Montenegro’s home mortgage finance market has been experiencing significant growth in recent years. As the country’s economy strengthens and real estate demand rises, the mortgage market has become an essential component of the financial sector. This market overview aims to provide a comprehensive analysis of Montenegro’s home mortgage finance market, including key insights, market dynamics, competitive landscape, and future outlook.

Meaning

The home mortgage finance market refers to the sector that facilitates the provision of loans to individuals or families seeking to purchase residential properties. In Montenegro, this market encompasses various financial institutions, including banks, credit unions, and specialized mortgage lenders, which offer mortgage products to potential homebuyers. These loans are secured by the property being purchased, serving as collateral.

Executive Summary

Montenegro’s home mortgage finance market has experienced steady growth in recent years, driven by factors such as a growing economy, increasing disposable income, and favorable government policies. The market provides individuals and families with the necessary financial means to acquire residential properties and has become an integral part of the country’s real estate sector. However, challenges such as regulatory constraints and changing interest rates pose potential risks. Despite these challenges, the market presents significant opportunities for investors and industry participants, fueled by increasing demand and the potential for innovation.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Montenegro’s home mortgage finance market has witnessed substantial growth in line with the country’s economic development and rising demand for residential properties.

The market is dominated by commercial banks, which offer a wide range of mortgage products to cater to different customer segments.

Low interest rates and favorable lending conditions have encouraged prospective homebuyers to enter the market, leading to increased mortgage loan applications and approvals.

Government initiatives and regulations aimed at promoting affordable housing have played a crucial role in boosting the mortgage finance market.

The market faces challenges such as changing interest rates, stringent lending regulations, and potential risks associated with the real estate market.

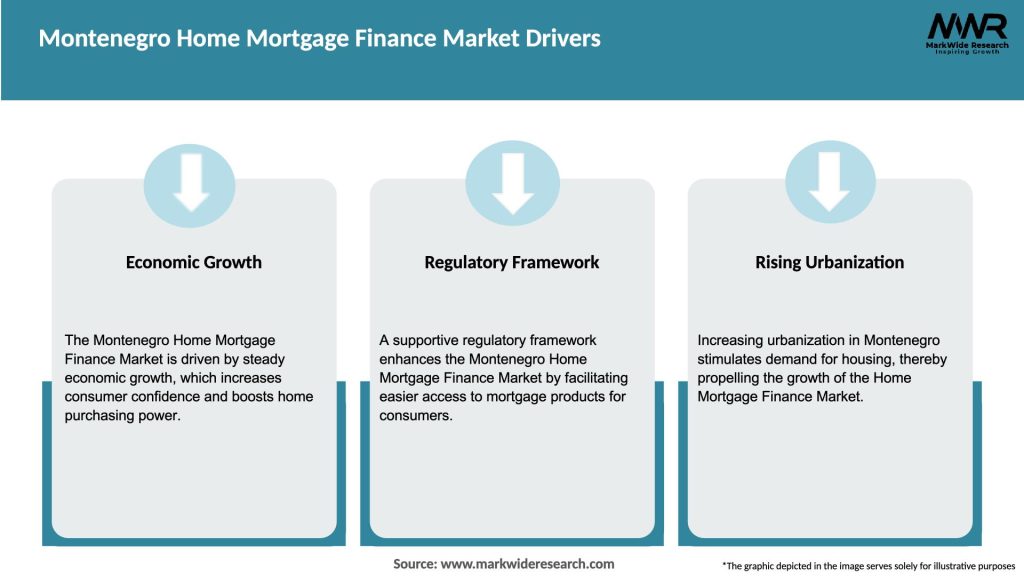

Market Drivers

Several key drivers contribute to the growth of Montenegro’s home mortgage finance market:

Economic Growth: Montenegro has experienced steady economic growth, leading to increased disposable income and improved living standards. This has fueled demand for residential properties and subsequently driven the mortgage finance market.

Low Interest Rates: Favorable interest rates offered by financial institutions have incentivized potential homebuyers to invest in property. Low borrowing costs make homeownership more affordable and attractive, stimulating market growth.

Government Initiatives: The government has introduced various initiatives to promote affordable housing and homeownership. These include subsidized mortgage programs, down payment assistance, and tax incentives, all of which have encouraged individuals and families to enter the market.

Urbanization and Demographic Trends: Urbanization and changing demographics, including a growing middle class and an increasing number of young professionals, have led to higher demand for housing. This trend has significantly impacted the mortgage finance market, creating new opportunities for lenders and investors.

Market Restraints

Despite the positive growth trajectory, Montenegro’s home mortgage finance market faces several challenges and restraints:

Regulatory Constraints: Stringent lending regulations, imposed to mitigate risks associated with mortgage lending, can limit market expansion. These regulations aim to ensure responsible lending practices but may lead to reduced accessibility to mortgage loans for certain individuals or segments.

Interest Rate Risks: Fluctuating interest rates can impact borrowers’ affordability and mortgage repayment capacity. If interest rates increase significantly, borrowers may face financial strain, leading to potential defaults and market instability.

Real Estate Market Volatility: The real estate market is subject to price fluctuations and cyclical trends. Market volatility and potential price corrections can affect borrowers’ property values, loan-to-value ratios, and lenders’ collateral security.

Economic Uncertainty: Economic downturns or instability can impact borrowers’ income stability, creditworthiness, and ability to repay mortgage loans. Uncertain economic conditions may result in reduced demand for housing and a slowdown in the mortgage finance market.

Market Opportunities

Despite the challenges, Montenegro’s home mortgage finance market presents several opportunities for industry participants and stakeholders:

Untapped Market Potential: The country’s mortgage market is still relatively underdeveloped compared to more mature economies. This presents an opportunity for lenders and investors to tap into a growing market and expand their operations.

Technology Adoption: The mortgage finance sector can benefit from technological advancements, such as digital mortgage application processes, automated underwriting, and online property valuation tools. Embracing such innovations can enhance efficiency, streamline operations, and improve the overall customer experience.

Green Mortgages: With an increasing focus on sustainable development, the market can explore opportunities in green mortgages. These loans incentivize energy-efficient homes and environmentally friendly construction, aligning with global sustainability goals and attracting environmentally conscious borrowers.

Diverse Customer Segments: There is room for catering to diverse customer segments, including first-time homebuyers, self-employed individuals, and expatriates. Tailoring mortgage products and services to meet the specific needs of these segments can unlock new market opportunities.

Market Dynamics

The home mortgage finance market in Montenegro is driven by a combination of economic, regulatory, and demographic factors. Economic growth, low interest rates, and government initiatives have stimulated market demand. However, regulatory constraints, interest rate risks, and real estate market volatility pose challenges. Opportunities lie in the untapped market potential, technology adoption, green mortgages, and diverse customer segments. Monitoring and adapting to market dynamics will be crucial for industry participants to navigate the evolving landscape successfully.

Regional Analysis

The home mortgage finance market in Montenegro exhibits regional variations influenced by factors such as urbanization, demographics, and economic development. Major urban centers, including Podgorica and coastal cities such as Budva and Tivat, attract higher demand for residential properties and mortgage financing. These regions benefit from infrastructure development, tourism, and investment, leading to increased real estate activities. In contrast, rural areas may have different dynamics with lower mortgage demand and a focus on agricultural or small-scale property purchases.

Competitive Landscape

Leading companies in the Montenegro Home Mortgage Finance Market:

Atlas Banka AD Podgorica

Crnogorska Komercijalna Banka

Hypo-Alpe-Adria-Bank AD Podgorica

NLB Montenegrobanka AD Podgorica

Hipotekarna Banka AD Podgorica

Societe Generale Montenegro

Erste Bank AD Podgorica

Invest Bank Montenegro AD Podgorica

ZIRAAT BANK Montenegro AD Podgorica

ProCredit Bank Montenegro AD Podgorica

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Segmentation

Montenegro’s home mortgage finance market can be segmented based on various criteria, including borrower profiles, loan types, and property categories:

Borrower Profiles: Segments may include first-time homebuyers, salaried employees, self-employed individuals, and expatriates. Each segment may have distinct mortgage requirements and eligibility criteria.

Loan Types: Segmentation can involve categorizing loans into fixed-rate mortgages, adjustable-rate mortgages, interest-only mortgages, and government-subsidized mortgages. Different loan types cater to borrowers’ preferences and risk profiles.

Property Categories: The market can be segmented based on property types, such as apartments, single-family homes, vacation homes, and commercial properties. Each category may have specific financing needs and associated risks.

Category-wise Insights

First-Time Homebuyers: This segment represents individuals or families purchasing their first residential property. They often require mortgage products with lower down payment requirements, affordable interest rates, and guidance throughout the homebuying process.

Self-Employed Individuals: Self-employedindividuals face unique challenges when it comes to obtaining mortgage financing. They may require specialized mortgage products that consider their variable income sources and financial documentation requirements.

Expatriates: Foreign nationals residing in Montenegro may seek mortgage financing for property purchases. Lenders can cater to this segment by offering mortgage products that accommodate their specific circumstances, such as income from abroad and residency status.

Luxury Properties: Montenegro’s real estate market includes high-end luxury properties, particularly in coastal regions. Lenders can develop mortgage products tailored to the unique needs of buyers in this segment, such as higher loan amounts and customized repayment terms.

Affordable Housing: The market presents opportunities to provide mortgage financing for affordable housing initiatives. Lenders can collaborate with government programs or non-profit organizations to offer subsidized mortgage products, down payment assistance, or favorable interest rates for low-income individuals and families.

Key Benefits for Industry Participants and Stakeholders

Industry participants and stakeholders in Montenegro’s home mortgage finance market can expect several benefits:

Revenue Growth: With the increasing demand for residential properties, lenders and financial institutions can experience revenue growth through mortgage loan origination and related services.

Portfolio Diversification: Mortgage lending allows financial institutions to diversify their loan portfolios and mitigate risks associated with other lending segments. A well-balanced portfolio can enhance stability and profitability.

Customer Relationships: Engaging in mortgage lending fosters long-term customer relationships. Successful mortgage experiences can lead to cross-selling opportunities, such as insurance products, investment services, and future refinancing or home equity products.

Market Differentiation: Developing innovative mortgage products and services can differentiate lenders in a competitive market. Differentiation can attract new customers and improve customer retention.

SWOT Analysis

Montenegro’s home mortgage finance market can be analyzed through a SWOT (Strengths, Weaknesses, Opportunities, and Threats) analysis:

Strengths:

Strong economic growth and rising disposable income

Favorable government policies promoting affordable housing

Growing demand for residential properties

Availability of established financial institutions with mortgage expertise

Weaknesses:

Stringent lending regulations limiting accessibility to mortgage loans

Vulnerability to real estate market volatility and potential price corrections

Limited market size compared to more mature economies

Opportunities:

Untapped market potential and room for market expansion

Technological advancements for improved customer experience and operational efficiency

Green mortgages and sustainability-focused lending opportunities

Tailored products for diverse customer segments, including expatriates and self-employed individuals

Threats:

Changing interest rates and interest rate risks impacting borrower affordability

Regulatory constraints affecting lending practices and market growth

Economic downturns or instability impacting borrowers’ repayment capacity

Competition from existing and emerging market players

Market Key Trends

Several key trends shape Montenegro’s home mortgage finance market:

Digital Transformation: The market is witnessing a shift towards digital mortgage processes, such as online applications, electronic document submission, and automated underwriting. This trend improves efficiency, reduces processing time, and enhances the overall customer experience.

Sustainable Financing: Increasing awareness of environmental sustainability has led to the emergence of green mortgages. These loans incentivize energy-efficient homes and eco-friendly construction, aligning with global sustainability goals and attracting environmentally conscious borrowers.

Customized Mortgage Products: Lenders are focusing on developing mortgage products tailored to specific borrower segments, such as first-time homebuyers, expatriates, and self-employed individuals. These products address the unique needs and challenges of each segment, fostering greater accessibility to mortgage financing.

Rise of Fintech Lenders: The mortgage finance market is witnessing the emergence of fintech lenders, leveraging technology and data analytics to streamline processes and offer competitive mortgage products. These lenders often provide faster approval times, innovative underwriting approaches, and user-friendly digital platforms.

Covid-19 Impact

The COVID-19 pandemic has had significant implications for Montenegro’s home mortgage finance market:

Economic Slowdown: The pandemic’s impact on the economy, including lockdown measures and reduced tourism activity, has affected borrowers’ income stability and repayment capacity. Lenders have experienced increased delinquencies and loan defaults.

Government Support: The government implemented various economic stimulus measures to support businesses and individuals during the pandemic. These measures, such as loan payment deferrals and mortgage moratoriums, aimed to alleviate financial burdens for borrowers and mitigate risks for lenders.

Increased Digitalization: The pandemic accelerated the digital transformation of the mortgage finance industry. Lenders adopted remote work practices, digital mortgage processes, and virtual property appraisals to ensure continuity in loan origination and servicing.

Shift in Demand: The pandemic influenced housing preferences, with increased interest in suburban and rural areas as remote work became more prevalent. This shift in demand patterns impacted property prices and mortgage financing requirements.

Key Industry Developments

Several notable developments have shaped Montenegro’s home mortgage finance market:

Government Housing Initiatives: The government introduced initiatives to promote affordable housing, such as subsidized mortgage programs, rent-to-own schemes, and down payment assistance for first-time homebuyers. These initiatives aim to address the housing affordability gap and stimulate market growth.

Mortgage Market Liberalization: Montenegro has taken steps to liberalize the mortgage market by introducing new regulations to enhance transparency, promote competition, and facilitate foreign investment in real estate. These measures aim to attract international buyers and boost the overall mortgage market.

Technological Advancements: Financial institutions have invested in technology to digitize mortgage processes, improve efficiency, and enhance customer experience. This includes online mortgage applications, digital document management, and automated underwriting systems.

Collaboration between Banks and Real Estate Developers: Banks and real estate developers have collaborated to offer bundled mortgage and property purchase packages. These collaborations simplify the homebuying process, provide financing options, and promote real estate sales.

Analyst Suggestions

Based on market trends and dynamics, analysts suggest the following strategies for industry participants:

Embrace Technological Advancements: Invest in digital mortgage platforms, automation tools, and data analytics to streamline operations, improve customer experience, and enhance risk management capabilities.

Innovate Mortgage Products: Develop specialized mortgage products targeting underserved segments, such as expatriates, self-employed individuals, and first-time homebuyers. Tailor products to address specific borrower needs and provide flexibility in eligibility criteria.

Focus on Risk Management: Maintain stringent risk assessment and underwriting practices to ensure responsible lending. Regularly review and update credit policies to align with changing market conditions and regulatory requirements.

Collaborate and Diversify: Explore partnerships with real estate developers, architects, and property listing platforms to offer comprehensive mortgage solutions and expand market reach. Diversify loan portfolios to mitigate risks associated with specific segments or property categories.

Future Outlook

Looking ahead, Montenegro’s home mortgage finance market is expected to continue its growth trajectory, driven by factors such as economic development, increased urbanization, and government support. The market will likely witness greater digitization, enhanced customer experiences, and innovative mortgage products. However, industry participants must remain attentive to evolving market dynamics, changing interest rates, and regulatory developments. Navigating potential challenges and capitalizing on emerging opportunities will be critical for sustained success in the future mortgage finance landscape.

Conclusion

Montenegro’s home mortgage finance market is experiencing steady growth, driven by economic development, low interest rates, and government initiatives. The market provides individuals and families with the means to acquire residential properties and offers opportunities for lenders and investors. However, challenges such as regulatory constraints,interest rate risks, and real estate market volatility exist. By embracing technological advancements, developing tailored mortgage products, and focusing on risk management, industry participants can navigate the market successfully. The future outlook is positive, with expected growth, greater digitization, and innovative mortgage solutions. Monitoring market dynamics, adapting to regulatory changes, and capitalizing on emerging trends will be crucial for sustained success in Montenegro’s home mortgage finance market.

What is Home Mortgage Finance?

Home Mortgage Finance refers to the various financial products and services that facilitate the borrowing of funds to purchase residential properties. This includes loans, mortgages, and other financing options tailored for homebuyers.

What are the key players in the Montenegro Home Mortgage Finance Market?

Key players in the Montenegro Home Mortgage Finance Market include local banks such as Crnogorska Komercijalna Banka and NLB Banka, as well as international financial institutions that offer mortgage products. These companies compete to provide attractive terms and services to homebuyers.

What are the growth factors driving the Montenegro Home Mortgage Finance Market?

The Montenegro Home Mortgage Finance Market is driven by factors such as increasing urbanization, a growing middle class, and favorable interest rates. Additionally, government initiatives to promote home ownership contribute to market growth.

What challenges does the Montenegro Home Mortgage Finance Market face?

Challenges in the Montenegro Home Mortgage Finance Market include economic instability, fluctuating property values, and regulatory hurdles. These factors can impact lending practices and consumer confidence in the housing market.

What opportunities exist in the Montenegro Home Mortgage Finance Market?

Opportunities in the Montenegro Home Mortgage Finance Market include the potential for digital mortgage solutions and the expansion of financing options for first-time homebuyers. Additionally, increasing foreign investment in real estate presents new avenues for growth.

What trends are shaping the Montenegro Home Mortgage Finance Market?

Trends in the Montenegro Home Mortgage Finance Market include the rise of online mortgage applications and the integration of technology in the lending process. There is also a growing emphasis on sustainable housing solutions and energy-efficient properties.

Leading companies in the Montenegro Home Mortgage Finance Market:

Atlas Banka AD Podgorica

Crnogorska Komercijalna Banka

Hypo-Alpe-Adria-Bank AD Podgorica

NLB Montenegrobanka AD Podgorica

Hipotekarna Banka AD Podgorica

Societe Generale Montenegro

Erste Bank AD Podgorica

Invest Bank Montenegro AD Podgorica

ZIRAAT BANK Montenegro AD Podgorica

ProCredit Bank Montenegro AD Podgorica

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.