444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Middle East and Africa kidney cancer therapeutics and diagnostics market represents a rapidly evolving healthcare segment addressing one of the most challenging oncological conditions in the region. This market encompasses comprehensive treatment solutions, advanced diagnostic technologies, and innovative therapeutic approaches specifically designed to combat renal cell carcinoma and other kidney cancer variants. The regional market demonstrates significant growth potential, driven by increasing cancer incidence rates, improving healthcare infrastructure, and growing awareness about early detection protocols.

Healthcare systems across the Middle East and Africa are experiencing substantial transformation, with governments investing heavily in oncology care capabilities. The market benefits from a growing population of approximately 1.7 billion people, with kidney cancer representing a significant health concern requiring specialized therapeutic interventions. Regional healthcare expenditure has increased substantially, supporting the adoption of advanced diagnostic equipment and cutting-edge treatment modalities.

Market dynamics indicate robust expansion driven by technological advancements in imaging systems, molecular diagnostics, and targeted therapy options. The region shows promising growth rates of approximately 8.2% CAGR for kidney cancer therapeutics, while diagnostic segment expansion reaches 9.1% annually. These growth patterns reflect increasing healthcare accessibility, rising disposable incomes, and enhanced medical tourism activities across key regional markets including UAE, Saudi Arabia, South Africa, and Egypt.

The Middle East and Africa kidney cancer therapeutics and diagnostics market refers to the comprehensive ecosystem of medical products, services, and technologies specifically designed for the prevention, detection, treatment, and management of kidney cancer within the MEA region. This market encompasses pharmaceutical interventions, medical devices, diagnostic equipment, and associated healthcare services targeting renal cell carcinoma, transitional cell carcinoma, and other kidney malignancies.

Therapeutic components include targeted therapy drugs, immunotherapy agents, chemotherapy medications, and surgical interventions, while diagnostic elements comprise imaging technologies, biomarker testing, genetic screening, and pathological examination services. The market serves healthcare providers, patients, and medical institutions across diverse economic and geographic landscapes, from advanced medical centers in Gulf Cooperation Council countries to emerging healthcare facilities in sub-Saharan Africa.

Market scope extends beyond traditional treatment paradigms to include personalized medicine approaches, precision diagnostics, and integrated care delivery models that address the unique demographic, genetic, and socioeconomic characteristics of Middle Eastern and African populations affected by kidney cancer.

Strategic market analysis reveals the Middle East and Africa kidney cancer therapeutics and diagnostics market as a high-growth healthcare segment characterized by increasing disease prevalence, expanding treatment options, and improving diagnostic capabilities. The market demonstrates strong fundamentals supported by demographic trends, healthcare infrastructure development, and rising awareness about kidney cancer prevention and treatment.

Key market drivers include aging population demographics, lifestyle-related risk factors, improved healthcare access, and government initiatives promoting cancer care excellence. The therapeutic segment shows particular strength in targeted therapy adoption, with immunotherapy utilization increasing by approximately 15.3% annually across major regional markets. Diagnostic segment growth is propelled by advanced imaging technology deployment and molecular diagnostic tool integration.

Regional market leaders include established pharmaceutical companies, medical device manufacturers, and specialized oncology service providers. The competitive landscape features both international corporations and regional healthcare organizations working to address the growing demand for comprehensive kidney cancer care solutions. Market penetration varies significantly across countries, with Gulf states showing higher adoption rates compared to emerging African markets.

Future market trajectory appears highly promising, supported by continued healthcare investment, technology advancement, and increasing patient awareness. The market benefits from favorable regulatory environments, expanding insurance coverage, and growing medical tourism activities that attract international patients seeking advanced kidney cancer treatment options.

Market intelligence reveals several critical insights shaping the Middle East and Africa kidney cancer therapeutics and diagnostics landscape:

Demographic transformation serves as a primary market driver, with aging populations across the Middle East and Africa experiencing higher kidney cancer incidence rates. The region’s demographic shift toward older age groups, combined with increasing life expectancy, creates sustained demand for comprehensive kidney cancer care solutions. Population aging particularly affects Gulf states and North African countries, where improved living standards contribute to longer lifespans and higher cancer detection rates.

Healthcare infrastructure development significantly drives market expansion through improved medical facility capabilities, enhanced diagnostic equipment availability, and expanded treatment options. Government investments in healthcare modernization programs create favorable conditions for advanced therapeutic and diagnostic technology adoption. Infrastructure improvements include specialized oncology centers, upgraded imaging facilities, and enhanced laboratory capabilities supporting comprehensive kidney cancer care delivery.

Rising awareness levels among healthcare providers and patients contribute to increased screening activities, earlier detection, and improved treatment outcomes. Educational initiatives, public health campaigns, and professional medical training programs enhance understanding of kidney cancer risk factors, symptoms, and treatment options. Awareness campaigns particularly target high-risk populations, including individuals with diabetes, hypertension, and family history of kidney disease.

Economic development across the region supports healthcare spending growth, insurance coverage expansion, and medical tourism activities. Improved economic conditions enable greater healthcare accessibility, advanced treatment affordability, and international collaboration in kidney cancer research and treatment. Economic growth particularly benefits middle-income populations seeking quality oncology care within the region rather than traveling to international medical centers.

Healthcare accessibility challenges represent significant market restraints, particularly in rural and economically disadvantaged areas where advanced kidney cancer diagnostics and therapeutics remain limited. Geographic barriers, inadequate transportation infrastructure, and concentrated medical expertise in urban centers create disparities in treatment access. Accessibility limitations affect approximately 35% of the regional population, particularly in sub-Saharan African countries with limited healthcare infrastructure.

Economic constraints limit market growth through restricted healthcare budgets, limited insurance coverage, and high treatment costs that exceed patient affordability. Many kidney cancer therapeutics, particularly targeted therapy and immunotherapy options, require substantial financial investments that challenge both healthcare systems and individual patients. Cost barriers particularly affect middle-income populations who may not qualify for government assistance but cannot afford premium treatment options.

Regulatory complexities across diverse national healthcare systems create challenges for market participants seeking regional expansion. Varying approval processes, different quality standards, and inconsistent regulatory frameworks complicate product registration and market entry strategies. Regulatory harmonization efforts remain limited, requiring companies to navigate multiple approval pathways for regional market access.

Healthcare workforce limitations constrain market development through shortages of specialized oncologists, trained diagnostic technicians, and experienced healthcare support staff. The region faces ongoing challenges in attracting and retaining qualified medical professionals, particularly in oncology specialties requiring advanced training and expertise. Workforce development initiatives show progress but require sustained investment and international collaboration to address existing gaps.

Telemedicine integration presents substantial opportunities for expanding kidney cancer care access across the region’s diverse geographic and economic landscape. Digital health platforms enable remote consultation, diagnostic support, and treatment monitoring capabilities that overcome traditional accessibility barriers. Telemedicine adoption has accelerated significantly, offering opportunities to serve underserved populations and provide specialized expertise to remote healthcare facilities.

Medical tourism development creates opportunities for regional healthcare providers to attract international patients seeking high-quality, cost-effective kidney cancer treatment. Countries with advanced medical infrastructure can position themselves as regional oncology centers, generating revenue while building expertise and capacity. Medical tourism particularly benefits Gulf states and select African countries with established healthcare reputations and modern medical facilities.

Public-private partnerships offer opportunities to accelerate healthcare infrastructure development, technology adoption, and treatment accessibility improvement. Collaborative initiatives between government agencies and private healthcare companies can leverage combined resources to address market challenges and expand service delivery capabilities. Partnership models show particular promise in diagnostic equipment deployment and specialized treatment center development.

Research collaboration opportunities enable regional participation in international kidney cancer studies, clinical trials, and treatment development programs. Academic medical centers and research institutions can contribute to global knowledge while accessing cutting-edge therapies and diagnostic technologies. Research initiatives particularly focus on genetic factors, environmental influences, and treatment responses specific to Middle Eastern and African populations.

Supply chain evolution significantly influences market dynamics through improved pharmaceutical distribution networks, enhanced diagnostic equipment availability, and streamlined healthcare logistics. Regional supply chain development reduces treatment delays, improves product availability, and supports consistent care delivery across diverse geographic markets. Distribution efficiency has improved substantially, with delivery times decreasing and product availability increasing in previously underserved areas.

Technology convergence drives market dynamics through integration of artificial intelligence, machine learning, and precision medicine approaches in kidney cancer diagnosis and treatment. Advanced technologies enhance diagnostic accuracy, treatment personalization, and patient outcome prediction capabilities. Technology integration shows particular promise in imaging analysis, biomarker identification, and treatment response monitoring applications.

Competitive intensity shapes market dynamics as established pharmaceutical companies, emerging biotech firms, and regional healthcare providers compete for market share. Competition drives innovation, improves treatment options, and enhances service quality while potentially reducing costs through market efficiency. Market competition particularly intensifies in therapeutic segments where multiple treatment options exist and in diagnostic areas with rapid technological advancement.

Regulatory evolution influences market dynamics through changing approval processes, updated quality standards, and harmonized regional frameworks. Regulatory improvements facilitate market access, reduce compliance costs, and accelerate product availability while maintaining safety and efficacy standards. Regulatory modernization efforts show progress in streamlining approval processes and encouraging innovation in kidney cancer care solutions.

Comprehensive market analysis employs multi-faceted research methodologies combining primary research, secondary data analysis, and expert consultation to provide accurate market insights. The research approach integrates quantitative analysis with qualitative assessment to capture market complexities and regional variations affecting kidney cancer therapeutics and diagnostics adoption.

Primary research activities include structured interviews with healthcare providers, pharmaceutical executives, medical device manufacturers, and regulatory officials across key regional markets. Survey methodologies capture patient perspectives, treatment experiences, and healthcare accessibility challenges. Primary data collection focuses on understanding market dynamics, competitive positioning, and emerging trends affecting kidney cancer care delivery.

Secondary research analysis incorporates government health statistics, medical literature review, industry reports, and regulatory documentation to establish market context and validate primary findings. Data sources include national health ministries, international health organizations, and regional medical associations providing kidney cancer epidemiology and treatment data.

Expert consultation involves collaboration with oncology specialists, healthcare economists, and regional market analysts to ensure research accuracy and relevance. Expert insights provide context for market trends, technology adoption patterns, and future development projections. Validation processes ensure research findings accurately reflect market realities and provide actionable insights for stakeholders.

Gulf Cooperation Council countries represent the most advanced segment of the regional market, with UAE, Saudi Arabia, and Qatar leading in healthcare infrastructure, treatment accessibility, and technology adoption. These markets demonstrate high treatment penetration rates of approximately 78% for eligible patients and sophisticated diagnostic capabilities supporting early detection and comprehensive care delivery. GCC healthcare systems benefit from substantial government investment, international medical partnerships, and medical tourism activities.

North African markets including Egypt, Morocco, and Tunisia show significant growth potential with expanding healthcare infrastructure and increasing kidney cancer awareness. These countries demonstrate improving diagnostic capabilities and growing access to targeted therapies, though challenges remain in rural area coverage and advanced treatment affordability. North African growth is supported by government healthcare initiatives and international development partnerships.

Sub-Saharan African markets present emerging opportunities with countries like South Africa, Nigeria, and Kenya developing specialized oncology capabilities. While facing infrastructure and resource constraints, these markets show promise through international collaboration, technology leapfrogging, and innovative care delivery models. Sub-Saharan development focuses on building foundational capabilities while accessing international expertise and resources.

Regional market distribution shows GCC countries accounting for approximately 45% of advanced therapeutic utilization, North Africa representing 32% of diagnostic activity, and sub-Saharan Africa comprising 23% of emerging market opportunities. These distribution patterns reflect economic development levels, healthcare infrastructure maturity, and population health priorities across the diverse regional landscape.

Market leadership features a combination of international pharmaceutical giants, specialized oncology companies, and regional healthcare providers competing across therapeutic and diagnostic segments. The competitive environment demonstrates increasing intensity as companies seek to establish strong regional presence and capture growing market opportunities.

Competitive strategies focus on regional partnership development, local manufacturing capabilities, and specialized distribution networks addressing unique market requirements. Companies increasingly emphasize patient access programs, healthcare provider education, and clinical research collaboration to strengthen market positioning and support sustainable growth.

By Treatment Type:

By Diagnostic Method:

By End User:

Therapeutic category analysis reveals targeted therapy as the fastest-growing segment, driven by improved efficacy, reduced side effects, and personalized treatment approaches. Targeted therapy adoption shows growth rates exceeding 18% annually in advanced regional medical centers, reflecting increasing physician confidence and patient acceptance of precision medicine approaches.

Immunotherapy segment demonstrates exceptional promise with innovative checkpoint inhibitors and combination therapy protocols showing superior outcomes compared to traditional treatments. Regional adoption varies significantly, with Gulf countries leading implementation while African markets show emerging interest supported by international access programs and clinical trial participation.

Diagnostic category insights highlight advanced imaging technologies as market leaders, with CT and MRI systems providing essential capabilities for kidney cancer detection and staging. Imaging technology utilization reaches approximately 85% in urban medical centers but drops to 45% in rural facilities, indicating significant expansion opportunities in underserved areas.

Molecular diagnostics represent the most innovative diagnostic category, offering personalized treatment selection and prognosis assessment capabilities. While adoption remains limited to specialized centers, growing awareness and declining costs support broader implementation across the regional healthcare landscape.

Healthcare providers benefit from expanded treatment options, improved diagnostic capabilities, and enhanced patient outcomes through access to advanced kidney cancer therapeutics and diagnostics. Modern treatment protocols enable better disease management, reduced complications, and improved quality of life for patients while supporting healthcare facility reputation and specialization development.

Pharmaceutical companies gain access to growing regional markets with substantial unmet medical needs and expanding healthcare infrastructure. Market opportunities include product portfolio expansion, regional partnership development, and clinical research collaboration supporting global development programs while addressing local population health requirements.

Medical device manufacturers benefit from increasing demand for advanced diagnostic equipment, imaging systems, and surgical instruments supporting kidney cancer care delivery. Regional market growth creates opportunities for technology deployment, service expansion, and local partnership development while contributing to healthcare capability enhancement.

Patients and families experience improved access to advanced treatments, better diagnostic accuracy, and enhanced care coordination through market development. Benefits include reduced travel requirements for specialized care, improved treatment outcomes, and expanded insurance coverage supporting affordable access to kidney cancer therapeutics and diagnostics.

Government healthcare systems achieve improved population health outcomes, enhanced medical tourism potential, and strengthened healthcare infrastructure through market development. Benefits include reduced healthcare costs through early detection, improved treatment efficiency, and enhanced regional medical reputation attracting international patients and investment.

Strengths:

Weaknesses:

Opportunities:

Threats:

Personalized medicine adoption represents a transformative trend reshaping kidney cancer treatment approaches across the region. Healthcare providers increasingly utilize genetic testing, biomarker analysis, and molecular profiling to customize treatment protocols for individual patients. Personalized treatment shows adoption rates of approximately 28% in leading medical centers, with expansion expected as technology costs decrease and clinical evidence strengthens.

Digital health integration emerges as a significant trend supporting remote patient monitoring, telemedicine consultation, and electronic health record systems. Digital platforms enhance care coordination, improve treatment adherence, and expand access to specialized expertise across geographic barriers. Digital health adoption accelerates particularly in Gulf countries where technology infrastructure supports advanced healthcare delivery models.

Combination therapy protocols gain prominence as clinical evidence demonstrates superior outcomes through strategic drug combinations and multimodal treatment approaches. Oncologists increasingly prescribe combination regimens targeting multiple cancer pathways simultaneously, improving treatment efficacy while managing side effects through coordinated care protocols.

Minimally invasive procedures trend toward broader adoption as surgical techniques advance and patient preferences shift toward less invasive treatment options. Robotic surgery, laparoscopic procedures, and image-guided interventions offer reduced recovery times, improved outcomes, and enhanced patient satisfaction while supporting healthcare facility differentiation and specialization development.

Regulatory harmonization initiatives across Gulf Cooperation Council countries streamline pharmaceutical approval processes and medical device registration requirements. These developments facilitate regional market access, reduce compliance costs, and accelerate innovative treatment availability while maintaining safety and efficacy standards.

Healthcare infrastructure expansion includes construction of specialized cancer centers, upgrade of diagnostic facilities, and implementation of advanced treatment technologies. Major projects in Saudi Arabia, UAE, and Egypt demonstrate commitment to comprehensive oncology care capability development supporting regional healthcare leadership aspirations.

International partnership agreements between regional healthcare providers and global medical institutions enhance clinical expertise, research capabilities, and treatment protocol development. Collaborations with leading cancer centers in Europe and North America bring advanced knowledge and technology to regional healthcare systems.

Clinical trial expansion activities increase regional participation in international kidney cancer research studies, providing patients access to experimental treatments while contributing to global medical knowledge. MarkWide Research analysis indicates clinical trial participation has increased by 24% over the past two years, reflecting growing research infrastructure and regulatory support.

Market entry strategies should prioritize partnership development with established regional healthcare providers, government agencies, and medical institutions to navigate complex regulatory environments and build sustainable market presence. Companies should focus on understanding local market dynamics, cultural considerations, and healthcare delivery preferences affecting product adoption and commercial success.

Investment priorities should emphasize healthcare infrastructure development, workforce training programs, and technology deployment supporting comprehensive kidney cancer care delivery. Strategic investments in diagnostic capabilities, treatment facilities, and healthcare information systems create foundation for sustainable market growth and improved patient outcomes.

Product development focus should address regional population characteristics, genetic factors, and environmental influences affecting kidney cancer incidence and treatment response. Customized solutions addressing local medical needs, economic constraints, and healthcare delivery preferences enhance market acceptance and clinical effectiveness.

Regulatory engagement requires proactive collaboration with government agencies, medical associations, and healthcare regulators to support policy development, approval process improvement, and market access facilitation. Early engagement in regulatory discussions helps shape favorable policy environments while ensuring compliance with evolving requirements.

Market trajectory indicates sustained growth driven by demographic trends, healthcare investment, and technology advancement supporting expanded kidney cancer care capabilities across the Middle East and Africa region. Long-term growth projections suggest the market will maintain robust expansion rates exceeding 7.5% annually through the next decade, supported by improving healthcare infrastructure and increasing treatment accessibility.

Technology evolution will continue reshaping kidney cancer diagnosis and treatment through artificial intelligence integration, precision medicine advancement, and digital health platform development. Emerging technologies promise improved diagnostic accuracy, personalized treatment selection, and enhanced patient monitoring capabilities while reducing healthcare costs and improving outcomes.

Regional integration efforts will facilitate healthcare collaboration, resource sharing, and expertise exchange across national boundaries. Harmonized regulatory frameworks, standardized treatment protocols, and coordinated research initiatives will strengthen regional healthcare capabilities while improving patient access to advanced kidney cancer care solutions.

Investment opportunities will expand across therapeutic development, diagnostic innovation, and healthcare infrastructure enhancement as regional markets mature and healthcare needs evolve. MWR projections indicate investment requirements will focus on technology deployment, workforce development, and facility expansion supporting comprehensive oncology care delivery across diverse regional markets.

The Middle East and Africa kidney cancer therapeutics and diagnostics market represents a dynamic and rapidly evolving healthcare segment with substantial growth potential driven by demographic trends, healthcare infrastructure development, and increasing disease awareness. Regional markets demonstrate significant opportunities for therapeutic innovation, diagnostic advancement, and comprehensive care delivery improvement while addressing unique population health needs and economic considerations.

Market fundamentals remain strong, supported by government healthcare investment, international collaboration, and growing medical tourism activities that enhance regional healthcare capabilities and reputation. The competitive landscape continues evolving as established pharmaceutical companies, medical device manufacturers, and regional healthcare providers compete to capture expanding market opportunities while addressing diverse patient populations and healthcare delivery requirements.

Future success in this market will depend on strategic partnership development, technology integration, and sustainable business model implementation that addresses regional healthcare challenges while delivering improved patient outcomes. Companies and healthcare providers that successfully navigate regulatory complexities, cultural considerations, and economic constraints while maintaining focus on clinical excellence and patient access will achieve sustainable competitive advantages in this promising healthcare market segment.

What is Kidney Cancer Therapeutics & Diagnostics?

Kidney Cancer Therapeutics & Diagnostics refers to the medical treatments and diagnostic tools used to manage and detect kidney cancer. This includes various therapies such as immunotherapy, targeted therapy, and surgical options, as well as diagnostic imaging and biomarker tests.

What are the key players in the Middle East and Africa Kidney Cancer Therapeutics & Diagnostics Market?

Key players in the Middle East and Africa Kidney Cancer Therapeutics & Diagnostics Market include companies like Roche, Bristol-Myers Squibb, Merck, and Novartis, among others. These companies are involved in developing innovative therapies and diagnostic solutions for kidney cancer.

What are the growth factors driving the Middle East and Africa Kidney Cancer Therapeutics & Diagnostics Market?

The growth of the Middle East and Africa Kidney Cancer Therapeutics & Diagnostics Market is driven by increasing incidence rates of kidney cancer, advancements in diagnostic technologies, and a growing focus on personalized medicine. Additionally, rising healthcare expenditure and improved access to treatment options contribute to market expansion.

What challenges does the Middle East and Africa Kidney Cancer Therapeutics & Diagnostics Market face?

The Middle East and Africa Kidney Cancer Therapeutics & Diagnostics Market faces challenges such as limited access to advanced healthcare facilities, high treatment costs, and varying levels of awareness about kidney cancer. These factors can hinder early diagnosis and effective treatment.

What opportunities exist in the Middle East and Africa Kidney Cancer Therapeutics & Diagnostics Market?

Opportunities in the Middle East and Africa Kidney Cancer Therapeutics & Diagnostics Market include the potential for new drug development, increasing investment in healthcare infrastructure, and the expansion of telemedicine services. These factors can enhance patient access to innovative treatments and diagnostics.

What trends are shaping the Middle East and Africa Kidney Cancer Therapeutics & Diagnostics Market?

Trends shaping the Middle East and Africa Kidney Cancer Therapeutics & Diagnostics Market include the rise of targeted therapies, the integration of artificial intelligence in diagnostics, and a shift towards minimally invasive surgical techniques. These trends are improving patient outcomes and streamlining treatment processes.

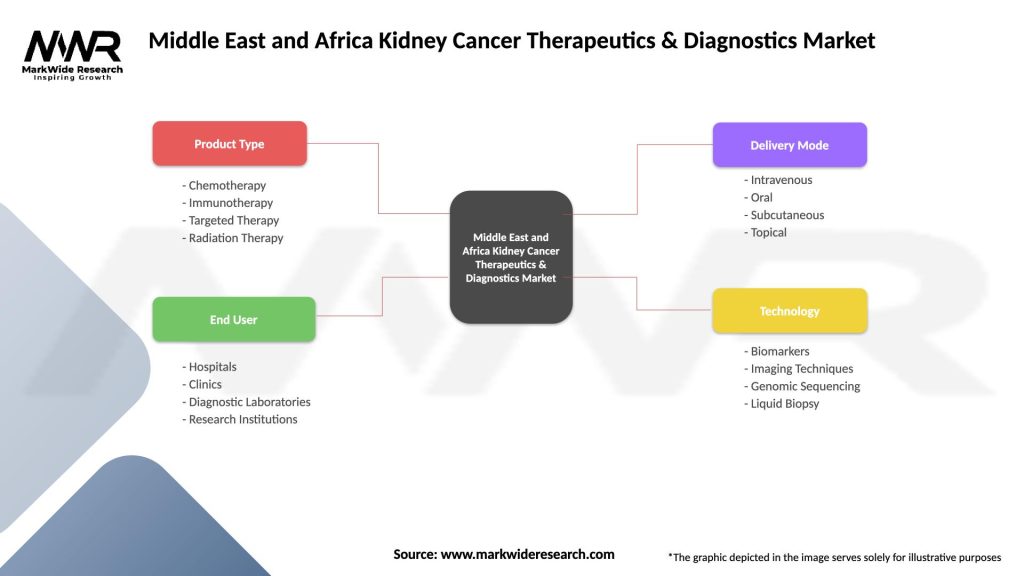

Middle East and Africa Kidney Cancer Therapeutics & Diagnostics Market

| Segmentation Details | Description |

|---|---|

| Product Type | Chemotherapy, Immunotherapy, Targeted Therapy, Radiation Therapy |

| End User | Hospitals, Clinics, Diagnostic Laboratories, Research Institutions |

| Delivery Mode | Intravenous, Oral, Subcutaneous, Topical |

| Technology | Biomarkers, Imaging Techniques, Genomic Sequencing, Liquid Biopsy |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Middle East and Africa Kidney Cancer Therapeutics & Diagnostics Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.