444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The North America kidney cancer therapeutics and diagnostics market represents a critical segment of the oncology healthcare landscape, encompassing advanced treatment modalities and diagnostic technologies for renal cell carcinoma and other kidney malignancies. This dynamic market has experienced substantial growth driven by increasing cancer incidence rates, technological innovations in diagnostic imaging, and breakthrough therapeutic developments including immunotherapy and targeted therapy approaches.

Market dynamics indicate robust expansion with the region maintaining a compound annual growth rate (CAGR) of 8.2% over the forecast period. The United States dominates the regional market, accounting for approximately 85% of North American market share, while Canada contributes significantly to the remaining portion. Advanced healthcare infrastructure, substantial research and development investments, and favorable reimbursement policies continue to drive market momentum across both countries.

Technological advancement in precision medicine and personalized treatment approaches has revolutionized kidney cancer management, with biomarker-based diagnostics and companion diagnostics gaining prominence. The integration of artificial intelligence in diagnostic imaging and the emergence of liquid biopsy technologies represent transformative developments reshaping the market landscape.

The North America kidney cancer therapeutics and diagnostics market refers to the comprehensive ecosystem of medical products, services, and technologies dedicated to the detection, diagnosis, treatment, and monitoring of kidney cancer within the United States and Canada. This market encompasses pharmaceutical therapeutics including chemotherapy agents, immunotherapy drugs, targeted therapy medications, and supportive care products, alongside diagnostic solutions such as imaging technologies, biomarker tests, and molecular diagnostic platforms.

Kidney cancer therapeutics include both systemic treatments and localized interventions designed to eliminate or control malignant renal tumors. The diagnostic component encompasses screening tools, imaging modalities, laboratory tests, and advanced molecular diagnostics that enable early detection, accurate staging, and treatment monitoring for optimal patient outcomes.

Strategic market analysis reveals the North America kidney cancer therapeutics and diagnostics market as a rapidly evolving sector characterized by significant innovation and substantial growth potential. The market benefits from strong demographic trends, including an aging population and increasing awareness of kidney cancer risk factors, contributing to higher diagnosis rates and expanded treatment demand.

Key market drivers include the rising incidence of renal cell carcinoma, accounting for approximately 90% of all kidney cancer cases, and the successful development of novel immunotherapy combinations that have demonstrated superior efficacy compared to traditional treatment approaches. The market has witnessed remarkable transformation with the introduction of checkpoint inhibitors and tyrosine kinase inhibitors, fundamentally changing treatment paradigms.

Competitive landscape features established pharmaceutical giants alongside emerging biotechnology companies, creating a dynamic environment for innovation and market expansion. Strategic partnerships between diagnostic companies and pharmaceutical manufacturers have accelerated the development of companion diagnostics, enhancing treatment precision and patient outcomes.

Market intelligence indicates several critical insights shaping the North America kidney cancer therapeutics and diagnostics landscape:

Primary growth drivers propelling the North America kidney cancer therapeutics and diagnostics market include demographic, technological, and regulatory factors that create favorable conditions for sustained expansion.

Demographic trends represent fundamental market drivers, with the aging North American population experiencing higher kidney cancer incidence rates. Risk factors including obesity, hypertension, and smoking prevalence contribute to increasing disease burden, while improved healthcare access ensures more patients receive appropriate diagnosis and treatment.

Innovation acceleration in therapeutic development has introduced breakthrough treatments that significantly improve patient outcomes. The success of immunotherapy combinations and targeted therapy approaches has expanded treatment options, creating new market opportunities and driving physician adoption of advanced treatment protocols.

Regulatory support through expedited approval pathways and breakthrough therapy designations has accelerated the introduction of innovative treatments to market. The FDA’s commitment to supporting oncology drug development through streamlined review processes has encouraged pharmaceutical investment and innovation in kidney cancer therapeutics.

Healthcare infrastructure improvements, including the expansion of comprehensive cancer centers and specialized oncology practices, have enhanced treatment accessibility and quality of care delivery across North America.

Market challenges present significant obstacles to growth and adoption within the North America kidney cancer therapeutics and diagnostics market, requiring strategic approaches to overcome barriers and limitations.

Cost considerations represent primary market restraints, with advanced therapeutics and diagnostic technologies requiring substantial financial investments from healthcare systems and patients. High treatment costs, particularly for novel immunotherapy combinations, create access barriers and reimbursement challenges that limit market penetration.

Regulatory complexity surrounding companion diagnostics and combination therapy approvals can delay market entry and increase development costs for pharmaceutical and diagnostic companies. The requirement for extensive clinical validation and regulatory coordination between therapeutic and diagnostic components creates additional hurdles.

Healthcare disparities across different regions and patient populations limit uniform market access, with rural areas and underserved communities experiencing reduced availability of advanced diagnostic and therapeutic options.

Technical limitations in current diagnostic technologies, including challenges in detecting early-stage kidney cancer and distinguishing between benign and malignant lesions, constrain diagnostic accuracy and clinical utility in certain patient populations.

Emerging opportunities within the North America kidney cancer therapeutics and diagnostics market present substantial potential for growth, innovation, and improved patient outcomes through strategic development and investment initiatives.

Artificial intelligence integration in diagnostic imaging represents a transformative opportunity, with AI-powered analysis systems demonstrating potential to improve diagnostic accuracy and reduce interpretation time. Machine learning algorithms for radiology and pathology applications offer significant market expansion possibilities.

Liquid biopsy development presents revolutionary opportunities for non-invasive cancer detection and monitoring. Circulating tumor DNA and other biomarker technologies could fundamentally change kidney cancer screening and surveillance practices, creating new market segments and revenue streams.

Combination therapy optimization through precision medicine approaches offers opportunities to develop more effective treatment regimens while minimizing adverse effects. The identification of optimal drug combinations based on patient-specific biomarkers represents a significant growth area.

Telemedicine expansion and remote monitoring technologies create opportunities to extend specialized kidney cancer care to underserved populations, potentially expanding market reach and improving patient access to expert oncology services.

Market dynamics within the North America kidney cancer therapeutics and diagnostics sector reflect complex interactions between technological innovation, regulatory evolution, competitive pressures, and changing clinical practice patterns that collectively shape market trajectory and growth potential.

Innovation cycles demonstrate accelerating pace of development, with breakthrough therapy designations and expedited approvals reducing time-to-market for promising treatments. The convergence of immunotherapy, targeted therapy, and precision diagnostics creates synergistic opportunities for comprehensive cancer care solutions.

Competitive intensity continues to increase as pharmaceutical companies invest heavily in kidney cancer research and development. Strategic partnerships between established players and emerging biotechnology companies are reshaping competitive dynamics and accelerating innovation timelines.

Reimbursement evolution plays a crucial role in market dynamics, with payers increasingly focusing on value-based care models and outcomes-based pricing structures. The demonstration of real-world effectiveness and cost-effectiveness becomes critical for market access and commercial success.

Clinical practice transformation toward multidisciplinary care teams and personalized treatment approaches influences market demand patterns and drives adoption of integrated diagnostic and therapeutic solutions.

Comprehensive research methodology employed in analyzing the North America kidney cancer therapeutics and diagnostics market incorporates multiple data sources, analytical approaches, and validation techniques to ensure accuracy and reliability of market insights and projections.

Primary research activities include extensive interviews with key opinion leaders, oncology specialists, pharmaceutical executives, and diagnostic company representatives across the United States and Canada. Survey data from healthcare providers and patient advocacy organizations provides additional perspectives on market trends and unmet needs.

Secondary research analysis encompasses review of clinical trial databases, regulatory filings, patent landscapes, and published literature to identify emerging trends and technological developments. Market intelligence from healthcare databases and industry reports provides quantitative foundation for market sizing and growth projections.

Data validation processes include triangulation of findings across multiple sources, expert review panels, and statistical analysis to ensure consistency and accuracy of market estimates and forecasts.

Regional market distribution across North America reveals distinct patterns of adoption, growth, and opportunity that reflect differences in healthcare infrastructure, regulatory environments, and patient populations between the United States and Canada.

United States market maintains dominant position with approximately 85% regional market share, driven by large patient population, advanced healthcare infrastructure, and substantial research and development investments. Major metropolitan areas including New York, Los Angeles, and Houston serve as key market centers with high concentrations of specialized cancer treatment facilities.

California and Texas represent the largest state markets, accounting for combined market share of approximately 25% due to large populations and comprehensive cancer care networks. The presence of leading academic medical centers and biotechnology companies in these states contributes to market leadership and innovation.

Canadian market demonstrates steady growth with increasing adoption of advanced therapeutics and diagnostic technologies. Provincial healthcare systems provide universal coverage that supports market access, while research collaborations with US institutions facilitate technology transfer and clinical development.

Regional disparities exist in access to advanced treatments and diagnostic technologies, with urban centers typically offering more comprehensive services compared to rural areas. Telemedicine initiatives and mobile diagnostic programs are addressing these gaps and expanding market reach.

Competitive environment within the North America kidney cancer therapeutics and diagnostics market features diverse participants ranging from multinational pharmaceutical corporations to specialized biotechnology companies and diagnostic technology providers.

Leading pharmaceutical companies dominating the therapeutics segment include:

Diagnostic market leaders include established medical technology companies and emerging molecular diagnostics specialists focused on precision oncology applications. Strategic collaborations between pharmaceutical and diagnostic companies are increasingly common to develop integrated treatment and testing solutions.

Competitive strategies emphasize innovation, clinical differentiation, and comprehensive patient support programs to gain market share and establish sustainable competitive advantages in this rapidly evolving market.

Market segmentation analysis reveals distinct categories within the North America kidney cancer therapeutics and diagnostics market, each characterized by unique growth patterns, competitive dynamics, and development opportunities.

By Therapeutic Class:

By Diagnostic Type:

By End User:

Therapeutic category analysis reveals distinct trends and opportunities within specific segments of the North America kidney cancer therapeutics and diagnostics market, providing insights into growth drivers and competitive positioning.

Immunotherapy segment demonstrates exceptional growth momentum with adoption rates increasing by 40% annually in first-line treatment settings. Combination immunotherapy regimens show particular promise, with clinical trials demonstrating superior outcomes compared to monotherapy approaches. The segment benefits from strong clinical evidence, favorable regulatory support, and increasing physician confidence in immune-based treatments.

Targeted therapy category maintains stable market position through continuous innovation and expanded indications. Next-generation tyrosine kinase inhibitors with improved safety profiles and enhanced efficacy are driving segment evolution, while combination approaches with immunotherapy create new treatment paradigms.

Diagnostic imaging segment experiences steady growth driven by technological advancement and increased screening awareness. Advanced imaging modalities including contrast-enhanced ultrasound and functional MRI provide improved diagnostic accuracy, while AI-powered analysis tools enhance interpretation efficiency and consistency.

Molecular diagnostics category represents the fastest-growing diagnostic segment, with biomarker testing becoming integral to treatment selection and monitoring. Companion diagnostics for targeted therapies and predictive biomarkers for immunotherapy response drive segment expansion and clinical adoption.

Industry participants across the North America kidney cancer therapeutics and diagnostics market ecosystem realize substantial benefits through strategic positioning, innovation investment, and collaborative partnerships that enhance competitive advantage and market success.

Pharmaceutical companies benefit from expanding market opportunities driven by increasing patient populations and growing treatment demand. The development of breakthrough therapies provides opportunities for premium pricing and market leadership, while combination therapy approaches create multiple revenue streams and extended patent protection.

Diagnostic companies gain from increasing demand for precision medicine solutions and companion diagnostics. The integration of artificial intelligence and machine learning technologies creates opportunities for differentiation and improved clinical utility, while partnerships with pharmaceutical companies provide stable revenue streams and market validation.

Healthcare providers benefit from improved treatment options that enhance patient outcomes and satisfaction. Advanced diagnostic technologies enable more accurate diagnosis and treatment selection, while comprehensive treatment protocols improve care quality and clinical efficiency.

Patients and caregivers realize significant benefits through access to innovative treatments with improved efficacy and reduced side effects. Early detection capabilities and personalized treatment approaches contribute to better survival rates and quality of life outcomes.

Healthcare systems benefit from value-based care opportunities and improved resource utilization through precision medicine approaches that optimize treatment selection and reduce unnecessary interventions.

Strengths:

Weaknesses:

Opportunities:

Threats:

Transformative trends shaping the North America kidney cancer therapeutics and diagnostics market reflect broader healthcare evolution toward personalized medicine, digital health integration, and value-based care delivery models.

Precision medicine adoption represents the most significant trend, with biomarker-driven treatment selection becoming standard practice. Genetic profiling and molecular characterization of tumors enable personalized treatment approaches that optimize efficacy while minimizing adverse effects, fundamentally changing clinical practice patterns.

Combination therapy optimization continues to evolve with novel drug combinations demonstrating superior outcomes compared to monotherapy approaches. The strategic combination of immunotherapy and targeted therapy agents creates synergistic effects that improve response rates and duration of response.

Digital health integration accelerates through telemedicine adoption, remote monitoring technologies, and digital therapeutics applications. These technologies expand access to specialized care while improving patient engagement and treatment adherence.

Artificial intelligence implementation in diagnostic imaging and treatment optimization shows remarkable potential for improving clinical outcomes. Machine learning algorithms enhance diagnostic accuracy and enable predictive analytics for treatment response and prognosis.

Value-based care transition influences market dynamics through outcomes-based pricing models and risk-sharing arrangements between payers and pharmaceutical companies, emphasizing real-world effectiveness and cost-effectiveness demonstration.

Recent industry developments within the North America kidney cancer therapeutics and diagnostics market demonstrate accelerating innovation pace and strategic collaboration trends that reshape competitive dynamics and market opportunities.

Regulatory approvals for breakthrough combination therapies have expanded treatment options significantly. MarkWide Research analysis indicates that recent FDA approvals for novel immunotherapy combinations have achieved response rates exceeding 70% in clinical trials, representing substantial improvement over previous standard treatments.

Strategic partnerships between pharmaceutical companies and diagnostic developers accelerate companion diagnostic development and regulatory approval processes. These collaborations ensure synchronized availability of therapeutic and diagnostic components for precision medicine applications.

Technology acquisitions by major pharmaceutical companies focus on artificial intelligence capabilities, liquid biopsy technologies, and digital health platforms that enhance drug development and patient care delivery capabilities.

Clinical trial innovations including adaptive trial designs and real-world evidence generation accelerate development timelines while reducing costs and improving regulatory success rates for promising treatments.

Investment trends show substantial venture capital and private equity funding directed toward emerging biotechnology companies developing novel therapeutic approaches and diagnostic technologies for kidney cancer applications.

Strategic recommendations for market participants in the North America kidney cancer therapeutics and diagnostics market emphasize innovation focus, partnership development, and patient-centric approaches to achieve sustainable competitive advantage and market success.

Innovation investment should prioritize combination therapy development and companion diagnostic integration to create comprehensive treatment solutions. Companies should focus on biomarker identification and validation to support precision medicine approaches and differentiate their offerings in competitive markets.

Partnership strategies should emphasize collaboration between pharmaceutical and diagnostic companies to develop integrated solutions that address complete patient care pathways. Strategic alliances with academic medical centers and research institutions can accelerate clinical development and provide access to patient populations for clinical trials.

Market access preparation requires early engagement with payers and regulatory authorities to ensure successful commercialization of innovative treatments. Value demonstration through health economics and outcomes research becomes critical for reimbursement approval and market adoption.

Digital transformation initiatives should focus on patient engagement technologies, remote monitoring capabilities, and artificial intelligence applications that enhance clinical outcomes and operational efficiency.

Geographic expansion strategies should consider underserved markets and rural populations where telemedicine and mobile diagnostic technologies can provide access to specialized kidney cancer care services.

Future market trajectory for the North America kidney cancer therapeutics and diagnostics market indicates sustained growth driven by continued innovation, expanding patient populations, and evolving treatment paradigms that emphasize personalized medicine and comprehensive care approaches.

Technological advancement will continue to drive market evolution with artificial intelligence, liquid biopsy technologies, and next-generation therapeutics creating new opportunities for improved patient outcomes. MWR projections suggest that AI-powered diagnostic tools could achieve adoption rates of 60% in major cancer centers within the next five years.

Treatment landscape transformation will emphasize combination approaches and precision medicine applications, with biomarker-driven treatment selection becoming universal standard of care. The integration of immunotherapy and targeted therapy combinations will likely expand to earlier disease stages and adjuvant treatment settings.

Market consolidation through strategic acquisitions and partnerships will create more comprehensive solution providers capable of addressing complete patient care pathways from diagnosis through treatment and monitoring.

Regulatory evolution toward adaptive approval pathways and real-world evidence acceptance will accelerate innovation and market access for breakthrough treatments, while maintaining appropriate safety and efficacy standards.

Global expansion opportunities will emerge as North American companies leverage their technological leadership to enter international markets, while international collaboration enhances research and development capabilities.

The North America kidney cancer therapeutics and diagnostics market represents a dynamic and rapidly evolving sector characterized by significant innovation, substantial growth potential, and transformative impact on patient care outcomes. The convergence of breakthrough therapeutic developments, advanced diagnostic technologies, and precision medicine approaches creates unprecedented opportunities for market participants and stakeholders.

Market fundamentals remain strong with increasing patient populations, supportive regulatory environments, and substantial investment in research and development driving sustained growth momentum. The successful introduction of immunotherapy combinations and targeted therapy innovations has fundamentally changed treatment paradigms and improved survival outcomes for kidney cancer patients across North America.

Strategic positioning for future success requires focus on innovation, collaboration, and patient-centric solutions that address evolving healthcare needs and market demands. Companies that successfully integrate therapeutic and diagnostic capabilities while leveraging digital health technologies will likely achieve sustainable competitive advantages in this competitive market environment.

Long-term outlook indicates continued market expansion driven by technological advancement, demographic trends, and evolving treatment standards that emphasize personalized medicine and comprehensive care approaches. The North America kidney cancer therapeutics and diagnostics market is well-positioned to maintain its leadership role in global oncology innovation while delivering improved outcomes for patients and value for healthcare systems.

What is Kidney Cancer Therapeutics & Diagnostics?

Kidney Cancer Therapeutics & Diagnostics refers to the medical treatments and diagnostic tools used to manage and detect kidney cancer. This includes various therapies such as immunotherapy, targeted therapy, and surgical options, as well as diagnostic methods like imaging and biomarker tests.

What are the key players in the North America Kidney Cancer Therapeutics & Diagnostics Market?

Key players in the North America Kidney Cancer Therapeutics & Diagnostics Market include Bristol-Myers Squibb, Merck & Co., and Pfizer, among others. These companies are involved in developing innovative therapies and diagnostic solutions for kidney cancer.

What are the growth factors driving the North America Kidney Cancer Therapeutics & Diagnostics Market?

The growth of the North America Kidney Cancer Therapeutics & Diagnostics Market is driven by factors such as the increasing incidence of kidney cancer, advancements in treatment technologies, and a growing focus on personalized medicine. Additionally, rising awareness and improved diagnostic capabilities contribute to market expansion.

What challenges does the North America Kidney Cancer Therapeutics & Diagnostics Market face?

Challenges in the North America Kidney Cancer Therapeutics & Diagnostics Market include high treatment costs, regulatory hurdles, and the complexity of developing effective therapies. Furthermore, competition among companies can lead to market saturation and pricing pressures.

What opportunities exist in the North America Kidney Cancer Therapeutics & Diagnostics Market?

Opportunities in the North America Kidney Cancer Therapeutics & Diagnostics Market include the potential for novel drug development, the integration of artificial intelligence in diagnostics, and expanding access to treatment options. Collaborations between biotech firms and research institutions also present significant growth prospects.

What trends are shaping the North America Kidney Cancer Therapeutics & Diagnostics Market?

Trends shaping the North America Kidney Cancer Therapeutics & Diagnostics Market include the rise of immunotherapy and targeted therapies, increased use of liquid biopsies for early detection, and a shift towards patient-centric care models. These trends are enhancing treatment outcomes and improving patient experiences.

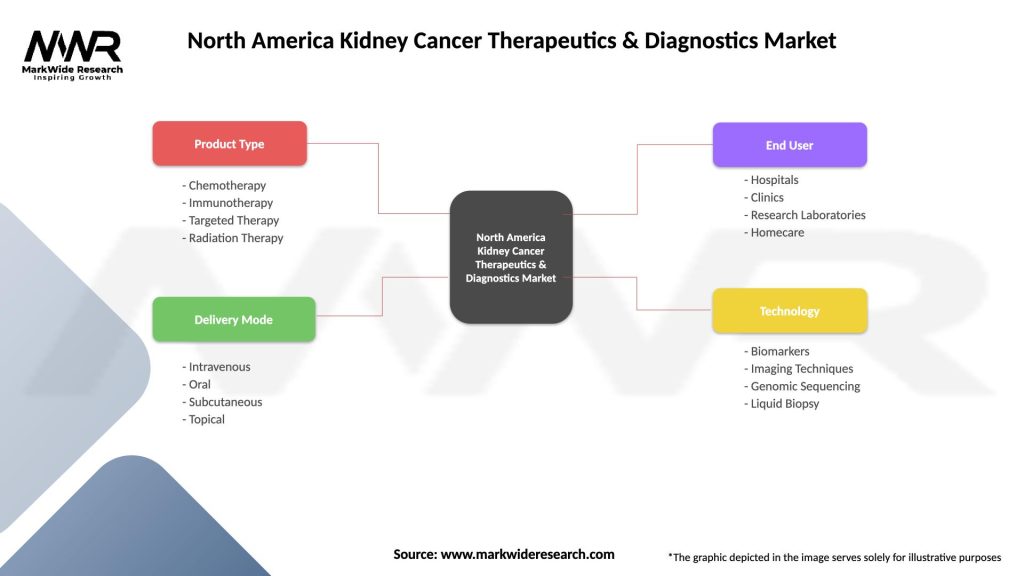

North America Kidney Cancer Therapeutics & Diagnostics Market

| Segmentation Details | Description |

|---|---|

| Product Type | Chemotherapy, Immunotherapy, Targeted Therapy, Radiation Therapy |

| Delivery Mode | Intravenous, Oral, Subcutaneous, Topical |

| End User | Hospitals, Clinics, Research Laboratories, Homecare |

| Technology | Biomarkers, Imaging Techniques, Genomic Sequencing, Liquid Biopsy |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the North America Kidney Cancer Therapeutics & Diagnostics Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.