444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

Market Overview

The mechanical ventilators market is experiencing significant growth due to the increasing prevalence of respiratory diseases and the rising demand for advanced healthcare facilities. Mechanical ventilators are devices used to provide respiratory support to patients who are unable to breathe on their own. These devices deliver a controlled amount of air or oxygen into the patient’s lungs, ensuring proper ventilation and oxygenation.

Meaning

Mechanical ventilators, also known as respirators or breathing machines, are critical medical devices that support patients with compromised respiratory function. They are commonly used in intensive care units (ICUs), emergency departments, and during surgical procedures. These devices play a vital role in assisting patients with respiratory failure or insufficiency, enabling them to receive the necessary oxygen and maintain proper lung function.

Executive Summary

The global mechanical ventilators market is witnessing steady growth, driven by factors such as the increasing geriatric population, the rising prevalence of chronic respiratory diseases, and advancements in technology. The market is highly competitive, with several key players offering innovative ventilator systems. The COVID-19 pandemic has further highlighted the importance of mechanical ventilators in managing severe respiratory complications.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Market Drivers

Market Restraints

Market Opportunities

Market Dynamics

The mechanical ventilators market is dynamic and influenced by various factors such as technological advancements, regulatory landscape, and the impact of the COVID-19 pandemic. Manufacturers are constantly innovating to meet the evolving needs of healthcare providers and improve patient outcomes. The market is highly competitive, with key players focusing on strategic collaborations, product launches, and mergers and acquisitions to strengthen their market position.

Regional Analysis

The mechanical ventilators market is segmented into several regions, including North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa. North America dominates the market, driven by the presence of well-established healthcare infrastructure, high healthcare expenditure, and a large patient pool with respiratory disorders. Europe follows closely, owing to the increasing prevalence of chronic respiratory diseases and favorable reimbursement policies. Asia-Pacific is expected to witness significant growth due to improving healthcare infrastructure, rising awareness, and a growing geriatric population.

Competitive Landscape

Leading Companies in Mechanical Ventilators Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Segmentation

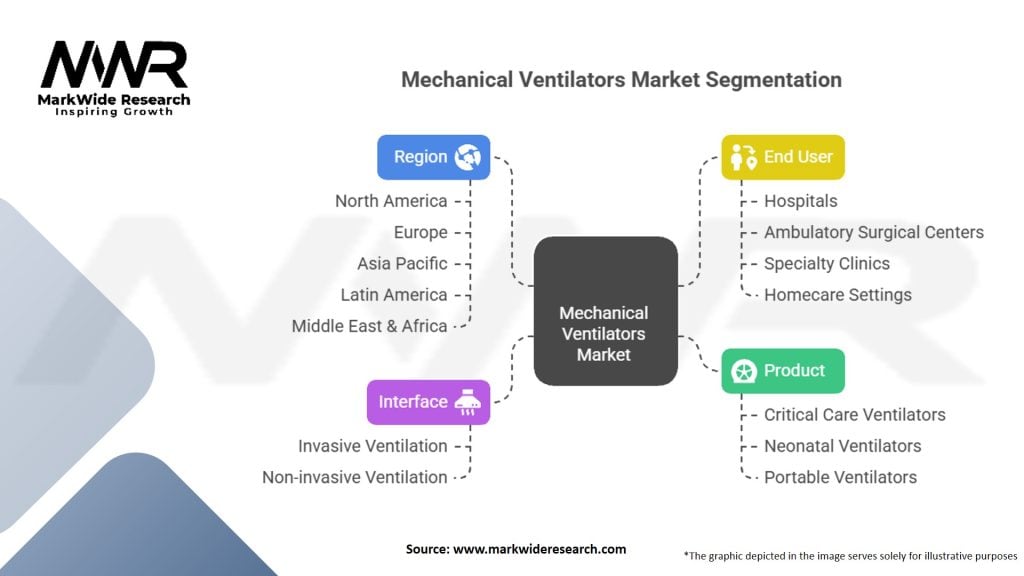

The mechanical ventilators market can be segmented based on product type, interface, end-user, and geography. By product type, the market is divided into intensive care ventilators, portable ventilators, and neonatal ventilators. The interface segment includes invasive and non-invasive ventilators. Based on end-user, the market can be categorized into hospitals, ambulatory surgical centers, and homecare settings. Geographically, the market is analyzed across North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

Category-wise Insights

Key Benefits for Industry Participants and Stakeholders

SWOT Analysis

Strengths:

Weaknesses:

Opportunities:

Threats:

Market Key Trends

Covid-19 Impact

The COVID-19 pandemic has had a profound impact on the mechanical ventilators market. The sudden surge in severe respiratory complications among COVID-19 patients created an unprecedented demand for ventilators worldwide. Governments and healthcare organizations rapidly increased their ventilator capacities to manage the influx of critically ill patients. This surge in demand led to supply chain disruptions, shortages of essential components, and increased production efforts by manufacturers. The pandemic also highlighted the need for portable and easy-to-use ventilators for use in field hospitals, ambulances, and homecare settings.

Key Industry Developments

Analyst Suggestions

Future Outlook

The future of the mechanical ventilators market looks promising, with sustained growth expected in the coming years. The increasing prevalence of respiratory diseases, technological advancements, and the need for advanced healthcare infrastructure will drive market expansion. Manufacturers will continue to invest in research and development to introduce innovative features and improve patient outcomes. The shift towards homecare settings and the adoption of remote monitoring capabilities will further shape the market landscape.

Conclusion

The mechanical ventilators market is witnessing significant growth driven by factors such as the rising prevalence of respiratory diseases, technological advancements, and increasing investments in healthcare infrastructure. Despite challenges such as high costs and regulatory requirements, the market offers ample opportunities for industry participants to innovate, expand their market presence, and improve patient outcomes. Collaboration, technological innovation, and a focus on emerging markets will be key strategies for success in the evolving mechanical ventilators market.

What is Mechanical Ventilators?

Mechanical ventilators are medical devices that provide mechanical assistance to patients who are unable to breathe adequately on their own. They are commonly used in critical care settings, such as intensive care units, to support patients with respiratory failure or during surgery.

What are the key companies in the Mechanical Ventilators Market?

Key companies in the Mechanical Ventilators Market include Philips Healthcare, Medtronic, and ResMed, which are known for their innovative ventilator technologies and solutions. These companies focus on enhancing patient care and improving ventilation efficiency, among others.

What are the drivers of growth in the Mechanical Ventilators Market?

The growth of the Mechanical Ventilators Market is driven by factors such as the increasing prevalence of respiratory diseases, the rising number of surgical procedures, and advancements in ventilator technology. Additionally, the growing demand for home care ventilators is contributing to market expansion.

What challenges does the Mechanical Ventilators Market face?

The Mechanical Ventilators Market faces challenges such as high costs associated with advanced ventilator systems and the need for skilled personnel to operate these devices. Furthermore, regulatory hurdles and the potential for device shortages during health crises can impact market stability.

What opportunities exist in the Mechanical Ventilators Market?

Opportunities in the Mechanical Ventilators Market include the development of portable and more efficient ventilators, as well as the integration of telemedicine solutions for remote monitoring. The increasing focus on home healthcare presents additional avenues for growth.

What trends are shaping the Mechanical Ventilators Market?

Trends in the Mechanical Ventilators Market include the shift towards smart ventilators equipped with AI and machine learning capabilities, enhancing patient monitoring and care. Additionally, there is a growing emphasis on sustainability and eco-friendly manufacturing practices in the production of these devices.

Mechanical Ventilators Market

| Segmentation Details | Description |

|---|---|

| Product | Critical Care Ventilators, Neonatal Ventilators, Portable Ventilators |

| Interface | Invasive Ventilation, Non-invasive Ventilation |

| End User | Hospitals, Ambulatory Surgical Centers, Specialty Clinics, Homecare Settings |

| Region | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading Companies in Mechanical Ventilators Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

North America

o US

o Canada

o Mexico

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA