444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Middle East data center server market represents one of the most dynamic and rapidly expanding technology sectors in the region, driven by unprecedented digital transformation initiatives and growing cloud adoption across various industries. Digital infrastructure development has become a strategic priority for Middle Eastern countries, with governments and enterprises investing heavily in modernizing their IT capabilities to support emerging technologies such as artificial intelligence, Internet of Things, and big data analytics.

Regional growth dynamics indicate that the Middle East is experiencing a significant surge in data center construction and server deployment, with the market expanding at a robust CAGR of 8.2% over the forecast period. This growth trajectory is primarily attributed to the region’s strategic position as a digital hub connecting Europe, Asia, and Africa, making it an ideal location for hyperscale data centers and edge computing infrastructure.

Key market drivers include the rapid adoption of cloud services, increasing internet penetration rates reaching 78% across major Middle Eastern countries, and substantial government investments in smart city initiatives. The region’s commitment to economic diversification away from oil dependency has accelerated technology adoption, with countries like the UAE, Saudi Arabia, and Qatar leading the charge in establishing themselves as regional technology centers.

Enterprise digitization across sectors including banking, telecommunications, healthcare, and retail has created unprecedented demand for high-performance server infrastructure. The growing emphasis on data sovereignty and regulatory compliance has also driven organizations to invest in local data center facilities, further boosting server market demand throughout the region.

The Middle East data center server market refers to the comprehensive ecosystem of server hardware, software, and related infrastructure solutions deployed within data center facilities across Middle Eastern countries. This market encompasses various server types including rack servers, blade servers, tower servers, and high-density computing systems designed to support diverse workloads ranging from traditional enterprise applications to modern cloud-native services.

Market scope includes both physical server hardware and virtualization technologies that enable efficient resource utilization and scalable computing capabilities. The definition extends beyond mere hardware procurement to include server management software, monitoring tools, and integrated solutions that provide complete data center computing infrastructure for organizations of all sizes.

Geographic coverage spans key Middle Eastern markets including the United Arab Emirates, Saudi Arabia, Qatar, Kuwait, Bahrain, Oman, Jordan, and other emerging technology hubs in the region. The market encompasses both public and private sector deployments, ranging from government data centers to enterprise facilities and cloud service provider infrastructure.

Strategic market positioning reveals that the Middle East data center server market has emerged as a critical component of the region’s digital transformation agenda, with substantial investments flowing into infrastructure modernization and capacity expansion. The market demonstrates strong fundamentals driven by increasing data generation, cloud migration trends, and regulatory requirements for local data processing and storage.

Technology evolution within the market shows a clear shift toward high-performance computing solutions, with organizations prioritizing energy-efficient servers that can support intensive workloads while minimizing operational costs. The adoption of next-generation server architectures, including ARM-based processors and specialized AI accelerators, is gaining momentum as enterprises seek to optimize performance for specific use cases.

Investment landscape indicates robust capital allocation toward data center infrastructure, with both domestic and international players establishing significant presence in the region. Major cloud service providers and colocation companies are expanding their footprint, driving demand for enterprise-grade server solutions that can support hyperscale operations and edge computing requirements.

Market maturation is evidenced by increasing sophistication in server deployment strategies, with organizations adopting hybrid and multi-cloud approaches that require flexible, scalable server infrastructure. The growing emphasis on sustainability and green computing is also influencing purchasing decisions, with energy-efficient server solutions experiencing 34% higher adoption rates compared to traditional alternatives.

Fundamental market dynamics reveal several critical insights that shape the Middle East data center server landscape:

Digital transformation initiatives represent the primary catalyst driving server market growth across the Middle East, with governments and enterprises investing heavily in modernizing their technology infrastructure to support digital economy objectives. The region’s ambitious Vision 2030 programs and similar strategic initiatives are creating substantial demand for high-performance computing infrastructure capable of supporting advanced digital services.

Cloud adoption acceleration continues to fuel server market expansion as organizations migrate from traditional on-premises infrastructure to hybrid and multi-cloud environments. This transition requires sophisticated server architectures that can seamlessly integrate with cloud platforms while maintaining performance, security, and compliance requirements specific to Middle Eastern markets.

Data sovereignty regulations are increasingly influencing server deployment decisions, with regional data protection laws requiring organizations to process and store sensitive information within local jurisdictions. This regulatory environment is driving investment in domestic data center facilities and associated server infrastructure, creating significant market opportunities for local and international vendors.

Smart city development across major Middle Eastern urban centers is generating substantial demand for edge computing infrastructure and distributed server deployments. These initiatives require robust server networks capable of processing real-time data from IoT sensors, traffic management systems, and citizen services platforms, driving specialized server market segments.

Financial sector modernization is contributing significantly to server market growth, with banks and financial institutions upgrading their core systems to support digital banking, fintech integration, and regulatory compliance requirements. The sector’s stringent performance and security requirements are driving demand for enterprise-grade server solutions with advanced capabilities.

High capital investment requirements pose significant challenges for many organizations considering server infrastructure upgrades, particularly for small and medium enterprises with limited IT budgets. The substantial upfront costs associated with enterprise-grade server deployments, including hardware, software licensing, and implementation services, can create barriers to market entry and expansion.

Skills shortage in server administration and data center management represents a critical constraint limiting market growth potential. The region faces challenges in developing sufficient technical expertise to support complex server environments, leading to increased operational costs and potential performance issues that may discourage infrastructure investments.

Power infrastructure limitations in certain Middle Eastern markets can restrict large-scale server deployments, particularly for energy-intensive high-performance computing applications. Inconsistent power quality and availability concerns may influence server selection criteria and deployment strategies, potentially limiting market expansion in specific geographic areas.

Vendor dependency risks associated with proprietary server technologies and limited local support capabilities can create hesitation among potential customers. Organizations may delay server investments due to concerns about long-term vendor viability, support availability, and technology lock-in scenarios that could impact future flexibility.

Cybersecurity concerns surrounding server infrastructure security and data protection continue to influence purchasing decisions, with organizations requiring extensive security validation and compliance verification before committing to new server deployments. These requirements can extend procurement cycles and increase implementation complexity.

Artificial intelligence integration presents substantial opportunities for specialized server solutions designed to support machine learning workloads and AI applications. The growing adoption of AI across industries including healthcare, finance, and government services is creating demand for GPU-accelerated servers and high-performance computing infrastructure optimized for AI workloads.

Edge computing expansion offers significant growth potential as organizations deploy distributed computing infrastructure to support IoT applications, content delivery networks, and real-time analytics. The proliferation of connected devices and demand for low-latency services is driving investment in edge server deployments across urban and industrial environments.

Green computing initiatives are creating opportunities for energy-efficient server technologies that can help organizations meet sustainability goals while reducing operational costs. The growing emphasis on environmental responsibility is driving demand for servers with advanced power management capabilities and renewable energy integration options.

Industry-specific solutions represent emerging opportunities for customized server configurations tailored to specific sector requirements. Healthcare, education, government, and manufacturing industries are seeking specialized server solutions that address unique compliance, performance, and integration requirements.

Managed services integration offers opportunities for comprehensive server solutions that combine hardware, software, and ongoing management services. Organizations increasingly prefer turnkey solutions that reduce internal IT complexity while ensuring optimal server performance and reliability.

Competitive landscape evolution within the Middle East data center server market demonstrates increasing sophistication as both established technology vendors and emerging players compete for market share. The dynamics are characterized by rapid technological innovation, aggressive pricing strategies, and comprehensive service offerings designed to differentiate vendors in a crowded marketplace.

Technology convergence trends are reshaping market dynamics as traditional server boundaries blur with storage, networking, and software-defined infrastructure solutions. This convergence is creating opportunities for integrated solutions while challenging vendors to develop comprehensive portfolios that address evolving customer requirements for simplified, scalable infrastructure.

Customer behavior patterns indicate a shift toward outcome-based purchasing decisions, with organizations prioritizing total cost of ownership and business value over initial acquisition costs. This trend is influencing vendor strategies and product development priorities, emphasizing long-term performance, reliability, and operational efficiency.

Supply chain considerations have become increasingly important market dynamics, with organizations seeking vendors that can provide reliable delivery schedules and local support capabilities. The global semiconductor shortage and geopolitical factors have highlighted the importance of supply chain resilience in server procurement decisions.

Partnership ecosystem development is creating new market dynamics as server vendors collaborate with cloud providers, system integrators, and technology consultants to deliver comprehensive solutions. These partnerships are enabling more effective market penetration and customer engagement strategies across diverse industry segments.

Comprehensive market analysis for the Middle East data center server market employs a multi-faceted research approach combining primary and secondary research methodologies to ensure accurate and actionable market insights. The research framework incorporates quantitative data analysis, qualitative stakeholder interviews, and industry expert consultations to provide a holistic view of market conditions and trends.

Primary research activities include structured interviews with key market participants including server vendors, system integrators, data center operators, and end-user organizations across major Middle Eastern markets. These interviews provide direct insights into market challenges, opportunities, and purchasing behavior patterns that inform strategic market assessments.

Secondary research components encompass analysis of industry reports, vendor financial statements, government publications, and technology trend analyses to establish market context and validate primary research findings. This approach ensures comprehensive coverage of market dynamics and competitive landscape factors.

Data validation processes include cross-referencing multiple information sources, statistical analysis of market data, and expert review of research findings to ensure accuracy and reliability. The methodology emphasizes triangulation of data points to minimize research bias and provide robust market intelligence.

Market modeling techniques utilize advanced analytical frameworks to project market trends, assess competitive positioning, and identify growth opportunities. These models incorporate economic indicators, technology adoption patterns, and regional development factors to generate reliable market forecasts and strategic recommendations.

United Arab Emirates maintains its position as the leading market for data center servers in the Middle East, accounting for approximately 35% of regional server deployments. The country’s strategic location, advanced telecommunications infrastructure, and business-friendly regulatory environment continue to attract major cloud service providers and enterprise data center investments, driving consistent server market growth.

Saudi Arabia represents the fastest-growing server market segment, with the Kingdom’s Vision 2030 initiative driving substantial investments in digital infrastructure and smart city development. The establishment of NEOM and other mega-projects is creating unprecedented demand for high-performance server infrastructure, with market growth rates exceeding 12% annually.

Qatar demonstrates strong server market fundamentals supported by ongoing World Cup legacy projects and national digitization initiatives. The country’s focus on becoming a regional technology hub is driving investments in data center infrastructure and associated server deployments, particularly in government and telecommunications sectors.

Kuwait and Bahrain show steady server market growth driven by financial sector modernization and government digitization programs. These markets are characterized by increasing adoption of cloud services and hybrid infrastructure models, creating opportunities for flexible server solutions that can support diverse workload requirements.

Emerging markets including Jordan, Oman, and other regional countries are experiencing growing server demand driven by improving telecommunications infrastructure and increasing internet penetration. According to MarkWide Research analysis, these markets collectively represent approximately 18% of regional server installations with significant growth potential as digital transformation initiatives expand.

Market leadership dynamics in the Middle East data center server market reflect a competitive environment dominated by established global technology vendors alongside emerging regional players and specialized solution providers. The competitive landscape is characterized by continuous innovation, strategic partnerships, and comprehensive service offerings designed to address diverse customer requirements.

Leading market participants include:

Competitive strategies focus on differentiation through technology innovation, local market expertise, and comprehensive service capabilities. Vendors are increasingly emphasizing sustainability, energy efficiency, and total cost of ownership advantages to distinguish their offerings in competitive procurement processes.

Partnership ecosystems play crucial roles in competitive positioning, with server vendors collaborating with local system integrators, cloud service providers, and technology consultants to enhance market reach and customer engagement capabilities throughout the region.

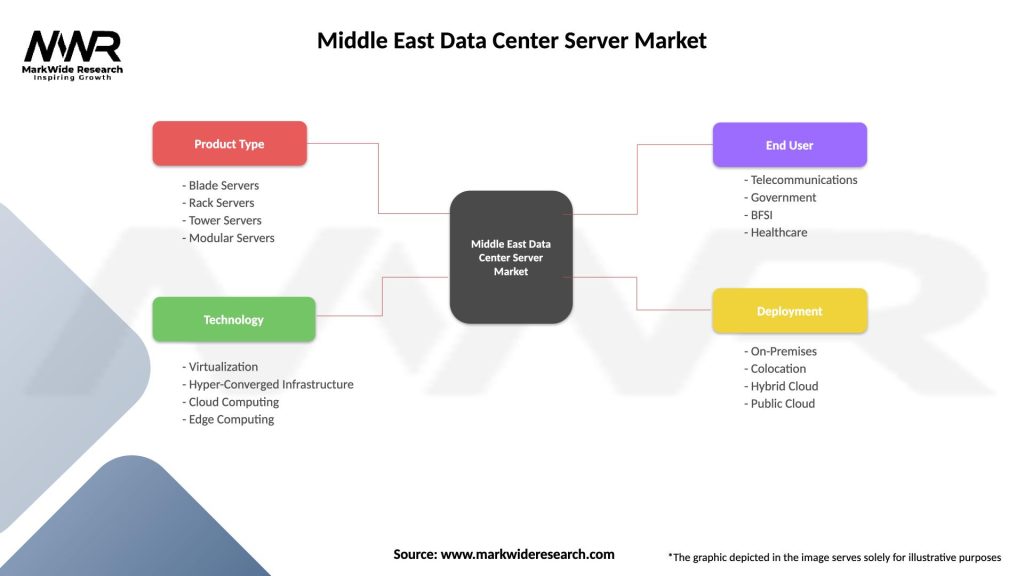

By Server Type:

By Processor Type:

By End-User Industry:

By Organization Size:

Enterprise Server Category demonstrates robust growth driven by digital transformation initiatives and application modernization projects across various industries. Organizations are prioritizing high-performance servers capable of supporting virtualized environments, database applications, and enterprise resource planning systems with demanding performance requirements.

Cloud Infrastructure Servers represent the fastest-growing category as hyperscale cloud providers and managed service providers expand their regional presence. These servers are optimized for multi-tenant environments, offering high density, energy efficiency, and automated management capabilities essential for cloud service delivery.

Edge Computing Servers constitute an emerging category with significant growth potential as organizations deploy distributed computing infrastructure to support IoT applications, content delivery, and real-time analytics. These servers are designed for remote deployment with enhanced reliability and minimal maintenance requirements.

AI and Machine Learning Servers show exceptional growth rates as organizations implement artificial intelligence capabilities across various business functions. These specialized servers incorporate GPU acceleration, high-speed interconnects, and optimized architectures for machine learning workloads and data analytics applications.

Storage-Optimized Servers address growing data management requirements with configurations designed for high-capacity storage, backup operations, and data archiving applications. The increasing focus on data retention and compliance is driving demand for servers with enhanced storage capabilities and data protection features.

Technology Vendors benefit from expanding market opportunities driven by regional digital transformation initiatives and increasing technology adoption across various industry sectors. The growing sophistication of customer requirements creates opportunities for differentiated solutions and value-added services that can command premium pricing and foster long-term customer relationships.

System Integrators gain advantages from increasing complexity of server deployments and growing demand for comprehensive implementation services. The trend toward hybrid and multi-cloud environments creates opportunities for specialized integration expertise and ongoing managed services that generate recurring revenue streams.

End-User Organizations realize significant benefits from advanced server technologies including improved performance, enhanced security, reduced operational costs, and greater scalability. Modern server solutions enable organizations to support digital business initiatives while maintaining operational efficiency and regulatory compliance.

Cloud Service Providers benefit from growing demand for cloud services and the need for robust infrastructure to support expanding customer bases. Investment in advanced server infrastructure enables service providers to offer competitive performance, reliability, and security while achieving operational efficiency targets.

Government Entities gain advantages from server infrastructure investments that support citizen services, smart city initiatives, and digital government programs. Modern server deployments enable improved service delivery, enhanced data security, and operational efficiency that supports public sector modernization objectives.

Investment Community benefits from understanding market dynamics and growth opportunities within the expanding Middle East technology sector. The server market represents a fundamental component of regional digital infrastructure development with attractive long-term growth prospects and strategic importance.

Strengths:

Weaknesses:

Opportunities:

Threats:

Hybrid Cloud Integration represents a dominant trend as organizations adopt flexible infrastructure strategies that combine on-premises servers with public and private cloud resources. This approach enables optimal workload placement, cost optimization, and regulatory compliance while maintaining operational flexibility and performance requirements.

Artificial Intelligence Acceleration is driving demand for specialized server configurations optimized for machine learning workloads and AI applications. Organizations across industries are implementing AI capabilities for customer service, fraud detection, predictive analytics, and operational optimization, requiring high-performance computing infrastructure.

Edge Computing Expansion continues to gain momentum as organizations deploy distributed server infrastructure to support IoT applications, content delivery networks, and real-time analytics. The proliferation of connected devices and demand for low-latency services is driving investment in edge server deployments across urban and industrial environments.

Sustainability Focus is influencing server selection criteria as organizations prioritize energy-efficient solutions that support environmental goals while reducing operational costs. Green computing initiatives are becoming standard requirements, with energy-efficient servers experiencing 42% higher adoption rates compared to traditional alternatives.

Security-First Architectures are becoming essential as cybersecurity threats continue to evolve and regulatory requirements become more stringent. Organizations are prioritizing servers with built-in security features, hardware-based encryption, and advanced threat protection capabilities to protect sensitive data and maintain compliance.

Automation and Orchestration trends are driving demand for servers that integrate seamlessly with automated management platforms and orchestration tools. Organizations seek infrastructure that can be managed programmatically to reduce operational complexity and improve efficiency in dynamic computing environments.

Major cloud service providers continue expanding their Middle East presence with new data center facilities and server infrastructure investments. These developments are creating substantial demand for hyperscale server solutions and driving competition among vendors to secure large-scale deployment contracts.

Government digitization initiatives across the region are generating significant server procurement opportunities as public sector organizations modernize their IT infrastructure. Recent announcements of smart city projects and digital government programs indicate sustained demand for enterprise-grade server solutions.

Technology partnerships between international server vendors and regional system integrators are enhancing market access and customer support capabilities. These collaborations are enabling more effective market penetration and localized service delivery across diverse Middle Eastern markets.

Regulatory developments including data protection laws and cybersecurity requirements are influencing server specification requirements and vendor selection criteria. Organizations are increasingly prioritizing compliance-ready solutions that address regional regulatory requirements.

Investment announcements from major technology companies indicate continued confidence in Middle East market potential, with substantial capital commitments for data center infrastructure and associated server deployments planned over the coming years.

Innovation initiatives including AI research centers, technology incubators, and digital innovation hubs are creating demand for specialized server infrastructure optimized for research and development applications.

Strategic positioning recommendations for market participants emphasize the importance of developing comprehensive regional strategies that address diverse market conditions and customer requirements across different Middle Eastern countries. MWR analysis indicates that successful vendors must balance global technology capabilities with local market expertise and support infrastructure.

Technology investment priorities should focus on emerging areas including AI-optimized servers, edge computing solutions, and energy-efficient architectures that align with regional sustainability goals. Organizations that invest early in these technologies are likely to gain competitive advantages as market demand accelerates.

Partnership development strategies are essential for effective market penetration, with recommendations to establish relationships with local system integrators, cloud service providers, and technology consultants. These partnerships can provide market access, customer relationships, and localized support capabilities that enhance competitive positioning.

Customer engagement approaches should emphasize total cost of ownership benefits, security capabilities, and compliance features that address specific regional requirements. Educational initiatives and proof-of-concept programs can help organizations understand the value proposition of advanced server technologies.

Market timing considerations suggest that current conditions present favorable opportunities for market entry and expansion, with growing demand, supportive government policies, and increasing technology adoption creating a positive environment for server market participants.

Long-term market prospects for the Middle East data center server market remain highly positive, with sustained growth expected to continue driven by ongoing digital transformation initiatives, increasing cloud adoption, and expanding technology infrastructure requirements. The market is projected to maintain strong growth momentum with compound annual growth rates exceeding 8% through 2030.

Technology evolution trends indicate continued advancement in server capabilities including improved energy efficiency, enhanced security features, and specialized architectures for emerging workloads. The integration of artificial intelligence, machine learning, and edge computing capabilities will drive demand for next-generation server solutions optimized for these applications.

Market expansion opportunities are expected to emerge from new industry sectors adopting digital technologies, government smart city initiatives, and growing demand for cloud services across the region. The development of 5G networks and IoT applications will create additional requirements for distributed server infrastructure and edge computing capabilities.

Competitive landscape evolution will likely feature increased consolidation among vendors, strategic partnerships, and continued innovation in server technologies and service delivery models. Organizations that can provide comprehensive solutions combining hardware, software, and services are expected to gain competitive advantages.

Regional development initiatives including economic diversification programs, technology sector investments, and infrastructure modernization projects will continue supporting server market growth. The establishment of technology free zones and innovation centers will create additional demand for advanced computing infrastructure.

Market assessment conclusions indicate that the Middle East data center server market represents a dynamic and rapidly expanding sector with substantial growth opportunities driven by regional digital transformation initiatives, increasing cloud adoption, and government investments in technology infrastructure. The market demonstrates strong fundamentals with diverse growth drivers across multiple industry sectors and geographic markets.

Strategic implications for market participants emphasize the importance of developing comprehensive regional strategies that address local market requirements while leveraging global technology capabilities. Success in this market requires understanding of diverse customer needs, regulatory environments, and competitive dynamics across different Middle Eastern countries.

Future market potential remains highly attractive with sustained growth expected to continue as organizations advance their digital transformation initiatives and adopt emerging technologies including artificial intelligence, edge computing, and hybrid cloud architectures. The region’s strategic position and commitment to technology sector development create favorable conditions for continued server market expansion.

Investment considerations support positive market outlook with multiple growth catalysts including government digitization programs, smart city development, and increasing enterprise technology adoption. The Middle East data center server market offers compelling opportunities for vendors, system integrators, and investors seeking exposure to the region’s expanding technology sector and digital infrastructure development initiatives.

What is Data Center Server?

Data Center Server refers to the specialized computing hardware used in data centers to manage, store, and process data. These servers are designed for high performance, reliability, and scalability to support various applications and services.

What are the key players in the Middle East Data Center Server Market?

Key players in the Middle East Data Center Server Market include companies like Dell Technologies, Hewlett Packard Enterprise, and Cisco Systems, which provide a range of server solutions for data centers, among others.

What are the main drivers of the Middle East Data Center Server Market?

The main drivers of the Middle East Data Center Server Market include the increasing demand for cloud computing services, the growth of big data analytics, and the rising need for data storage and management solutions across various industries.

What challenges does the Middle East Data Center Server Market face?

Challenges in the Middle East Data Center Server Market include high operational costs, the need for skilled workforce, and concerns regarding data security and compliance with regulations.

What opportunities exist in the Middle East Data Center Server Market?

Opportunities in the Middle East Data Center Server Market include the expansion of smart city initiatives, the adoption of edge computing, and the increasing investment in renewable energy solutions for data centers.

What trends are shaping the Middle East Data Center Server Market?

Trends shaping the Middle East Data Center Server Market include the rise of hyper-converged infrastructure, the integration of artificial intelligence for data management, and the growing emphasis on sustainability and energy efficiency in data center operations.

Middle East Data Center Server Market

| Segmentation Details | Description |

|---|---|

| Product Type | Blade Servers, Rack Servers, Tower Servers, Modular Servers |

| Technology | Virtualization, Hyper-Converged Infrastructure, Cloud Computing, Edge Computing |

| End User | Telecommunications, Government, BFSI, Healthcare |

| Deployment | On-Premises, Colocation, Hybrid Cloud, Public Cloud |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Middle East Data Center Server Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.