444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Middle East and Africa private equity fund market represents a dynamic and rapidly evolving investment landscape that has gained significant momentum over the past decade. This region has emerged as an attractive destination for private equity investments, driven by economic diversification initiatives, growing entrepreneurial ecosystems, and increasing institutional investor confidence. The market encompasses various investment strategies including buyouts, growth capital, venture capital, and distressed investments across multiple sectors.

Regional dynamics indicate that the Middle East and Africa private equity sector is experiencing robust growth, with the market expanding at a compound annual growth rate (CAGR) of 8.2% over recent years. The Gulf Cooperation Council (GCC) countries, particularly the United Arab Emirates and Saudi Arabia, have established themselves as key hubs for private equity activity, while emerging markets in Africa, including Nigeria, Kenya, and South Africa, are attracting increasing investor attention.

Investment focus areas within the region span technology, healthcare, financial services, consumer goods, and infrastructure development. The market benefits from supportive government policies, regulatory reforms, and the establishment of sovereign wealth funds that actively participate in private equity investments. Digital transformation initiatives and the growing startup ecosystem have created numerous opportunities for venture capital and growth equity investments, particularly in fintech, e-commerce, and digital healthcare solutions.

The Middle East and Africa private equity fund market refers to the comprehensive ecosystem of investment funds, institutional investors, fund managers, and portfolio companies operating within the private equity space across the Middle East and African regions. This market encompasses various forms of private capital investments, including leveraged buyouts, growth capital investments, venture capital funding, and mezzanine financing targeted at privately held companies or public companies undergoing privatization.

Private equity funds in this region typically acquire significant ownership stakes in companies with the objective of improving operational performance, implementing strategic initiatives, and ultimately generating substantial returns through eventual exits via initial public offerings, strategic sales, or secondary buyouts. The market includes both domestic and international fund managers who raise capital from institutional investors such as pension funds, sovereign wealth funds, insurance companies, and high-net-worth individuals.

Geographic scope covers the six Gulf Cooperation Council countries (UAE, Saudi Arabia, Kuwait, Qatar, Bahrain, and Oman), along with other Middle Eastern markets including Egypt, Jordan, and Lebanon, as well as key African markets such as Nigeria, South Africa, Kenya, Ghana, and Morocco. The market facilitates capital formation, supports business growth, and contributes to economic development through strategic investments in high-potential companies across diverse industry sectors.

Market momentum in the Middle East and Africa private equity sector continues to strengthen, supported by favorable economic conditions, regulatory improvements, and increasing institutional investor participation. The region has witnessed a significant increase in fund formation activities, with 73% of new funds focusing on growth capital and expansion strategies rather than traditional buyout approaches. This shift reflects the market’s emphasis on supporting emerging businesses and facilitating economic diversification initiatives.

Investment activity has shown remarkable resilience despite global economic uncertainties, with technology and healthcare sectors leading deal flow. The market benefits from substantial sovereign wealth fund participation, which accounts for approximately 42% of total institutional commitments to regional private equity funds. Cross-border investments have increased substantially, with international fund managers establishing local presence to capitalize on regional opportunities.

Exit strategies have evolved significantly, with strategic sales becoming the preferred exit route for 58% of successful investments. The development of local capital markets and increasing merger and acquisition activity have created more diverse exit opportunities for private equity investors. Sector diversification remains a key trend, with funds expanding beyond traditional focus areas to include renewable energy, education technology, and sustainable infrastructure projects.

Future prospects indicate continued growth momentum, supported by government initiatives to develop local capital markets, attract foreign investment, and promote entrepreneurship. The market is expected to benefit from increasing institutional investor allocations to alternative investments and the growing sophistication of local investment management capabilities.

Strategic positioning within the global private equity landscape has elevated the Middle East and Africa region as an emerging market destination with significant growth potential. The following key insights demonstrate the market’s evolution and future trajectory:

Economic diversification initiatives across the Middle East and Africa region serve as primary catalysts for private equity market growth. Government-led programs aimed at reducing dependence on oil revenues and developing knowledge-based economies create substantial investment opportunities for private equity funds. Vision 2030 programs in Saudi Arabia and similar strategic initiatives in other GCC countries have established clear frameworks for private sector development and foreign investment attraction.

Demographic advantages present compelling investment opportunities, with the region hosting one of the world’s youngest populations and rapidly growing middle-class segments. This demographic profile drives demand for consumer goods, financial services, healthcare, and education, creating attractive investment targets for private equity funds. Urbanization trends and increasing disposable income levels further enhance market attractiveness for growth capital investments.

Regulatory reforms have significantly improved the investment climate, with governments implementing investor-friendly policies, streamlining business registration processes, and establishing specialized economic zones. Foreign ownership regulations have been relaxed in many jurisdictions, allowing international private equity funds greater access to local investment opportunities. The establishment of financial free zones and international financial centers has created conducive environments for fund management activities.

Infrastructure development programs across the region generate substantial investment opportunities in transportation, utilities, telecommunications, and urban development projects. Public-private partnerships have become increasingly common, providing private equity funds with access to large-scale infrastructure investments that offer stable, long-term returns.

Limited exit opportunities remain a significant challenge for private equity investors in the region, despite recent improvements in capital market development. Stock market liquidity constraints and limited strategic buyer pools can extend investment holding periods and impact return expectations. The relatively small size of many regional stock exchanges limits the feasibility of initial public offerings for portfolio companies.

Regulatory complexity across different jurisdictions creates operational challenges for fund managers seeking to implement regional investment strategies. Varying legal frameworks, tax structures, and compliance requirements necessitate sophisticated legal and regulatory expertise, increasing operational costs and complexity. Cross-border investment activities often face bureaucratic delays and regulatory uncertainties.

Currency volatility and economic instability in certain markets can impact investment returns and create additional risk management challenges. Political risks and regional geopolitical tensions may affect investor confidence and limit capital flows to certain markets. Economic sanctions and international trade restrictions can complicate investment activities and exit strategies.

Limited institutional investor base in some markets constrains fundraising activities and reduces the availability of long-term capital for private equity investments. Pension fund development remains nascent in many African markets, limiting domestic institutional participation in private equity funds. Insurance company investment regulations often restrict alternative investment allocations, further limiting potential investor base expansion.

Technology sector expansion presents exceptional growth opportunities for private equity investors, particularly in fintech, e-commerce, and digital transformation solutions. The region’s rapid digital adoption rates and government support for technology innovation create favorable conditions for venture capital and growth equity investments. Artificial intelligence and blockchain technology applications offer significant potential for early-stage and expansion capital investments.

Healthcare infrastructure development represents a substantial opportunity area, driven by growing healthcare expenditure, aging populations in certain markets, and increasing demand for specialized medical services. Medical technology and healthcare services companies present attractive investment targets for private equity funds seeking exposure to defensive, growth-oriented sectors.

Renewable energy projects align with regional sustainability initiatives and offer long-term investment opportunities with stable cash flow profiles. Solar and wind energy developments, supported by government incentives and international climate commitments, create attractive investment propositions for infrastructure-focused private equity funds.

Financial services expansion opportunities exist across banking, insurance, and capital markets development. Islamic finance products and services represent a specialized market segment with significant growth potential, particularly for funds with expertise in Sharia-compliant investment structures. Microfinance and financial inclusion initiatives in African markets offer impact investment opportunities with attractive returns.

Competitive landscape evolution reflects increasing sophistication and specialization within the Middle East and Africa private equity market. International fund managers continue to establish regional presence through local offices, joint ventures, and strategic partnerships with domestic investment firms. This trend has intensified competition for high-quality investment opportunities while simultaneously bringing global best practices and expertise to regional markets.

Investor preferences have shifted toward funds with strong environmental, social, and governance (ESG) credentials, reflecting global trends in responsible investing. Impact investing strategies have gained traction, particularly in African markets where private equity funds can address social challenges while generating financial returns. Approximately 34% of regional funds now incorporate formal ESG criteria into their investment processes.

Deal sourcing mechanisms have become more sophisticated, with fund managers leveraging technology platforms, industry networks, and strategic partnerships to identify investment opportunities. Proprietary deal flow development has become increasingly important as competition for attractive assets intensifies. The use of data analytics and artificial intelligence in deal origination has improved efficiency and success rates.

Portfolio management approaches have evolved to emphasize operational improvement and strategic value creation rather than financial engineering. Management team development and corporate governance enhancement have become standard practices for private equity funds seeking to maximize portfolio company performance and exit valuations.

Comprehensive market analysis for the Middle East and Africa private equity fund market employs a multi-faceted research approach combining primary and secondary data sources. Primary research activities include structured interviews with fund managers, institutional investors, portfolio company executives, and industry experts across key regional markets. Survey methodologies capture quantitative data on fund performance, investment preferences, and market outlook perspectives.

Secondary research components encompass analysis of regulatory filings, fund prospectuses, annual reports, and industry publications. Database analysis includes examination of deal databases, fund performance metrics, and market transaction data to identify trends and patterns. Academic research papers and industry white papers provide additional insights into market dynamics and emerging trends.

Regional market coverage ensures comprehensive analysis across all major Middle Eastern and African markets, with particular focus on high-activity jurisdictions including the UAE, Saudi Arabia, Egypt, Nigeria, South Africa, and Kenya. Sector analysis examines investment activity across technology, healthcare, financial services, consumer goods, and infrastructure sectors.

Data validation processes include cross-referencing multiple sources, expert review panels, and statistical analysis to ensure accuracy and reliability. Market sizing methodologies employ bottom-up and top-down approaches to validate market metrics and growth projections. Regular updates and revisions maintain data currency and relevance for market participants.

Gulf Cooperation Council markets dominate regional private equity activity, accounting for approximately 67% of total fund commitments and deal volume. The United Arab Emirates serves as the primary hub for fund management activities, benefiting from sophisticated financial infrastructure, favorable regulatory environment, and strategic geographic location. Dubai International Financial Centre and Abu Dhabi Global Market provide world-class platforms for fund establishment and operations.

Saudi Arabia represents the largest single market opportunity, driven by Vision 2030 initiatives and substantial government support for private sector development. The Public Investment Fund has emerged as a major anchor investor for regional and international private equity funds, providing significant capital commitments and co-investment opportunities. Recent regulatory reforms have opened previously restricted sectors to foreign investment.

African markets demonstrate significant growth potential, with Nigeria, South Africa, and Kenya leading investment activity. Nigeria’s market benefits from large population size, growing consumer base, and expanding technology sector. However, currency volatility and regulatory challenges require specialized expertise and risk management capabilities. South Africa offers the most developed capital markets infrastructure and institutional investor base on the continent.

Egypt has emerged as an attractive investment destination following economic reforms and currency devaluation, which have improved asset valuations and investment opportunities. Morocco and Kenya represent growing markets with increasing private equity activity, supported by government initiatives to attract foreign investment and develop local capital markets.

Market leadership in the Middle East and Africa private equity sector encompasses both regional specialists and international fund managers with local presence. The competitive landscape reflects diverse investment strategies, sector focuses, and geographic coverage areas.

Competitive differentiation strategies include sector specialization, geographic focus, value creation capabilities, and ESG integration. Local market expertise and established networks provide competitive advantages for regional fund managers, while international firms leverage global resources and cross-border capabilities.

Investment strategy segmentation reveals diverse approaches within the Middle East and Africa private equity market, reflecting varying risk-return profiles and market opportunities:

By Investment Strategy:

By Sector Focus:

By Geographic Focus:

Growth capital strategies have gained significant prominence, representing the fastest-growing segment within the regional private equity market. These investments typically involve minority or majority stakes in companies with proven business models seeking expansion capital. Technology companies dominate growth capital deal flow, with fintech and e-commerce platforms attracting substantial investor interest. The average growth capital investment size has increased by 28% annually over recent years.

Buyout investments remain concentrated in mature markets with established corporate sectors, particularly in the GCC region. Family business transitions represent a significant opportunity area, as many regional companies seek professional management and capital to support next-generation growth. Management buyouts have become increasingly common, supported by improving debt markets and management team sophistication.

Venture capital activity has accelerated dramatically, driven by government initiatives to support entrepreneurship and innovation. Startup ecosystems in Dubai, Riyadh, Cairo, and Lagos have attracted increasing venture capital attention, with 65% of venture investments focusing on technology-enabled businesses. Corporate venture capital programs launched by regional conglomerates have supplemented traditional venture capital funding sources.

Infrastructure investments benefit from substantial government spending on development projects and public-private partnership opportunities. Renewable energy infrastructure has emerged as a preferred investment category, supported by government sustainability commitments and attractive project economics. Digital infrastructure investments, including data centers and telecommunications networks, have gained momentum with increasing digitalization trends.

Portfolio companies benefit significantly from private equity partnerships through access to growth capital, strategic guidance, and operational expertise. Management teams gain exposure to international best practices, corporate governance standards, and professional development opportunities. Private equity involvement often accelerates business expansion, market entry strategies, and operational efficiency improvements.

Institutional investors achieve portfolio diversification and access to attractive risk-adjusted returns through private equity allocations. Sovereign wealth funds and pension funds benefit from long-term capital appreciation and inflation hedging characteristics of private equity investments. The asset class provides exposure to regional economic growth and development themes.

Economic development benefits include job creation, technology transfer, and entrepreneurship promotion. Private equity investments contribute to corporate sector development, management capability building, and capital market sophistication. Tax revenue generation and foreign direct investment attraction support broader economic development objectives.

Fund managers benefit from growing institutional investor allocations to alternative investments and increasing market sophistication. Career development opportunities and compensation structures attract top talent to the regional private equity industry. Deal flow quality continues to improve as more companies recognize the value of private equity partnerships.

Strengths:

Weaknesses:

Opportunities:

Threats:

ESG integration has become a dominant trend, with private equity funds increasingly incorporating environmental, social, and governance factors into investment decision-making processes. Impact investing strategies are gaining traction, particularly in African markets where funds can address social challenges while generating financial returns. Approximately 45% of regional funds now have formal ESG policies and reporting frameworks.

Technology adoption in fund management operations has accelerated, with firms implementing advanced analytics, artificial intelligence, and digital platforms for deal sourcing, due diligence, and portfolio monitoring. Virtual deal execution capabilities developed during the pandemic have become permanent features of fund operations, improving efficiency and reducing transaction costs.

Sector specialization continues to increase, with funds developing deep expertise in specific industries such as healthcare, technology, or financial services. Thematic investing approaches focusing on demographic trends, digitalization, or sustainability themes have gained popularity among institutional investors seeking targeted exposure to regional growth drivers.

Co-investment opportunities have expanded significantly, with institutional investors increasingly seeking direct investment alongside fund managers. Sovereign wealth funds and family offices are particularly active in co-investment activities, seeking to increase exposure to attractive deals while reducing fee burden.

Regulatory enhancements across multiple jurisdictions have improved the investment climate for private equity activities. Saudi Arabia’s Capital Market Authority has introduced new regulations facilitating private fund establishment and operations, while the UAE’s Securities and Commodities Authority has streamlined fund licensing procedures. These regulatory improvements have reduced operational complexity and compliance costs for fund managers.

Capital market development initiatives include the establishment of specialized exchanges for growth companies and the introduction of new listing requirements designed to facilitate private equity exits. Tadawul’s Nomu market in Saudi Arabia and similar initiatives in other regional markets have created additional exit opportunities for portfolio companies.

International partnerships between regional and global fund managers have increased substantially, bringing international expertise and capital to local markets. Joint venture structures and strategic alliances have become common mechanisms for international firms to establish regional presence while leveraging local market knowledge and networks.

Government initiatives supporting entrepreneurship and innovation have created favorable conditions for venture capital and growth equity investments. Startup accelerators, government-backed venture funds, and regulatory sandboxes for fintech companies have enhanced the regional startup ecosystem and deal flow quality.

MarkWide Research analysis indicates that private equity fund managers should prioritize sector specialization and local market expertise to differentiate themselves in an increasingly competitive landscape. Technology sector focus remains particularly attractive, given the region’s rapid digital transformation and government support for innovation initiatives. Funds should develop capabilities in ESG integration and impact measurement to meet evolving institutional investor requirements.

Portfolio construction strategies should emphasize diversification across sectors and geographies while maintaining sufficient concentration to leverage expertise and generate superior returns. Co-investment programs can help funds access larger deals and strengthen relationships with institutional investors seeking direct investment opportunities.

Exit planning should begin at the investment stage, with fund managers developing multiple exit scenarios and maintaining flexibility to capitalize on market opportunities. Strategic buyer cultivation and capital market development monitoring are essential for optimizing exit timing and valuations.

Risk management frameworks must address currency volatility, political risks, and regulatory changes while maintaining investment discipline and return objectives. Local partnership strategies can help mitigate risks and enhance deal sourcing capabilities in challenging markets.

Market expansion is expected to continue over the next decade, driven by economic diversification initiatives, demographic trends, and increasing institutional investor allocations to alternative investments. MWR projections indicate that the regional private equity market will maintain robust growth momentum, with fund formation activity increasing at a compound annual growth rate of 9.1% through 2030.

Sector evolution will likely favor technology, healthcare, and sustainable infrastructure investments, reflecting global trends and regional development priorities. Venture capital activity is expected to accelerate significantly, supported by government initiatives and improving startup ecosystem maturity. Growth capital strategies will continue to dominate deal flow as regional companies seek expansion financing.

Geographic expansion into frontier African markets presents significant opportunities for experienced fund managers with appropriate risk management capabilities. Cross-border investment activity is expected to increase as regional economic integration progresses and regulatory barriers are reduced.

Institutional investor participation will likely expand as pension funds, insurance companies, and sovereign wealth funds increase alternative investment allocations. Local institutional development and regulatory improvements will support domestic capital formation and reduce dependence on international funding sources.

The Middle East and Africa private equity fund market represents a compelling investment opportunity characterized by strong growth fundamentals, supportive government policies, and increasing institutional investor interest. Despite challenges related to exit market development and regulatory complexity, the region offers attractive risk-adjusted returns and exposure to significant economic development themes.

Market maturation continues to progress, with improving regulatory frameworks, expanding institutional investor base, and growing management expertise creating favorable conditions for sustained growth. Technology sector opportunities, demographic advantages, and infrastructure development requirements provide substantial deal flow potential for specialized fund managers.

Success factors for private equity investors include local market expertise, sector specialization, strong operational capabilities, and effective risk management frameworks. The market rewards fund managers who can navigate regulatory complexity while identifying and developing high-quality investment opportunities across diverse sectors and geographies.

Looking forward, the Middle East and Africa private equity market is positioned for continued expansion, supported by economic diversification initiatives, technological innovation, and increasing integration with global capital markets. Fund managers who establish strong regional presence and develop specialized capabilities will be well-positioned to capitalize on the significant opportunities presented by this dynamic and evolving market landscape.

What is Private Equity Fund?

Private Equity Fund refers to investment funds that are directly invested in private companies or public companies that are intended to be delisted from public stock exchanges. These funds typically focus on acquiring equity ownership in companies to drive growth and improve operational efficiencies.

What are the key players in the Middle East and Africa Private Equity Fund Market?

Key players in the Middle East and Africa Private Equity Fund Market include firms such as Actis, Abraaj Group, and Helios Investment Partners, which focus on various sectors including technology, healthcare, and consumer goods, among others.

What are the growth factors driving the Middle East and Africa Private Equity Fund Market?

The growth of the Middle East and Africa Private Equity Fund Market is driven by increasing foreign direct investment, a growing number of startups, and the diversification of economies away from oil dependency. Additionally, favorable regulatory environments are encouraging more investments.

What challenges does the Middle East and Africa Private Equity Fund Market face?

The Middle East and Africa Private Equity Fund Market faces challenges such as political instability, regulatory uncertainties, and limited exit opportunities for investors. These factors can hinder the growth and attractiveness of private equity investments in the region.

What opportunities exist in the Middle East and Africa Private Equity Fund Market?

Opportunities in the Middle East and Africa Private Equity Fund Market include the rise of technology-driven startups, increasing consumer demand in various sectors, and the potential for infrastructure development. These factors present avenues for significant returns on investment.

What trends are shaping the Middle East and Africa Private Equity Fund Market?

Trends shaping the Middle East and Africa Private Equity Fund Market include a growing focus on sustainable investments, increased interest in fintech and healthtech sectors, and the rise of impact investing. These trends reflect a shift towards responsible and innovative investment strategies.

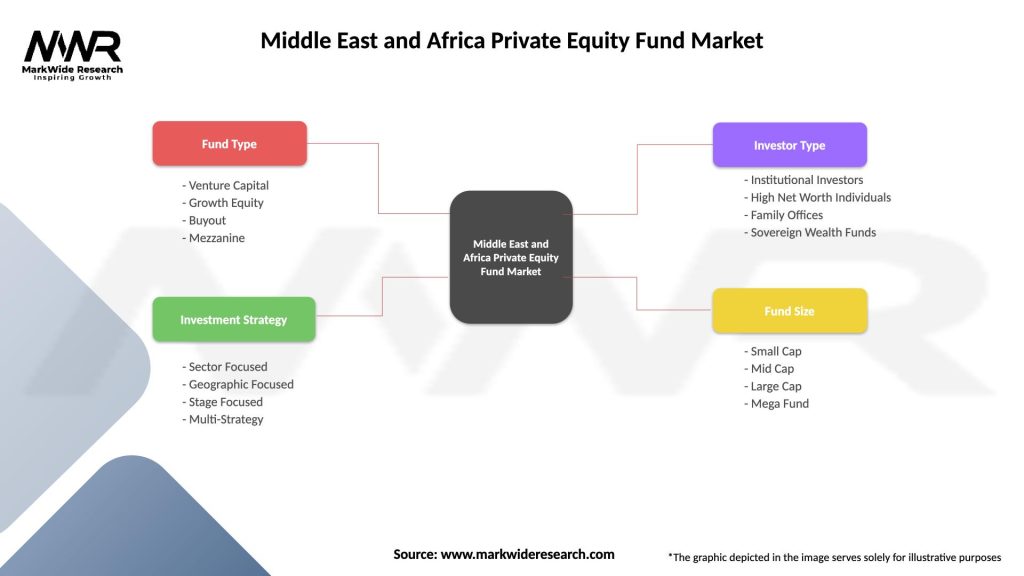

Middle East and Africa Private Equity Fund Market

| Segmentation Details | Description |

|---|---|

| Fund Type | Venture Capital, Growth Equity, Buyout, Mezzanine |

| Investment Strategy | Sector Focused, Geographic Focused, Stage Focused, Multi-Strategy |

| Investor Type | Institutional Investors, High Net Worth Individuals, Family Offices, Sovereign Wealth Funds |

| Fund Size | Small Cap, Mid Cap, Large Cap, Mega Fund |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Middle East and Africa Private Equity Fund Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.