444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Middle East and Africa electric vehicle battery manufacturing market represents a rapidly emerging sector within the global automotive electrification landscape. This dynamic market encompasses the production, assembly, and distribution of lithium-ion batteries, solid-state batteries, and other advanced energy storage solutions specifically designed for electric vehicles across the MEA region. Market dynamics indicate substantial growth potential driven by increasing government initiatives, rising environmental awareness, and strategic investments in clean energy infrastructure.

Regional development varies significantly across the Middle East and Africa, with countries like the United Arab Emirates, Saudi Arabia, and South Africa leading the charge in establishing manufacturing capabilities. The market is experiencing accelerated growth at approximately 12.5% CAGR as nations prioritize energy diversification and sustainable transportation solutions. Manufacturing capabilities are expanding through strategic partnerships between international battery manufacturers and local automotive companies, creating a robust ecosystem for electric vehicle battery production.

Investment patterns show increasing capital allocation toward battery manufacturing facilities, with particular emphasis on lithium-ion technology and emerging solid-state battery solutions. The market benefits from abundant mineral resources in Africa, including lithium, cobalt, and rare earth elements essential for battery production. Government support through favorable policies, tax incentives, and infrastructure development programs continues to drive market expansion across key regional markets.

The Middle East and Africa electric vehicle battery manufacturing market refers to the comprehensive ecosystem of companies, facilities, and supply chains involved in producing energy storage systems specifically designed for electric vehicles within the MEA region. This market encompasses various battery technologies including lithium-ion, nickel-metal hydride, and emerging solid-state batteries, along with associated manufacturing processes, quality control systems, and distribution networks.

Manufacturing scope includes cell production, battery pack assembly, thermal management systems, and battery management software integration. The market covers both original equipment manufacturer (OEM) production and aftermarket battery solutions, serving passenger vehicles, commercial trucks, buses, and specialized electric vehicles. Value chain integration extends from raw material processing and cell manufacturing to final assembly and recycling services, creating a comprehensive battery ecosystem across the region.

Market transformation in the Middle East and Africa electric vehicle battery manufacturing sector reflects the region’s strategic shift toward sustainable mobility solutions and energy independence. The market demonstrates robust growth potential driven by government mandates, increasing electric vehicle adoption, and substantial investments in manufacturing infrastructure. Key market drivers include environmental regulations, declining battery costs, and growing consumer awareness of electric vehicle benefits.

Regional leadership emerges from countries implementing comprehensive electric mobility strategies, with the UAE and Saudi Arabia establishing themselves as manufacturing hubs through strategic partnerships and foreign direct investment. Technology adoption focuses primarily on lithium-ion battery systems, with approximately 78% market share due to proven performance and established supply chains. Manufacturing capacity expansion continues through joint ventures between international battery manufacturers and regional automotive companies.

Competitive dynamics feature a mix of global battery manufacturers establishing regional operations and emerging local companies developing specialized solutions for regional market requirements. The market benefits from abundant natural resources, strategic geographic positioning, and increasing government support for clean energy initiatives across multiple countries in the region.

Strategic insights reveal several critical factors shaping the Middle East and Africa electric vehicle battery manufacturing market:

Government initiatives serve as the primary catalyst for electric vehicle battery manufacturing market growth across the Middle East and Africa. National electrification strategies, carbon reduction targets, and clean energy mandates create substantial demand for locally manufactured battery solutions. Policy support includes tax incentives, import duty reductions, and direct subsidies for battery manufacturing facilities, encouraging both domestic and international investment in the sector.

Environmental consciousness drives increasing adoption of electric vehicles, creating corresponding demand for battery manufacturing capacity. Rising fuel costs, air quality concerns, and climate change awareness motivate consumers and fleet operators to transition toward electric mobility solutions. Corporate sustainability initiatives by major companies and government agencies further accelerate electric vehicle procurement, supporting battery manufacturing market expansion.

Economic diversification strategies across oil-dependent Middle Eastern economies prioritize clean technology manufacturing as a means of reducing petroleum reliance. Countries like Saudi Arabia and the UAE view electric vehicle battery manufacturing as a strategic industry for economic transformation. Resource availability in African markets provides cost advantages for battery raw materials, supporting competitive manufacturing operations and export potential.

Technology advancement in battery chemistry, manufacturing processes, and energy density improvements makes electric vehicles increasingly attractive to consumers. Cost reduction in battery production, with manufacturing costs declining by approximately 15% annually, enhances electric vehicle affordability and market penetration across price-sensitive regional markets.

Infrastructure limitations present significant challenges for electric vehicle battery manufacturing market development across the Middle East and Africa. Inadequate charging infrastructure, unreliable power grids, and limited technical expertise constrain market growth potential. Manufacturing complexity requires sophisticated production facilities, specialized equipment, and highly skilled workforce, creating barriers for new market entrants and regional manufacturers.

Capital requirements for establishing battery manufacturing facilities demand substantial upfront investments, often exceeding the financial capabilities of local companies. Technology gaps between international manufacturers and regional companies create competitive disadvantages and dependency on foreign technology licensing. Supply chain vulnerabilities expose manufacturers to raw material price volatility and availability constraints, particularly for critical battery components.

Regulatory uncertainty in some regional markets creates investment hesitation among potential manufacturers and technology partners. Quality standards and certification requirements for battery safety and performance may exceed current regional manufacturing capabilities, necessitating significant investment in quality control systems and testing facilities.

Market maturity limitations result in relatively small domestic electric vehicle markets, constraining economies of scale for local battery manufacturers. Competition from established international manufacturers with proven track records and advanced technology creates market entry challenges for regional companies attempting to develop battery manufacturing capabilities.

Strategic partnerships between international battery manufacturers and regional companies create substantial opportunities for technology transfer, market development, and manufacturing capability enhancement. Joint ventures enable knowledge sharing, risk distribution, and access to established supply chains while providing international partners with regional market access and resource advantages.

Export potential represents a significant opportunity for Middle East and Africa battery manufacturers to serve global markets, particularly as international companies seek supply chain diversification. Resource integration opportunities allow regional manufacturers to develop vertically integrated operations, from raw material extraction through finished battery production, creating competitive cost advantages.

Government procurement programs for electric vehicle fleets provide stable demand foundations for regional battery manufacturers. Public transportation electrification initiatives, including bus and taxi fleet conversions, create substantial market opportunities for specialized battery solutions. Commercial vehicle electrification in logistics, mining, and construction sectors offers high-value market segments for battery manufacturers.

Innovation opportunities in battery recycling, second-life applications, and specialized battery chemistries for extreme climate conditions provide differentiation possibilities for regional manufacturers. Research collaboration with international universities and technology institutes can accelerate innovation and establish the region as a center for battery technology development.

Competitive dynamics in the Middle East and Africa electric vehicle battery manufacturing market reflect the interplay between established international manufacturers and emerging regional companies. Market consolidation trends show increasing collaboration between global technology leaders and local manufacturing partners, creating hybrid business models that leverage international expertise with regional advantages.

Technology evolution drives continuous market transformation, with manufacturers investing in next-generation battery chemistries, improved energy density, and enhanced safety features. Manufacturing efficiency improvements through automation and process optimization enable cost reductions of approximately 8-10% annually, supporting market competitiveness and expansion.

Supply chain dynamics emphasize regional integration and reduced import dependency, with manufacturers developing local supplier networks for battery components and raw materials. Quality assurance requirements drive investment in testing facilities, certification processes, and manufacturing standards compliance, ensuring international market acceptance of regional battery products.

Market segmentation reveals distinct opportunities across passenger vehicles, commercial transportation, and stationary energy storage applications. Customer preferences vary significantly across different regional markets, requiring customized battery solutions and manufacturing approaches to address specific performance, cost, and durability requirements.

Comprehensive analysis of the Middle East and Africa electric vehicle battery manufacturing market employs multiple research methodologies to ensure accuracy and reliability of market insights. Primary research includes extensive interviews with industry executives, government officials, technology experts, and key stakeholders across the regional market ecosystem.

Secondary research encompasses analysis of government publications, industry reports, company financial statements, and regulatory documents from key markets across the Middle East and Africa. Market data collection involves systematic monitoring of manufacturing capacity announcements, investment commitments, and technology partnership agreements throughout the region.

Quantitative analysis utilizes statistical modeling, trend analysis, and forecasting techniques to project market development scenarios and growth trajectories. Qualitative assessment incorporates expert opinions, industry insights, and strategic analysis to understand market dynamics, competitive positioning, and future opportunities.

Validation processes ensure data accuracy through cross-referencing multiple sources, expert review, and consistency checks across different market segments and geographic regions. MarkWide Research methodology emphasizes comprehensive market coverage, objective analysis, and actionable insights for industry participants and stakeholders.

United Arab Emirates leads the Middle East electric vehicle battery manufacturing market through strategic government initiatives, substantial infrastructure investments, and partnerships with international technology companies. The UAE’s market share represents approximately 35% of regional manufacturing capacity, driven by Dubai’s smart city initiatives and Abu Dhabi’s clean energy strategy. Manufacturing facilities focus on lithium-ion battery assembly and pack integration for both domestic and export markets.

Saudi Arabia demonstrates rapid market development through the NEOM project and Vision 2030 economic diversification strategy. Investment commitments exceed previous regional benchmarks, with emphasis on establishing comprehensive battery manufacturing ecosystems. Strategic partnerships with international manufacturers accelerate technology transfer and manufacturing capability development across the kingdom.

South Africa represents the largest African market for electric vehicle battery manufacturing, leveraging abundant mineral resources and established automotive manufacturing infrastructure. Market positioning focuses on serving both domestic demand and export opportunities to other African markets. Resource advantages in lithium and platinum group metals provide competitive manufacturing cost structures.

Egypt emerges as a strategic manufacturing hub for North African markets, with government support for electric vehicle assembly and battery production. Geographic positioning offers access to European, Middle Eastern, and African markets, supporting export-oriented manufacturing strategies. Investment incentives attract international manufacturers seeking regional production capabilities.

Morocco develops battery manufacturing capabilities through automotive industry partnerships and renewable energy integration. Manufacturing focus emphasizes cost-effective production for European export markets while serving growing domestic electric vehicle demand.

Market leadership in the Middle East and Africa electric vehicle battery manufacturing sector features a combination of international technology companies and emerging regional manufacturers:

Competitive strategies emphasize technology localization, supply chain integration, and customized solutions for regional market conditions. Partnership models facilitate knowledge transfer while providing international manufacturers with access to regional resources and markets.

By Battery Type:

By Vehicle Type:

By Application:

Lithium-ion Battery Manufacturing dominates the regional market through established technology, proven performance, and extensive supply chain development. Manufacturing processes focus on cell production, pack assembly, and thermal management system integration. Cost optimization strategies emphasize automation, quality control, and supply chain efficiency improvements.

Solid-state Battery Development represents the next generation of battery technology with superior safety characteristics and energy density potential. Research investments by regional manufacturers and international partners accelerate technology development and commercial viability. Manufacturing challenges include production scalability and cost competitiveness compared to lithium-ion alternatives.

Commercial Vehicle Batteries require specialized solutions for heavy-duty applications, extreme operating conditions, and extended service life requirements. Performance specifications emphasize durability, fast charging capabilities, and thermal management for commercial fleet operations. Market opportunities include public transportation, logistics, and industrial vehicle electrification.

Battery Management Systems integration becomes increasingly sophisticated, incorporating advanced monitoring, safety features, and performance optimization capabilities. Software development focuses on predictive maintenance, energy optimization, and integration with vehicle control systems.

Manufacturing Companies benefit from access to abundant raw materials, government incentives, and growing regional demand for electric vehicle batteries. Cost advantages through resource proximity and competitive labor costs enhance manufacturing competitiveness. Market access to both domestic and export opportunities provides revenue diversification and growth potential.

Government Stakeholders achieve economic diversification objectives, job creation, and environmental sustainability goals through battery manufacturing industry development. Technology transfer enhances regional innovation capabilities and industrial competitiveness. Energy security improvements through domestic battery production reduce import dependency and enhance supply chain resilience.

Automotive Manufacturers gain access to locally produced battery solutions, reducing supply chain risks and transportation costs. Customization opportunities enable development of batteries optimized for regional operating conditions and customer requirements. Partnership potential with regional battery manufacturers supports integrated electric vehicle development strategies.

Investors access high-growth market opportunities with substantial government support and favorable regulatory environments. Resource advantages provide competitive positioning and potential returns through vertical integration strategies. Export potential offers market expansion opportunities beyond regional boundaries.

Strengths:

Weaknesses:

Opportunities:

Threats:

Localization Strategies drive increasing emphasis on domestic battery manufacturing capabilities, reducing import dependency and enhancing supply chain resilience. Government mandates for local content requirements accelerate investment in regional manufacturing facilities and technology transfer programs. Manufacturing partnerships between international companies and regional firms create hybrid business models leveraging global expertise with local advantages.

Technology Innovation focuses on developing battery solutions optimized for extreme climate conditions prevalent across Middle Eastern and African markets. Research investments in thermal management, durability enhancement, and performance optimization address specific regional operating requirements. Next-generation technologies including solid-state batteries and advanced lithium chemistries receive increasing attention from manufacturers and investors.

Sustainability Integration emphasizes environmentally responsible manufacturing processes, battery recycling programs, and circular economy principles. Recycling infrastructure development supports sustainable battery lifecycle management and raw material recovery. Carbon footprint reduction initiatives align with global environmental standards and customer expectations.

Digital Integration incorporates Industry 4.0 technologies, artificial intelligence, and advanced analytics into battery manufacturing processes. Quality control systems utilize machine learning and predictive analytics to optimize production efficiency and product reliability. Supply chain digitization enhances transparency, traceability, and risk management capabilities.

Strategic Investments continue expanding across the Middle East and Africa, with major announcements including new manufacturing facilities, technology partnerships, and capacity expansion projects. Government initiatives provide substantial financial support through direct investment, tax incentives, and infrastructure development programs supporting battery manufacturing industry growth.

Technology Partnerships between international battery manufacturers and regional companies accelerate knowledge transfer and manufacturing capability development. Joint ventures enable risk sharing, market access, and technology localization while providing international partners with resource advantages and regional market penetration opportunities.

Infrastructure Development includes charging network expansion, grid modernization, and manufacturing facility construction supporting electric vehicle adoption and battery manufacturing industry growth. Research facilities establishment enhances regional innovation capabilities and supports technology development initiatives.

Regulatory Frameworks evolution includes updated safety standards, environmental regulations, and industry certification requirements ensuring international competitiveness of regional battery manufacturers. Trade agreements facilitate export opportunities and international market access for regional battery producers.

Strategic Focus recommendations emphasize developing core competencies in specific battery technologies and applications rather than attempting to compete across all market segments. MarkWide Research analysis suggests prioritizing partnerships with established international manufacturers to accelerate technology transfer and market development while leveraging regional resource advantages.

Investment Priorities should emphasize manufacturing infrastructure, workforce development, and quality assurance systems to ensure international competitiveness. Technology development investments should focus on applications optimized for regional operating conditions and customer requirements rather than competing directly with established international technologies.

Market Entry strategies should leverage government support programs, resource advantages, and strategic partnerships to overcome barriers and accelerate market penetration. Export development requires early establishment of international quality certifications and supply chain partnerships to access global markets effectively.

Risk Management approaches should address technology obsolescence, supply chain vulnerabilities, and market volatility through diversification strategies and flexible manufacturing capabilities. Sustainability integration becomes increasingly important for long-term competitiveness and market acceptance.

Market trajectory for the Middle East and Africa electric vehicle battery manufacturing sector indicates sustained growth driven by government support, increasing electric vehicle adoption, and strategic investments in manufacturing infrastructure. Growth projections suggest the market will expand at approximately 12.5% CAGR over the next decade, supported by favorable policy environments and resource advantages.

Technology evolution will emphasize next-generation battery chemistries, improved manufacturing processes, and specialized solutions for regional operating conditions. Solid-state batteries are expected to achieve commercial viability within the forecast period, representing approximately 15-20% market share by 2030. Manufacturing automation will enhance production efficiency and quality consistency while reducing operational costs.

Regional leadership will likely consolidate around countries with comprehensive electric mobility strategies, substantial government support, and successful international partnerships. Export opportunities will expand as global manufacturers seek supply chain diversification and regional companies develop international quality standards and certifications.

Industry maturation will feature increased consolidation, technology standardization, and supply chain integration. MWR projections indicate that successful regional manufacturers will achieve significant market positions through strategic partnerships, technology innovation, and operational excellence. Sustainability requirements will drive investment in recycling infrastructure and environmentally responsible manufacturing processes.

The Middle East and Africa electric vehicle battery manufacturing market represents a transformative opportunity for regional economic development, technological advancement, and sustainable mobility solutions. Market fundamentals including abundant natural resources, government support, and growing electric vehicle adoption create a favorable environment for industry development and international competitiveness.

Strategic advantages through resource proximity, cost competitiveness, and government incentives position the region for significant market growth and export potential. Technology partnerships with international manufacturers accelerate capability development while providing access to established supply chains and global markets. Investment momentum continues building across multiple countries, creating a comprehensive regional ecosystem for battery manufacturing and electric vehicle support.

Future success will depend on continued government support, effective technology transfer, and development of specialized solutions addressing regional market requirements. The Middle East and Africa electric vehicle battery manufacturing market is positioned to become a significant contributor to global battery supply chains while supporting regional economic diversification and environmental sustainability objectives.

What is Electric Vehicle Battery Manufacturing?

Electric Vehicle Battery Manufacturing refers to the production processes involved in creating batteries specifically designed for electric vehicles, including lithium-ion and solid-state batteries. This sector is crucial for the growth of electric mobility and sustainable transportation solutions.

What are the key players in the Middle East And Africa Electric Vehicle Battery Manufacturing Market?

Key players in the Middle East And Africa Electric Vehicle Battery Manufacturing Market include companies like LG Chem, Samsung SDI, and AESC, which are known for their advancements in battery technology and production capabilities, among others.

What are the growth factors driving the Middle East And Africa Electric Vehicle Battery Manufacturing Market?

The growth of the Middle East And Africa Electric Vehicle Battery Manufacturing Market is driven by increasing demand for electric vehicles, government incentives for clean energy, and advancements in battery technology that enhance performance and reduce costs.

What challenges does the Middle East And Africa Electric Vehicle Battery Manufacturing Market face?

Challenges in the Middle East And Africa Electric Vehicle Battery Manufacturing Market include supply chain disruptions, high raw material costs, and the need for skilled labor to support advanced manufacturing processes.

What opportunities exist in the Middle East And Africa Electric Vehicle Battery Manufacturing Market?

Opportunities in the Middle East And Africa Electric Vehicle Battery Manufacturing Market include the potential for local production to reduce import dependency, partnerships with automotive manufacturers, and investments in research and development for innovative battery technologies.

What trends are shaping the Middle East And Africa Electric Vehicle Battery Manufacturing Market?

Trends in the Middle East And Africa Electric Vehicle Battery Manufacturing Market include the shift towards sustainable materials, the development of fast-charging technologies, and the increasing integration of renewable energy sources in battery production.

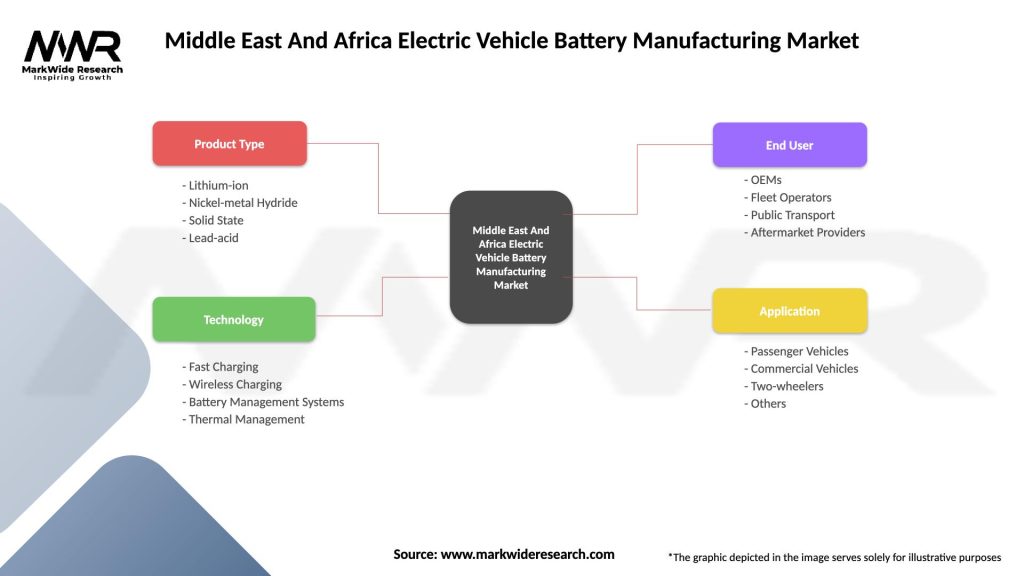

Middle East And Africa Electric Vehicle Battery Manufacturing Market

| Segmentation Details | Description |

|---|---|

| Product Type | Lithium-ion, Nickel-metal Hydride, Solid State, Lead-acid |

| Technology | Fast Charging, Wireless Charging, Battery Management Systems, Thermal Management |

| End User | OEMs, Fleet Operators, Public Transport, Aftermarket Providers |

| Application | Passenger Vehicles, Commercial Vehicles, Two-wheelers, Others |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Middle East And Africa Electric Vehicle Battery Manufacturing Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.