444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

Market Overview

The mortgage lending market plays a crucial role in the global financial industry, providing individuals and businesses with the necessary funds to purchase real estate properties. It is a dynamic and ever-evolving market that is influenced by various economic factors and regulatory policies. Mortgage lending involves the provision of loans secured by real estate properties, with the property serving as collateral for the loan. This market serves as a significant driver of economic growth and stability, facilitating homeownership and real estate investment.

Meaning

Mortgage lending refers to the process of providing loans to borrowers for the purpose of purchasing or refinancing real estate properties. Lenders, such as banks, credit unions, and mortgage companies, assess the borrower’s creditworthiness, evaluate the property’s value, and determine the loan terms, including interest rates and repayment periods. The borrower then repays the loan over time, typically through monthly installments. The mortgage lender holds a lien on the property until the loan is fully repaid.

Executive Summary

The mortgage lending market has experienced significant growth and transformation in recent years. With the increasing demand for homeownership, favorable interest rates, and government initiatives to support the housing market, the mortgage lending industry has witnessed a surge in activity. However, this market also faces challenges, such as changing regulations, economic uncertainties, and the impact of technological advancements. To succeed in this competitive landscape, mortgage lenders need to adapt to the evolving market conditions and provide innovative solutions to meet the needs of borrowers.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Market Drivers

Market Restraints

Market Opportunities

Market Dynamics

The mortgage lending market is influenced by a complex interplay of factors, including economic conditions, regulatory policies, demographic trends, and technological advancements. These dynamics shape the market landscape, drive competition, and impact customer preferences. Mortgage lenders need to adapt and respond to these dynamics to remain competitive and meet the evolving needs of borrowers.

Regional Analysis

The mortgage lending market varies across regions due to differences in economic conditions, regulatory frameworks, cultural factors, and housing market dynamics. While some regions experience robust mortgage lending activity, others may face challenges such as limited access to credit or volatile housing markets. A comprehensive regional analysis is necessary to understand the specific dynamics and opportunities within each market.

Competitive Landscape

Leading Companies in the Mortgage Lending Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

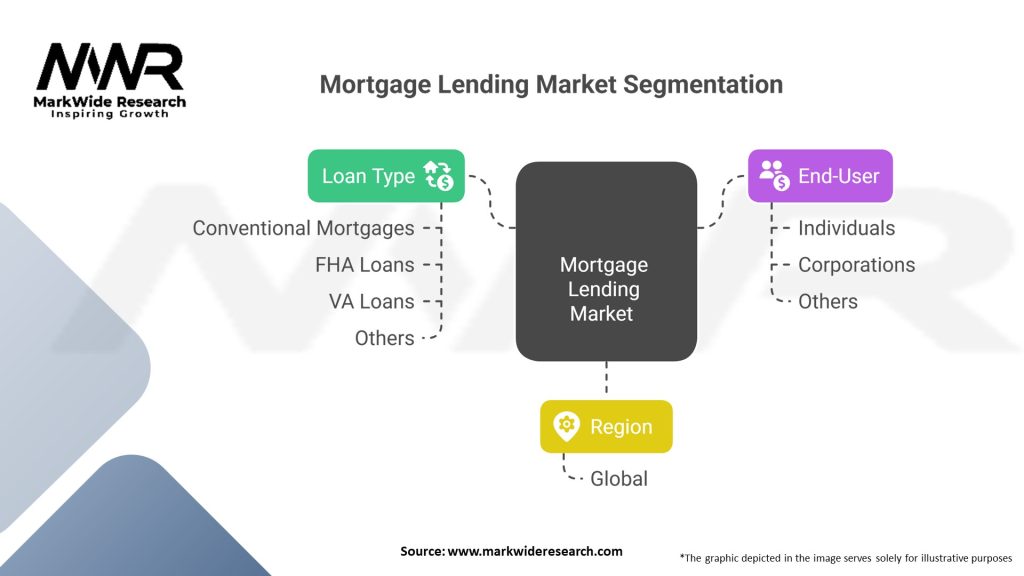

Segmentation

The mortgage lending market can be segmented based on various criteria, including loan type, borrower profile, property type, and geographical location. Segmentation allows lenders to target specific customer segments, customize their offerings, and effectively address the unique needs and preferences of different borrower groups.

Category-wise Insights

Key Benefits for Industry Participants and Stakeholders

SWOT Analysis

Market Key Trends

Covid-19 Impact

The COVID-19 pandemic had a significant impact on the mortgage lending market. The initial phase of the pandemic caused economic uncertainties, disrupted financial markets, and led to job losses and income instability for many borrowers. As a result, mortgage lenders faced increased delinquencies and forbearance requests, while tightening lending standards to mitigate risks.

However, the mortgage lending market rebounded as governments and central banks implemented stimulus measures, such as interest rate cuts and mortgage forbearance programs. These initiatives aimed to support borrowers and maintain stability in the housing market. Additionally, low-interest rates and changing housing preferences drove a surge in refinancing activity.

The pandemic also accelerated digital transformation in the mortgage lending industry. Lenders rapidly adopted remote and digital processes to ensure business continuity and provide contactless mortgage experiences for borrowers. The shift towards digital solutions and remote transactions is expected to continue even after the pandemic subsides.

Key Industry Developments

Analyst Suggestions

Future Outlook

The future of the mortgage lending market is expected to be shaped by technological advancements, changing demographics, regulatory reforms, and economic conditions. The adoption of digital solutions, data analytics, and artificial intelligence will continue to drive efficiency and improve customer experiences. The focus on sustainable practices and green mortgages is likely to gain further traction. Additionally, lenders will need to navigate evolving regulatory landscapes and adapt to changing borrower preferences and market dynamics to remain competitive in the industry.

Conclusion

The mortgage lending market is a vital component of the global financial industry, facilitating homeownership and supporting the real estate sector. It is influenced by various factors, including economic conditions, regulatory policies, technological advancements, and customer preferences. The market presents opportunities for lenders to grow their loan portfolios, embrace digital transformation, and cater to emerging markets and underserved customer segments. However, mortgage lenders must navigate challenges such as economic uncertainties, stringent regulations, and changing market dynamics. By embracing innovation, prioritizing risk management, and understanding customer needs, lenders can position themselves for success in the evolving mortgage lending landscape.

What is Mortgage Lending?

Mortgage lending refers to the process of providing loans to individuals or businesses to purchase real estate, where the property itself serves as collateral. This sector includes various types of loans, such as fixed-rate mortgages, adjustable-rate mortgages, and government-backed loans.

What are the key players in the Mortgage Lending Market?

Key players in the Mortgage Lending Market include large financial institutions like Wells Fargo, JPMorgan Chase, and Bank of America, as well as specialized mortgage lenders such as Quicken Loans and Rocket Mortgage, among others.

What are the main drivers of growth in the Mortgage Lending Market?

The main drivers of growth in the Mortgage Lending Market include low interest rates, increasing homebuyer demand, and favorable government policies that encourage home ownership. Additionally, the rise of digital mortgage platforms has made the lending process more accessible.

What challenges does the Mortgage Lending Market face?

The Mortgage Lending Market faces challenges such as regulatory compliance, fluctuating interest rates, and economic uncertainties that can affect borrower confidence. Additionally, rising home prices can limit affordability for potential buyers.

What opportunities exist in the Mortgage Lending Market?

Opportunities in the Mortgage Lending Market include the expansion of online lending platforms, the development of innovative mortgage products, and the potential for increased lending to underserved communities. These factors can enhance market accessibility and customer engagement.

What trends are shaping the Mortgage Lending Market?

Trends shaping the Mortgage Lending Market include the growing use of technology in the application process, the rise of alternative lending models, and an increased focus on sustainability in lending practices. These trends are transforming how lenders interact with borrowers and assess risk.

Mortgage Lending Market

| Segmentation Details | Details |

|---|---|

| Loan Type | Conventional Mortgages, FHA Loans, VA Loans, Others |

| End-User | Individuals, Corporations, Others |

| Region | Global |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading Companies in the Mortgage Lending Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

North America

o US

o Canada

o Mexico

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA