444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The medical devices and equipment logistics market represents a critical component of the global healthcare supply chain, encompassing the specialized transportation, storage, and distribution of medical equipment, devices, and supplies. This sophisticated logistics ecosystem ensures that life-saving medical technologies reach healthcare facilities, hospitals, and clinics efficiently and safely. The market has experienced unprecedented growth, driven by increasing healthcare demands, technological advancements, and the critical need for reliable medical supply chains demonstrated during global health emergencies.

Market dynamics indicate robust expansion with the sector growing at a CAGR of 8.2% as healthcare systems worldwide prioritize supply chain resilience. The integration of advanced technologies such as IoT sensors, blockchain tracking, and AI-powered inventory management has revolutionized how medical devices move through the supply chain. Temperature-controlled logistics represents approximately 35% of the total market share, reflecting the critical nature of maintaining product integrity for sensitive medical equipment and pharmaceuticals.

Regional distribution shows North America commanding 42% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions collectively account for 8% of the global market. This distribution reflects the concentration of major medical device manufacturers and advanced healthcare infrastructure in developed economies, while emerging markets demonstrate significant growth potential driven by healthcare infrastructure development and increasing medical device adoption rates.

The medical devices and equipment logistics market refers to the comprehensive ecosystem of specialized supply chain services designed to handle the unique requirements of medical products throughout their journey from manufacturers to end-users. This market encompasses warehousing, transportation, inventory management, regulatory compliance, and distribution services specifically tailored for medical devices, diagnostic equipment, surgical instruments, and related healthcare products.

Core components of this market include temperature-controlled storage facilities, specialized transportation vehicles equipped with monitoring systems, regulatory compliance management, inventory tracking technologies, and last-mile delivery services to healthcare facilities. The market also encompasses reverse logistics for medical device returns, recalls, and end-of-life product management, ensuring complete lifecycle support for medical equipment.

Specialized requirements distinguish this market from general logistics, including strict regulatory compliance with FDA, CE marking, and other international standards, maintenance of cold chain integrity for temperature-sensitive devices, sterile handling procedures, and comprehensive documentation and traceability systems. These unique characteristics create barriers to entry and demand specialized expertise from logistics service providers.

Market transformation in medical devices and equipment logistics reflects the evolving healthcare landscape, with increasing emphasis on supply chain visibility, regulatory compliance, and patient safety. The sector has witnessed significant consolidation among logistics providers, with major players investing heavily in specialized infrastructure and technology capabilities to serve the unique needs of medical device manufacturers and healthcare providers.

Technology adoption has accelerated dramatically, with 67% of logistics providers implementing IoT-based tracking systems and 54% adopting artificial intelligence for demand forecasting and inventory optimization. These technological advancements have resulted in improved delivery accuracy, reduced product damage, and enhanced regulatory compliance capabilities across the supply chain.

Regulatory landscape continues to evolve, with stricter requirements for product traceability, serialization, and supply chain security driving increased investment in compliance technologies and processes. The market has demonstrated remarkable resilience during global disruptions, with logistics providers adapting quickly to changing demand patterns and implementing robust contingency planning measures.

Future prospects remain highly positive, driven by aging populations, increasing chronic disease prevalence, technological innovation in medical devices, and growing emphasis on personalized medicine. The market is expected to benefit from continued healthcare infrastructure development in emerging economies and increasing adoption of digital health technologies requiring specialized logistics support.

Strategic insights reveal several critical factors shaping the medical devices and equipment logistics market landscape:

Primary growth drivers propelling the medical devices and equipment logistics market include the fundamental shift toward value-based healthcare delivery models, which emphasize cost-effectiveness and patient outcomes. Healthcare providers increasingly recognize that efficient medical device logistics directly impact patient care quality, operational efficiency, and cost management, driving demand for specialized logistics services.

Demographic trends represent a significant market driver, with global population aging creating increased demand for medical devices and equipment. The prevalence of chronic diseases continues to rise, requiring sophisticated medical technologies and creating sustained demand for reliable logistics services. Technological advancement in medical devices, including miniaturization, connectivity, and personalization, creates new logistics challenges and opportunities for specialized service providers.

Regulatory requirements serve as both drivers and challenges, with increasing emphasis on product traceability, serialization, and supply chain security creating demand for advanced logistics capabilities. Healthcare systems worldwide are implementing stricter quality standards and compliance requirements, necessitating investment in specialized logistics infrastructure and processes.

Globalization of medical device manufacturing and distribution creates complex supply chain requirements, driving demand for integrated logistics solutions that can manage international shipping, customs clearance, regulatory compliance, and local distribution across multiple markets simultaneously.

Significant challenges facing the medical devices and equipment logistics market include the high cost of specialized infrastructure and technology required to meet stringent regulatory and quality requirements. The initial investment in temperature-controlled facilities, monitoring systems, and compliance technologies creates barriers to entry for smaller logistics providers and increases operational costs across the industry.

Regulatory complexity presents ongoing challenges, with varying requirements across different countries and regions creating compliance burdens for logistics providers serving global markets. The need to maintain current knowledge of evolving regulations, implement necessary changes, and demonstrate compliance through comprehensive documentation requires significant resources and expertise.

Skilled workforce shortage affects the industry, with demand for professionals experienced in medical device logistics, regulatory compliance, and specialized handling procedures exceeding supply. Training and retaining qualified personnel requires substantial investment and creates operational challenges for logistics providers seeking to expand their capabilities.

Technology integration challenges arise from the need to connect diverse systems across multiple stakeholders in the supply chain, including manufacturers, logistics providers, healthcare facilities, and regulatory agencies. Achieving seamless data flow and system interoperability requires significant technical expertise and ongoing maintenance investment.

Emerging opportunities in the medical devices and equipment logistics market center on the rapid expansion of digital health technologies, telemedicine, and remote patient monitoring solutions. These innovative healthcare delivery models create new logistics requirements for direct-to-patient device distribution, home healthcare equipment management, and specialized handling of connected medical devices.

Geographic expansion presents substantial opportunities, particularly in emerging markets where healthcare infrastructure development and increasing medical device adoption create demand for specialized logistics services. Countries in Asia-Pacific, Latin America, and Africa represent significant growth potential as healthcare systems modernize and regulatory frameworks mature.

Technology innovation opportunities include the development of advanced tracking and monitoring systems, artificial intelligence applications for demand forecasting and inventory optimization, and blockchain solutions for enhanced supply chain transparency and security. These technological advancements can create competitive advantages and new revenue streams for logistics providers.

Sustainability initiatives offer opportunities for differentiation and cost reduction through eco-friendly packaging solutions, route optimization technologies, and carbon footprint reduction programs. Healthcare organizations increasingly prioritize environmental responsibility, creating market demand for sustainable logistics solutions.

Dynamic market forces shaping the medical devices and equipment logistics landscape reflect the complex interplay between technological advancement, regulatory evolution, and changing healthcare delivery models. The market demonstrates strong resilience and adaptability, with logistics providers continuously evolving their capabilities to meet emerging challenges and opportunities.

Competitive dynamics show increasing consolidation among logistics providers, with larger companies acquiring specialized capabilities and smaller firms to create comprehensive service offerings. This consolidation trend enables providers to achieve economies of scale, invest in advanced technologies, and offer integrated solutions across global markets.

Customer expectations continue to evolve, with healthcare providers demanding greater supply chain visibility, faster delivery times, and enhanced service quality. The shift toward value-based healthcare models creates pressure for logistics providers to demonstrate their contribution to patient outcomes and operational efficiency through measurable performance metrics.

Innovation cycles in the medical device industry create corresponding changes in logistics requirements, with new product categories, packaging formats, and distribution models requiring adaptive logistics solutions. Successful logistics providers maintain flexibility and innovation capabilities to support their customers’ evolving needs.

Comprehensive research approach employed in analyzing the medical devices and equipment logistics market combines primary and secondary research methodologies to ensure accuracy and reliability of market insights. The research framework incorporates quantitative analysis of market data, qualitative assessment of industry trends, and expert interviews with key stakeholders across the supply chain.

Primary research includes structured interviews with logistics service providers, medical device manufacturers, healthcare facility procurement managers, and regulatory experts. Survey methodologies capture quantitative data on market size, growth rates, technology adoption, and service preferences across different market segments and geographic regions.

Secondary research encompasses analysis of industry reports, regulatory filings, company financial statements, and trade association publications. This comprehensive data collection approach ensures broad market coverage and validates primary research findings through multiple independent sources.

Data validation processes include cross-referencing multiple sources, expert review panels, and statistical analysis to ensure research accuracy and reliability. The methodology incorporates regular updates to reflect market changes and emerging trends, maintaining current and relevant market intelligence for stakeholders.

North American market dominance reflects the region’s advanced healthcare infrastructure, large medical device manufacturing base, and sophisticated logistics capabilities. The United States leads regional growth with 78% market share within North America, driven by major medical device companies, extensive healthcare networks, and stringent regulatory requirements that demand specialized logistics expertise.

European market demonstrates strong growth across key countries including Germany, France, and the United Kingdom, with the region benefiting from harmonized regulatory frameworks and cross-border trade facilitation. The European market shows particular strength in specialized logistics for high-value medical equipment and innovative medical technologies, with efficiency improvements of 23% achieved through regional logistics optimization.

Asia-Pacific region represents the fastest-growing market segment, with countries like China, Japan, and India driving expansion through healthcare infrastructure development and increasing medical device adoption. The region shows remarkable growth potential with annual growth rates exceeding 12% in several key markets, supported by government healthcare initiatives and rising healthcare expenditure.

Emerging markets in Latin America, Middle East, and Africa demonstrate significant opportunities for market expansion, with improving healthcare infrastructure and increasing medical device penetration creating demand for specialized logistics services. These regions show adoption rates increasing by 18% annually as healthcare systems modernize and regulatory frameworks develop.

Market leadership in medical devices and equipment logistics is characterized by a mix of global logistics giants and specialized healthcare logistics providers, each bringing unique capabilities and market positioning strategies. The competitive landscape demonstrates ongoing consolidation and strategic partnership formation to create comprehensive service offerings.

Competitive strategies focus on technology investment, geographic expansion, specialized capability development, and strategic partnerships with medical device manufacturers and healthcare providers. Companies differentiate through service quality, regulatory expertise, technology innovation, and comprehensive solution offerings.

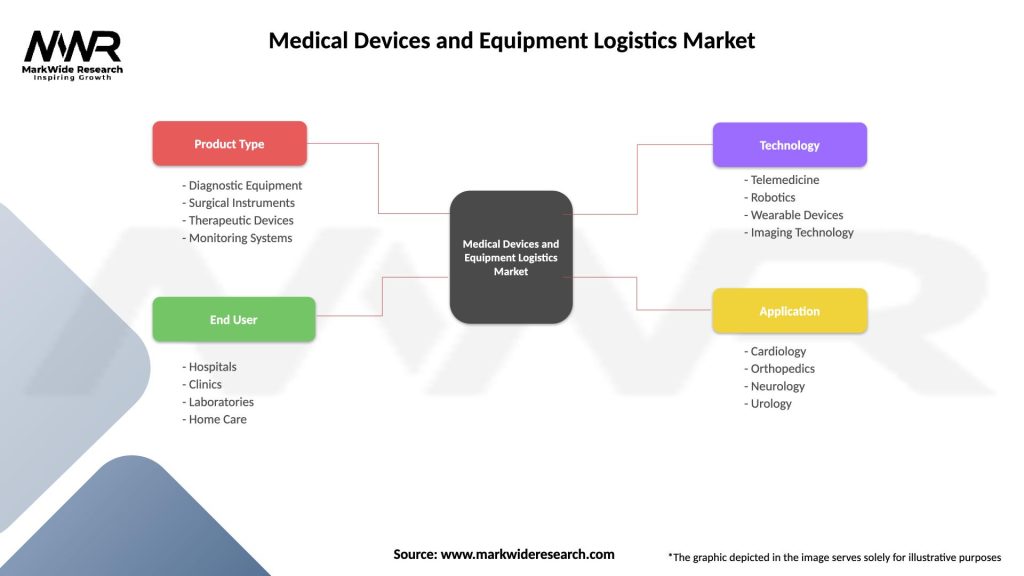

Market segmentation analysis reveals distinct categories based on device type, service type, end-user, and geographic region, each with unique characteristics and growth patterns. Understanding these segments enables targeted strategies and specialized service development.

By Device Type:

By Service Type:

Diagnostic equipment logistics represents the largest market segment, driven by increasing demand for advanced imaging systems, laboratory automation, and point-of-care diagnostic devices. This category requires specialized handling capabilities, technical expertise, and often includes installation and maintenance services as part of the logistics offering.

Surgical instrument logistics demands the highest levels of precision and sterile handling, with logistics providers investing in specialized facilities and processes to maintain product integrity. The category shows strong growth driven by minimally invasive surgical techniques and robotic surgery adoption, creating new logistics requirements for sophisticated surgical equipment.

Patient monitoring systems represent a rapidly growing category, fueled by the expansion of remote patient monitoring, telemedicine, and connected health technologies. These devices often require configuration, data connectivity setup, and ongoing technical support, creating opportunities for value-added logistics services.

Therapeutic device logistics encompasses a diverse range of treatment equipment with varying logistics requirements, from simple devices requiring standard handling to complex systems needing specialized transportation and installation services. This category benefits from increasing adoption of home healthcare and outpatient treatment models.

Implantable device logistics represents the highest-value segment, with strict regulatory requirements, comprehensive traceability needs, and often urgent delivery requirements. According to MarkWide Research analysis, this segment shows consistent growth driven by aging populations and advancing implant technologies.

Medical device manufacturers benefit from specialized logistics partnerships through reduced operational complexity, improved supply chain efficiency, and enhanced regulatory compliance capabilities. Outsourcing logistics functions allows manufacturers to focus on core competencies while ensuring reliable product distribution and customer service.

Healthcare providers gain significant advantages through improved inventory management, reduced carrying costs, and enhanced product availability. Specialized logistics services ensure timely delivery of critical medical equipment, reducing stockouts and improving patient care continuity while optimizing working capital requirements.

Logistics service providers benefit from the high-margin nature of specialized medical device logistics, long-term customer relationships, and opportunities for value-added services. The sector offers stable revenue streams and growth opportunities through geographic expansion and service diversification.

Patients and healthcare systems ultimately benefit from improved access to medical technologies, reduced healthcare costs through efficient supply chains, and enhanced safety through proper handling and traceability of medical devices. Efficient logistics contribute to better patient outcomes and healthcare system sustainability.

Regulatory agencies benefit from improved supply chain transparency, enhanced traceability capabilities, and better compliance monitoring through advanced logistics technologies and processes. Specialized logistics providers serve as partners in maintaining product safety and regulatory compliance.

Strengths:

Weaknesses:

Opportunities:

Threats:

Digital transformation represents the most significant trend reshaping the medical devices and equipment logistics market, with companies investing heavily in IoT sensors, artificial intelligence, and blockchain technologies to enhance supply chain visibility and efficiency. These digital solutions enable real-time tracking, predictive analytics, and automated decision-making throughout the logistics process.

Sustainability initiatives are gaining prominence as healthcare organizations prioritize environmental responsibility and cost reduction. Logistics providers are implementing eco-friendly packaging solutions, optimizing transportation routes to reduce carbon emissions, and developing circular economy approaches to medical device lifecycle management.

Direct-to-patient logistics emerges as a growing trend driven by home healthcare expansion, telemedicine adoption, and patient preference for convenient care delivery. This trend requires new logistics capabilities including residential delivery, patient education, and device setup services, creating opportunities for specialized service providers.

Automation and robotics adoption accelerates across medical device logistics operations, with automated storage and retrieval systems, robotic picking solutions, and autonomous delivery vehicles improving efficiency and reducing human error. These technologies particularly benefit high-volume, repetitive logistics processes while maintaining the precision required for medical device handling.

Collaborative logistics models gain traction as companies seek to optimize costs and improve service levels through shared resources, joint distribution networks, and integrated supply chain solutions. These collaborative approaches enable smaller companies to access sophisticated logistics capabilities while reducing overall industry costs.

Strategic acquisitions continue to reshape the competitive landscape, with major logistics companies acquiring specialized healthcare logistics providers to expand their capabilities and market presence. These acquisitions enable rapid capability development and geographic expansion while providing acquired companies with resources for technology investment and infrastructure development.

Technology partnerships between logistics providers and technology companies accelerate innovation in medical device logistics, with collaborations focusing on IoT solutions, artificial intelligence applications, and blockchain implementations. These partnerships combine logistics expertise with technological innovation to create advanced supply chain solutions.

Regulatory developments including updated serialization requirements, enhanced traceability standards, and new safety regulations drive industry adaptation and investment in compliance capabilities. MWR research indicates that regulatory compliance investments have increased by 31% over the past two years as companies adapt to evolving requirements.

Infrastructure investments by major logistics providers include new distribution centers, specialized storage facilities, and advanced transportation fleets designed specifically for medical device logistics. These investments demonstrate long-term commitment to the healthcare logistics market and enable improved service capabilities.

Sustainability initiatives gain momentum with companies implementing carbon reduction programs, sustainable packaging solutions, and circular economy approaches to medical device logistics. These initiatives respond to customer demands for environmental responsibility while often providing cost benefits through operational efficiency improvements.

Strategic recommendations for medical devices and equipment logistics market participants emphasize the critical importance of technology investment, regulatory compliance excellence, and customer relationship development. Companies should prioritize digital transformation initiatives that enhance supply chain visibility, improve operational efficiency, and enable data-driven decision making.

Technology adoption should focus on integrated solutions that provide end-to-end supply chain visibility, predictive analytics capabilities, and automated compliance monitoring. Companies should evaluate IoT sensors, artificial intelligence platforms, and blockchain solutions based on their ability to solve specific operational challenges and create competitive advantages.

Geographic expansion strategies should target emerging markets with growing healthcare infrastructure and increasing medical device adoption, while maintaining service excellence in established markets. Companies should consider strategic partnerships or acquisitions to accelerate market entry and capability development in new regions.

Service diversification opportunities include value-added services such as device installation, technical support, training services, and lifecycle management solutions. These services create additional revenue streams while strengthening customer relationships and increasing switching costs.

Sustainability integration should become a core component of business strategy, with companies developing comprehensive environmental programs that reduce costs while meeting customer expectations for responsible business practices. This includes packaging optimization, transportation efficiency, and end-of-life device management solutions.

Long-term prospects for the medical devices and equipment logistics market remain highly positive, driven by fundamental demographic trends, technological advancement, and evolving healthcare delivery models. The market is expected to benefit from continued aging of global populations, increasing prevalence of chronic diseases, and growing adoption of advanced medical technologies requiring specialized logistics support.

Technology evolution will continue to transform the industry, with artificial intelligence, machine learning, and advanced analytics becoming standard capabilities for leading logistics providers. These technologies will enable predictive maintenance, demand forecasting, and automated decision-making that improve efficiency and reduce costs throughout the supply chain.

Market consolidation is expected to continue as companies seek scale advantages, technology capabilities, and geographic coverage through strategic acquisitions and partnerships. This consolidation will create larger, more capable logistics providers while potentially reducing competition in some market segments.

Regulatory evolution will drive continued investment in compliance capabilities, with increasing emphasis on supply chain security, product traceability, and data protection. Companies that excel in regulatory compliance will gain competitive advantages and customer trust in an increasingly complex regulatory environment.

Emerging opportunities in personalized medicine, gene therapy, and advanced diagnostics will create new logistics requirements and market segments. According to MarkWide Research projections, these emerging segments could represent 15% of total market growth over the next five years, offering significant opportunities for logistics providers that develop specialized capabilities early.

The medical devices and equipment logistics market stands at a pivotal point in its evolution, characterized by robust growth prospects, technological transformation, and increasing strategic importance to healthcare delivery systems worldwide. The market has demonstrated remarkable resilience and adaptability, successfully navigating global challenges while continuing to innovate and expand its capabilities.

Key success factors for market participants include technology leadership, regulatory compliance excellence, operational efficiency, and strong customer relationships. Companies that invest in digital transformation, maintain high service quality standards, and develop specialized capabilities will be best positioned to capitalize on growth opportunities and maintain competitive advantages.

Future growth will be driven by demographic trends, healthcare infrastructure development, and continued innovation in medical technologies. The market’s critical role in healthcare delivery ensures sustained demand for specialized logistics services, while emerging opportunities in digital health, personalized medicine, and global market expansion provide additional growth vectors.

The medical devices and equipment logistics market represents a dynamic and essential component of the global healthcare ecosystem, with strong fundamentals and promising prospects for continued expansion and innovation in the years ahead.

What is Medical Devices and Equipment Logistics?

Medical Devices and Equipment Logistics refers to the processes involved in the transportation, storage, and distribution of medical devices and equipment. This includes managing supply chains, ensuring compliance with regulations, and maintaining the integrity of products throughout their lifecycle.

What are the key players in the Medical Devices and Equipment Logistics Market?

Key players in the Medical Devices and Equipment Logistics Market include companies like Cardinal Health, Medtronic, and Thermo Fisher Scientific, which provide comprehensive logistics solutions tailored for the healthcare sector, among others.

What are the main drivers of the Medical Devices and Equipment Logistics Market?

The main drivers of the Medical Devices and Equipment Logistics Market include the increasing demand for advanced medical technologies, the growth of the healthcare sector, and the rising need for efficient supply chain management to ensure timely delivery of critical medical supplies.

What challenges does the Medical Devices and Equipment Logistics Market face?

Challenges in the Medical Devices and Equipment Logistics Market include stringent regulatory requirements, the complexity of managing diverse product types, and the need for temperature-controlled logistics for sensitive medical products.

What opportunities exist in the Medical Devices and Equipment Logistics Market?

Opportunities in the Medical Devices and Equipment Logistics Market include the adoption of advanced technologies like IoT and AI for better tracking and management, as well as the expansion of e-commerce in healthcare, which requires efficient logistics solutions.

What trends are shaping the Medical Devices and Equipment Logistics Market?

Trends shaping the Medical Devices and Equipment Logistics Market include the increasing focus on sustainability in logistics practices, the rise of telemedicine requiring rapid delivery of devices, and the integration of automation in supply chain processes.

Medical Devices and Equipment Logistics Market

| Segmentation Details | Description |

|---|---|

| Product Type | Diagnostic Equipment, Surgical Instruments, Therapeutic Devices, Monitoring Systems |

| End User | Hospitals, Clinics, Laboratories, Home Care |

| Technology | Telemedicine, Robotics, Wearable Devices, Imaging Technology |

| Application | Cardiology, Orthopedics, Neurology, Urology |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Medical Devices and Equipment Logistics Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

North America

o US

o Canada

o Mexico

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA