444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The North America home appliance market represents one of the most dynamic and technologically advanced segments in the global consumer goods industry. This comprehensive market encompasses a wide range of essential household products, from traditional white goods like refrigerators and washing machines to cutting-edge smart home technologies that are revolutionizing how consumers interact with their living spaces. Market dynamics indicate robust growth driven by technological innovation, changing consumer preferences, and increasing emphasis on energy efficiency.

Regional leadership in North America stems from high disposable incomes, strong housing market activity, and early adoption of smart home technologies. The market demonstrates remarkable resilience and adaptability, with manufacturers continuously innovating to meet evolving consumer demands for connectivity, sustainability, and convenience. Growth projections suggest the market will expand at a CAGR of 6.2% over the forecast period, driven primarily by smart appliance adoption and replacement cycles.

Consumer behavior patterns reveal increasing preference for premium, energy-efficient appliances with advanced features. The integration of Internet of Things (IoT) technology has transformed traditional appliances into connected devices that offer enhanced functionality and user experience. Market penetration of smart appliances has reached 34% in urban households, indicating significant growth potential in suburban and rural markets.

The North America home appliance market refers to the comprehensive ecosystem of household electrical and mechanical devices designed to perform domestic tasks, enhance living comfort, and improve household efficiency across the United States, Canada, and Mexico. This market encompasses both traditional appliances and modern smart devices that integrate advanced technologies to provide automated, connected, and energy-efficient solutions for contemporary homes.

Market scope includes major appliance categories such as refrigeration systems, cooking appliances, laundry equipment, dishwashers, and small kitchen appliances. The definition extends to emerging categories like smart home hubs, connected cleaning devices, and energy management systems that represent the future of home automation. Technological integration has expanded the traditional boundaries of home appliances to include devices with artificial intelligence, machine learning capabilities, and seamless connectivity features.

Strategic analysis of the North America home appliance market reveals a mature yet rapidly evolving industry characterized by intense competition, technological innovation, and shifting consumer preferences toward smart, sustainable solutions. The market demonstrates strong fundamentals supported by steady housing construction, renovation activities, and increasing consumer awareness of energy efficiency benefits.

Key market drivers include rising disposable incomes, urbanization trends, and growing emphasis on home automation. The COVID-19 pandemic accelerated demand for home appliances as consumers invested in upgrading their living spaces during extended periods of remote work and social distancing. Smart appliance adoption has increased by 28% since 2020, reflecting changing consumer priorities and technological readiness.

Competitive landscape features established multinational corporations alongside innovative technology companies entering the market with disruptive solutions. Market leaders focus on product differentiation through advanced features, energy efficiency improvements, and comprehensive smart home ecosystem integration. Premium segment growth outpaces overall market expansion, with luxury appliances capturing 42% of total market revenue despite representing only 18% of unit sales.

Market intelligence reveals several critical insights that define the current landscape and future trajectory of the North America home appliance market:

Primary growth drivers propelling the North America home appliance market forward include a combination of demographic, technological, and economic factors that create sustained demand for innovative household solutions.

Housing market strength continues to drive appliance demand through new construction and renovation projects. The millennial generation’s entry into homeownership represents a significant demographic shift, bringing different expectations for appliance functionality, connectivity, and design aesthetics. Smart home adoption has become a key driver, with consumers increasingly viewing connected appliances as essential components of modern living.

Energy efficiency regulations and consumer environmental consciousness drive demand for advanced appliances that reduce utility costs and environmental impact. Government incentive programs and utility rebates further encourage adoption of energy-efficient models. Technological advancement in areas such as artificial intelligence, machine learning, and sensor technology enables manufacturers to develop increasingly sophisticated products that offer superior performance and user experience.

Lifestyle changes accelerated by the pandemic have increased focus on home comfort, convenience, and functionality. Remote work trends have elevated the importance of home environments, driving investment in premium appliances that enhance daily living experiences.

Market challenges facing the North America home appliance industry include several factors that may limit growth potential and create operational difficulties for manufacturers and retailers.

Supply chain disruptions have significantly impacted appliance availability and pricing, with semiconductor shortages particularly affecting smart appliance production. Raw material cost inflation has pressured manufacturer margins and consumer pricing, potentially limiting demand in price-sensitive segments. Labor shortages in manufacturing and installation services have created bottlenecks that affect market growth.

Economic uncertainty and inflation concerns may cause consumers to delay discretionary appliance purchases, particularly in the premium segment. Rising interest rates could impact housing market activity, which directly correlates with appliance demand. Regulatory complexity across different states and provinces creates compliance challenges for manufacturers operating across North America.

Technology adoption barriers exist among certain consumer segments, particularly older demographics who may resist smart appliance features. Privacy and security concerns related to connected devices may limit adoption rates despite technological advantages.

Significant opportunities exist within the North America home appliance market for companies that can effectively leverage emerging trends and address evolving consumer needs.

Smart home ecosystem integration presents substantial growth potential as consumers seek seamless connectivity between appliances and home automation systems. The development of comprehensive platforms that enable unified control and optimization of multiple appliances represents a key opportunity for market leaders. Artificial intelligence integration can enable predictive maintenance, personalized user experiences, and automated optimization of appliance performance.

Sustainability initiatives offer opportunities for differentiation through eco-friendly materials, circular economy principles, and carbon-neutral manufacturing processes. Service-based business models including appliance-as-a-service offerings could transform traditional ownership models and create recurring revenue streams.

Emerging market segments such as compact urban appliances, multi-functional devices, and specialized solutions for aging populations present untapped growth potential. Direct-to-consumer channels enable manufacturers to build stronger customer relationships and capture higher margins while providing personalized shopping experiences.

Complex market dynamics shape the competitive landscape and growth trajectory of the North America home appliance market through interconnected forces that influence supply, demand, and industry evolution.

Competitive intensity has increased as traditional appliance manufacturers face competition from technology companies entering the smart home market. This convergence has accelerated innovation cycles and forced established players to invest heavily in digital transformation and connectivity capabilities. Market consolidation continues as companies seek scale advantages and complementary technology capabilities through strategic acquisitions.

Consumer expectations have evolved rapidly, demanding appliances that offer not just functionality but also connectivity, energy efficiency, and aesthetic appeal. The shift toward premium products has created opportunities for differentiation but also increased competitive pressure on pricing and features. Retail channel evolution has transformed how consumers research, compare, and purchase appliances, with online channels gaining 37% market share in certain categories.

Regulatory environment continues to evolve with stricter energy efficiency standards and safety requirements that drive innovation while potentially increasing compliance costs. MarkWide Research analysis indicates that regulatory changes have accelerated the adoption of advanced technologies by an average of 18 months compared to historical patterns.

Comprehensive research methodology employed in analyzing the North America home appliance market combines multiple data sources and analytical approaches to ensure accuracy and reliability of market insights.

Primary research includes extensive surveys of consumers, retailers, and industry professionals to gather firsthand insights into market trends, preferences, and challenges. In-depth interviews with key industry executives provide strategic perspectives on market direction and competitive dynamics. Secondary research encompasses analysis of industry reports, government statistics, trade publications, and company financial statements to establish market baselines and validate primary findings.

Quantitative analysis utilizes statistical modeling to project market trends, segment performance, and regional variations. Qualitative assessment provides context for numerical data through expert opinions, case studies, and trend analysis. Market sizing and forecasting employ multiple methodologies including top-down and bottom-up approaches to ensure accuracy and account for various market scenarios.

Data validation processes include cross-referencing multiple sources, expert review panels, and sensitivity analysis to ensure research reliability and minimize potential biases in market assessment.

Regional market dynamics across North America reveal distinct patterns of demand, competition, and growth opportunities that reflect local economic conditions, consumer preferences, and regulatory environments.

United States market dominates the regional landscape, accounting for approximately 78% of total North America home appliance demand. Strong economic fundamentals, high homeownership rates, and early adoption of smart technologies drive market leadership. Regional variations within the US include higher demand for energy-efficient appliances in California due to regulatory requirements and utility incentives, while southern states show preference for larger capacity appliances suited to family-oriented lifestyles.

Canadian market represents 16% of regional demand, characterized by strong preference for energy-efficient appliances due to climate considerations and government incentive programs. Bilingual requirements and metric system preferences create unique market considerations for manufacturers operating in Canada.

Mexican market shows the highest growth potential with 6% current market share but rapidly expanding middle class and urbanization trends. Price sensitivity remains higher in Mexico, creating opportunities for value-oriented product lines while premium segments show emerging growth in major metropolitan areas.

Competitive environment in the North America home appliance market features established multinational corporations, innovative technology companies, and specialized manufacturers competing across multiple dimensions including technology, design, pricing, and customer service.

Competitive strategies increasingly focus on smart technology integration, energy efficiency improvements, and comprehensive customer service offerings. Brand differentiation occurs through design innovation, specialized features, and ecosystem integration capabilities that create customer loyalty and premium pricing opportunities.

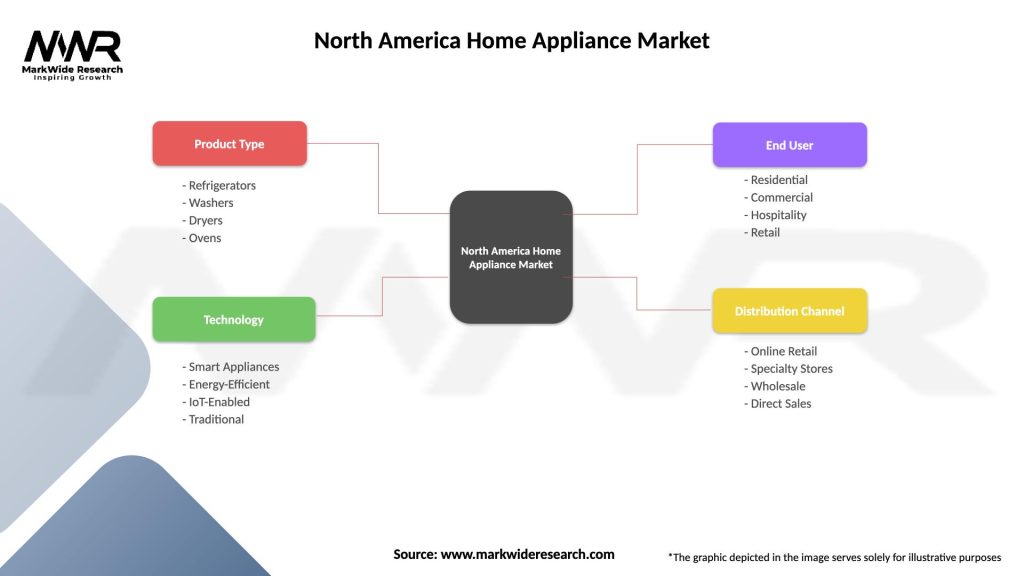

Market segmentation analysis reveals distinct categories within the North America home appliance market, each with unique characteristics, growth patterns, and competitive dynamics.

By Product Type:

By Technology:

By Distribution Channel:

Detailed category analysis provides insights into specific appliance segments that drive market growth and innovation within the North America home appliance market.

Refrigeration Category: Represents the largest single appliance category with steady replacement demand and growing preference for smart features. French door configurations and counter-depth designs show strong growth, while energy efficiency improvements drive premium pricing. Smart refrigerators with internal cameras and inventory management capabilities are gaining traction among tech-savvy consumers.

Laundry Appliances: High-efficiency washers and dryers dominate new sales, with front-loading configurations preferred for energy and water savings. Stackable units address space constraints in urban markets, while large capacity models serve family-oriented segments. Smart features including remote monitoring and cycle optimization show increasing adoption.

Cooking Appliances: Induction cooktops and convection ovens gain market share due to energy efficiency and performance advantages. Smart cooking features including recipe integration, temperature monitoring, and automated cooking programs appeal to culinary enthusiasts. Premium materials and professional-style designs command significant price premiums.

Dishwashers: Third rack designs and advanced wash systems drive replacement purchases, while quiet operation becomes increasingly important. Smart connectivity enables remote operation and maintenance alerts, enhancing user convenience and appliance longevity.

Industry participants across the North America home appliance market value chain realize significant benefits from market growth, technological advancement, and evolving consumer preferences.

Manufacturers benefit from premium pricing opportunities through smart technology integration and energy efficiency improvements. Innovation capabilities enable differentiation in competitive markets while building customer loyalty through superior performance and features. Scale advantages in manufacturing and distribution create cost efficiencies that support competitive pricing strategies.

Retailers capitalize on higher margin opportunities through premium appliance sales and extended service offerings. Digital transformation enables enhanced customer experiences through virtual showrooms, augmented reality demonstrations, and personalized recommendations. Service revenue streams provide recurring income and strengthen customer relationships.

Consumers realize substantial benefits through improved appliance performance, energy savings, and enhanced convenience. Smart features enable remote monitoring, predictive maintenance, and optimized operation that reduces long-term ownership costs. Energy-efficient appliances provide ongoing utility bill savings while supporting environmental sustainability goals.

Utility Companies benefit from reduced peak demand and improved grid stability through smart appliance integration and demand response programs. Energy efficiency improvements help utilities meet regulatory requirements while reducing infrastructure investment needs.

Strengths:

Weaknesses:

Opportunities:

Threats:

Transformative trends reshaping the North America home appliance market reflect changing consumer lifestyles, technological capabilities, and environmental consciousness.

Smart Home Integration continues accelerating with appliances becoming integral components of connected home ecosystems. Voice control integration with Amazon Alexa, Google Assistant, and Apple HomeKit enables seamless user interaction and automation. Machine learning algorithms optimize appliance performance based on usage patterns and preferences.

Sustainability Focus drives demand for energy-efficient appliances, recyclable materials, and carbon-neutral manufacturing processes. Circular economy principles influence product design for repairability, upgradability, and end-of-life recycling. Water conservation features become increasingly important in drought-prone regions.

Customization and Personalization trends enable consumers to configure appliances for specific needs and aesthetic preferences. Modular designs allow component upgrades and feature additions over appliance lifecycles. Color and finish options expand beyond traditional white and stainless steel to include bold colors and premium materials.

Health and Wellness Integration incorporates air purification, water filtration, and food safety features into traditional appliances. Antimicrobial surfaces and UV sanitization capabilities address health concerns accelerated by pandemic experiences.

Recent industry developments demonstrate the dynamic nature of the North America home appliance market and highlight strategic initiatives by major market participants.

Technology Partnerships between appliance manufacturers and software companies accelerate smart feature development and ecosystem integration. Strategic acquisitions enable traditional manufacturers to acquire technology capabilities while tech companies gain manufacturing expertise and distribution channels.

Manufacturing Investments in North American production facilities reduce supply chain risks and support reshoring initiatives. Automation upgrades improve manufacturing efficiency and quality while addressing labor shortage challenges. Sustainable manufacturing practices reduce environmental impact and support corporate responsibility goals.

Product Innovation focuses on breakthrough technologies including induction cooking, heat pump dryers, and advanced refrigeration systems. MWR analysis indicates that innovation cycles have accelerated by 25% compared to pre-pandemic timelines, driven by competitive pressure and changing consumer expectations.

Retail Channel Evolution includes expansion of online sales capabilities, virtual showroom experiences, and direct-to-consumer delivery services. Service integration provides comprehensive customer support including installation, maintenance, and upgrade services.

Strategic recommendations for market participants focus on leveraging emerging opportunities while addressing key challenges in the evolving North America home appliance market.

Technology Investment should prioritize smart home integration capabilities, artificial intelligence applications, and user experience improvements. Platform development that enables seamless integration across multiple appliance categories creates competitive advantages and customer loyalty. Investment in cybersecurity and data privacy protection becomes essential as connectivity increases.

Market Positioning strategies should emphasize value proposition differentiation through energy efficiency, smart features, and comprehensive service offerings. Premium segment focus offers higher margins and growth potential, while value segments require operational efficiency and cost optimization.

Distribution Strategy optimization should balance traditional retail relationships with direct-to-consumer capabilities. Omnichannel approaches that integrate online and offline experiences provide competitive advantages in customer acquisition and retention.

Sustainability Initiatives should encompass product design, manufacturing processes, and end-of-life management to meet evolving consumer expectations and regulatory requirements. Circular economy principles create opportunities for new business models and customer engagement strategies.

Future market trajectory for the North America home appliance market indicates continued growth driven by technological innovation, demographic trends, and evolving consumer preferences toward smart, sustainable solutions.

Technology Evolution will accelerate integration of artificial intelligence, machine learning, and advanced sensors that enable predictive maintenance, automated optimization, and personalized user experiences. 5G connectivity will enhance real-time communication capabilities and enable new applications in remote monitoring and control.

Market Expansion opportunities exist in underserved segments including compact urban appliances, aging-in-place solutions, and specialized commercial applications. MarkWide Research projects that smart appliance penetration will reach 67% of households by 2028, representing substantial growth from current levels.

Sustainability Integration will become increasingly important with carbon-neutral manufacturing, renewable energy integration, and circular economy principles driving product development and business model innovation. Regulatory evolution will continue pushing energy efficiency standards while creating opportunities for advanced technology adoption.

Business Model Innovation including appliance-as-a-service offerings, subscription maintenance programs, and integrated smart home solutions will create new revenue streams and customer relationship models. Ecosystem partnerships between appliance manufacturers, technology companies, and service providers will define competitive advantages in the connected home market.

The North America home appliance market stands at a transformative inflection point where traditional manufacturing excellence converges with cutting-edge technology innovation to create unprecedented opportunities for growth and differentiation. Market dynamics reveal a robust ecosystem driven by consumer demand for smart, efficient, and sustainable household solutions that enhance daily living experiences while reducing environmental impact.

Strategic positioning for success in this evolving market requires balancing innovation investment with operational efficiency, premium product development with value segment competitiveness, and technology advancement with user-friendly design. Companies that successfully navigate these challenges while building comprehensive smart home ecosystems will capture disproportionate market share and customer loyalty in the years ahead.

Future success will depend on the ability to anticipate and respond to changing consumer preferences, regulatory requirements, and technological possibilities while maintaining the reliability and performance standards that define appliance industry excellence. The convergence of sustainability, connectivity, and personalization represents both the greatest opportunity and the most significant challenge facing market participants as they shape the future of home appliance innovation in North America.

What is Home Appliance?

Home appliances refer to electrical or mechanical devices used in households for various tasks, such as cooking, cleaning, and food preservation. Common examples include refrigerators, washing machines, and microwaves.

What are the key players in the North America Home Appliance Market?

Key players in the North America Home Appliance Market include Whirlpool Corporation, General Electric, Samsung Electronics, and LG Electronics, among others.

What are the main drivers of growth in the North America Home Appliance Market?

The growth of the North America Home Appliance Market is driven by factors such as increasing consumer demand for energy-efficient appliances, advancements in smart home technology, and a growing focus on convenience and time-saving solutions.

What challenges does the North America Home Appliance Market face?

Challenges in the North America Home Appliance Market include intense competition among manufacturers, fluctuating raw material prices, and changing consumer preferences towards sustainable products.

What opportunities exist in the North America Home Appliance Market?

Opportunities in the North America Home Appliance Market include the rising trend of smart home integration, the demand for eco-friendly appliances, and the potential for growth in online retail channels.

What trends are shaping the North America Home Appliance Market?

Trends in the North America Home Appliance Market include the increasing adoption of IoT-enabled devices, a shift towards minimalist designs, and a growing emphasis on energy efficiency and sustainability.

North America Home Appliance Market

| Segmentation Details | Description |

|---|---|

| Product Type | Refrigerators, Washers, Dryers, Ovens |

| Technology | Smart Appliances, Energy-Efficient, IoT-Enabled, Traditional |

| End User | Residential, Commercial, Hospitality, Retail |

| Distribution Channel | Online Retail, Specialty Stores, Wholesale, Direct Sales |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the North America Home Appliance Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.