444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Mexico diabetes drugs and devices market represents a rapidly expanding healthcare sector driven by the country’s significant diabetes prevalence and growing awareness of advanced treatment options. Mexico faces one of the highest diabetes rates globally, with approximately 12.8% of the adult population living with diabetes, creating substantial demand for innovative therapeutic solutions and monitoring devices. The market encompasses a comprehensive range of products including insulin formulations, oral antidiabetic medications, glucose monitoring systems, insulin delivery devices, and continuous glucose monitoring technologies.

Healthcare infrastructure improvements across Mexico have facilitated better access to diabetes management solutions, particularly in urban centers like Mexico City, Guadalajara, and Monterrey. The market benefits from increasing healthcare expenditure, government initiatives promoting diabetes awareness, and growing adoption of digital health technologies. Private healthcare providers and public institutions are collaborating to expand treatment accessibility, while pharmaceutical companies are investing in local manufacturing and distribution capabilities.

Market dynamics are influenced by demographic trends, including an aging population and rising obesity rates, which contribute to increased diabetes incidence. The market is experiencing robust growth at a CAGR of 8.2%, driven by technological advancements in glucose monitoring, insulin delivery systems, and personalized medicine approaches. Digital health integration and telemedicine adoption have accelerated, particularly following the COVID-19 pandemic, creating new opportunities for remote patient monitoring and medication adherence solutions.

The Mexico diabetes drugs and devices market refers to the comprehensive ecosystem of pharmaceutical products, medical devices, and digital health solutions designed to manage, monitor, and treat diabetes mellitus among the Mexican population. This market encompasses both Type 1 and Type 2 diabetes management solutions, including traditional medications, advanced biologics, glucose monitoring systems, insulin delivery devices, and emerging digital therapeutics platforms.

Market scope includes prescription medications such as insulin formulations, metformin, sulfonylureas, DPP-4 inhibitors, GLP-1 receptor agonists, and SGLT-2 inhibitors, alongside medical devices including blood glucose meters, continuous glucose monitors, insulin pens, insulin pumps, and smartphone-connected monitoring systems. The market also encompasses healthcare services, patient education programs, and digital platforms that support diabetes self-management and clinical decision-making.

Stakeholders in this market include pharmaceutical manufacturers, medical device companies, healthcare providers, government health agencies, insurance companies, patients, caregivers, and technology companies developing digital health solutions. The market operates within Mexico’s regulatory framework overseen by COFEPRIS (Federal Commission for Protection against Health Risks) and integrates with both public healthcare systems like IMSS and ISSSTE, as well as private healthcare providers.

Mexico’s diabetes drugs and devices market demonstrates exceptional growth potential driven by high disease prevalence, improving healthcare access, and increasing adoption of advanced treatment technologies. The market benefits from strong government support for diabetes prevention and management programs, coupled with growing private sector investment in innovative therapeutic solutions. Key growth drivers include rising diabetes awareness, expanding healthcare infrastructure, and increasing penetration of digital health technologies.

Market segmentation reveals significant opportunities across multiple product categories, with insulin products maintaining the largest market share at approximately 35% of total market volume. Glucose monitoring devices represent the fastest-growing segment, experiencing 12.4% annual growth due to increasing adoption of continuous glucose monitoring systems and smartphone-integrated devices. Oral antidiabetic medications continue to dominate prescription volumes, particularly metformin and combination therapies.

Competitive landscape features both international pharmaceutical giants and emerging local players, with companies focusing on product localization, affordability initiatives, and distribution network expansion. Market access improvements through government healthcare programs and private insurance coverage expansion are creating new opportunities for premium diabetes management solutions. The market is positioned for sustained growth, supported by demographic trends, technological innovation, and increasing healthcare investment.

Critical market insights reveal several transformative trends shaping Mexico’s diabetes drugs and devices landscape:

Primary market drivers propelling growth in Mexico’s diabetes drugs and devices sector stem from multiple interconnected factors creating sustained demand for innovative diabetes management solutions.

Demographic pressures represent the most significant driver, with Mexico’s diabetes prevalence continuing to rise due to lifestyle changes, urbanization, and dietary transitions. The country’s aging population, combined with increasing obesity rates exceeding 36% among adults, creates a growing patient base requiring long-term diabetes management. Genetic predisposition factors among the Mexican population further contribute to higher diabetes susceptibility rates.

Healthcare infrastructure development is expanding access to diabetes care across urban and rural areas. Government investments in healthcare facilities, specialist training programs, and medication distribution networks are improving treatment accessibility. Insurance coverage expansion through programs like Seguro Popular and INSABI is reducing financial barriers to diabetes medications and devices, enabling more patients to access advanced treatment options.

Technological advancement adoption is accelerating market growth through innovative glucose monitoring systems, smart insulin delivery devices, and digital health platforms. Smartphone penetration exceeding 80% in urban areas is facilitating mobile health application adoption, enabling better diabetes self-management and remote monitoring capabilities. Artificial intelligence integration in glucose prediction algorithms and personalized treatment recommendations is enhancing clinical outcomes and patient engagement.

Significant market restraints continue to challenge the expansion of Mexico’s diabetes drugs and devices market, despite overall positive growth trends and increasing healthcare investment.

Economic constraints represent the primary barrier to market expansion, particularly affecting middle and lower-income populations who struggle with medication affordability. Despite insurance coverage improvements, many advanced diabetes devices and newer medication formulations remain expensive, limiting accessibility for significant patient segments. Currency fluctuations affecting imported medical devices and pharmaceutical ingredients create pricing volatility that impacts both providers and patients.

Healthcare system limitations persist in rural and underserved areas, where specialist availability remains limited and healthcare infrastructure requires further development. Geographic disparities in healthcare access create uneven market penetration, with urban centers receiving disproportionate attention from pharmaceutical companies and device manufacturers. Supply chain challenges occasionally disrupt medication availability, particularly for specialized insulin formulations and advanced monitoring devices.

Regulatory complexities can slow the introduction of innovative diabetes management solutions, with COFEPRIS approval processes requiring comprehensive clinical data and safety documentation. Cultural barriers and health literacy limitations in some populations affect treatment adherence and proper device utilization, reducing the effectiveness of advanced diabetes management technologies. Healthcare provider training gaps in emerging technologies can limit the adoption of sophisticated glucose monitoring and insulin delivery systems.

Substantial market opportunities are emerging across Mexico’s diabetes drugs and devices landscape, driven by unmet medical needs, technological innovation, and evolving healthcare delivery models.

Digital health expansion presents significant opportunities for companies developing integrated diabetes management platforms combining glucose monitoring, medication tracking, and lifestyle coaching. Artificial intelligence applications in predictive glucose modeling and personalized treatment optimization offer potential for improved clinical outcomes and reduced healthcare costs. Telemedicine integration creates opportunities for remote diabetes specialist consultations and continuous patient monitoring services.

Biosimilar medication development offers opportunities to improve treatment affordability while maintaining clinical efficacy, particularly for insulin products and newer biologic medications. Local manufacturing initiatives supported by government incentives can reduce import dependencies and create cost-effective treatment options. Combination therapy innovations addressing multiple diabetes complications simultaneously present opportunities for comprehensive patient care solutions.

Rural market penetration represents an underserved opportunity, with potential for mobile health clinics, pharmacy partnerships, and community health worker programs to expand diabetes care access. Preventive care programs targeting pre-diabetic populations offer opportunities for early intervention and disease progression prevention. Pediatric diabetes management solutions addressing the growing incidence of Type 1 diabetes in children present specialized market opportunities requiring age-appropriate devices and educational programs.

Complex market dynamics shape the competitive landscape and growth trajectory of Mexico’s diabetes drugs and devices market, influenced by regulatory changes, technological advancement, and evolving patient needs.

Supply and demand dynamics are driven by increasing diabetes prevalence balanced against healthcare system capacity and affordability constraints. Demand growth consistently outpaces supply infrastructure development, particularly for specialized services like continuous glucose monitoring and insulin pump therapy. Price sensitivity among patients and healthcare providers creates pressure for cost-effective solutions while maintaining clinical efficacy standards.

Competitive dynamics feature intense rivalry between international pharmaceutical companies and emerging local manufacturers, with competition focusing on product affordability, distribution network strength, and clinical support services. Innovation cycles are accelerating, with companies investing heavily in next-generation glucose monitoring technologies, smart insulin delivery systems, and digital therapeutics platforms. Partnership strategies between pharmaceutical companies, technology firms, and healthcare providers are creating integrated care solutions.

Regulatory dynamics continue evolving as COFEPRIS adapts approval processes for digital health technologies and combination medical devices. Reimbursement dynamics are improving through expanded insurance coverage and government healthcare programs, though disparities remain across different patient populations. Market access dynamics vary significantly between urban and rural areas, creating opportunities for innovative distribution models and community-based care programs.

Comprehensive research methodology employed for analyzing Mexico’s diabetes drugs and devices market incorporates multiple data sources, analytical frameworks, and validation techniques to ensure accuracy and reliability of market insights.

Primary research activities included extensive interviews with healthcare providers, diabetes specialists, hospital administrators, pharmacy managers, and patient advocacy groups across major Mexican cities. Survey methodologies captured patient preferences, treatment adherence patterns, and device utilization rates among diverse demographic groups. Healthcare provider surveys assessed prescribing patterns, technology adoption rates, and barriers to implementing advanced diabetes management solutions.

Secondary research analysis incorporated data from government health agencies, pharmaceutical industry reports, medical device manufacturer publications, and academic research studies focusing on diabetes epidemiology in Mexico. Regulatory filing analysis provided insights into new product approvals, clinical trial activities, and market entry strategies. Financial analysis of publicly traded companies operating in the Mexican diabetes market revealed investment trends and strategic priorities.

Data validation processes included cross-referencing multiple sources, expert panel reviews, and statistical analysis to ensure data accuracy and eliminate potential biases. MarkWide Research analytical frameworks were applied to segment market data by product categories, geographic regions, and patient demographics. Forecasting models incorporated demographic trends, healthcare policy changes, and technology adoption curves to project future market development scenarios.

Regional market analysis reveals significant variations in diabetes drugs and devices adoption across Mexico’s diverse geographic and demographic landscape, with distinct patterns emerging in different states and metropolitan areas.

Central Mexico Region dominates market activity, with Mexico City and surrounding states accounting for approximately 42% of total market consumption. This region benefits from concentrated healthcare infrastructure, higher income levels, and greater access to specialized diabetes care services. Private healthcare penetration is highest in this region, supporting adoption of premium diabetes management technologies and newer medication formulations. Digital health adoption rates are most advanced, with smartphone-connected glucose monitoring devices achieving significant market penetration.

Northern Border States including Nuevo León, Chihuahua, and Baja California represent approximately 28% of market share, driven by industrial development, higher employment rates, and proximity to U.S. healthcare innovations. Cross-border healthcare activities influence treatment preferences and technology adoption patterns. Manufacturing presence of international pharmaceutical companies in this region supports local market development and employment opportunities.

Southern and Southeastern Regions present significant growth opportunities despite currently representing 18% of market activity. These areas face healthcare access challenges but benefit from government programs targeting underserved populations. Rural diabetes management initiatives are expanding through mobile health clinics and community health worker programs. Indigenous population considerations require culturally appropriate diabetes education and management approaches.

Competitive landscape analysis reveals a dynamic market structure featuring established international pharmaceutical companies, emerging local manufacturers, and innovative technology firms competing across multiple product categories and market segments.

Market competition intensifies around product affordability, clinical efficacy, and patient support services, with companies investing in local partnerships, healthcare provider education, and patient assistance programs to differentiate their offerings in the Mexican market.

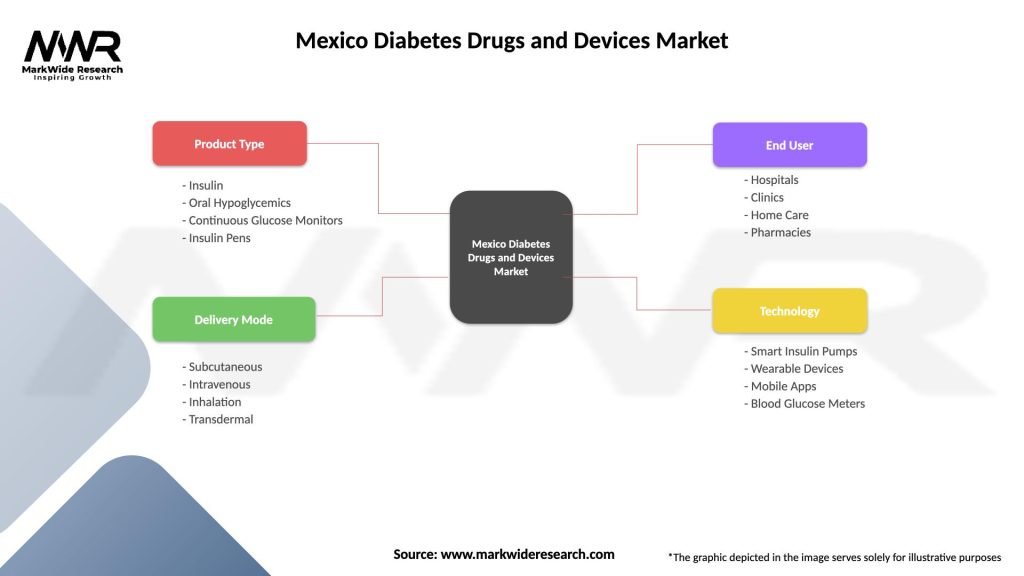

Market segmentation analysis provides detailed insights into product categories, patient demographics, and distribution channels that define Mexico’s diabetes drugs and devices market structure.

By Product Type:

By Diabetes Type:

By Distribution Channel:

Detailed category analysis reveals distinct growth patterns, competitive dynamics, and market opportunities across different product segments within Mexico’s diabetes drugs and devices market.

Insulin Products Category maintains market leadership through continuous innovation in formulation and delivery systems. Long-acting insulin analogs are gaining preference over traditional human insulin due to improved glycemic control and reduced hypoglycemia risk. Biosimilar insulin products are creating price competition while expanding access for cost-sensitive patients. Insulin pen systems dominate delivery preferences, with smart pens featuring dose tracking and smartphone connectivity gaining adoption among tech-savvy patients.

Oral Antidiabetic Medications represent the highest prescription volume category, with metformin remaining first-line therapy for Type 2 diabetes management. Combination therapies are increasingly prescribed to achieve glycemic targets while simplifying dosing regimens. SGLT-2 inhibitors are experiencing rapid growth due to cardiovascular and renal protection benefits beyond glucose control. DPP-4 inhibitors maintain steady market share through favorable safety profiles and minimal side effects.

Glucose Monitoring Devices category is experiencing technological transformation with continuous glucose monitoring systems challenging traditional fingerstick meters. Smartphone connectivity is becoming standard in new glucose meter launches, enabling data sharing with healthcare providers and family members. Flash glucose monitoring technology is gaining rapid adoption due to convenience and reduced testing discomfort. Test strip consumption remains high, creating recurring revenue opportunities for device manufacturers.

Industry participants and stakeholders in Mexico’s diabetes drugs and devices market realize significant benefits through participation in this growing healthcare sector, creating value for patients, providers, and investors.

Pharmaceutical Companies benefit from sustained demand growth driven by increasing diabetes prevalence and expanding healthcare coverage. Revenue stability is enhanced through chronic disease management requiring long-term medication adherence. Innovation opportunities in personalized medicine, digital therapeutics, and combination therapies create competitive advantages and premium pricing potential. Local manufacturing investments reduce import costs while qualifying for government incentives and improving supply chain reliability.

Medical Device Manufacturers capitalize on technological advancement adoption and growing patient preference for convenient, connected monitoring solutions. Recurring revenue models through consumable supplies like test strips and sensor replacements provide predictable income streams. Data analytics opportunities from connected devices create additional value propositions for healthcare providers and patients. Partnership opportunities with pharmaceutical companies enable integrated diabetes management solutions.

Healthcare Providers benefit from improved patient outcomes through access to advanced diabetes management technologies and comprehensive treatment options. Operational efficiency gains through digital health integration and remote monitoring capabilities reduce clinic visit requirements while maintaining care quality. Revenue diversification through diabetes education programs, device training services, and specialized care clinics creates additional income sources. Clinical decision support tools enhance treatment optimization and patient satisfaction scores.

Patients and Caregivers realize improved quality of life through better glucose control, reduced complications, and enhanced treatment convenience. Treatment accessibility improvements through expanded insurance coverage and government programs reduce financial burden. Technology integration enables better self-management capabilities and family involvement in diabetes care. Educational resources and support programs improve treatment adherence and clinical outcomes.

Comprehensive SWOT analysis evaluates the strategic position of Mexico’s diabetes drugs and devices market, identifying internal strengths and weaknesses alongside external opportunities and threats.

Strengths:

Weaknesses:

Opportunities:

Threats:

Emerging market trends are reshaping Mexico’s diabetes drugs and devices landscape, driven by technological innovation, changing patient preferences, and evolving healthcare delivery models.

Digital Health Integration represents the most significant trend, with connected glucose monitoring devices and smartphone applications becoming standard components of diabetes management. Artificial intelligence algorithms are being integrated into glucose prediction models, medication dosing recommendations, and lifestyle coaching platforms. Telemedicine adoption has accelerated dramatically, enabling remote diabetes specialist consultations and continuous patient monitoring services.

Personalized Medicine Advancement is gaining momentum through pharmacogenomic testing to optimize medication selection and dosing for individual patients. Continuous glucose monitoring data is being used to develop personalized insulin dosing algorithms and dietary recommendations. Biomarker research is advancing toward more precise diabetes subtype classification and targeted therapy selection.

Value-Based Care Models are emerging as healthcare providers and payers focus on clinical outcomes rather than treatment volume. Pay-for-performance contracts are being implemented for diabetes management programs, incentivizing improved glycemic control and reduced complications. Risk-sharing agreements between pharmaceutical companies and healthcare systems are becoming more common for expensive diabetes medications.

Preventive Care Emphasis is shifting focus toward pre-diabetes intervention programs and lifestyle modification initiatives. Community health worker programs are expanding to provide diabetes education and support in underserved areas. Workplace wellness programs targeting diabetes prevention and management are gaining adoption among large employers.

Recent industry developments highlight the dynamic nature of Mexico’s diabetes drugs and devices market, with significant advances in product innovation, regulatory approvals, and market access initiatives.

Regulatory Approvals have accelerated for innovative diabetes management technologies, with COFEPRIS streamlining approval processes for digital health applications and connected medical devices. Biosimilar insulin approvals are increasing market competition while improving treatment affordability for Mexican patients. Combination therapy approvals are expanding treatment options for complex diabetes management scenarios.

Technology Launches include next-generation continuous glucose monitoring systems with extended wear time and improved accuracy. Smart insulin pen systems with dose tracking and smartphone connectivity are entering the Mexican market through major pharmaceutical companies. Artificial intelligence platforms for glucose prediction and insulin dosing optimization are being piloted in major healthcare systems.

Partnership Agreements between international pharmaceutical companies and local distributors are expanding market reach and improving product accessibility. Healthcare provider partnerships are creating integrated diabetes care centers offering comprehensive services from diagnosis through ongoing management. Technology company collaborations are developing Mexico-specific mobile health applications and patient engagement platforms.

Investment Activities include significant funding for local pharmaceutical manufacturing facilities and diabetes device assembly operations. Research and development investments are focusing on Mexico-specific diabetes complications and treatment approaches. Digital health startups targeting the Mexican diabetes market are receiving increased venture capital funding and strategic partnerships.

Strategic recommendations for market participants in Mexico’s diabetes drugs and devices sector focus on addressing key challenges while capitalizing on emerging opportunities for sustainable growth and market leadership.

Market Access Strategy should prioritize affordability initiatives including patient assistance programs, tiered pricing models, and partnerships with government healthcare programs. Distribution network expansion into underserved rural areas through pharmacy partnerships and mobile health clinics can capture untapped market potential. Insurance coverage advocacy efforts should focus on demonstrating long-term cost-effectiveness of advanced diabetes management technologies.

Product Development Focus should emphasize culturally appropriate solutions considering Mexican dietary preferences, lifestyle patterns, and health literacy levels. Spanish-language digital platforms with intuitive interfaces can improve patient engagement and treatment adherence. Combination products addressing multiple diabetes complications simultaneously offer opportunities for differentiated market positioning.

Partnership Strategy recommendations include healthcare provider collaborations for integrated diabetes care delivery and clinical outcome improvement. Technology partnerships with Mexican software companies can accelerate digital health solution development and local market adaptation. Academic research collaborations can support clinical evidence generation and regulatory approval processes.

Investment Priorities should focus on local manufacturing capabilities to reduce import dependencies and improve supply chain resilience. Digital health infrastructure investments can support telemedicine expansion and remote patient monitoring services. Healthcare provider education programs can accelerate adoption of innovative diabetes management technologies and improve clinical outcomes.

Future market outlook for Mexico’s diabetes drugs and devices sector indicates sustained growth driven by demographic trends, technological advancement, and healthcare system evolution, with MarkWide Research projecting continued expansion across all major product categories.

Growth trajectory is expected to maintain momentum with projected CAGR of 8.5% over the next five years, supported by increasing diabetes prevalence, expanding healthcare coverage, and accelerating technology adoption. Digital health integration will become increasingly central to diabetes management, with connected devices and artificial intelligence platforms achieving mainstream adoption. Personalized medicine approaches will gain prominence through advanced biomarker research and pharmacogenomic applications.

Technology evolution will focus on non-invasive glucose monitoring solutions, automated insulin delivery systems, and comprehensive diabetes management platforms integrating multiple health parameters. Artificial intelligence applications will expand beyond glucose prediction to include complication risk assessment, medication optimization, and lifestyle intervention recommendations. Wearable device integration will create holistic health monitoring ecosystems supporting diabetes management within broader wellness frameworks.

Market structure changes will include increased local manufacturing presence by international companies seeking to improve cost competitiveness and supply chain reliability. Biosimilar competition will intensify, driving down medication costs while maintaining clinical efficacy standards. Digital health startups will play increasingly important roles in innovation and market disruption, particularly in patient engagement and care coordination solutions.

Healthcare delivery transformation will emphasize value-based care models focusing on clinical outcomes and long-term cost-effectiveness. Preventive care programs will expand significantly, targeting pre-diabetic populations and high-risk individuals through community-based interventions. Integrated care networks will become more prevalent, combining primary care, specialist services, and digital health platforms for comprehensive diabetes management.

Mexico’s diabetes drugs and devices market represents a compelling growth opportunity characterized by substantial unmet medical needs, expanding healthcare infrastructure, and accelerating technology adoption. The market benefits from strong demographic drivers, including high diabetes prevalence and an aging population, combined with improving healthcare access through government programs and insurance coverage expansion.

Market dynamics favor continued expansion across all major product categories, with particular strength in digital health solutions, continuous glucose monitoring systems, and personalized medicine approaches. Competitive landscape evolution is creating opportunities for both established pharmaceutical companies and innovative technology firms to capture market share through differentiated product offerings and strategic partnerships.

Strategic success factors include addressing affordability challenges, expanding rural market access, and developing culturally appropriate solutions for the Mexican population. Technology integration will be crucial for market leadership, with companies investing in connected devices, artificial intelligence platforms, and comprehensive diabetes management ecosystems positioned for sustained growth.

The future outlook remains highly positive, with sustained growth projected across all market segments driven by demographic trends, healthcare system improvements, and continued innovation in diabetes management technologies. Market participants who successfully navigate regulatory requirements, address accessibility challenges, and leverage digital health opportunities will be well-positioned to capitalize on Mexico’s expanding diabetes drugs and devices market.

What is Diabetes Drugs and Devices?

Diabetes Drugs and Devices refer to the medications and tools used to manage diabetes, including insulin, oral hypoglycemics, glucose meters, and insulin pumps. These products are essential for maintaining blood sugar levels and preventing complications associated with diabetes.

What are the key players in the Mexico Diabetes Drugs and Devices Market?

Key players in the Mexico Diabetes Drugs and Devices Market include Sanofi, Novo Nordisk, and Abbott Laboratories. These companies are known for their innovative products and significant market presence, among others.

What are the growth factors driving the Mexico Diabetes Drugs and Devices Market?

The Mexico Diabetes Drugs and Devices Market is driven by the increasing prevalence of diabetes, rising awareness about diabetes management, and advancements in technology. Additionally, the growing aging population contributes to the demand for effective diabetes care solutions.

What challenges does the Mexico Diabetes Drugs and Devices Market face?

The Mexico Diabetes Drugs and Devices Market faces challenges such as high costs of advanced diabetes management devices and limited access to healthcare in rural areas. Regulatory hurdles and the need for continuous innovation also pose significant challenges.

What opportunities exist in the Mexico Diabetes Drugs and Devices Market?

Opportunities in the Mexico Diabetes Drugs and Devices Market include the development of smart insulin delivery systems and the integration of telemedicine for diabetes management. There is also potential for growth in personalized medicine and patient education initiatives.

What trends are shaping the Mexico Diabetes Drugs and Devices Market?

Trends in the Mexico Diabetes Drugs and Devices Market include the increasing adoption of continuous glucose monitoring systems and the rise of digital health solutions. Additionally, there is a growing focus on preventive care and lifestyle management to support diabetes patients.

Mexico Diabetes Drugs and Devices Market

| Segmentation Details | Description |

|---|---|

| Product Type | Insulin, Oral Hypoglycemics, Continuous Glucose Monitors, Insulin Pens |

| Delivery Mode | Subcutaneous, Intravenous, Inhalation, Transdermal |

| End User | Hospitals, Clinics, Home Care, Pharmacies |

| Technology | Smart Insulin Pumps, Wearable Devices, Mobile Apps, Blood Glucose Meters |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Mexico Diabetes Drugs and Devices Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.