The Military EO and IR Sensors Market encompasses the development, production, and deployment of electro-optical (EO) and infrared (IR) sensors for military applications. These sensors play a critical role in providing situational awareness, surveillance, target acquisition, and tracking capabilities to military forces across land, sea, and air domains. With the increasing complexity of modern warfare and the growing demand for advanced sensor technologies, the military EO and IR sensors market continue to evolve, offering innovative solutions to address emerging threats and operational requirements.

Meaning

Military EO and IR sensors are advanced electronic devices designed to detect, identify, and track targets using electromagnetic radiation in the visible, infrared, and thermal spectra. These sensors are utilized in a wide range of military platforms, including unmanned aerial vehicles (UAVs), helicopters, armored vehicles, ships, and soldier systems, to enhance situational awareness, reconnaissance, and surveillance capabilities. Military EO and IR sensors enable military forces to operate effectively in diverse environments and combat scenarios, providing crucial information for decision-making and mission execution.

Executive Summary

The Military EO and IR Sensors Market have experienced significant growth in recent years, driven by the increasing adoption of unmanned systems, the modernization of military fleets, and the growing emphasis on network-centric warfare capabilities. Advancements in sensor technology, such as higher resolution, longer detection ranges, and enhanced integration with other sensors and platforms, have expanded the operational capabilities of military forces. However, challenges such as defense budget constraints, export control regulations, and technological obsolescence pose potential hurdles to market growth. Nevertheless, opportunities abound for military EO and IR sensor manufacturers to innovate, collaborate, and address evolving defense requirements in the dynamic global security landscape.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Rise of Unmanned Systems: The proliferation of unmanned systems, including UAVs, unmanned ground vehicles (UGVs), and unmanned maritime vehicles (UMVs), drives the demand for EO and IR sensors for surveillance, reconnaissance, and target acquisition missions.

Integration of Sensor Fusion: The integration of EO and IR sensors with other sensor modalities, such as radar, LIDAR, and electronic warfare (EW) systems, enables multi-sensor fusion capabilities, enhancing detection, tracking, and classification of targets in complex and contested environments.

Miniaturization and SWaP-C Optimization: Advances in miniaturization, size, weight, power, and cost (SWaP-C) optimization enable the integration of EO and IR sensors into smaller platforms, such as unmanned aerial vehicles (UAVs), soldier-worn systems, and tactical vehicles, expanding their operational versatility and accessibility.

Enhanced Connectivity and Data Sharing: The adoption of network-centric warfare concepts and digital battlefield architectures facilitates enhanced connectivity and data sharing capabilities, enabling seamless integration of EO and IR sensors into wider command, control, communications, computers, intelligence, surveillance, and reconnaissance (C4ISR) networks.

Market Drivers

Modernization of Military Fleets: The ongoing modernization efforts by defense forces worldwide, aimed at upgrading aging platforms with advanced sensor technologies, drive the demand for EO and IR sensors to enhance situational awareness, lethality, and survivability capabilities.

Counterinsurgency and Counterterrorism Operations: The rise of asymmetric threats and non-state actors necessitates the use of EO and IR sensors for counterinsurgency, counterterrorism, and stabilization operations, enabling military forces to conduct precision targeting and intelligence gathering in urban and asymmetric warfare environments.

Border and Maritime Security: The need to secure borders, coastlines, and maritime domains against illicit activities, smuggling, piracy, and illegal migration drives the adoption of EO and IR sensors for border surveillance, maritime patrol, and coastal defense applications.

Rapid Technological Advancements: Continuous advancements in EO and IR sensor technology, such as higher resolutions, improved sensitivity, and enhanced signal processing algorithms, enable the development of next-generation sensors with enhanced performance, reliability, and affordability.

Market Restraints

Defense Budget Constraints: Budgetary constraints and defense spending reductions in key defense markets pose challenges to military EO and IR sensor manufacturers, limiting investment in research and development, procurement programs, and technology upgrades.

Export Control Regulations: Stringent export control regulations and licensing requirements for sensitive defense technologies restrict the international transfer of EO and IR sensors, limiting market access and export opportunities for manufacturers.

Technology Obsolescence: The rapid pace of technological obsolescence in EO and IR sensor technology poses challenges to manufacturers, requiring continuous investment in research and development to stay ahead of emerging threats and maintain technological superiority.

Cybersecurity Vulnerabilities: The increasing connectivity and digitalization of EO and IR sensor systems expose them to cybersecurity vulnerabilities, including hacking, data breaches, and electronic warfare (EW) attacks, necessitating robust cybersecurity measures to safeguard sensitive information and mission-critical capabilities.

Market Opportunities

Counter-Drone Solutions: The proliferation of unmanned aerial threats, including drones and UAVs, presents opportunities for military EO and IR sensor manufacturers to develop counter-drone solutions, including detection, tracking, and neutralization systems, to protect military installations, critical infrastructure, and deployed forces.

Urban Warfare Solutions: The urbanization of conflict and the prevalence of asymmetric threats in urban environments create demand for EO and IR sensors optimized for urban warfare operations, providing enhanced situational awareness, targeting, and surveillance capabilities for military forces operating in complex terrain.

Maritime Surveillance Systems: The growing maritime security challenges, including piracy, illegal fishing, and maritime smuggling, drive the demand for EO and IR sensors for maritime surveillance, coastal patrol, and maritime domain awareness applications, enabling navies and coast guards to protect maritime borders and enforce maritime laws.

Integrated Sensor Suites: The integration of EO and IR sensors into integrated sensor suites and multi-domain sensor platforms, such as airborne ISR aircraft, naval surface vessels, and ground-based command posts, offers opportunities for manufacturers to provide comprehensive sensor solutions that address diverse mission requirements and operational scenarios.

Market Dynamics

The Military EO and IR Sensors Market operate within a dynamic environment influenced by factors such as evolving threat landscapes, defense budgets, technological advancements, geopolitical tensions, and regulatory frameworks. Manufacturers must navigate these dynamics by investing in innovation, strategic partnerships, international collaborations, and customer relationships to sustain growth and competitiveness in the global defense market.

Regional Analysis

North America: North America dominates the Military EO and IR Sensors Market, driven by significant defense spending, technological leadership, and a robust industrial base comprising major sensor manufacturers, defense primes, and government research institutions.

Europe: Europe is a key region for military EO and IR sensor manufacturing, supported by defense modernization programs, NATO interoperability requirements, and a network of defense contractors, research centers, and government agencies.

Asia-Pacific: Asia-Pacific presents opportunities for military EO and IR sensor manufacturers, driven by regional security challenges, territorial disputes, and the modernization of armed forces across countries such as China, India, Japan, South Korea, and Australia.

Middle East and Africa: The Middle East and Africa region exhibit demand for military EO and IR sensors driven by regional conflicts, terrorism threats, and defense procurement initiatives by governments seeking to enhance their military capabilities and safeguard national security interests.

Competitive Landscape

Leading Companies in the Military EO and IR Sensors Market:

Raytheon Technologies Corporation

Lockheed Martin Corporation

Thales Group

FLIR Systems, Inc.

Leonardo S.p.A.

BAE Systems plc

L3Harris Technologies, Inc.

Northrop Grumman Corporation

Elbit Systems Ltd.

Rheinmetall AG

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

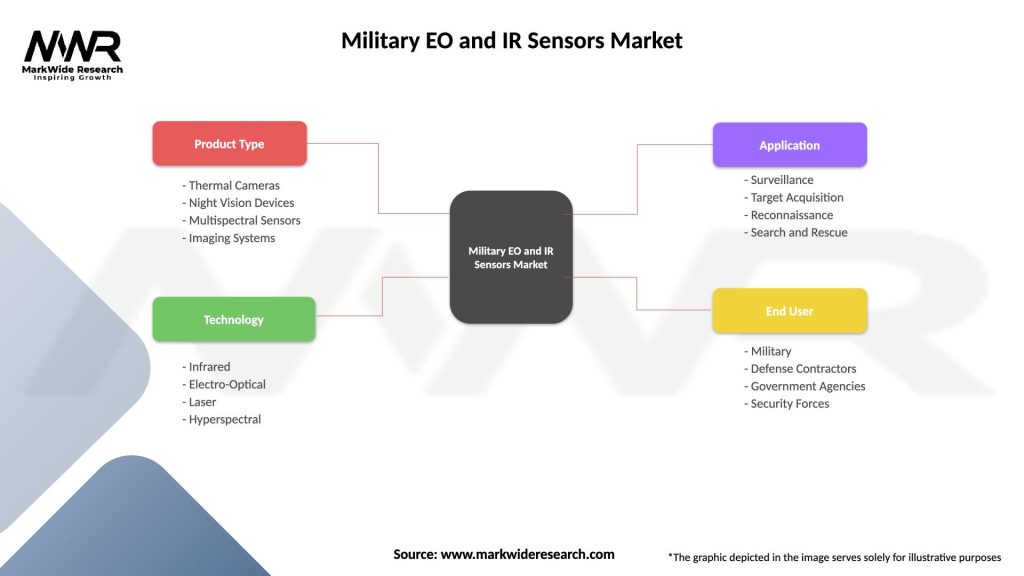

Segmentation

The Military EO and IR Sensors Market can be segmented based on various factors, including technology type, platform, wavelength band, application, and geography. Common segmentation categories include:

Technology Type: EO sensors, IR sensors, multispectral sensors, hyperspectral sensors, thermal imaging sensors, and laser rangefinders.

Platform: Airborne, ground-based, naval, and soldier-worn platforms.

Application: Surveillance, reconnaissance, target acquisition, fire control, navigation, and situational awareness.

Segmentation enables a more granular analysis of market trends, customer preferences, and competitive dynamics, facilitating targeted marketing strategies, product development initiatives, and market expansion efforts.

Category-wise Insights

Unmanned Systems Sensors: EO and IR sensors for unmanned aerial vehicles (UAVs), unmanned ground vehicles (UGVs), and unmanned maritime vehicles (UMVs) offer surveillance, reconnaissance, and target acquisition capabilities for autonomous and remotely operated platforms.

Ground-based Sensors: EO and IR sensors deployed on ground-based platforms, including fixed installations, mobile surveillance systems, and border security units, provide situational awareness, perimeter defense, and force protection capabilities.

Naval Sensors: EO and IR sensors integrated into naval vessels, including ships, submarines, and unmanned surface vessels (USVs), offer maritime surveillance, target tracking, and anti-ship missile defense capabilities for naval operations and maritime security missions.

Soldier Systems Sensors: EO and IR sensors incorporated into soldier-worn systems, including helmets, weapon sights, and handheld devices, provide individual soldiers with enhanced situational awareness, target acquisition, and night vision capabilities for dismounted operations.

Key Benefits for Industry Participants and Stakeholders

Enhanced Situational Awareness: Military EO and IR sensors provide enhanced situational awareness capabilities, enabling military forces to detect, identify, and track targets in diverse environments and operational scenarios.

Improved Target Acquisition: EO and IR sensors facilitate target acquisition and engagement, allowing military forces to accurately engage enemy threats, conduct precision strikes, and minimize collateral damage during combat operations.

Force Protection: EO and IR sensors contribute to force protection by detecting and mitigating threats, providing early warning of enemy activity, and enhancing the survivability of military personnel and assets.

Mission Effectiveness: Military EO and IR sensors enhance mission effectiveness by providing real-time intelligence, surveillance, and reconnaissance (ISR) capabilities, enabling informed decision-making and mission planning for military commanders.

Operational Flexibility: EO and IR sensors offer operational flexibility by providing day and night vision capabilities, enabling military forces to conduct operations in low-light conditions, adverse weather, and complex terrain with reduced risk and increased effectiveness.

SWOT Analysis

Strengths:

Technological expertise in EO and IR sensor design, development, and manufacturing.

Established track record of delivering high-performance sensor solutions for military applications.

Strategic partnerships with defense contractors, government agencies, and research institutions.

Global presence and customer support network for sales, distribution, and aftermarket services.

Weaknesses:

Dependence on defense procurement budgets and government contracts for revenue.

Vulnerability to defense spending fluctuations and geopolitical tensions impacting market demand.

Intense competition from domestic and international sensor manufacturers offering similar products.

Regulatory compliance requirements and export control restrictions limiting market access and international expansion.

Opportunities:

Advancements in sensor technology, including higher resolution, longer detection range, and improved reliability.

Emerging applications for military EO and IR sensors in urban warfare, counterinsurgency, and maritime surveillance.

Collaboration with defense primes, research institutions, and technology startups on joint development programs.

Expansion into emerging markets, including Asia-Pacific, Middle East, and Africa, for defense procurement opportunities.

Threats:

Defense budget constraints and spending reductions impacting defense procurement programs and investments.

Rapid technological obsolescence and disruptive innovations from competitors and alternative sensor technologies.

Regulatory challenges, including export control regulations, ITAR compliance, and cybersecurity vulnerabilities.

Geopolitical tensions, regional conflicts, and defense trade restrictions affecting international sales and market expansion.

Market Key Trends

Multi-Sensor Integration: The integration of EO and IR sensors with other sensor modalities, including radar, electronic warfare (EW), and acoustic sensors, enables multi-sensor fusion capabilities for enhanced situational awareness and target detection.

Compact and Lightweight Sensors: Advances in sensor miniaturization and packaging enable the development of compact and lightweight EO and IR sensors for integration into unmanned systems, soldier-worn systems, and small tactical platforms.

Network-Centric Warfare: The adoption of network-centric warfare concepts and digital battlefield architectures drives the demand for networked EO and IR sensor systems capable of seamless integration into wider command, control, communications, computers, intelligence, surveillance, and reconnaissance (C4ISR) networks.

Artificial Intelligence and Machine Learning: The integration of artificial intelligence (AI) and machine learning (ML) algorithms into EO and IR sensor systems enables autonomous target recognition, pattern recognition, and decision-making capabilities, enhancing sensor performance and operational effectiveness.

Covid-19 Impact

The COVID-19 pandemic has had mixed effects on the Military EO and IR Sensors Market. While the initial disruption to supply chains, manufacturing operations, and defense procurement programs impacted market growth and investment, the subsequent recovery and resilience of defense spending, coupled with emerging security threats and geopolitical tensions, have driven demand for EO and IR sensor solutions for military applications. The pandemic has accelerated trends such as unmanned systems integration, digitalization, and remote operations, further fueling market opportunities for sensor manufacturers to innovate and adapt to evolving defense requirements.

Key Industry Developments

Next-Generation Sensor Technologies: Development of next-generation EO and IR sensor technologies, including advanced focal plane arrays (FPAs), multispectral imaging, and quantum cascade lasers (QCLs), to enhance sensor performance, sensitivity, and resolution.

Integrated Sensor Suites: Integration of EO and IR sensors into integrated sensor suites and multi-domain sensor platforms, including airborne ISR aircraft, ground-based command posts, and naval surface vessels, to provide comprehensive situational awareness and mission capabilities.

Counter-UAS Solutions: Development of counter-unmanned aerial systems (C-UAS) solutions incorporating EO and IR sensors for detection, tracking, and neutralization of hostile drones and UAVs in defense, critical infrastructure, and public safety applications.

Cyber-Resilient Sensor Systems: Enhancement of cybersecurity capabilities in EO and IR sensor systems to mitigate cyber threats, including hacking, malware, and data breaches, ensuring the integrity, confidentiality, and availability of sensitive sensor data and mission-critical capabilities.

Analyst Suggestions

Investment in R&D and Innovation: Military EO and IR sensor manufacturers should continue to invest in research and development to drive innovation, develop next-generation sensor technologies, and maintain technological leadership in the global defense market.

Collaboration and Partnerships: Foster collaboration with defense primes, government agencies, research institutions, and technology startups on joint development programs, technology transfer initiatives, and international partnerships to address emerging defense requirements and expand market opportunities.

Diversification of Product Portfolio: Expand product portfolio to offer a comprehensive range of EO and IR sensor solutions tailored to diverse mission requirements, operational scenarios, and customer needs, including integrated sensor suites, modular sensor architectures, and scalable sensor platforms.

Customer-Centric Approach: Adopt a customer-centric approach to understand end-user requirements, prioritize customer needs, and deliver tailored sensor solutions that offer maximum value, performance, and reliability for military applications.

Future Outlook

The Military EO and IR Sensors Market are poised for growth in the coming years, driven by increasing defense spending, emerging security threats, technological advancements, and the adoption of unmanned systems, network-centric warfare, and digital battlefield concepts. Despite challenges such as defense budget constraints, export control regulations, and geopolitical tensions, opportunities abound for EO and IR sensor manufacturers to innovate, collaborate, and address evolving defense requirements, ensuring continued growth and competitiveness in the global defense market.

Conclusion

The Military EO and IR Sensors Market play a critical role in enhancing the situational awareness, reconnaissance, and targeting capabilities of military forces worldwide. With advancements in sensor technology, integration with unmanned systems, and adoption of network-centric warfare concepts, EO and IR sensors are becoming indispensable assets for modern militaries operating in diverse and dynamic operational environments. While challenges such as defense budget constraints, export control regulations, and technological obsolescence remain, opportunities abound for sensor manufacturers to innovate, collaborate, and address emerging defense requirements, ensuring continued growth and competitiveness in the global defense market. By staying agile, adaptive, and customer-focused, EO and IR sensor manufacturers can navigate market dynamics, capitalize on emerging trends, and contribute to the defense and security of nations in the 21st century.

What is Military EO and IR Sensors?

Military EO and IR Sensors refer to electro-optical and infrared devices used for surveillance, targeting, and reconnaissance in military applications. These sensors are crucial for enhancing situational awareness and operational effectiveness on the battlefield.

What are the key players in the Military EO and IR Sensors Market?

Key players in the Military EO and IR Sensors Market include Raytheon Technologies, Northrop Grumman, Thales Group, and Leonardo S.p.A., among others. These companies are known for their advanced sensor technologies and solutions tailored for defense applications.

What are the main drivers of the Military EO and IR Sensors Market?

The main drivers of the Military EO and IR Sensors Market include the increasing demand for advanced surveillance systems, the need for enhanced situational awareness, and the growing focus on modernizing military capabilities. Additionally, geopolitical tensions are prompting nations to invest in advanced sensor technologies.

What challenges does the Military EO and IR Sensors Market face?

The Military EO and IR Sensors Market faces challenges such as high development costs, rapid technological advancements, and stringent regulatory requirements. Additionally, the integration of these sensors into existing military systems can be complex and resource-intensive.

What opportunities exist in the Military EO and IR Sensors Market?

Opportunities in the Military EO and IR Sensors Market include the development of next-generation sensors with improved capabilities, the integration of artificial intelligence for enhanced data analysis, and the expansion of applications in unmanned systems. These advancements can significantly enhance military operations.

What trends are shaping the Military EO and IR Sensors Market?

Trends shaping the Military EO and IR Sensors Market include the increasing use of miniaturized sensors, advancements in sensor fusion technologies, and the growing adoption of unmanned aerial vehicles (UAVs) equipped with EO and IR sensors. These trends are driving innovation and improving operational efficiency.

Leading Companies in the Military EO and IR Sensors Market:

Raytheon Technologies Corporation

Lockheed Martin Corporation

Thales Group

FLIR Systems, Inc.

Leonardo S.p.A.

BAE Systems plc

L3Harris Technologies, Inc.

Northrop Grumman Corporation

Elbit Systems Ltd.

Rheinmetall AG

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.