444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Mexico plastic packaging films market represents a dynamic and rapidly evolving sector within the country’s broader packaging industry. This market encompasses a diverse range of flexible plastic films used across multiple applications, from food packaging to industrial wrapping solutions. Market dynamics indicate robust growth driven by increasing consumer demand, expanding manufacturing capabilities, and evolving packaging technologies.

Growth trajectories in the Mexican plastic packaging films sector demonstrate remarkable resilience, with the market experiencing a compound annual growth rate (CAGR) of 6.2% over recent years. This expansion reflects Mexico’s strategic position as a manufacturing hub and its growing domestic consumption patterns. Industry participants benefit from the country’s proximity to major North American markets and favorable trade agreements that facilitate cross-border commerce.

Technological advancements continue to reshape the landscape, with manufacturers increasingly adopting sustainable production methods and innovative film formulations. The integration of biodegradable materials and enhanced barrier properties has become a defining characteristic of the modern Mexican plastic packaging films market, positioning it for sustained growth in the coming decade.

The Mexico plastic packaging films market refers to the comprehensive ecosystem of flexible plastic film production, distribution, and consumption within Mexican territory. This market encompasses various polymer-based films including polyethylene, polypropylene, polyester, and specialty barrier films used for packaging applications across diverse industries.

Plastic packaging films serve as protective barriers that preserve product integrity, extend shelf life, and facilitate efficient distribution. These films are manufactured through processes such as blown film extrusion, cast film production, and multilayer co-extrusion, creating products with specific performance characteristics tailored to end-user requirements.

Market scope includes both rigid and flexible film applications, spanning food and beverage packaging, pharmaceutical wrapping, industrial protective films, and consumer goods packaging. The Mexican market’s unique position benefits from domestic production capabilities combined with strategic imports from regional partners, creating a balanced supply ecosystem.

Strategic positioning of Mexico’s plastic packaging films market reflects the country’s emergence as a key player in North American packaging supply chains. The market demonstrates strong fundamentals with consistent demand growth across multiple sectors, particularly in food packaging where 75% of total consumption is concentrated.

Manufacturing capabilities have expanded significantly, with domestic production facilities increasingly adopting advanced technologies and sustainable practices. This evolution supports both local market needs and export opportunities, particularly to the United States and Canada. Investment flows into the sector have accelerated, driven by multinational corporations establishing regional production hubs.

Sustainability initiatives are becoming increasingly important, with 40% of manufacturers implementing recycling programs and developing bio-based film alternatives. These efforts align with global environmental trends and regulatory requirements, positioning Mexican producers favorably in international markets. Market consolidation continues as larger players acquire smaller operations to achieve economies of scale and technological integration.

Market segmentation reveals distinct patterns in consumption and growth across different application areas. The following insights highlight critical market dynamics:

Economic growth serves as a fundamental driver for Mexico’s plastic packaging films market, with expanding GDP supporting increased consumer spending and industrial activity. The country’s growing middle class demonstrates higher consumption of packaged goods, directly translating to increased demand for flexible packaging solutions.

Manufacturing sector expansion significantly impacts market dynamics, particularly in automotive, electronics, and food processing industries. Mexico’s position as a preferred manufacturing destination for multinational corporations creates sustained demand for industrial packaging films and protective materials. Foreign direct investment continues to flow into manufacturing sectors, supporting packaging demand growth.

Urbanization trends contribute to changing consumption patterns, with urban populations showing preference for convenient, packaged products. This demographic shift supports growth in retail packaging applications and drives innovation in consumer-friendly packaging formats. E-commerce expansion further amplifies demand for protective packaging films used in shipping and logistics applications.

Trade agreements including USMCA provide market access advantages and encourage cross-border commerce, supporting both domestic production and export opportunities. These agreements facilitate technology transfer and investment flows that strengthen the overall market ecosystem.

Environmental concerns pose significant challenges to the plastic packaging films market, with increasing regulatory pressure and consumer awareness driving demand for sustainable alternatives. Government initiatives targeting single-use plastics create compliance costs and require substantial investment in alternative technologies.

Raw material price volatility affects profitability and planning capabilities for manufacturers. Fluctuations in petroleum prices directly impact production costs for polymer-based films, creating margin pressure and requiring sophisticated hedging strategies. Supply chain disruptions can significantly impact operations, particularly for companies dependent on imported raw materials.

Regulatory complexity increases operational challenges, with evolving food safety standards, environmental regulations, and trade requirements creating compliance burdens. Companies must invest in quality systems and regulatory expertise to maintain market access and avoid penalties.

Competition from alternative packaging materials including paper, glass, and metal containers limits growth potential in certain applications. Consumer preferences for perceived environmentally friendly alternatives can reduce demand for traditional plastic films, particularly in premium market segments.

Sustainable packaging innovation presents substantial opportunities for companies developing biodegradable, compostable, and recyclable film solutions. Market demand for eco-friendly alternatives continues growing, with consumers willing to pay premium prices for environmentally responsible packaging options.

Smart packaging technologies offer differentiation opportunities through integration of sensors, indicators, and interactive features. These advanced solutions provide added value for food safety, product authentication, and consumer engagement applications. Digital printing capabilities enable customization and shorter production runs, supporting brand differentiation strategies.

Export market expansion leverages Mexico’s competitive advantages in serving North and South American markets. Strategic positioning and cost competitiveness create opportunities for Mexican manufacturers to capture market share from higher-cost producers. Nearshoring trends support this expansion as companies seek to reduce supply chain risks and transportation costs.

Pharmaceutical packaging growth represents a high-value opportunity segment, with stringent quality requirements and premium pricing supporting attractive margins. Mexico’s growing pharmaceutical manufacturing sector creates domestic demand while export opportunities exist in regional markets.

Supply chain integration characterizes the modern Mexican plastic packaging films market, with manufacturers increasingly developing vertical integration strategies to control costs and quality. This integration extends from raw material sourcing through converting and distribution, creating more resilient business models.

Technology adoption rates vary significantly across market segments, with food packaging leading in advanced barrier technologies while industrial applications focus on cost optimization. Automation levels in production facilities have increased by 35% over recent years, improving efficiency and consistency while reducing labor dependency.

Customer relationship dynamics are evolving toward longer-term partnerships and collaborative product development. Brand owners increasingly seek packaging suppliers who can provide technical expertise, sustainability solutions, and supply chain reliability. Service integration becomes a key differentiator as customers value comprehensive solutions over commodity products.

Market concentration continues as larger players acquire smaller operations to achieve scale advantages and technology access. This consolidation creates opportunities for specialized niche players while challenging mid-sized companies to differentiate their offerings or seek strategic partnerships.

Primary research forms the foundation of comprehensive market analysis, incorporating extensive interviews with industry executives, manufacturers, suppliers, and end-users across Mexico’s plastic packaging films ecosystem. This approach ensures current market insights and validates quantitative findings through qualitative assessment.

Secondary research encompasses analysis of industry publications, government statistics, trade association reports, and company financial statements to establish market baselines and identify trends. Data triangulation methods verify findings across multiple sources, ensuring accuracy and reliability of market assessments.

Market modeling employs sophisticated analytical techniques to project future trends and quantify market opportunities. These models incorporate economic indicators, demographic trends, regulatory changes, and technological developments to provide comprehensive market forecasts.

Industry validation processes include expert panel reviews and stakeholder feedback sessions to ensure research findings accurately reflect market realities. This validation approach enhances the credibility and practical applicability of market insights for strategic decision-making.

Central Mexico dominates the plastic packaging films market, accounting for approximately 45% of national consumption. This region benefits from concentrated manufacturing activity, proximity to major consumer markets, and established supply chain infrastructure. Mexico City metropolitan area serves as the primary hub for packaging converters and brand owners.

Northern border states represent the second-largest market segment, driven by maquiladora manufacturing and cross-border trade activities. States including Nuevo León, Chihuahua, and Tijuana demonstrate strong growth in industrial packaging applications, supported by automotive and electronics manufacturing clusters.

Western regions including Jalisco and surrounding states show robust growth in food packaging applications, supported by agricultural processing and beverage manufacturing. This region accounts for approximately 25% of market share and demonstrates particular strength in flexible food packaging solutions.

Southern and southeastern regions represent emerging opportunities with growing manufacturing presence and improving infrastructure. These areas show potential for market expansion as economic development initiatives attract investment and industrial activity.

Market leadership is distributed among several key players, each with distinct competitive advantages and market positioning strategies. The competitive environment reflects a mix of multinational corporations, regional players, and specialized niche providers.

By Material Type:

By Application:

By Technology:

Food packaging films demonstrate the strongest growth dynamics, driven by Mexico’s expanding food processing industry and changing consumer preferences. Barrier films within this category show particular promise, with 8.5% annual growth reflecting demand for extended shelf life and product protection. Fresh produce packaging represents an emerging opportunity as modern retail formats expand.

Industrial packaging applications benefit from Mexico’s manufacturing sector growth, particularly in automotive and electronics industries. Protective films used in manufacturing processes show consistent demand growth, while stretch films for logistics applications expand with e-commerce and distribution activity.

Pharmaceutical packaging represents the highest-value category, with stringent regulatory requirements supporting premium pricing. This segment requires specialized manufacturing capabilities and quality certifications, creating barriers to entry but attractive margins for qualified suppliers.

Sustainable packaging films emerge as a distinct category with growing market acceptance. Biodegradable films show 12% annual growth despite higher costs, reflecting consumer and regulatory pressure for environmental responsibility. This category attracts premium pricing and brand differentiation opportunities.

Manufacturers benefit from Mexico’s competitive cost structure, strategic location, and growing domestic market. Access to skilled labor, established supply chains, and favorable trade agreements create sustainable competitive advantages. Production efficiency improvements through technology adoption and scale economies enhance profitability and market position.

Brand owners gain access to innovative packaging solutions that enhance product differentiation and consumer appeal. Mexican suppliers offer flexibility, responsiveness, and cost competitiveness while maintaining quality standards. Supply chain proximity reduces logistics costs and lead times for North American markets.

Investors find attractive opportunities in a growing market with favorable demographics and economic trends. The sector offers diversification across multiple end-use applications and growth stages, from mature food packaging to emerging sustainable solutions. Market consolidation creates acquisition opportunities and economies of scale.

Technology providers benefit from increasing demand for advanced production equipment, automation systems, and sustainable technologies. Mexican manufacturers’ modernization efforts create substantial equipment and technology service opportunities.

Strengths:

Weaknesses:

Opportunities:

Threats:

Sustainability transformation represents the most significant trend reshaping the Mexican plastic packaging films market. Companies increasingly invest in circular economy solutions, including recycling infrastructure, biodegradable materials, and reduced packaging designs. This transformation affects product development, manufacturing processes, and customer relationships across the entire value chain.

Digital integration accelerates across manufacturing and supply chain operations, with companies adopting Industry 4.0 technologies for improved efficiency and quality control. Smart manufacturing systems enable real-time monitoring, predictive maintenance, and flexible production capabilities that enhance competitiveness.

Customization demand grows as brand owners seek differentiated packaging solutions for market segmentation and consumer engagement. Digital printing technologies enable shorter runs and variable designs, supporting personalization trends and regional market adaptation.

Supply chain localization accelerates as companies seek to reduce risks and improve responsiveness. This trend benefits Mexican manufacturers through nearshoring opportunities and supports domestic supply chain development. Vertical integration strategies become more common as companies seek greater control over quality and costs.

Capacity expansion projects continue across the Mexican plastic packaging films market, with major manufacturers investing in new production lines and facility upgrades. Recent announcements include significant investments in multilayer film capabilities and sustainable packaging technologies, reflecting confidence in long-term market growth.

Strategic partnerships between Mexican manufacturers and international technology providers accelerate innovation and capability development. These collaborations focus on advanced barrier technologies, sustainable materials, and smart packaging solutions that enhance market competitiveness.

Regulatory developments include new environmental standards and food safety requirements that drive industry modernization. MarkWide Research analysis indicates these regulations create both challenges and opportunities, favoring companies with advanced capabilities and compliance systems.

Merger and acquisition activity remains active as companies seek scale advantages and technology access. Recent transactions demonstrate industry consolidation trends and the strategic value of Mexican market positions for international players.

Investment priorities should focus on sustainable packaging technologies and advanced manufacturing capabilities that address evolving market demands. Companies investing in biodegradable films and recycling infrastructure position themselves advantageously for long-term growth and regulatory compliance.

Market positioning strategies should emphasize value-added services and technical expertise rather than competing solely on price. Customer partnership approaches that provide collaborative product development and supply chain integration create sustainable competitive advantages.

Geographic expansion within Mexico should target emerging regions with growing manufacturing activity and improving infrastructure. Export market development represents significant opportunities, particularly in Central and South American markets where Mexican producers enjoy competitive advantages.

Technology adoption should prioritize automation, quality systems, and digital integration that enhance operational efficiency and customer service capabilities. Companies that successfully integrate smart manufacturing technologies achieve superior performance and market positioning.

Long-term growth prospects for Mexico’s plastic packaging films market remain positive, supported by favorable demographic trends, economic development, and strategic advantages. MWR projections indicate sustained growth across multiple application segments, with particular strength in sustainable packaging solutions and high-performance films.

Technology evolution will continue driving market transformation, with smart packaging and sustainable materials becoming mainstream rather than niche applications. Companies that successfully navigate this transition through innovation and strategic positioning will capture disproportionate value creation opportunities.

Market structure changes are expected to continue, with further consolidation among manufacturers and increased vertical integration across the value chain. This evolution favors companies with strong financial resources, technological capabilities, and market positioning.

Sustainability requirements will intensify, with 85% of major brand owners expected to implement comprehensive sustainable packaging programs within five years. This trend creates both challenges for traditional materials and opportunities for innovative solutions that meet environmental and performance requirements.

The Mexico plastic packaging films market stands at a critical juncture, balancing traditional growth drivers with emerging sustainability imperatives and technological innovations. Market fundamentals remain strong, supported by Mexico’s strategic advantages, growing domestic consumption, and expanding manufacturing sector.

Competitive dynamics continue evolving as companies adapt to changing customer requirements, regulatory pressures, and technological possibilities. Success in this environment requires strategic focus on innovation, sustainability, and operational excellence while maintaining cost competitiveness and market responsiveness.

Future success will depend on companies’ ability to navigate the transition toward sustainable packaging solutions while capturing growth opportunities in emerging applications and export markets. The Mexican market’s unique position provides substantial advantages for companies that successfully execute comprehensive strategies addressing both current market needs and future requirements.

What is Plastic Packaging Films?

Plastic packaging films are thin layers of plastic used to wrap, protect, and preserve products. They are commonly used in various applications, including food packaging, medical supplies, and consumer goods.

What are the key players in the Mexico Plastic Packaging Films Market?

Key players in the Mexico Plastic Packaging Films Market include Amcor, Sealed Air Corporation, and Berry Global, among others. These companies are known for their innovative packaging solutions and extensive product offerings.

What are the main drivers of the Mexico Plastic Packaging Films Market?

The Mexico Plastic Packaging Films Market is driven by the growing demand for convenient packaging solutions, increased consumer preference for ready-to-eat meals, and the rise of e-commerce. Additionally, advancements in film technology are enhancing product performance.

What challenges does the Mexico Plastic Packaging Films Market face?

The Mexico Plastic Packaging Films Market faces challenges such as environmental concerns regarding plastic waste and stringent regulations on plastic usage. These factors are prompting companies to seek sustainable alternatives and improve recycling processes.

What opportunities exist in the Mexico Plastic Packaging Films Market?

Opportunities in the Mexico Plastic Packaging Films Market include the development of biodegradable films and the expansion of packaging solutions for the pharmaceutical industry. Additionally, increasing investments in sustainable packaging technologies are expected to drive growth.

What trends are shaping the Mexico Plastic Packaging Films Market?

Trends in the Mexico Plastic Packaging Films Market include the shift towards eco-friendly materials, the integration of smart packaging technologies, and the growing popularity of flexible packaging solutions. These trends are influencing consumer choices and industry practices.

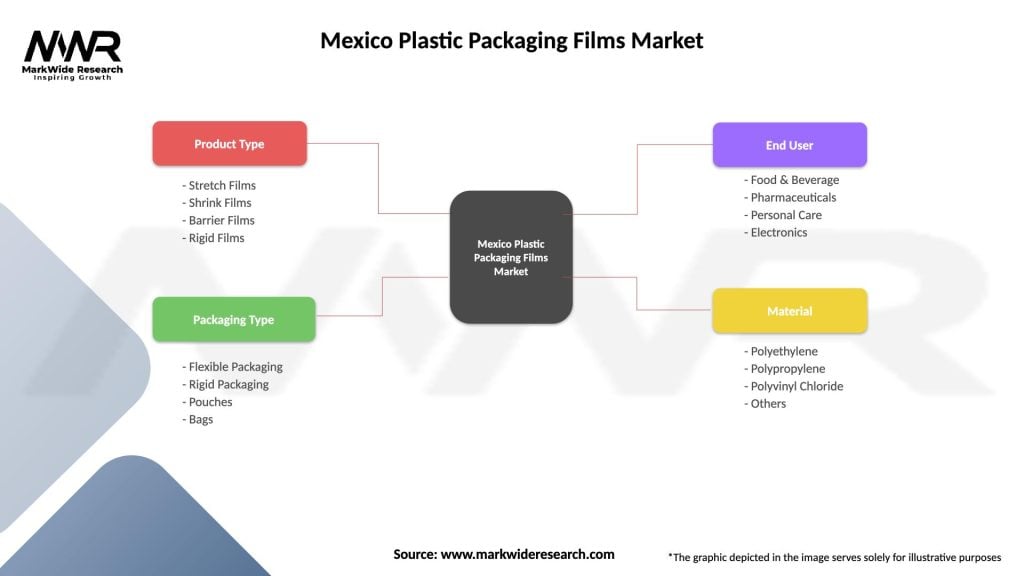

Mexico Plastic Packaging Films Market

| Segmentation Details | Description |

|---|---|

| Product Type | Stretch Films, Shrink Films, Barrier Films, Rigid Films |

| Packaging Type | Flexible Packaging, Rigid Packaging, Pouches, Bags |

| End User | Food & Beverage, Pharmaceuticals, Personal Care, Electronics |

| Material | Polyethylene, Polypropylene, Polyvinyl Chloride, Others |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Mexico Plastic Packaging Films Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.