444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The MEA Sodium-dependent Glucose Co-transporter 2 Inhibitors market represents a rapidly evolving pharmaceutical landscape across the Middle East and Africa region. This therapeutic segment has witnessed remarkable growth momentum, driven by increasing diabetes prevalence and enhanced healthcare infrastructure development. SGLT2 inhibitors have emerged as a cornerstone treatment option for type 2 diabetes management, offering unique mechanisms of action that complement traditional therapeutic approaches.

Regional dynamics indicate substantial market expansion potential, with healthcare systems increasingly recognizing the clinical benefits of SGLT2 inhibitor therapy. The market demonstrates robust growth trajectories, with adoption rates accelerating at approximately 12.5% annually across key MEA territories. Healthcare providers are witnessing improved patient outcomes through enhanced glycemic control and cardiovascular protection benefits.

Market penetration varies significantly across different MEA countries, with Gulf Cooperation Council nations leading adoption rates while African markets show emerging growth patterns. The therapeutic landscape encompasses multiple drug classes within the SGLT2 inhibitor category, including empagliflozin, dapagliflozin, and canagliflozin formulations. Clinical evidence supporting cardiovascular and renal protective effects has accelerated market acceptance among healthcare professionals and patients alike.

The MEA Sodium-dependent Glucose Co-transporter 2 Inhibitors market refers to the comprehensive pharmaceutical sector encompassing the development, manufacturing, distribution, and clinical application of SGLT2 inhibitor medications across Middle Eastern and African healthcare systems. These innovative therapeutic agents function by blocking glucose reabsorption in the kidneys, promoting glucose excretion through urine and providing glycemic control for diabetes patients.

SGLT2 inhibitors represent a distinct class of antidiabetic medications that offer unique physiological benefits beyond glucose management. The market encompasses various formulations, combination therapies, and delivery mechanisms designed to optimize patient compliance and therapeutic outcomes. Healthcare stakeholders recognize these medications as valuable tools for comprehensive diabetes management strategies.

Regional market dynamics reflect diverse healthcare infrastructure capabilities, regulatory frameworks, and patient access considerations across MEA territories. The market includes branded medications, generic alternatives, and combination therapies that integrate SGLT2 inhibitors with other antidiabetic agents for enhanced therapeutic efficacy.

Strategic market analysis reveals significant growth opportunities within the MEA SGLT2 inhibitors landscape, driven by increasing diabetes prevalence and evolving treatment paradigms. The market demonstrates strong fundamentals with expanding patient populations and enhanced healthcare access initiatives across the region. Key therapeutic advantages including weight management benefits and cardiovascular protection have accelerated clinical adoption rates.

Market segmentation indicates diverse opportunities across different drug formulations, with empagliflozin and dapagliflozin leading market share positions. Regional variations in healthcare infrastructure and regulatory approval processes create distinct market dynamics across MEA countries. Healthcare investment in diabetes management programs has increased substantially, with approximately 18% growth in specialized diabetes care facilities.

Competitive landscape features established pharmaceutical companies alongside emerging regional players, creating dynamic market conditions. The market benefits from increasing healthcare awareness campaigns and professional education initiatives that promote SGLT2 inhibitor therapy adoption. Patient access programs and insurance coverage expansion have improved medication accessibility across diverse socioeconomic segments.

Clinical adoption patterns reveal accelerating SGLT2 inhibitor utilization across MEA healthcare systems, with endocrinologists and primary care physicians increasingly prescribing these medications as first-line or combination therapies. The market demonstrates strong growth fundamentals supported by robust clinical evidence and expanding therapeutic indications beyond diabetes management.

Diabetes prevalence escalation represents the primary market driver, with MEA regions experiencing substantial increases in type 2 diabetes incidence rates. Urbanization trends and lifestyle modifications contribute to growing patient populations requiring advanced therapeutic interventions. Healthcare systems are responding with enhanced diabetes management programs that prioritize innovative treatment approaches.

Clinical evidence expansion continues to drive market growth as new studies demonstrate SGLT2 inhibitor benefits in cardiovascular protection and chronic kidney disease management. These expanded therapeutic indications broaden the addressable patient population beyond traditional diabetes management. Medical professionals increasingly recognize the multifaceted benefits of SGLT2 inhibitor therapy in comprehensive patient care strategies.

Healthcare infrastructure development across MEA countries facilitates improved medication access and specialized diabetes care services. Government initiatives promoting diabetes awareness and prevention programs create favorable market conditions for SGLT2 inhibitor adoption. Insurance coverage expansion and patient assistance programs enhance medication affordability and accessibility across diverse patient populations.

Pharmaceutical innovation drives market advancement through new formulations, combination therapies, and improved delivery mechanisms. Research and development investments focus on optimizing therapeutic efficacy while minimizing adverse effects. Regulatory support for expedited approval processes encourages pharmaceutical companies to introduce innovative SGLT2 inhibitor products in MEA markets.

Economic constraints present significant challenges for market expansion, particularly in developing African countries where healthcare budgets remain limited. High medication costs relative to average income levels restrict patient access to SGLT2 inhibitor therapy. Healthcare financing limitations impact both public and private sector adoption of these advanced therapeutic options.

Healthcare infrastructure gaps in certain MEA regions limit specialized diabetes care availability and SGLT2 inhibitor prescription capabilities. Rural areas often lack adequate endocrinology services and diabetes management programs. Medical professional training requirements for optimal SGLT2 inhibitor utilization may exceed current educational infrastructure capabilities in some territories.

Regulatory complexities across different MEA countries create market entry barriers and approval delays for pharmaceutical companies. Varying regulatory standards and documentation requirements increase operational costs and market access timelines. Import restrictions and local manufacturing requirements may limit product availability in certain markets.

Patient awareness limitations regarding SGLT2 inhibitor benefits and appropriate usage may restrict market adoption rates. Cultural factors and traditional medicine preferences can influence patient acceptance of modern pharmaceutical interventions. Healthcare provider education needs regarding optimal SGLT2 inhibitor prescribing practices require ongoing investment and support.

Emerging market expansion presents substantial growth opportunities as MEA countries develop healthcare infrastructure and increase diabetes care investments. Untapped patient populations in sub-Saharan Africa represent significant market potential for SGLT2 inhibitor therapy. Healthcare partnerships between international pharmaceutical companies and local distributors can accelerate market penetration.

Combination therapy development offers innovative treatment approaches that integrate SGLT2 inhibitors with complementary antidiabetic medications. Fixed-dose combinations can improve patient compliance while providing comprehensive glycemic management. Pharmaceutical innovation in delivery mechanisms and formulation optimization creates competitive advantages and market differentiation opportunities.

Digital health integration enables enhanced patient monitoring and medication management through connected healthcare technologies. Telemedicine platforms can expand SGLT2 inhibitor therapy access to remote and underserved populations. Healthcare digitization initiatives across MEA countries create favorable conditions for innovative diabetes management solutions.

Generic market development provides cost-effective alternatives that can expand patient access to SGLT2 inhibitor therapy. Local manufacturing capabilities in certain MEA countries offer opportunities for reduced medication costs and improved supply chain efficiency. Market competition through generic alternatives can stimulate overall market growth and accessibility improvements.

Supply chain evolution reflects increasing pharmaceutical distribution capabilities across MEA regions, with improved cold chain management and logistics infrastructure supporting SGLT2 inhibitor availability. Regional distribution networks are expanding to reach previously underserved markets. Pharmaceutical partnerships between international manufacturers and local distributors enhance market reach and operational efficiency.

Competitive dynamics intensify as multiple pharmaceutical companies introduce SGLT2 inhibitor products across different MEA markets. Price competition and value-based healthcare initiatives influence market positioning strategies. Market differentiation focuses on clinical efficacy, safety profiles, and patient support programs that enhance therapeutic outcomes.

Regulatory harmonization efforts across MEA countries facilitate streamlined approval processes and reduced market entry barriers. Collaborative regulatory frameworks enable faster access to innovative SGLT2 inhibitor therapies. Quality standards alignment ensures consistent product safety and efficacy across different regional markets.

Healthcare policy evolution supports diabetes management initiatives and SGLT2 inhibitor therapy integration into national healthcare programs. Government investments in diabetes prevention and treatment programs create favorable market conditions. Public-private partnerships enhance healthcare delivery capabilities and medication accessibility across diverse patient populations.

Comprehensive market analysis employs multiple research methodologies to ensure accurate and reliable insights into the MEA SGLT2 inhibitors market landscape. Primary research initiatives include extensive interviews with healthcare professionals, pharmaceutical industry executives, and regulatory authorities across key MEA countries. Data collection encompasses both quantitative and qualitative research approaches to capture market dynamics comprehensively.

Secondary research incorporates analysis of published clinical studies, regulatory filings, pharmaceutical company reports, and healthcare industry publications. Market data validation occurs through cross-referencing multiple authoritative sources and expert consultations. Regional analysis considers country-specific healthcare systems, regulatory environments, and market conditions that influence SGLT2 inhibitor adoption patterns.

Statistical modeling techniques enable accurate market trend analysis and growth projections based on historical data and emerging market indicators. Forecasting methodologies account for regional variations and country-specific factors that impact market development. Expert validation ensures research findings align with industry knowledge and practical market experiences.

Market segmentation analysis examines different therapeutic categories, patient demographics, and regional markets to provide detailed insights into growth opportunities and market dynamics. Research methodology incorporates feedback from healthcare stakeholders to ensure practical relevance and actionable insights for market participants.

Gulf Cooperation Council countries demonstrate the highest SGLT2 inhibitor adoption rates within the MEA region, with approximately 35% market share driven by advanced healthcare infrastructure and higher per capita healthcare spending. The UAE and Saudi Arabia lead regional market development through comprehensive diabetes management programs and specialized endocrinology services. Healthcare investments in these countries support innovative therapeutic approaches and patient access initiatives.

North African markets show emerging growth potential with increasing healthcare infrastructure development and diabetes awareness programs. Egypt and Morocco represent key growth markets with expanding healthcare systems and growing middle-class populations. Market penetration in these countries benefits from government healthcare initiatives and international pharmaceutical company investments.

Sub-Saharan African markets present significant long-term opportunities despite current infrastructure limitations and economic constraints. South Africa leads regional adoption with approximately 22% market share within the African continent, supported by established healthcare systems and pharmaceutical distribution networks. Healthcare development initiatives across the region create favorable conditions for future market expansion.

Regional variations in regulatory approval processes and healthcare policies influence market entry strategies and product availability timelines. Countries with streamlined regulatory frameworks demonstrate faster SGLT2 inhibitor market development. Cross-border collaboration initiatives enhance regional market integration and pharmaceutical supply chain efficiency.

Market leadership within the MEA SGLT2 inhibitors sector reflects a competitive environment featuring established international pharmaceutical companies alongside emerging regional players. The competitive landscape demonstrates dynamic positioning strategies focused on clinical differentiation and market access optimization.

Competitive strategies emphasize clinical evidence generation, healthcare professional education, and patient access programs that demonstrate value beyond traditional pharmaceutical marketing approaches. Companies invest in real-world evidence studies and health economic research to support market positioning and reimbursement negotiations.

Product segmentation within the MEA SGLT2 inhibitors market encompasses multiple therapeutic categories and formulation approaches designed to optimize patient outcomes and clinical utility. Market segmentation analysis reveals distinct growth patterns and opportunities across different product categories.

By Drug Type:

By Application:

By Distribution Channel:

Monotherapy applications represent the foundational market segment where SGLT2 inhibitors serve as standalone therapeutic interventions for diabetes management. This category demonstrates steady growth with approximately 28% adoption rate among newly diagnosed type 2 diabetes patients. Clinical protocols increasingly recognize SGLT2 inhibitors as first-line therapy options due to their unique mechanism of action and favorable safety profiles.

Combination therapy categories show accelerating growth as healthcare providers seek comprehensive diabetes management approaches that address multiple pathophysiological mechanisms. Fixed-dose combinations integrating SGLT2 inhibitors with metformin or DPP-4 inhibitors demonstrate improved patient compliance and therapeutic outcomes. Pharmaceutical development focuses on optimizing combination formulations that enhance efficacy while minimizing adverse effects.

Extended-release formulations provide enhanced patient convenience and improved medication adherence through simplified dosing regimens. These specialized formulations address patient compliance challenges while maintaining therapeutic efficacy. Market acceptance of extended-release options continues growing as healthcare providers recognize the importance of medication adherence in diabetes management.

Pediatric applications represent an emerging category with limited but growing clinical evidence supporting SGLT2 inhibitor use in adolescent diabetes populations. Regulatory approvals for pediatric indications create new market opportunities while requiring specialized clinical protocols and safety monitoring. Healthcare providers approach pediatric SGLT2 inhibitor therapy with careful consideration of risk-benefit profiles and long-term safety implications.

Healthcare providers benefit from SGLT2 inhibitor therapy through improved patient outcomes and comprehensive diabetes management capabilities. These medications offer unique therapeutic advantages including cardiovascular protection and weight management benefits that extend beyond traditional glycemic control. Clinical practice enhancement occurs through access to evidence-based treatment options with proven efficacy and safety profiles.

Pharmaceutical companies gain competitive advantages through SGLT2 inhibitor portfolio development and market positioning strategies. Revenue growth opportunities exist across multiple therapeutic indications and patient populations. Market differentiation occurs through clinical evidence generation, combination therapy development, and patient support program implementation.

Patients experience significant benefits through improved glycemic control, reduced cardiovascular risk, and enhanced quality of life outcomes. SGLT2 inhibitor therapy provides weight management advantages and reduced hypoglycemia risk compared to traditional diabetes medications. Treatment satisfaction increases through once-daily dosing convenience and comprehensive therapeutic benefits.

Healthcare systems realize cost-effectiveness benefits through reduced hospitalization rates and long-term complication prevention. SGLT2 inhibitor therapy contributes to improved population health outcomes and reduced healthcare resource utilization. Economic benefits include decreased emergency department visits and reduced need for intensive diabetes management interventions.

Regulatory authorities benefit from robust clinical evidence supporting SGLT2 inhibitor safety and efficacy across diverse patient populations. Comprehensive post-market surveillance data enhances regulatory decision-making and public health protection. Healthcare policy development benefits from real-world evidence demonstrating therapeutic value and cost-effectiveness outcomes.

Strengths:

Weaknesses:

Opportunities:

Threats:

Personalized medicine approaches are transforming SGLT2 inhibitor therapy through genetic testing and biomarker identification that optimize treatment selection for individual patients. Healthcare providers increasingly utilize precision medicine principles to enhance therapeutic outcomes and minimize adverse effects. Clinical protocols evolve to incorporate patient-specific factors that influence SGLT2 inhibitor efficacy and safety profiles.

Digital health integration accelerates through connected glucose monitoring devices and mobile health applications that enhance SGLT2 inhibitor therapy management. Telemedicine platforms expand access to specialized diabetes care and medication monitoring services. Healthcare technology advancement enables real-time patient monitoring and data-driven treatment optimization strategies.

Combination therapy innovation drives market evolution through development of triple and quadruple combination formulations that address multiple diabetes pathophysiology mechanisms simultaneously. Pharmaceutical companies invest in complex formulation development to enhance therapeutic efficacy while maintaining patient compliance. Clinical research focuses on optimizing combination ratios and identifying synergistic therapeutic interactions.

Value-based healthcare models influence SGLT2 inhibitor market dynamics through outcome-based pricing and reimbursement strategies. Healthcare systems increasingly evaluate medications based on long-term health economic benefits rather than acquisition costs alone. Market access strategies emphasize demonstrating real-world effectiveness and cost-effectiveness outcomes to support reimbursement decisions.

Regulatory harmonization trends facilitate streamlined approval processes and reduced market entry barriers across MEA countries. International regulatory collaboration enhances safety monitoring and post-market surveillance capabilities. Quality standards alignment ensures consistent product safety and efficacy across different regional markets while reducing regulatory compliance costs.

Clinical trial expansion across MEA regions demonstrates pharmaceutical industry commitment to generating region-specific safety and efficacy data for SGLT2 inhibitor therapy. Major pharmaceutical companies invest in local clinical research capabilities and patient recruitment infrastructure. Research initiatives focus on addressing regional population characteristics and healthcare system requirements.

Manufacturing capacity development includes establishment of local production facilities and supply chain infrastructure to enhance SGLT2 inhibitor availability and reduce costs. Regional manufacturing initiatives support government policies promoting local pharmaceutical production. Supply chain optimization improves medication accessibility while reducing dependence on international imports.

Healthcare partnership agreements between international pharmaceutical companies and regional healthcare providers expand SGLT2 inhibitor access and clinical expertise. Collaborative initiatives include healthcare professional training programs and patient education campaigns. Strategic alliances enhance market penetration while building local healthcare capabilities and knowledge transfer.

Regulatory milestone achievements include accelerated approval processes and expanded therapeutic indications for SGLT2 inhibitors across multiple MEA countries. Regulatory authorities recognize the clinical value and safety profiles of these medications through streamlined review processes. Market access improvements result from collaborative efforts between pharmaceutical companies and regulatory agencies to expedite patient access to innovative therapies.

Digital health initiatives integrate SGLT2 inhibitor therapy with connected healthcare technologies and patient monitoring systems. Pharmaceutical companies develop companion digital therapeutics and mobile health applications that enhance medication management. Technology partnerships create comprehensive diabetes management ecosystems that improve patient outcomes and healthcare provider efficiency.

Market entry strategies should prioritize countries with established healthcare infrastructure and favorable regulatory environments while building capabilities for future expansion into emerging markets. MarkWide Research analysis indicates that successful market penetration requires comprehensive understanding of local healthcare systems and patient access barriers. Companies should invest in regional partnerships and local expertise development to navigate complex market dynamics effectively.

Product development focus should emphasize combination therapies and patient-friendly formulations that address compliance challenges and enhance therapeutic outcomes. Innovation opportunities exist in developing region-specific formulations that consider local patient preferences and healthcare delivery constraints. Clinical evidence generation remains critical for supporting market access and reimbursement negotiations across diverse MEA healthcare systems.

Healthcare partnership development represents a crucial success factor for sustainable market growth and clinical adoption. Companies should establish collaborative relationships with key opinion leaders, healthcare institutions, and government agencies to build market credibility and access. Educational initiatives targeting healthcare professionals and patients can accelerate adoption rates and improve therapeutic outcomes.

Pricing strategies must balance commercial objectives with market access requirements and patient affordability considerations. Tiered pricing approaches and patient assistance programs can expand market reach while maintaining commercial viability. Value demonstration through health economic studies and real-world evidence generation supports premium pricing and reimbursement negotiations.

Digital transformation integration should complement traditional pharmaceutical marketing and distribution approaches with innovative patient engagement and medication management solutions. Technology partnerships can enhance competitive positioning while improving patient outcomes and healthcare provider satisfaction. Data analytics capabilities enable personalized patient support and treatment optimization strategies.

Market expansion trajectory indicates sustained growth potential driven by increasing diabetes prevalence and healthcare infrastructure development across MEA regions. The market is projected to maintain robust growth momentum with approximately 14.2% CAGR over the next five years. Healthcare investments in diabetes management programs and specialized care services will continue supporting market development and patient access improvements.

Therapeutic innovation will drive market evolution through next-generation SGLT2 inhibitors with enhanced efficacy profiles and reduced side effect risks. Pharmaceutical research focuses on developing selective inhibitors and combination therapies that optimize therapeutic benefits. Clinical pipeline development includes novel formulations and delivery mechanisms that improve patient compliance and treatment outcomes.

Regional market maturation will occur at different rates across MEA countries, with GCC nations leading adoption while African markets demonstrate emerging growth potential. Healthcare policy evolution and economic development will influence market accessibility and growth trajectories. Market penetration rates are expected to increase significantly as healthcare infrastructure and professional education programs expand.

Competitive landscape evolution will intensify as patent expirations enable generic competition and biosimilar development. Market dynamics will shift toward value-based competition emphasizing clinical outcomes and cost-effectiveness. MWR projections indicate that successful companies will differentiate through comprehensive patient support programs and innovative therapeutic approaches rather than traditional marketing strategies alone.

Healthcare integration trends will incorporate SGLT2 inhibitor therapy into comprehensive diabetes management protocols and chronic disease prevention programs. Digital health technologies will enhance medication management and patient monitoring capabilities. Future market success will depend on companies’ ability to adapt to evolving healthcare delivery models and patient engagement preferences across diverse MEA markets.

The MEA Sodium-dependent Glucose Co-transporter 2 Inhibitors market represents a dynamic and rapidly evolving pharmaceutical sector with substantial growth potential across diverse regional markets. The therapeutic landscape demonstrates strong fundamentals driven by increasing diabetes prevalence, expanding healthcare infrastructure, and growing recognition of SGLT2 inhibitor clinical benefits beyond traditional glycemic control.

Market opportunities exist across multiple dimensions including geographic expansion, therapeutic innovation, and healthcare partnership development. Successful market participants must navigate complex regional dynamics while building sustainable competitive advantages through clinical evidence generation and patient access optimization. Strategic positioning requires comprehensive understanding of local healthcare systems, regulatory requirements, and patient needs across different MEA countries.

Future market success will depend on companies’ ability to balance commercial objectives with healthcare value creation and patient accessibility considerations. The evolving competitive landscape demands innovative approaches to product development, market access, and patient engagement that extend beyond traditional pharmaceutical business models. Healthcare transformation trends including digitization and value-based care will continue shaping market dynamics and growth opportunities throughout the region.

What is Sodium-dependent Glucose Co-transporter 2 Inhibitors?

Sodium-dependent Glucose Co-transporter 2 Inhibitors are a class of medications used primarily to manage type two diabetes by preventing glucose reabsorption in the kidneys, thereby promoting glucose excretion in urine.

What are the key players in the MEA Sodium-dependent Glucose Co-transporter 2 Inhibitors Market?

Key players in the MEA Sodium-dependent Glucose Co-transporter 2 Inhibitors Market include AstraZeneca, Boehringer Ingelheim, and Johnson & Johnson, among others.

What are the growth factors driving the MEA Sodium-dependent Glucose Co-transporter 2 Inhibitors Market?

The growth of the MEA Sodium-dependent Glucose Co-transporter 2 Inhibitors Market is driven by the rising prevalence of diabetes, increasing awareness of diabetes management, and advancements in drug formulations.

What challenges does the MEA Sodium-dependent Glucose Co-transporter 2 Inhibitors Market face?

Challenges in the MEA Sodium-dependent Glucose Co-transporter 2 Inhibitors Market include potential side effects, competition from alternative diabetes treatments, and regulatory hurdles in drug approval processes.

What opportunities exist in the MEA Sodium-dependent Glucose Co-transporter 2 Inhibitors Market?

Opportunities in the MEA Sodium-dependent Glucose Co-transporter 2 Inhibitors Market include the development of new formulations, expansion into emerging markets, and increasing collaborations between pharmaceutical companies and healthcare providers.

What trends are shaping the MEA Sodium-dependent Glucose Co-transporter 2 Inhibitors Market?

Trends in the MEA Sodium-dependent Glucose Co-transporter 2 Inhibitors Market include a focus on personalized medicine, the integration of digital health technologies, and an emphasis on patient-centric treatment approaches.

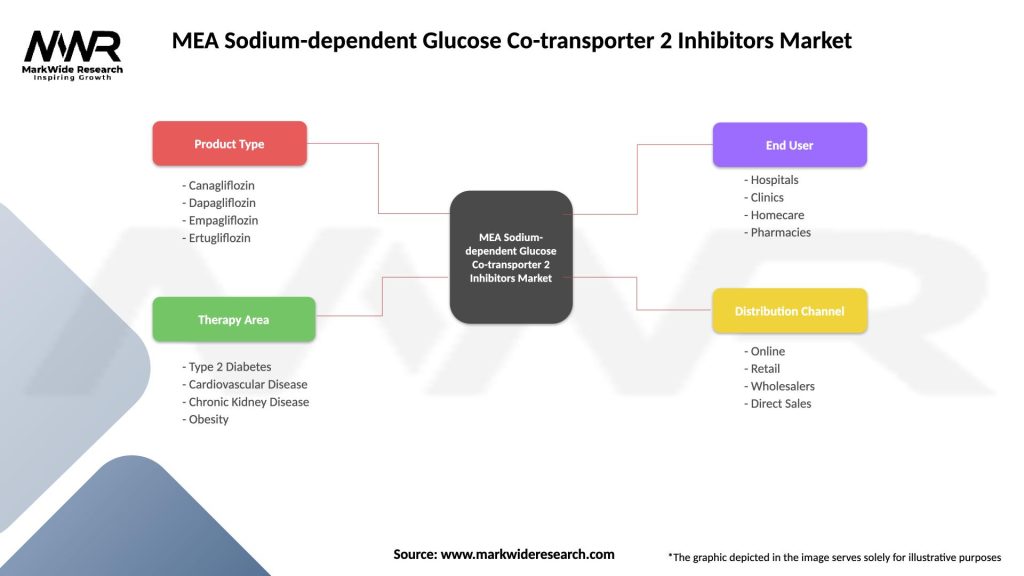

MEA Sodium-dependent Glucose Co-transporter 2 Inhibitors Market

| Segmentation Details | Description |

|---|---|

| Product Type | Canagliflozin, Dapagliflozin, Empagliflozin, Ertugliflozin |

| Therapy Area | Type 2 Diabetes, Cardiovascular Disease, Chronic Kidney Disease, Obesity |

| End User | Hospitals, Clinics, Homecare, Pharmacies |

| Distribution Channel | Online, Retail, Wholesalers, Direct Sales |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the MEA Sodium-dependent Glucose Co-transporter 2 Inhibitors Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.