market includes both hardware-as-a-service models and comprehensive turnkey solutions that deliver processed geospatial intelligence to end users.

Service providers in this market range from specialized geospatial companies to large engineering consultancies that have integrated LiDAR capabilities into their broader service portfolios. The market also includes emerging technology companies that focus on specific applications such as autonomous vehicle mapping, precision agriculture, or environmental monitoring services.

Market leadership in the North America LiDAR service sector is characterized by a diverse ecosystem of established surveying companies, technology innovators, and specialized service providers. The market has demonstrated remarkable resilience and growth, particularly accelerated by increased demand for contactless surveying solutions and digital transformation initiatives across multiple industries.

Key growth drivers include the rapid expansion of autonomous vehicle testing programs, which account for approximately 23% of total service demand, along with increasing infrastructure investment and smart city initiatives. The construction and engineering sectors represent the largest application segment, utilizing LiDAR services for project planning, progress monitoring, and quality assurance activities.

Technological evolution has significantly enhanced service capabilities, with modern LiDAR systems offering improved accuracy, faster data collection, and enhanced integration with other sensing technologies. The adoption of cloud-based processing platforms has democratized access to advanced analytics capabilities, enabling smaller service providers to compete effectively with larger organizations.

Market consolidation trends indicate strategic acquisitions and partnerships as companies seek to expand their service capabilities and geographic coverage. The integration of complementary technologies such as photogrammetry, thermal imaging, and multispectral sensing has created comprehensive geospatial intelligence platforms that deliver enhanced value to customers.

Industry transformation is being driven by several critical factors that are reshaping the competitive landscape and service delivery models. The following insights highlight the most significant market developments:

Market maturation is evident in the standardization of service delivery processes and the development of industry-specific solutions that address unique customer requirements. The emergence of subscription-based service models provides customers with predictable costs and continuous access to updated technology capabilities.

Infrastructure modernization initiatives across North America represent the primary catalyst for LiDAR service demand, with government agencies and private organizations investing heavily in digital transformation projects. The need for accurate baseline measurements and ongoing monitoring of critical infrastructure assets drives consistent demand for high-precision surveying services.

Autonomous vehicle development has emerged as a significant market driver, with automotive manufacturers and technology companies requiring detailed high-definition maps for navigation system development. This application segment demands extremely high accuracy and frequent updates, creating opportunities for specialized service providers to develop long-term partnerships with industry leaders.

Environmental compliance requirements increasingly mandate precise monitoring of natural resources, wetlands, and protected areas. LiDAR services provide the accuracy and documentation capabilities necessary to meet regulatory requirements while supporting sustainable development practices. Climate change adaptation planning also relies heavily on detailed topographic and vegetation analysis capabilities.

Construction industry evolution toward Building Information Modeling (BIM) and digital construction processes creates substantial demand for as-built documentation and progress monitoring services. The integration of LiDAR data with BIM workflows enables improved project coordination and quality control throughout the construction lifecycle.

Cost reduction pressures across multiple industries drive adoption of LiDAR services as organizations seek more efficient alternatives to traditional surveying methods. The ability to capture comprehensive spatial data in single collection events reduces project timelines and minimizes field work requirements.

High initial investment requirements for advanced LiDAR equipment and specialized software platforms create barriers to entry for new service providers. The capital-intensive nature of the business model requires significant financial resources and technical expertise, limiting market participation to well-funded organizations.

Technical complexity associated with LiDAR data processing and analysis requires specialized skills that are in limited supply within the workforce. The shortage of qualified technicians and analysts constrains service capacity and increases operational costs for existing providers.

Weather dependency affects data collection operations, particularly for aerial surveys that require specific atmospheric conditions for optimal results. Seasonal limitations and weather-related delays can impact project schedules and revenue predictability for service providers.

Data management challenges arise from the massive volumes of information generated by LiDAR systems, requiring substantial storage infrastructure and processing capabilities. The complexity of managing, archiving, and retrieving large datasets creates ongoing operational challenges and costs.

Regulatory uncertainties surrounding drone operations and data privacy requirements create compliance challenges for service providers. Evolving regulations regarding airspace usage and data collection activities require continuous monitoring and adaptation of operational procedures.

Emerging applications in precision agriculture present significant growth opportunities as farmers increasingly adopt technology-driven approaches to crop management and yield optimization. LiDAR services enable detailed terrain analysis, drainage planning, and vegetation monitoring that support sustainable farming practices and improved productivity.

Smart city initiatives across major metropolitan areas create demand for comprehensive urban mapping and monitoring services. The integration of LiDAR data with Internet of Things (IoT) sensors and urban planning systems enables more effective city management and infrastructure optimization strategies.

Renewable energy development requires detailed site assessment and ongoing monitoring services for wind and solar installations. LiDAR technology provides critical data for optimizing turbine placement, assessing solar potential, and monitoring environmental impacts throughout project lifecycles.

Insurance industry adoption of geospatial technologies for risk assessment and claims processing creates new market segments for specialized LiDAR services. Property assessment, disaster response, and risk modeling applications offer opportunities for service providers to develop industry-specific solutions.

International expansion opportunities exist as North American service providers leverage their technological expertise and operational experience to enter emerging markets. The export of LiDAR services and technology solutions represents a significant growth avenue for established market participants.

Competitive intensity within the North America LiDAR service market continues to increase as new entrants leverage technological advances to challenge established providers. The market exhibits characteristics of both consolidation among larger players and fragmentation as specialized niche providers emerge to serve specific industry segments.

Technology evolution drives continuous improvement in service capabilities and cost-effectiveness, with solid-state LiDAR systems and advanced processing algorithms enabling new applications and improved performance. The integration of artificial intelligence capabilities has reduced processing times by approximately 40% while improving data accuracy and consistency.

Customer expectations have evolved toward demanding faster turnaround times, higher accuracy, and more comprehensive deliverables. Service providers must continuously invest in technology upgrades and process improvements to meet these increasing demands while maintaining competitive pricing structures.

Partnership strategies have become increasingly important as service providers seek to expand their capabilities and market reach through strategic alliances. Collaborations between technology companies, service providers, and end-user industries create integrated solutions that deliver enhanced value propositions.

Market cyclicality reflects broader economic conditions and infrastructure investment patterns, with government spending and private construction activity significantly influencing demand levels. Service providers must develop diversified customer bases and flexible operational models to manage these cyclical variations effectively.

Comprehensive analysis of the North America LiDAR service market employs multiple research methodologies to ensure accuracy and completeness of market insights. Primary research activities include extensive interviews with industry executives, technology providers, and end-user organizations to gather firsthand perspectives on market trends and challenges.

Secondary research encompasses analysis of industry publications, government reports, patent filings, and financial statements from publicly traded companies. This approach provides quantitative data on market size, growth rates, and competitive positioning while identifying emerging trends and technological developments.

Market modeling techniques utilize statistical analysis and forecasting methods to project future market conditions and growth trajectories. These models incorporate multiple variables including economic indicators, technology adoption rates, and regulatory changes to provide robust market projections.

Industry validation processes involve cross-referencing findings with multiple sources and conducting follow-up interviews to verify key insights and conclusions. This rigorous approach ensures the reliability and accuracy of market intelligence provided to stakeholders.

Continuous monitoring of market developments enables real-time updates to research findings and maintains the relevance of market intelligence throughout rapidly changing industry conditions. This ongoing research approach provides stakeholders with current and actionable market insights.

United States dominance in the North America LiDAR service market reflects the country’s advanced technology infrastructure, substantial infrastructure investment, and leading position in autonomous vehicle development. The U.S. market benefits from strong government support for geospatial technology adoption and a mature ecosystem of service providers and technology companies.

California leadership within the U.S. market stems from the concentration of technology companies, autonomous vehicle testing programs, and environmental monitoring requirements. The state accounts for approximately 28% of total market activity, driven by Silicon Valley technology companies and extensive infrastructure projects.

Texas expansion represents significant growth potential due to large-scale energy projects, urban development initiatives, and favorable regulatory environments for drone operations. The state’s diverse industrial base creates demand across multiple application segments including oil and gas, construction, and agriculture.

Canadian market growth is driven primarily by mining and forestry applications, with service providers developing specialized solutions for resource extraction and environmental monitoring in challenging terrain conditions. The country’s vast geography and natural resource wealth create unique opportunities for LiDAR service applications.

Regional specialization patterns have emerged as service providers develop expertise in applications most relevant to their local markets. Coastal regions focus on flood mapping and coastal erosion monitoring, while inland areas emphasize agricultural and infrastructure applications.

Market leadership is distributed among several categories of service providers, each bringing distinct capabilities and market positioning strategies. The competitive landscape includes established surveying companies, technology-focused startups, and large engineering consultancies that have integrated LiDAR capabilities.

Competitive differentiation strategies focus on technological capabilities, industry specialization, and service quality rather than price competition alone. Leading providers invest heavily in advanced equipment, proprietary processing algorithms, and specialized expertise to maintain competitive advantages.

Market consolidation trends indicate ongoing acquisition activity as larger companies seek to expand their geographic coverage and technical capabilities. Strategic partnerships between technology providers and service companies create integrated solutions that enhance competitive positioning.

By Platform Type:

By Application:

By Service Type:

Airborne LiDAR services continue to dominate the market due to their efficiency in covering large areas and established workflows for data processing and analysis. These services benefit from mature technology platforms and extensive operational experience, making them the preferred choice for regional mapping projects and infrastructure assessment initiatives.

Mobile LiDAR adoption has accelerated significantly, with growth rates of approximately 18% annually driven by infrastructure maintenance requirements and smart city initiatives. The technology’s ability to capture detailed corridor information while maintaining traffic flow makes it particularly valuable for transportation agencies and utility companies.

UAV-based services represent the fastest-growing segment, offering flexibility and cost-effectiveness for smaller projects and challenging access locations. Regulatory improvements and technology advances have expanded the operational envelope for drone-based LiDAR systems, creating new market opportunities.

Terrestrial scanning services maintain strong demand in construction and industrial applications where high accuracy and detailed structural information are required. The integration of terrestrial LiDAR with Building Information Modeling workflows has created new value propositions for construction industry clients.

Specialized applications such as autonomous vehicle mapping and precision agriculture are driving innovation in service delivery models and creating opportunities for niche providers to develop industry-specific expertise and solutions.

Service providers benefit from expanding market opportunities and technological advances that enable more efficient operations and higher-value service offerings. The integration of artificial intelligence and machine learning capabilities reduces processing costs while improving data quality and consistency.

End-user organizations gain access to accurate, timely spatial information that supports better decision-making and improved project outcomes. LiDAR services enable organizations to reduce field work requirements, minimize safety risks, and accelerate project timelines while maintaining high accuracy standards.

Technology companies benefit from growing demand for advanced sensors, processing software, and cloud-based platforms that support LiDAR service delivery. The market expansion creates opportunities for hardware manufacturers and software developers to introduce innovative solutions.

Government agencies leverage LiDAR services to improve infrastructure management, environmental monitoring, and emergency response capabilities. The technology enables more effective resource allocation and supports evidence-based policy development and implementation.

Investment community benefits from the market’s strong growth prospects and increasing adoption across multiple industry verticals. The sector’s resilience and technological innovation create attractive investment opportunities in both established companies and emerging technology providers.

Strengths:

Weaknesses:

Opportunities:

Threats:

Artificial intelligence integration represents the most significant technological trend, with machine learning algorithms increasingly used for automated feature extraction, classification, and quality control processes. This integration has improved processing efficiency by approximately 35% while reducing manual intervention requirements.

Cloud-based processing platforms are transforming service delivery models by enabling scalable computing resources and collaborative workflows. These platforms allow service providers to handle larger projects and offer customers real-time access to processed data and analysis results.

Multi-sensor fusion approaches combine LiDAR with photogrammetry, thermal imaging, and multispectral sensors to create comprehensive geospatial intelligence solutions. This trend addresses customer demands for more complete information and enhanced analytical capabilities.

Real-time processing capabilities are emerging as edge computing technologies enable immediate data analysis and decision support. This trend is particularly important for applications such as autonomous vehicle navigation and emergency response where immediate results are critical.

Subscription service models are gaining popularity as customers seek predictable costs and continuous access to updated technology capabilities. These models provide service providers with recurring revenue streams and stronger customer relationships.

Mobile platform expansion continues with improved drone capabilities and vehicle-mounted systems offering greater flexibility and cost-effectiveness. Regulatory improvements and technology advances are expanding the operational envelope for mobile LiDAR applications.

Technology partnerships between LiDAR service providers and software companies are creating integrated solutions that streamline workflows and improve customer value propositions. These collaborations enable service providers to offer comprehensive geospatial intelligence platforms rather than just data collection services.

Regulatory improvements for drone operations have expanded the market for UAV-based LiDAR services, with recent changes enabling beyond visual line of sight operations and automated flight systems. These developments reduce operational constraints and improve service efficiency.

Market consolidation activities include strategic acquisitions and mergers as companies seek to expand their capabilities and geographic coverage. Recent transactions have focused on combining complementary technologies and accessing new customer segments.

Government initiatives supporting digital infrastructure development create new opportunities for LiDAR service providers. Programs focused on smart cities, transportation modernization, and environmental monitoring drive consistent demand for geospatial services.

International expansion efforts by North American service providers are establishing global market presence and creating export opportunities for technology and expertise. These initiatives leverage the region’s technological leadership to access emerging markets.

MarkWide Research analysis indicates that service providers should focus on developing specialized expertise in high-growth application areas such as autonomous vehicle mapping and precision agriculture. These segments offer opportunities for premium pricing and long-term customer relationships.

Technology investment priorities should emphasize artificial intelligence capabilities and cloud-based processing platforms that improve operational efficiency and enable scalable service delivery. Companies that successfully integrate these technologies will maintain competitive advantages in an increasingly competitive market.

Partnership strategies should focus on creating comprehensive solutions that address complete customer workflows rather than individual components. Collaborations with software companies, hardware manufacturers, and industry specialists can create differentiated value propositions.

Geographic expansion opportunities exist in underserved regions and emerging international markets where North American expertise and technology can command premium pricing. Service providers should evaluate expansion strategies that leverage their core competencies.

Workforce development initiatives are critical for addressing skills shortages and supporting market growth. Companies should invest in training programs and partnerships with educational institutions to develop qualified technicians and analysts.

Market growth projections indicate continued expansion driven by increasing adoption across multiple industry verticals and technological advances that improve service capabilities and cost-effectiveness. The integration of LiDAR services with emerging technologies such as digital twins and Internet of Things platforms will create new value propositions and market opportunities.

Technology evolution will focus on improving automation, reducing costs, and expanding application possibilities. Solid-state LiDAR systems and advanced processing algorithms will enable new service delivery models and applications that are currently not economically viable.

Market maturation will lead to increased standardization of service delivery processes and the development of industry-specific solutions. This evolution will improve service quality and consistency while reducing customer acquisition costs for service providers.

Regulatory environment improvements will continue to expand operational possibilities for drone-based services and reduce compliance burdens for service providers. These changes will enable more efficient service delivery and access to previously restricted areas and applications.

Global expansion opportunities will grow as international markets develop infrastructure and adopt advanced geospatial technologies. North American service providers are well-positioned to leverage their technological expertise and operational experience in these emerging markets.

The North America LiDAR service market represents a dynamic and rapidly evolving sector with strong growth prospects driven by technological innovation and expanding applications across multiple industries. The market benefits from a mature ecosystem of service providers, advanced technology infrastructure, and supportive regulatory environments that enable continued expansion and innovation.

Key success factors for market participants include technological expertise, operational efficiency, and the ability to develop specialized solutions for specific industry applications. Companies that successfully integrate artificial intelligence capabilities, cloud-based platforms, and multi-sensor technologies will maintain competitive advantages and capture disproportionate market growth.

Future market development will be characterized by continued consolidation among service providers, increasing automation of data processing workflows, and expansion into new application areas. The integration of LiDAR services with broader digital transformation initiatives will create additional value propositions and market opportunities for innovative service providers.

What is LiDAR Service?

LiDAR Service refers to the use of Light Detection and Ranging technology to measure distances and create high-resolution maps of the Earth’s surface. It is widely used in applications such as topographic mapping, forestry, and urban planning.

What are the key companies in the North America LiDAR Service Market?

Key companies in the North America LiDAR Service Market include Leica Geosystems, Quantum Spatial, and Woolpert, among others.

What are the main drivers of growth in the North America LiDAR Service Market?

The main drivers of growth in the North America LiDAR Service Market include the increasing demand for accurate mapping in construction and infrastructure projects, advancements in LiDAR technology, and the growing adoption of LiDAR in environmental monitoring.

What challenges does the North America LiDAR Service Market face?

Challenges in the North America LiDAR Service Market include high operational costs, the need for skilled personnel to interpret data, and regulatory hurdles related to data privacy and usage.

What opportunities exist in the North America LiDAR Service Market?

Opportunities in the North America LiDAR Service Market include the expansion of applications in autonomous vehicles, increased use in agriculture for precision farming, and the integration of LiDAR with other technologies like GIS and AI.

What trends are shaping the North America LiDAR Service Market?

Trends shaping the North America LiDAR Service Market include the miniaturization of LiDAR sensors, the rise of drone-based LiDAR services, and the growing emphasis on real-time data processing for various applications.

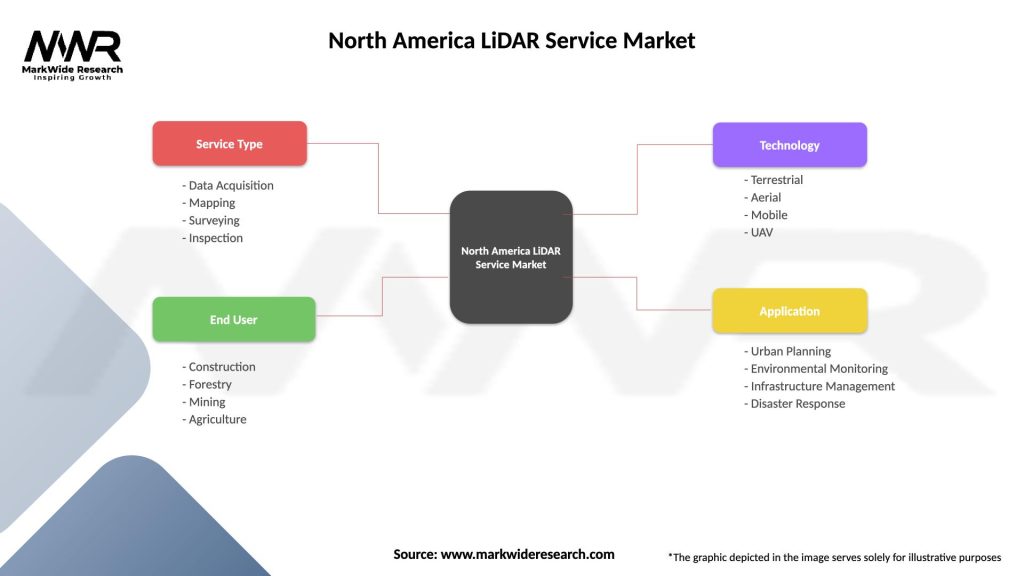

North America LiDAR Service Market

| Segmentation Details | Description |

|---|---|

| Service Type | Data Acquisition, Mapping, Surveying, Inspection |

| End User | Construction, Forestry, Mining, Agriculture |

| Technology | Terrestrial, Aerial, Mobile, UAV |

| Application | Urban Planning, Environmental Monitoring, Infrastructure Management, Disaster Response |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the North America LiDAR Service Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.