444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

Market Overview

The Middle East and Africa bunker fuel market is a significant sector within the global energy market. Bunker fuel, also known as marine fuel or ship fuel, refers to the fuel used by ships and vessels for propulsion. It is a vital component of the shipping industry and plays a crucial role in global trade and transportation.

Meaning

Bunker fuel is a type of fuel specifically designed for maritime vessels, including cargo ships, tankers, and container ships. It provides the energy required for propulsion and other onboard operations during a voyage. Bunker fuel is typically characterized by its high viscosity and high sulfur content, which allows it to meet the demanding needs of marine engines. The Middle East and Africa region, with its strategic location and abundant oil reserves, holds a significant share in the global bunker fuel market.

Executive Summary

The Middle East and Africa bunker fuel market has experienced steady growth over the years, driven by increasing international trade, rising maritime activities, and the region’s vast oil reserves. The market is highly competitive, with several key players vying for market share. The COVID-19 pandemic has also impacted the market, leading to temporary disruptions in supply chains and a decline in demand. However, as the global economy recovers and trade volumes rebound, the bunker fuel market is expected to regain its momentum.

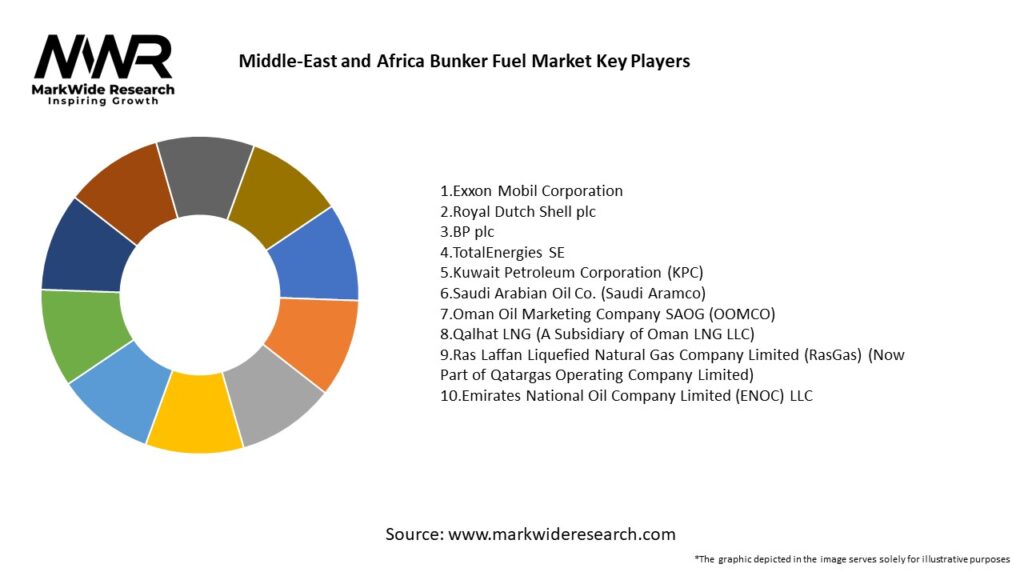

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

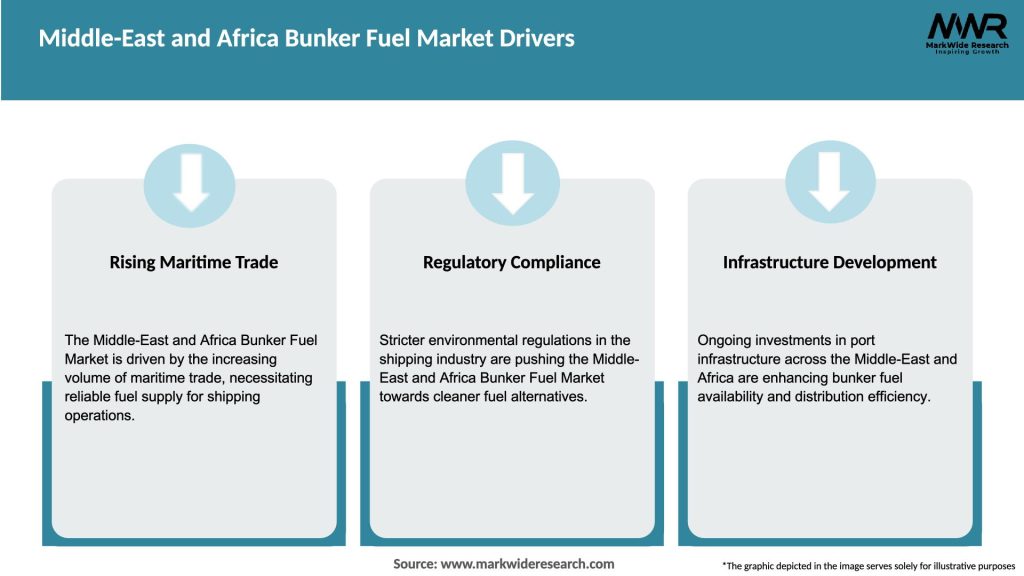

Market Drivers

Market Restraints

Market Opportunities

Market Dynamics

The Middle East and Africa bunker fuel market is influenced by various dynamic factors, including economic trends, geopolitical developments, regulatory changes, and technological advancements. These dynamics shape the market landscape and impact the strategies adopted by industry participants.

Economic trends, such as fluctuations in oil prices and changes in global trade patterns, can have a significant impact on bunker fuel demand. Geopolitical developments, including conflicts and regional tensions, may disrupt shipping routes and influence market dynamics. Regulatory changes, particularly related to environmental standards, can drive the adoption of cleaner fuels and impact the demand for traditional bunker fuel.

Technological advancements play a crucial role in the evolution of the bunker fuel market. Innovations in engine design, exhaust gas cleaning systems (scrubbers), and alternative fuel technologies present opportunities for market growth and product diversification.

Regional Analysis

The Middle East and Africa region comprises several countries with strategic locations along major shipping routes. The region’s rich oil reserves make it a significant player in the global bunker fuel market. Key countries in the region include Saudi Arabia, the United Arab Emirates, South Africa, Nigeria, and Egypt.

Saudi Arabia, with its vast oil reserves and extensive port infrastructure, is a major supplier of bunker fuel. The United Arab Emirates, particularly Dubai and Fujairah, has emerged as a prominent bunkering hub in the region. South Africa plays a vital role in the African maritime industry, with its ports serving as key gateways for trade. Nigeria and Egypt also have significant shipping activities and contribute to the region’s bunker fuel market.

Competitive Landscape

Leading Companies in Middle-East and Africa Bunker Fuel Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

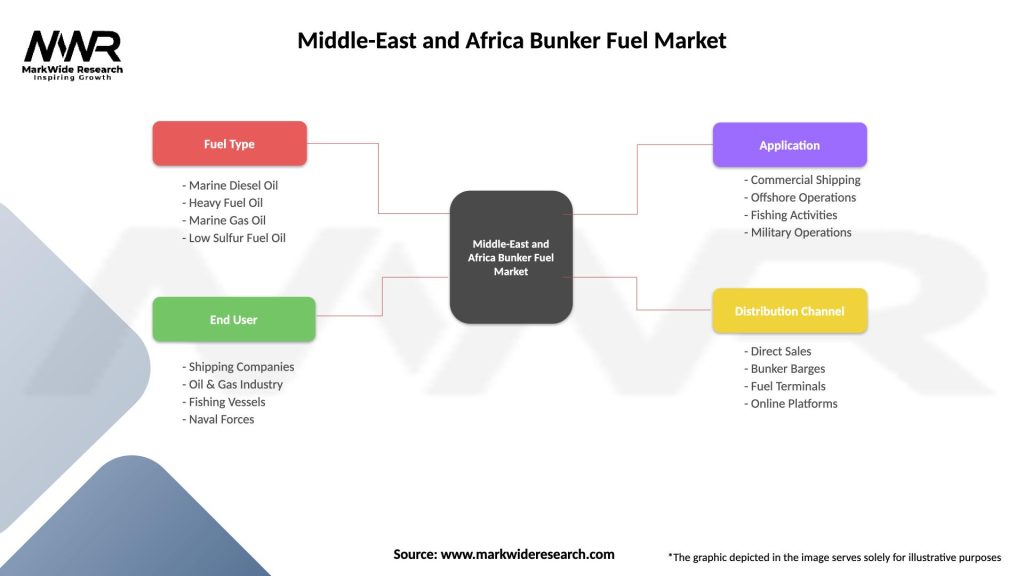

Segmentation

The Middle East and Africa bunker fuel market can be segmented based on fuel type, end-use, and distribution channel.

By fuel type, the market can be segmented into:

By end-use, the market can be segmented into:

By distribution channel,the market can be segmented into:

These segmentation criteria help understand the market dynamics and cater to the specific needs of different end-users.

Category-wise Insights

Key Benefits for Industry Participants and Stakeholders

SWOT Analysis

Strengths:

Weaknesses:

Opportunities:

Threats:

Market Key Trends

Covid-19 Impact

The COVID-19 pandemic had a significant impact on the Middle East and Africa bunker fuel market. The restrictions imposed to control the spread of the virus, such as lockdowns and travel bans, resulted in a decline in global trade and reduced maritime activities. This led to a temporary decrease in bunker fuel demand.

The closure of ports and disruptions in supply chains affected the availability of bunker fuel. Moreover, the volatility in oil prices during the pandemic added uncertainty to the market, impacting the profitability of bunker fuel suppliers.

However, as the global economy recovers and trade volumes rebound, the bunker fuel market is expected to regain its momentum. The resumption of maritime activities and the gradual lifting of travel restrictions will contribute to the recovery of the market.

Key Industry Developments

Analyst Suggestions

Future Outlook

The Middle East and Africa bunker fuel market is expected to witness steady growth in the coming years. The region’s strategic location, abundant oil reserves, and increasing maritime activities will continue to drive the demand for bunker fuel.

The adoption of low-sulfur fuels, scrubber installations, and the development of LNG bunkering infrastructure will shape the future of the market. The focus on sustainability and the transition towards cleaner fuels will open up new opportunities for industry participants.

However, the market also faces challenges, such as environmental concerns and the volatility of oil prices. Industry players need to remain agile, adapt to regulatory changes, and invest in technological advancements to stay competitive and capture market share.

Conclusion

In conclusion, the Middle East and Africa bunker fuel market is poised for growth, driven by factors such as increasing international trade, expanding maritime activities, and government initiatives. The market presents opportunities for the adoption of low-sulfur fuels, scrubber technologies, and the development of LNG bunkering infrastructure. By embracing sustainability, strengthening supply chains, and leveraging digitalization, industry participants can navigate the evolving landscape and secure a prosperous future in the bunker fuel market.

What is Bunker Fuel?

Bunker fuel refers to the fuel used aboard ships, primarily for propulsion and power generation. It is a crucial component in the maritime industry, particularly for commercial shipping and naval operations.

What are the key players in the Middle-East and Africa Bunker Fuel Market?

Key players in the Middle-East and Africa Bunker Fuel Market include companies like Emirates National Oil Company (ENOC), Gulf Oil Marine, and Total Marine Fuels, among others.

What are the main drivers of the Middle-East and Africa Bunker Fuel Market?

The main drivers of the Middle-East and Africa Bunker Fuel Market include the growth of international trade, increasing shipping activities, and the expansion of port infrastructure in the region.

What challenges does the Middle-East and Africa Bunker Fuel Market face?

Challenges in the Middle-East and Africa Bunker Fuel Market include regulatory compliance with environmental standards, fluctuations in crude oil prices, and competition from alternative fuels.

What opportunities exist in the Middle-East and Africa Bunker Fuel Market?

Opportunities in the Middle-East and Africa Bunker Fuel Market include the adoption of cleaner fuel technologies, investment in sustainable shipping practices, and the potential for growth in offshore oil and gas exploration.

What trends are shaping the Middle-East and Africa Bunker Fuel Market?

Trends shaping the Middle-East and Africa Bunker Fuel Market include the shift towards low-sulfur fuels, advancements in fuel management technologies, and increasing focus on reducing greenhouse gas emissions in shipping.

Middle-East and Africa Bunker Fuel Market

| Segmentation Details | Description |

|---|---|

| Fuel Type | Marine Diesel Oil, Heavy Fuel Oil, Marine Gas Oil, Low Sulfur Fuel Oil |

| End User | Shipping Companies, Oil & Gas Industry, Fishing Vessels, Naval Forces |

| Application | Commercial Shipping, Offshore Operations, Fishing Activities, Military Operations |

| Distribution Channel | Direct Sales, Bunker Barges, Fuel Terminals, Online Platforms |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading Companies in Middle-East and Africa Bunker Fuel Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.