The Middle East Intelligent Virtual Assistant (IVA) Based Banking Market represents a significant evolution in the banking sector, leveraging artificial intelligence (AI) and natural language processing (NLP) technologies to enhance customer service, streamline operations, and drive digital transformation. Intelligent virtual assistants offer personalized assistance, proactive engagement, and efficient transactional support, reshaping the way customers interact with banks and financial institutions across the Middle East region.

Meaning

Intelligent Virtual Assistants (IVAs) in the banking sector refer to AI-powered digital assistants capable of understanding and responding to customer queries, performing transactions, providing account information, and offering personalized recommendations through natural language interactions. These virtual assistants leverage machine learning algorithms, chatbot frameworks, and voice recognition technologies to deliver seamless, intuitive, and personalized banking experiences across digital channels.

Executive Summary

The Middle East Intelligent Virtual Assistant (IVA) Based Banking Market is witnessing rapid growth driven by increasing digitization, rising customer expectations, and the growing adoption of AI-powered solutions in the banking industry. IVAs enable banks to improve customer engagement, reduce operational costs, and gain competitive advantage by delivering personalized, efficient, and responsive banking services through digital channels.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Rising Demand for Digital Banking: The Middle East region is experiencing a surge in demand for digital banking services, fueled by smartphone penetration, internet connectivity, and changing customer preferences. IVAs offer banks an opportunity to enhance their digital offerings and deliver convenient, accessible, and personalized banking experiences to customers.

Focus on Customer Experience: Banks in the Middle East are increasingly prioritizing customer experience as a key differentiator in a competitive market landscape. IVAs enable banks to deliver proactive, personalized, and context-aware interactions, enhancing customer satisfaction, loyalty, and retention.

Advancements in AI and NLP Technologies: Continuous advancements in AI and NLP technologies are driving innovation in the field of intelligent virtual assistants. Banks are leveraging these technologies to develop smarter, more conversational, and intuitive virtual assistants capable of understanding complex queries and providing accurate responses in real-time.

Integration with Omnichannel Banking: IVAs are being integrated seamlessly into omnichannel banking platforms, allowing customers to interact with virtual assistants across multiple touchpoints, including websites, mobile apps, social media platforms, and messaging channels. This omnichannel approach ensures consistency and continuity in customer interactions, regardless of the channel used.

Market Drivers

Increasing Customer Expectations: Customers in the Middle East expect banks to provide personalized, convenient, and efficient banking services tailored to their individual needs. IVAs enable banks to meet these expectations by offering proactive assistance, personalized recommendations, and instant support through digital channels.

Cost Reduction and Operational Efficiency: IVAs help banks reduce operational costs by automating routine tasks, such as account inquiries, transaction processing, and basic customer support queries. By offloading repetitive tasks to virtual assistants, banks can optimize resource allocation, improve efficiency, and focus on value-added activities.

24/7 Availability and Accessibility: IVAs provide round-the-clock availability and accessibility, allowing customers to access banking services anytime, anywhere, without the need for human intervention. This 24/7 support enhances customer satisfaction, reduces wait times, and increases convenience for customers with busy schedules or in different time zones.

Enhanced Security and Fraud Prevention: Intelligent virtual assistants incorporate advanced security features, authentication protocols, and fraud detection mechanisms to safeguard customer data and prevent unauthorized access or fraudulent activities. Banks can leverage IVAs to enhance security measures, build trust, and reassure customers about the safety of their transactions and information.

Market Restraints

Integration Challenges: Integrating IVAs into existing banking systems and legacy infrastructure poses technical challenges, including data integration, interoperability issues, and compatibility with backend systems. Banks need to invest in robust integration frameworks and API-based solutions to ensure seamless connectivity and data exchange between virtual assistants and backend systems.

Privacy and Data Confidentiality Concerns: Privacy regulations, data protection laws, and customer confidentiality concerns present challenges for banks implementing IVAs. Banks must adhere to stringent privacy standards, secure customer consent, and implement data encryption and anonymization techniques to protect sensitive customer information and maintain trust.

User Adoption and Acceptance: User adoption and acceptance of IVAs depend on factors such as user experience, usability, and perceived value. Banks need to design intuitive, user-friendly interfaces, and provide adequate training and support to encourage customer adoption and usage of virtual assistants.

Accuracy and Reliability: The accuracy and reliability of IVAs in understanding user queries, interpreting intent, and providing relevant responses can impact customer satisfaction and trust. Banks must continuously train and improve virtual assistants’ natural language processing capabilities, speech recognition accuracy, and contextual understanding to deliver accurate and reliable results.

Market Opportunities

Personalized Financial Advice: IVAs can offer personalized financial advice, product recommendations, and wealth management services based on customer preferences, financial goals, and risk profiles. Banks can leverage IVAs to enhance customer engagement, cross-sell and upsell products, and drive revenue growth through targeted recommendations.

Voice Banking and Conversational Interfaces: Voice banking and conversational interfaces enable customers to perform banking transactions, check account balances, and make payments using natural language commands and voice interactions. Banks can capitalize on the growing popularity of voice-enabled devices and smart speakers to offer voice banking services through IVAs.

Multilingual Support and Localization: The Middle East region is culturally diverse, with multiple languages and dialects spoken across different countries. IVAs can provide multilingual support and localization capabilities, catering to the linguistic preferences and cultural sensitivities of diverse customer segments in the region.

AI-Powered Analytics and Insights: IVAs generate valuable data and insights about customer preferences, behavior patterns, and transaction histories. Banks can leverage AI-powered analytics and machine learning algorithms to analyze this data, gain actionable insights, and personalize marketing campaigns, product offerings, and customer interactions.

Market Dynamics

The Middle East Intelligent Virtual Assistant (IVA) Based Banking Market operates within a dynamic ecosystem shaped by technological advancements, regulatory changes, competitive pressures, and evolving customer expectations. Understanding these dynamics is essential for banks and financial institutions to navigate market challenges, capitalize on growth opportunities, and drive innovation in the digital banking landscape.

Regional Analysis

The Middle East Intelligent Virtual Assistant (IVA) Based Banking Market exhibits regional variations in adoption rates, market maturity, and regulatory frameworks across countries in the region. Let’s explore key regional insights:

United Arab Emirates (UAE): The UAE is a leading hub for digital innovation and fintech adoption in the Middle East, with banks investing in AI-powered solutions, including IVAs, to enhance customer engagement, drive operational efficiency, and differentiate their offerings in a competitive market landscape.

Saudi Arabia: Saudi Arabia is witnessing increasing demand for digital banking services, driven by government initiatives, regulatory reforms, and the growing popularity of mobile banking apps. Banks in Saudi Arabia are leveraging IVAs to automate routine tasks, improve service quality, and deliver personalized banking experiences to customers.

Qatar: Qatar’s banking sector is embracing digital transformation, with a focus on enhancing customer experience, innovation, and agility. IVAs play a crucial role in Qatar’s digital banking strategy, enabling banks to deliver seamless, intuitive, and personalized services across digital channels, including mobile banking and online platforms.

Kuwait: Kuwait’s banking industry is undergoing rapid digitization, driven by changing customer preferences, regulatory initiatives, and competitive pressures. Banks in Kuwait are investing in AI-powered solutions such as IVAs to streamline operations, reduce costs, and offer innovative banking services tailored to customer needs.

Bahrain: Bahrain is emerging as a fintech hub in the Middle East, with a supportive regulatory environment, government initiatives, and investment in digital infrastructure. Banks in Bahrain are partnering with fintech companies to deploy AI-powered solutions like IVAs, driving innovation, and enhancing customer engagement in the banking sector.

Competitive Landscape

Leading Companies in Middle East Intelligent Virtual Assistant (IVA) Based Banking Market:

Nuance Communications, Inc.

IBM Corporation

Oracle Corporation

Google LLC

Microsoft Corporation

Amazon Web Services, Inc.

Samsung Electronics Co., Ltd.

Inbenta Technologies Inc.

Kasisto Inc.

Creative Virtual Ltd.

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

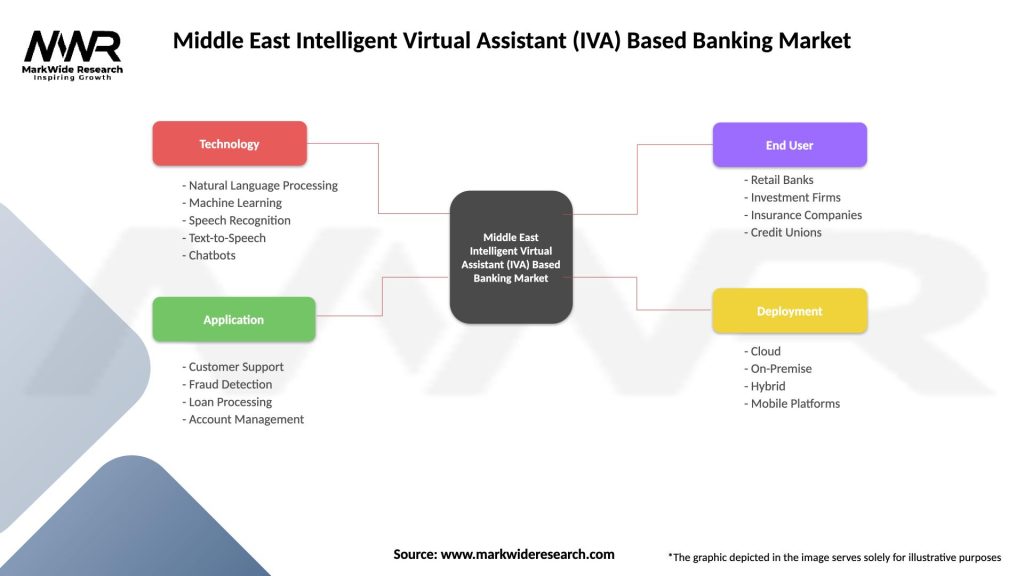

Segmentation

The Middle East Intelligent Virtual Assistant (IVA) Based Banking Market can be segmented based on various factors, including:

Technology Type: Segmentation by technology type includes text-based chatbots, voice-enabled assistants, virtual avatars, and omnichannel solutions, catering to diverse customer preferences and interaction modes.

Bank Size: Segmentation by bank size includes large multinational banks, regional banks, and community banks, each with unique requirements, scale, and resources for implementing IVAs and digital banking solutions.

Customer Segment: Segmentation by customer segment includes retail banking, corporate banking, wealth management, and private banking, targeting specific customer demographics, needs, and preferences with tailored IVAs and personalized services.

Service Offering: Segmentation by service offering includes account inquiries, fund transfers, bill payments, loan applications, investment advice, and personalized recommendations, providing a comprehensive range of banking services through IVAs.

Category-wise Insights

Customer Service and Support: IVAs offer automated customer service and support solutions, handling common queries, providing account information, and resolving issues through natural language interactions, reducing wait times and improving service quality.

Transaction Processing: IVAs enable secure and efficient transaction processing, allowing customers to transfer funds, pay bills, set up recurring payments, and perform other banking transactions through digital channels, enhancing convenience and accessibility.

Personal Financial Management: IVAs provide personal financial management tools, budgeting advice, spending insights, and financial goal tracking features to help customers manage their finances, make informed decisions, and achieve their financial objectives.

Product Recommendations: IVAs analyze customer preferences, transaction histories, and behavioral data to offer personalized product recommendations, including credit cards, loans, savings accounts, and investment products, driving cross-selling and upselling opportunities.

Key Benefits for Industry Participants and Stakeholders

The Middle East Intelligent Virtual Assistant (IVA) Based Banking Market offers several benefits for industry participants and stakeholders:

Enhanced Customer Experience: IVAs enhance customer experience by providing personalized assistance, proactive engagement, and seamless interactions across digital channels, improving satisfaction, loyalty, and retention.

Operational Efficiency: IVAs automate routine tasks, streamline operations, and reduce manual intervention, enabling banks to optimize resource allocation, improve efficiency, and lower operational costs.

24/7 Availability: IVAs provide round-the-clock availability and accessibility, allowing banks to offer instant support, handle peak loads, and serve customers across different time zones without human intervention.

Data-driven Insights: IVAs generate valuable data and insights about customer preferences, behavior patterns, and transaction histories, enabling banks to analyze customer needs, personalize offerings, and drive targeted marketing campaigns.

SWOT Analysis

A SWOT analysis provides insights into the strengths, weaknesses, opportunities, and threats of the Middle East Intelligent Virtual Assistant (IVA) Based Banking Market:

Strengths:

Advanced AI and NLP technologies

Enhanced customer engagement

Operational efficiency gains

Personalized banking experiences

Weaknesses:

Integration challenges with legacy systems

Privacy and security concerns

User adoption barriers

Reliance on third-party technology providers

Opportunities:

Growing demand for digital banking

Expansion into new customer segments

Multilingual support and localization

AI-driven analytics and insights

Threats:

Regulatory compliance requirements

Competition from fintech startups

Cybersecurity risks and data breaches

Technology obsolescence and disruption

Market Key Trends

Voice Banking and Natural Language Processing: Voice banking and NLP technologies are driving the adoption of conversational interfaces and voice-enabled virtual assistants, offering intuitive and frictionless banking experiences for customers across the Middle East region.

AI-driven Personalization: AI-driven personalization is reshaping banking interactions, with IVAs analyzing customer data, preferences, and behaviors to deliver tailored recommendations, offers, and assistance, fostering deeper customer relationships and loyalty.

Omnichannel Engagement: Omnichannel engagement strategies are gaining traction, with banks integrating IVAs seamlessly across digital touchpoints, including websites, mobile apps, messaging platforms, and social media channels, ensuring consistent and cohesive customer experiences.

Ethical AI and Responsible Banking: Ethical AI principles and responsible banking practices are guiding the development and deployment of IVAs, with banks prioritizing transparency, fairness, and accountability in AI algorithms, decision-making processes, and customer interactions.

Covid-19 Impact

The COVID-19 pandemic has accelerated the adoption of Intelligent Virtual Assistants (IVAs) in the Middle East banking sector, driven by the need for remote engagement, contactless transactions, and digital self-service capabilities:

Digital Transformation Acceleration: The pandemic accelerated banks’ digital transformation initiatives, prompting rapid adoption of IVAs to meet increased demand for remote banking services, support virtual interactions, and ensure business continuity.

Customer Service Resilience: IVAs played a crucial role in maintaining customer service resilience during the pandemic, handling surges in customer inquiries, providing timely assistance, and alleviating pressure on call centers and frontline staff.

Remote Work Enablement: IVAs enabled banks to facilitate remote work and collaboration among employees, automating internal processes, providing self-service tools, and delivering virtual training and support to remote workforce.

Contactless Banking Solutions: IVAs offered contactless banking solutions, enabling customers to perform transactions, access account information, and seek assistance without physical contact or visits to bank branches, reducing health risks and ensuring safety.

Key Industry Developments

Partnerships and Collaborations: Banks in the Middle East are partnering with technology providers, fintech startups, and AI specialists to develop and deploy IVAs, leveraging external expertise, resources, and capabilities to accelerate innovation and digital transformation.

Investments in AI Research: Banks are investing in AI research, talent acquisition, and innovation centers to advance AI capabilities, develop proprietary algorithms, and address industry-specific challenges in areas such as natural language understanding, sentiment analysis, and conversational AI.

Regulatory Compliance Frameworks: Regulators in the Middle East are developing regulatory compliance frameworks, guidelines, and standards for AI adoption in the banking sector, ensuring responsible AI deployment, ethical use of customer data, and adherence to privacy and security regulations.

Customer-Centric Design: Banks are adopting a customer-centric design approach to IVAs, focusing on usability, accessibility, and inclusivity, and conducting user testing, feedback sessions, and iterative improvements to enhance the overall user experience and satisfaction.

Analyst Suggestions

Invest in AI Talent and Expertise: Banks should invest in AI talent acquisition, training, and upskilling programs to build internal capabilities in AI development, deployment, and management, ensuring alignment with business objectives and industry best practices.

Prioritize Data Privacy and Security: Banks must prioritize data privacy and security in AI-driven initiatives, implementing robust encryption, authentication, and access control mechanisms to safeguard customer data, comply with regulatory requirements, and build trust with customers.

Enhance Multilingual Support: Banks operating in culturally diverse markets should enhance multilingual support and localization capabilities in IVAs, catering to the linguistic preferences and cultural sensitivities of diverse customer segments, and ensuring inclusivity and accessibility for all customers.

Foster Collaboration and Knowledge Sharing: Banks should foster collaboration and knowledge sharing within the industry, sharing best practices, lessons learned, and success stories in AI adoption, and collaborating with industry consortia, regulatory bodies, and academia to drive innovation and thought leadership in AI-driven banking.

Future Outlook

The future outlook for the Middle East Intelligent Virtual Assistant (IVA) Based Banking Market is promising, with continued growth and innovation expected in the coming years:

AI-driven Personalization: AI-driven personalization will continue to drive innovation in the banking sector, with IVAs evolving to deliver hyper-personalized banking experiences tailored to individual customer needs, preferences, and life stages.

Conversational AI Advancements: Advancements in conversational AI, natural language understanding, and sentiment analysis will enhance IVAs’ ability to understand and respond to complex queries, emotions, and contexts, enabling more human-like interactions and empathetic engagement.

Integration with Emerging Technologies: IVAs will integrate with emerging technologies such as augmented reality (AR), virtual reality (VR), and mixed reality (MR) to offer immersive and interactive banking experiences, enabling customers to visualize financial data, explore products, and interact with virtual assistants in virtual environments.

Ethical AI and Responsible Banking: Banks will prioritize ethical AI principles, responsible banking practices, and AI governance frameworks in IVAs, ensuring transparency, fairness, and accountability in AI algorithms, decision-making processes, and customer interactions.

Conclusion

The Middle East Intelligent Virtual Assistant (IVA) Based Banking Market represents a transformative shift in the banking sector, leveraging AI, NLP, and conversational technologies to deliver personalized, efficient, and intuitive banking experiences across digital channels. IVAs offer banks an opportunity to enhance customer engagement, streamline operations, and drive digital transformation, reshaping the future of banking in the Middle East region. By investing in AI talent, prioritizing data privacy, fostering collaboration, and embracing ethical AI principles, banks can unlock the full potential of IVAs and deliver superior banking experiences that meet the evolving needs and expectations of customers in the digital age.

What is Intelligent Virtual Assistant (IVA) Based Banking?

Intelligent Virtual Assistant (IVA) Based Banking refers to the use of AI-driven virtual assistants in the banking sector to enhance customer service, streamline operations, and provide personalized financial advice. These systems can handle inquiries, process transactions, and assist with account management, improving overall customer experience.

What are the key players in the Middle East Intelligent Virtual Assistant (IVA) Based Banking Market?

Key players in the Middle East Intelligent Virtual Assistant (IVA) Based Banking Market include banks and technology firms such as Emirates NBD, National Bank of Abu Dhabi, and IBM. These companies are leveraging AI technologies to develop innovative solutions for customer engagement and operational efficiency, among others.

What are the growth factors driving the Middle East Intelligent Virtual Assistant (IVA) Based Banking Market?

The growth of the Middle East Intelligent Virtual Assistant (IVA) Based Banking Market is driven by increasing demand for enhanced customer service, the rise of digital banking, and the need for operational efficiency. Additionally, the growing adoption of AI technologies in financial services is contributing to market expansion.

What challenges does the Middle East Intelligent Virtual Assistant (IVA) Based Banking Market face?

Challenges in the Middle East Intelligent Virtual Assistant (IVA) Based Banking Market include concerns over data privacy and security, the need for regulatory compliance, and the integration of IVA systems with existing banking infrastructure. These factors can hinder the adoption and effectiveness of virtual assistants in banking.

What opportunities exist in the Middle East Intelligent Virtual Assistant (IVA) Based Banking Market?

Opportunities in the Middle East Intelligent Virtual Assistant (IVA) Based Banking Market include the potential for personalized banking experiences, the expansion of mobile banking applications, and the integration of advanced analytics for better customer insights. These factors can lead to improved customer satisfaction and loyalty.

What trends are shaping the Middle East Intelligent Virtual Assistant (IVA) Based Banking Market?

Trends shaping the Middle East Intelligent Virtual Assistant (IVA) Based Banking Market include the increasing use of natural language processing for better customer interactions, the rise of omnichannel banking solutions, and the growing focus on AI ethics and transparency. These trends are influencing how banks implement IVA technologies.

Leading Companies in Middle East Intelligent Virtual Assistant (IVA) Based Banking Market:

Nuance Communications, Inc.

IBM Corporation

Oracle Corporation

Google LLC

Microsoft Corporation

Amazon Web Services, Inc.

Samsung Electronics Co., Ltd.

Inbenta Technologies Inc.

Kasisto Inc.

Creative Virtual Ltd.

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

Based Banking Market")