444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Middle East data center physical security market represents a rapidly evolving landscape driven by increasing digitalization, cloud adoption, and stringent regulatory requirements across the region. Physical security infrastructure has become paramount as organizations recognize the critical importance of protecting their data center assets from both external threats and internal vulnerabilities. The market encompasses comprehensive security solutions including access control systems, surveillance technologies, perimeter security, fire suppression systems, and environmental monitoring solutions.

Regional dynamics indicate substantial growth momentum, with the market experiencing a compound annual growth rate of 12.8% as organizations prioritize robust security frameworks. The increasing adoption of hybrid cloud architectures and edge computing deployments has intensified the demand for sophisticated physical security measures. Countries such as the United Arab Emirates, Saudi Arabia, and Qatar are leading the market expansion, driven by significant investments in digital infrastructure and smart city initiatives.

Technology integration continues to reshape the market landscape, with artificial intelligence, machine learning, and IoT-enabled security solutions gaining prominence. The convergence of physical and cybersecurity measures has created new opportunities for comprehensive security platforms that address both domains simultaneously. Compliance requirements and international security standards are further driving market growth as organizations seek to meet regulatory obligations while protecting critical infrastructure assets.

The Middle East data center physical security market refers to the comprehensive ecosystem of hardware, software, and services designed to protect data center facilities from physical threats, unauthorized access, and environmental hazards across Middle Eastern countries. This market encompasses multiple layers of security infrastructure including perimeter protection, access control mechanisms, surveillance systems, fire suppression technologies, and environmental monitoring solutions specifically tailored for data center environments.

Physical security solutions in this context extend beyond traditional security measures to include sophisticated biometric authentication systems, AI-powered video analytics, thermal imaging technologies, and integrated security management platforms. The market addresses the unique challenges faced by data centers in the Middle East, including extreme weather conditions, geopolitical considerations, and diverse regulatory frameworks across different countries in the region.

Stakeholders in this market include data center operators, colocation providers, cloud service providers, enterprise organizations, government entities, security solution vendors, system integrators, and managed security service providers. The market’s scope covers both greenfield data center developments and retrofit security upgrades for existing facilities, reflecting the region’s dynamic infrastructure development landscape.

Market momentum in the Middle East data center physical security sector reflects the region’s accelerated digital transformation journey and increasing recognition of security as a fundamental business enabler. The market demonstrates robust growth characteristics driven by substantial investments in data center infrastructure, cloud adoption initiatives, and regulatory compliance requirements. Government initiatives supporting digital economy development and smart city projects have created significant opportunities for security solution providers.

Technology evolution continues to shape market dynamics, with organizations increasingly adopting integrated security platforms that combine multiple protection layers. The integration of artificial intelligence and machine learning capabilities has enhanced threat detection accuracy by approximately 45%, while reducing false alarm rates and operational overhead. Biometric authentication systems have achieved widespread adoption, with deployment rates increasing significantly across major data center facilities.

Competitive landscape characteristics include the presence of both international security vendors and regional solution providers, creating a diverse ecosystem of offerings tailored to local market requirements. Strategic partnerships between technology vendors and local system integrators have become increasingly important for market penetration and customer service delivery. Service-based models are gaining traction as organizations seek to optimize security investments while maintaining operational flexibility.

Strategic insights reveal several critical factors shaping the Middle East data center physical security market landscape:

Market maturity varies significantly across different countries, with the UAE and Saudi Arabia leading in terms of advanced security implementations, while other markets are experiencing rapid catch-up growth. Vendor strategies increasingly focus on providing localized support and compliance expertise to address specific regional requirements and cultural considerations.

Digital transformation initiatives across the Middle East region serve as the primary catalyst for data center physical security market growth. Organizations are investing heavily in digital infrastructure to support economic diversification goals and smart city developments. The increasing reliance on digital services has elevated the importance of data center security as a critical business function rather than a compliance requirement.

Regulatory frameworks continue to evolve across Middle Eastern countries, with governments implementing stricter data protection and infrastructure security requirements. The introduction of comprehensive cybersecurity laws and data localization mandates has created mandatory security implementation requirements for data center operators. Compliance costs associated with regulatory violations have increased significantly, making proactive security investments more attractive than reactive approaches.

Threat landscape evolution has intensified the focus on physical security measures as cybercriminals increasingly target physical infrastructure vulnerabilities. The sophistication of physical attacks on data centers has grown substantially, requiring more advanced detection and prevention capabilities. Insurance requirements have also become more stringent, with providers demanding comprehensive physical security measures as prerequisites for coverage.

Cloud service expansion by major international providers in the Middle East region has raised security standards and customer expectations. The presence of global cloud platforms has created competitive pressure for local data center operators to implement world-class security measures. Service level agreements increasingly include specific physical security requirements, driving market demand for certified and auditable security solutions.

Implementation costs represent a significant barrier for many organizations, particularly smaller data center operators and enterprises with limited security budgets. The comprehensive nature of modern physical security solutions requires substantial upfront investments in hardware, software, and professional services. Total cost of ownership considerations often extend beyond initial implementation to include ongoing maintenance, upgrades, and staff training requirements.

Technical complexity associated with integrating multiple security systems and technologies poses challenges for organizations lacking specialized expertise. The need to coordinate various security components while maintaining operational efficiency requires sophisticated project management and technical skills. System integration challenges often result in extended implementation timelines and increased project risks.

Skills shortage in the cybersecurity and physical security domains limits market growth potential as organizations struggle to find qualified personnel to manage complex security infrastructures. The rapid evolution of security technologies requires continuous training and certification, creating ongoing human resource challenges. Talent retention has become increasingly difficult as demand for security professionals exceeds supply across the region.

Cultural and regulatory variations across different Middle Eastern countries create complexity for vendors and system integrators operating in multiple markets. Differences in privacy laws, security standards, and business practices require customized approaches for each country market. Standardization challenges limit the ability to achieve economies of scale and may increase solution costs for end customers.

Artificial intelligence integration presents substantial opportunities for enhancing security effectiveness while reducing operational overhead. AI-powered analytics can improve threat detection accuracy, automate routine security tasks, and provide predictive insights for proactive security management. Machine learning algorithms can adapt to evolving threat patterns and reduce false positive rates, making security systems more efficient and cost-effective.

Edge computing expansion creates new market segments for distributed security solutions as organizations deploy smaller data centers closer to end users. The proliferation of edge facilities requires scalable security architectures that can be deployed consistently across multiple locations. Remote monitoring capabilities become increasingly important for managing security across distributed infrastructure deployments.

Managed security services represent a growing opportunity as organizations seek to outsource complex security operations to specialized providers. The shortage of internal security expertise makes managed services an attractive alternative for many organizations. Service provider partnerships can create new revenue streams for security vendors while addressing customer resource constraints.

Sustainability initiatives are driving demand for energy-efficient security solutions that align with corporate environmental goals. Green data center certifications increasingly include security system energy consumption as evaluation criteria. Solar-powered security systems and other sustainable technologies present opportunities for differentiation in environmentally conscious markets.

Supply chain considerations have become increasingly important following global disruptions that affected security equipment availability and pricing. Organizations are prioritizing vendors with robust supply chain management and local inventory capabilities. Component shortages have led to longer lead times and increased costs for certain security technologies, influencing purchasing decisions and project timelines.

Technology convergence between physical security and IT infrastructure is creating new market dynamics as traditional boundaries between security and IT departments blur. Integrated platforms that combine security management with IT operations are gaining traction among organizations seeking operational efficiency. API integration capabilities have become essential requirements for security solutions to interface with existing IT management systems.

Vendor consolidation trends are reshaping the competitive landscape as larger security companies acquire specialized solution providers to expand their portfolio offerings. This consolidation is creating more comprehensive solution suites while potentially reducing vendor choice for customers. Partnership strategies between complementary vendors are becoming more common to address customer demands for integrated solutions.

Customer expectations continue to evolve toward more sophisticated, user-friendly security solutions that provide comprehensive visibility and control. Organizations increasingly demand security platforms that can demonstrate clear return on investment through operational efficiency improvements and risk reduction. Performance metrics and analytics capabilities have become standard requirements for security solution evaluations.

Primary research activities encompassed comprehensive interviews with key stakeholders across the Middle East data center physical security ecosystem, including data center operators, security solution vendors, system integrators, and end-user organizations. The research methodology incorporated structured questionnaires, in-depth interviews, and focus group discussions to gather qualitative insights and quantitative data points from industry participants.

Secondary research involved extensive analysis of industry reports, vendor documentation, regulatory publications, and market intelligence databases to validate primary research findings and identify market trends. The research team analyzed financial reports, product announcements, partnership agreements, and merger and acquisition activities to understand competitive dynamics and market evolution patterns.

Data validation processes included cross-referencing information from multiple sources, conducting follow-up interviews to clarify inconsistencies, and applying statistical analysis techniques to ensure data accuracy and reliability. The research methodology incorporated both quantitative and qualitative analysis approaches to provide comprehensive market insights and actionable intelligence for stakeholders.

Geographic coverage included detailed analysis of major Middle Eastern markets including the United Arab Emirates, Saudi Arabia, Qatar, Kuwait, Bahrain, Oman, and other relevant countries in the region. The research methodology accounted for regional variations in market maturity, regulatory requirements, and technology adoption patterns to provide accurate country-specific insights and regional market dynamics.

United Arab Emirates maintains its position as the leading market for data center physical security solutions, accounting for approximately 35% of regional market share. The country’s advanced digital infrastructure, favorable business environment, and strategic location as a regional hub drive substantial investments in data center security. Dubai and Abu Dhabi host numerous international data center facilities that require world-class security implementations to meet global standards and customer expectations.

Saudi Arabia represents the fastest-growing market segment, driven by Vision 2030 initiatives and massive investments in digital transformation projects. The kingdom’s focus on developing local data center capabilities and reducing dependence on international providers has created significant opportunities for security solution vendors. NEOM and other megaprojects are incorporating advanced security technologies from the design phase, setting new standards for integrated security implementations.

Qatar demonstrates strong market growth supported by preparations for major international events and ongoing economic diversification efforts. The country’s emphasis on smart city development and digital government initiatives has driven demand for sophisticated data center security solutions. Government sector investments in secure data center infrastructure have created substantial market opportunities for both international and regional vendors.

Other Gulf Cooperation Council countries including Kuwait, Bahrain, and Oman are experiencing steady market growth as organizations modernize their IT infrastructure and adopt cloud services. These markets show increasing sophistication in security requirements while maintaining focus on cost-effective solutions. Regional collaboration initiatives are creating opportunities for standardized security approaches across multiple countries.

Market leadership is characterized by a mix of international security vendors and regional solution providers, each bringing unique strengths to address diverse customer requirements. The competitive landscape reflects the complexity of data center security needs and the importance of local market knowledge and support capabilities.

Strategic partnerships between international vendors and local system integrators have become increasingly important for market success. These collaborations combine global technology expertise with local market knowledge and regulatory compliance capabilities. Regional service capabilities often determine vendor selection as customers prioritize ongoing support and maintenance quality over initial product features.

By Technology:

By Deployment Model:

By End User:

Access Control Systems represent the largest market segment, driven by increasing adoption of biometric authentication and multi-factor authentication requirements. Organizations are implementing sophisticated access control measures that combine multiple authentication factors to ensure only authorized personnel can access critical areas. Integration capabilities with existing IT systems and identity management platforms have become essential requirements for access control solutions.

Video Surveillance Technologies are experiencing rapid growth due to advances in AI-powered analytics and high-resolution imaging capabilities. Modern surveillance systems can automatically detect suspicious activities, track personnel movements, and provide forensic capabilities for incident investigation. Thermal imaging integration has gained popularity for 24/7 monitoring capabilities in challenging environmental conditions.

Environmental Monitoring Solutions have become increasingly sophisticated, incorporating IoT sensors and predictive analytics to prevent equipment failures and security breaches. These systems monitor multiple environmental parameters and can automatically trigger security responses when anomalies are detected. Integration with building management systems provides comprehensive facility monitoring and control capabilities.

Fire Suppression Systems specifically designed for data center environments are gaining traction as organizations recognize the unique fire risks associated with high-density computing equipment. Advanced suppression systems use clean agents that protect equipment while effectively suppressing fires. Early detection capabilities have improved significantly through the integration of multiple sensor technologies and AI-powered analysis.

Data Center Operators benefit from comprehensive physical security solutions through reduced operational risks, improved compliance posture, and enhanced customer confidence. Advanced security systems provide detailed audit trails and reporting capabilities that support regulatory compliance and customer security requirements. Operational efficiency improvements result from automated security processes and integrated management platforms that reduce manual oversight requirements.

Enterprise Organizations gain significant value through improved data protection, reduced insurance costs, and enhanced business continuity capabilities. Physical security investments protect critical business assets while demonstrating commitment to data protection and regulatory compliance. Risk mitigation benefits extend beyond immediate security concerns to include reputation protection and competitive advantage through superior security posture.

Security Solution Vendors benefit from growing market demand and opportunities for technology innovation and differentiation. The evolving threat landscape creates continuous opportunities for product development and market expansion. Recurring revenue opportunities through managed services and ongoing support contracts provide stable business models and long-term customer relationships.

System Integrators gain access to expanding market opportunities and the ability to provide comprehensive security solutions that address multiple customer requirements. The complexity of modern security implementations creates demand for specialized integration expertise and ongoing support services. Partnership opportunities with technology vendors provide access to advanced solutions and competitive differentiation capabilities.

Strengths:

Weaknesses:

Opportunities:

Threats:

Artificial Intelligence Integration continues to transform the physical security landscape through advanced analytics, automated threat detection, and predictive maintenance capabilities. AI-powered systems can analyze vast amounts of security data to identify patterns and anomalies that would be impossible for human operators to detect. Machine learning algorithms continuously improve detection accuracy while reducing false positive rates, making security systems more efficient and cost-effective.

Zero Trust Architecture principles are being applied to physical security implementations, requiring verification and authentication for all access requests regardless of location or previous authorization. This approach enhances security posture by eliminating assumptions about trusted zones within data center facilities. Continuous verification processes ensure that access privileges remain appropriate throughout user sessions and facility interactions.

Biometric Authentication adoption has accelerated significantly, with organizations implementing multi-modal biometric systems that combine fingerprint, facial recognition, and iris scanning technologies. These advanced authentication methods provide higher security levels while improving user experience through faster and more convenient access processes. Liveness detection capabilities prevent spoofing attacks and ensure authentication integrity.

Cloud-Based Security Management platforms are gaining traction as organizations seek centralized visibility and control across multiple facilities and locations. Cloud platforms provide scalability, automatic updates, and advanced analytics capabilities that would be difficult to implement with on-premises solutions. Remote monitoring capabilities enable security operations centers to manage multiple facilities from centralized locations.

Strategic acquisitions and partnerships have reshaped the competitive landscape as companies seek to expand their solution portfolios and market reach. Major security vendors have acquired specialized technology companies to integrate advanced capabilities such as AI analytics, biometric authentication, and IoT sensor technologies. MarkWide Research analysis indicates that merger and acquisition activity has increased by 28% over the past two years as companies position themselves for market growth.

Product innovations continue to drive market evolution with the introduction of integrated security platforms that combine multiple technologies in unified management interfaces. Vendors are focusing on developing solutions that address the complete security lifecycle from threat detection through incident response and forensic analysis. Interoperability standards have improved significantly, enabling better integration between different vendor solutions.

Regulatory developments across Middle Eastern countries have created new compliance requirements that drive security solution adoption. Recent data protection laws and critical infrastructure protection regulations have established mandatory security standards for data center facilities. Certification programs have been introduced to ensure security solutions meet regional requirements and international standards.

Investment announcements from major cloud service providers and data center operators indicate continued market expansion and modernization efforts. These investments include both new facility construction and security upgrades for existing infrastructure. Government initiatives supporting digital transformation and smart city development continue to create market opportunities for security solution providers.

Technology Integration should be prioritized by organizations seeking to maximize security effectiveness while controlling operational costs. Integrated platforms that combine multiple security functions provide better visibility, simplified management, and improved incident response capabilities. Vendor selection should emphasize integration capabilities and long-term technology roadmaps rather than individual product features.

Skills Development initiatives are essential for organizations implementing advanced security technologies. Investment in staff training and certification programs will ensure optimal system utilization and return on investment. Partnership strategies with managed security service providers can address skills gaps while providing access to specialized expertise and 24/7 monitoring capabilities.

Compliance Planning should incorporate anticipated regulatory changes and international standards to avoid costly retrofits and upgrades. Organizations should engage with regulatory bodies and industry associations to stay informed about evolving requirements. Documentation processes should be established to support audit requirements and demonstrate compliance with applicable standards.

Scalability Considerations are crucial for organizations planning facility expansions or technology upgrades. Security architectures should be designed to accommodate future growth and technology evolution without requiring complete system replacements. Modular approaches enable incremental improvements and technology updates while maintaining operational continuity.

Market growth trajectory remains positive with continued expansion expected across all major Middle Eastern markets. MWR projections indicate sustained growth momentum driven by ongoing digital transformation initiatives, regulatory requirements, and increasing security awareness among organizations. The market is expected to maintain a growth rate exceeding 10% annually as new technologies and applications create additional demand.

Technology evolution will continue to drive market transformation through the integration of artificial intelligence, machine learning, and advanced analytics capabilities. Next-generation security solutions will provide predictive capabilities that enable proactive threat prevention rather than reactive response. Quantum computing applications may emerge as a new frontier for both security threats and protection technologies.

Regional market maturation will create opportunities for more sophisticated security implementations and specialized solution providers. As markets mature, customer requirements will become more specific and demanding, creating opportunities for niche vendors and specialized service providers. Standardization efforts may improve interoperability and reduce implementation complexity across the region.

Sustainability initiatives will increasingly influence security solution selection as organizations prioritize environmental responsibility alongside security effectiveness. Energy-efficient technologies and sustainable manufacturing practices will become important vendor selection criteria. Circular economy principles may drive new business models for security equipment lifecycle management and recycling programs.

The Middle East data center physical security market represents a dynamic and rapidly evolving landscape characterized by strong growth momentum, technological innovation, and increasing sophistication in customer requirements. The convergence of digital transformation initiatives, regulatory compliance mandates, and evolving threat landscapes has created substantial opportunities for security solution providers while driving continuous market expansion across the region.

Strategic considerations for market participants include the importance of technology integration, local market expertise, and comprehensive service capabilities in achieving competitive success. Organizations that can effectively combine advanced security technologies with regional knowledge and support capabilities are best positioned to capitalize on market opportunities. The ongoing evolution toward AI-powered solutions and integrated security platforms will continue to reshape competitive dynamics and customer expectations.

Future market development will be influenced by continued investments in digital infrastructure, evolving regulatory frameworks, and the increasing sophistication of security threats. Success in this market requires a long-term perspective that encompasses technology innovation, skills development, and strategic partnerships to address the complex and evolving needs of data center operators across the Middle East region.

What is Data Center Physical Security?

Data Center Physical Security refers to the measures and protocols implemented to protect data centers from physical threats such as unauthorized access, natural disasters, and vandalism. This includes surveillance systems, access control, and environmental controls to ensure the safety and integrity of data and equipment.

What are the key players in the Middle East Data Center Physical Security Market?

Key players in the Middle East Data Center Physical Security Market include companies like Cisco Systems, Honeywell International, and Schneider Electric, which provide various security solutions and technologies. These companies focus on enhancing physical security through advanced surveillance, access control systems, and integrated security management solutions, among others.

What are the main drivers of the Middle East Data Center Physical Security Market?

The main drivers of the Middle East Data Center Physical Security Market include the increasing demand for data storage and processing, the rise in cyber threats necessitating robust physical security measures, and regulatory compliance requirements. Additionally, the growth of cloud computing and digital transformation initiatives are contributing to the market’s expansion.

What challenges does the Middle East Data Center Physical Security Market face?

Challenges in the Middle East Data Center Physical Security Market include the high costs associated with implementing advanced security technologies and the complexity of integrating various security systems. Furthermore, the rapid evolution of security threats requires continuous updates and training, which can strain resources.

What opportunities exist in the Middle East Data Center Physical Security Market?

Opportunities in the Middle East Data Center Physical Security Market include the increasing investment in smart city projects and the growing emphasis on data privacy and protection. Additionally, advancements in AI and IoT technologies present new avenues for enhancing security measures and improving operational efficiency.

What trends are shaping the Middle East Data Center Physical Security Market?

Trends shaping the Middle East Data Center Physical Security Market include the adoption of AI-driven surveillance systems, the integration of physical and cybersecurity measures, and the growing focus on sustainability in security practices. These trends reflect a shift towards more proactive and comprehensive security strategies.

Middle East Data Center Physical Security Market

| Segmentation Details | Description |

|---|---|

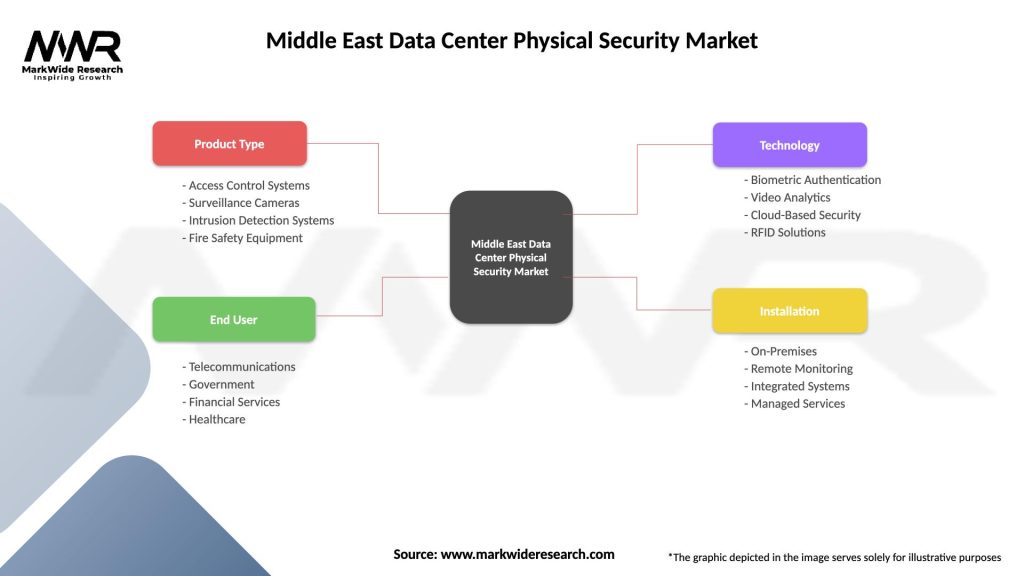

| Product Type | Access Control Systems, Surveillance Cameras, Intrusion Detection Systems, Fire Safety Equipment |

| End User | Telecommunications, Government, Financial Services, Healthcare |

| Technology | Biometric Authentication, Video Analytics, Cloud-Based Security, RFID Solutions |

| Installation | On-Premises, Remote Monitoring, Integrated Systems, Managed Services |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Middle East Data Center Physical Security Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.