444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The MEA distributed solar power generation market represents a transformative shift in the region’s energy landscape, characterized by rapid technological advancement and increasing adoption of decentralized renewable energy solutions. Middle East and Africa regions are experiencing unprecedented growth in distributed solar installations, driven by abundant solar resources, declining technology costs, and supportive government policies. The market encompasses residential rooftop systems, commercial solar installations, and community-based solar projects that collectively contribute to energy independence and sustainability goals.

Market dynamics indicate robust expansion across key MEA countries, with the distributed solar power generation market experiencing accelerated growth rates of approximately 12.5% CAGR in recent years. This growth trajectory reflects increasing awareness of renewable energy benefits, technological improvements in solar panel efficiency, and favorable regulatory frameworks supporting distributed energy resources. The region’s strategic focus on diversifying energy portfolios and reducing dependence on traditional fossil fuels continues to drive substantial investments in solar infrastructure.

Regional adoption patterns vary significantly across MEA territories, with countries like South Africa, UAE, and Saudi Arabia leading in distributed solar deployment. The market benefits from exceptional solar irradiation levels, making distributed solar power generation economically viable and environmentally beneficial. Technology integration with smart grid systems and energy storage solutions further enhances the appeal of distributed solar installations for both residential and commercial applications.

The distributed solar power generation market refers to the comprehensive ecosystem of decentralized solar energy systems that generate electricity at or near the point of consumption, rather than at large centralized power plants. This market encompasses various solar technologies including photovoltaic panels, inverters, energy storage systems, and smart grid integration components that enable efficient distributed energy generation across residential, commercial, and industrial sectors.

Distributed solar systems typically range from small residential rooftop installations to larger commercial and community solar projects that serve local energy needs while contributing excess power to the grid. The market includes both grid-tied and off-grid solutions, with increasing emphasis on hybrid systems that combine solar generation with battery storage for enhanced energy security and independence.

Key characteristics of distributed solar power generation include scalability, modularity, and the ability to reduce transmission losses by generating power closer to consumption points. This approach democratizes energy production, allowing individual consumers and businesses to become active participants in the energy ecosystem while contributing to overall grid stability and renewable energy adoption goals.

Strategic market analysis reveals that the MEA distributed solar power generation market is positioned for exceptional growth, driven by convergence of favorable environmental conditions, supportive policies, and technological advancement. The market demonstrates strong momentum across multiple segments, with residential installations showing particularly robust adoption rates of approximately 18% annually in key markets.

Investment trends indicate increasing capital allocation toward distributed solar projects, supported by declining equipment costs and improved financing mechanisms. Commercial and industrial segments are experiencing accelerated adoption as businesses recognize the economic benefits of distributed solar power generation, including reduced energy costs and enhanced sustainability credentials.

Technological evolution continues to enhance market attractiveness, with improvements in solar panel efficiency, energy storage integration, and smart grid connectivity creating new opportunities for distributed energy deployment. The market benefits from increasing collaboration between technology providers, financial institutions, and government agencies to create comprehensive distributed solar ecosystems.

Regional leadership varies across MEA countries, with established markets demonstrating mature adoption patterns while emerging markets show significant growth potential. The overall market trajectory suggests sustained expansion supported by favorable regulatory environments and increasing recognition of distributed solar power generation as a viable alternative to traditional energy sources.

Market intelligence reveals several critical insights that define the MEA distributed solar power generation landscape:

Market segmentation analysis indicates diverse opportunities across residential, commercial, and utility-scale distributed applications, each presenting unique growth drivers and implementation challenges that shape overall market development patterns.

Primary growth drivers propelling the MEA distributed solar power generation market include exceptional solar resource availability, with many regions receiving over 2,000 kWh/m² of annual solar irradiation. This abundant natural resource creates ideal conditions for distributed solar installations, making them economically attractive and environmentally beneficial across diverse applications.

Economic factors significantly influence market expansion, particularly declining solar technology costs and improving system economics. The levelized cost of electricity from distributed solar systems has decreased substantially, making solar power generation competitive with grid electricity in many MEA markets. Additionally, rising conventional energy costs create favorable economic conditions for distributed solar adoption.

Policy initiatives across MEA countries are actively supporting distributed solar power generation through various mechanisms including feed-in tariffs, net metering programs, and renewable energy mandates. Government commitments to carbon reduction and energy diversification create supportive regulatory environments that encourage distributed solar investments.

Energy security concerns drive interest in distributed solar power generation as countries seek to reduce dependence on energy imports and enhance grid resilience. Distributed solar systems contribute to energy independence while providing backup power capabilities during grid outages, particularly when combined with energy storage solutions.

Technological advancement continues to improve distributed solar system performance and reliability, with innovations in panel efficiency, inverter technology, and monitoring systems enhancing overall value propositions. Smart grid integration capabilities enable better system optimization and grid interaction, further supporting market growth.

Implementation challenges present significant barriers to distributed solar power generation market expansion, particularly high upfront capital requirements that can limit adoption among cost-sensitive consumers and small businesses. Despite declining equipment costs, initial investment requirements remain substantial for many potential adopters, especially in emerging markets with limited access to financing.

Grid infrastructure limitations in many MEA regions create technical challenges for distributed solar integration, including inadequate transmission capacity and outdated grid management systems. These infrastructure constraints can limit the ability to accommodate distributed solar power generation and may require substantial utility investments to address.

Regulatory uncertainty in some markets creates hesitation among potential investors and adopters, particularly regarding long-term policy stability and grid interconnection procedures. Inconsistent regulatory frameworks and changing government policies can impact project economics and investment decisions.

Technical expertise gaps limit market development in regions lacking sufficient skilled workforce for distributed solar system installation, maintenance, and operation. This skills shortage can increase project costs and reduce system performance, hindering market growth potential.

Intermittency concerns associated with solar power generation create challenges for grid operators and energy planners, particularly in systems with high distributed solar penetration. Managing variable solar output requires sophisticated grid management capabilities and potentially additional backup power resources.

Emerging market segments present substantial opportunities for distributed solar power generation expansion, particularly in rural electrification and off-grid applications where distributed solar systems can provide reliable electricity access. These applications address critical energy needs while creating new market opportunities for technology providers and service companies.

Commercial sector adoption represents a significant growth opportunity, with businesses increasingly recognizing distributed solar power generation benefits including reduced energy costs, enhanced sustainability profiles, and improved energy security. Corporate sustainability commitments and environmental reporting requirements are driving commercial solar adoption across various industries.

Energy storage integration creates new value propositions for distributed solar systems, enabling energy independence, grid services participation, and enhanced system economics. The combination of solar generation with battery storage opens opportunities for time-of-use optimization and backup power applications.

Agrivoltaics applications present innovative opportunities combining solar power generation with agricultural activities, particularly relevant in MEA regions with extensive agricultural sectors. These dual-use systems can provide additional revenue streams for farmers while contributing to renewable energy goals.

Digital transformation opportunities include development of advanced monitoring, control, and optimization systems that enhance distributed solar power generation performance and enable new service models. Internet of Things integration and artificial intelligence applications can improve system efficiency and reduce operational costs.

Supply chain evolution significantly impacts MEA distributed solar power generation market dynamics, with increasing local manufacturing capabilities reducing costs and improving supply security. Regional solar panel production facilities and component manufacturing are developing to serve growing local demand while reducing dependence on imports.

Competitive landscape dynamics reflect increasing participation from both international technology providers and local companies, creating diverse market ecosystems with varying approaches to distributed solar power generation. This competition drives innovation and cost reduction while expanding market access through diverse business models.

Financial market development continues to evolve, with new financing mechanisms and investment structures supporting distributed solar adoption. Solar loans, leasing programs, and power purchase agreements are becoming more widely available, improving market accessibility for diverse customer segments.

Technology convergence with other distributed energy resources creates synergistic opportunities, particularly integration with energy storage, electric vehicle charging, and smart home systems. These convergence trends enhance the value proposition of distributed solar power generation while creating new market opportunities.

Grid modernization efforts across MEA regions are improving conditions for distributed solar integration, with smart grid investments and advanced metering infrastructure supporting better distributed energy resource management. These improvements facilitate higher distributed solar penetration levels while maintaining grid stability.

Comprehensive market analysis employs multiple research methodologies to ensure accurate and reliable insights into the MEA distributed solar power generation market. Primary research includes extensive interviews with industry stakeholders, technology providers, government officials, and end-users to gather firsthand market intelligence and validate market trends.

Secondary research methodology incorporates analysis of government publications, industry reports, academic studies, and regulatory documents to establish comprehensive market context and historical trends. This approach ensures thorough coverage of market dynamics and regulatory influences affecting distributed solar power generation adoption.

Data validation processes include cross-referencing multiple sources, expert consultations, and statistical analysis to ensure research accuracy and reliability. Market sizing and forecasting methodologies employ established econometric models adapted for renewable energy market characteristics and regional economic conditions.

Regional analysis approach considers country-specific factors including solar resource availability, regulatory frameworks, economic conditions, and infrastructure development to provide nuanced market insights. This methodology recognizes significant variations across MEA markets while identifying common trends and opportunities.

Technology assessment includes evaluation of current and emerging distributed solar technologies, cost trends, and performance characteristics to inform market projections and opportunity identification. This technical analysis supports strategic recommendations and market development insights.

Middle East markets demonstrate strong distributed solar power generation adoption, led by UAE and Saudi Arabia where government initiatives and abundant solar resources create favorable conditions. The UAE’s distributed solar programs have achieved approximately 25% market penetration in targeted segments, while Saudi Arabia’s Vision 2030 supports substantial distributed solar deployment across residential and commercial applications.

North African markets show significant potential for distributed solar power generation, with countries like Morocco and Egypt developing comprehensive renewable energy strategies that include distributed solar components. Morocco’s distributed solar initiatives have demonstrated 15% annual growth in residential installations, supported by favorable financing mechanisms and government incentives.

Sub-Saharan Africa presents unique opportunities for distributed solar power generation, particularly in off-grid and mini-grid applications that address energy access challenges. South Africa leads regional adoption with established net metering programs and commercial solar markets, while countries like Kenya and Ghana show rapid growth in distributed solar applications.

Gulf Cooperation Council countries collectively represent mature markets for distributed solar power generation, with established regulatory frameworks and strong government support. These markets benefit from high electricity tariffs, abundant solar resources, and sophisticated financial markets that support distributed solar investments.

Regional collaboration initiatives are emerging to share best practices and coordinate distributed solar power generation development across MEA countries. These collaborative efforts include technology transfer programs, joint research initiatives, and coordinated policy development that supports regional market growth.

Market leadership in the MEA distributed solar power generation sector includes both international technology providers and emerging regional players who offer comprehensive solutions across the distributed solar value chain:

Regional companies are increasingly important in the MEA distributed solar power generation market, offering localized services, installation expertise, and market-specific solutions. These companies often partner with international technology providers to deliver comprehensive distributed solar solutions tailored to local market conditions.

Strategic partnerships between technology providers, financial institutions, and local companies are becoming increasingly common, creating integrated value chains that support distributed solar power generation market development across diverse MEA markets.

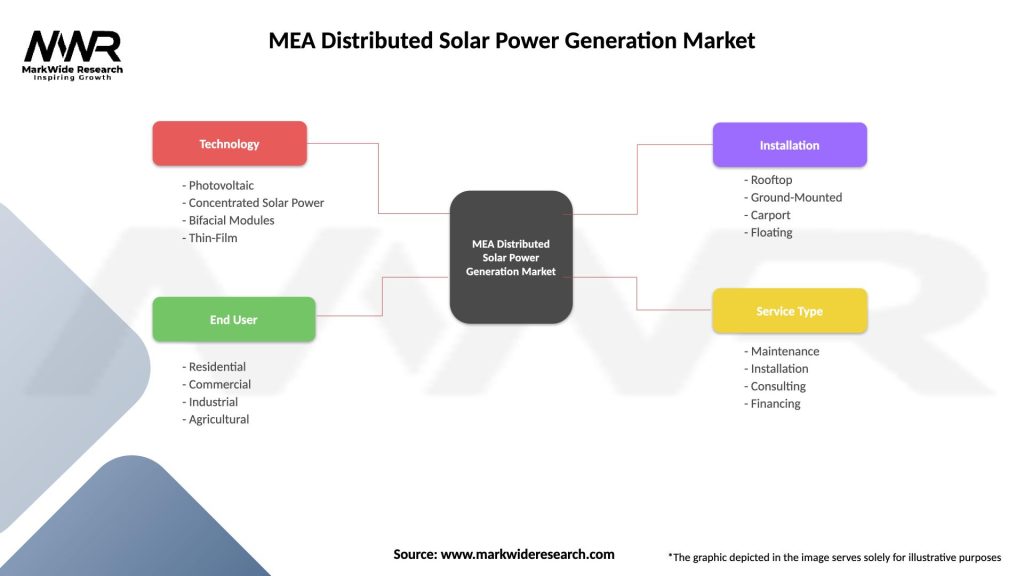

By Technology:

By Application:

By System Type:

By End-User:

Residential segment analysis reveals strong growth momentum driven by declining system costs and increasing environmental awareness. Residential distributed solar power generation systems typically range from 3-10 kW capacity, with financing options including solar loans, leasing programs, and power purchase agreements making adoption more accessible to diverse income levels.

Commercial sector insights indicate businesses are increasingly adopting distributed solar power generation to reduce operating costs and meet sustainability goals. Commercial systems typically range from 50 kW to several megawatts, with payback periods of 5-8 years making them attractive investments for cost-conscious businesses.

Industrial applications demonstrate significant potential for large-scale distributed solar power generation, particularly in energy-intensive industries seeking to reduce electricity costs and carbon footprints. Industrial distributed solar systems often integrate with existing facilities and can provide substantial portions of facility energy requirements.

Agricultural sector opportunities include innovative agrivoltaic applications that combine solar power generation with farming activities, creating dual revenue streams while addressing rural energy needs. These applications are particularly relevant in MEA regions with extensive agricultural sectors and high solar irradiation levels.

Off-grid applications serve critical energy access needs in remote areas where grid connection is impractical or unavailable. These systems typically include battery storage and are essential for rural electrification and development initiatives across MEA regions.

Technology providers benefit from expanding market opportunities across diverse MEA countries, with growing demand for distributed solar power generation systems creating substantial revenue potential. The market offers opportunities for both established international companies and emerging regional players to develop specialized solutions for local market conditions.

Financial institutions gain access to new investment opportunities in the growing distributed solar sector, with various financing models including project finance, equipment leasing, and green bonds supporting market development. The sector offers attractive risk-adjusted returns while supporting sustainable development goals.

End-users realize significant benefits including reduced energy costs, enhanced energy security, and improved sustainability profiles. Residential customers can achieve 20-40% electricity bill reductions, while commercial users benefit from predictable energy costs and corporate sustainability advantages.

Government stakeholders achieve multiple policy objectives through distributed solar power generation support, including renewable energy targets, energy security enhancement, and economic development. Distributed solar deployment creates local employment opportunities while reducing carbon emissions and energy import dependence.

Utility companies can benefit from distributed solar integration through reduced peak demand, deferred infrastructure investments, and new service opportunities. Progressive utilities are developing distributed energy resource management capabilities and new business models that incorporate distributed solar power generation.

Environmental stakeholders benefit from reduced carbon emissions and environmental impact associated with distributed solar power generation adoption. The technology contributes to air quality improvement and climate change mitigation while supporting sustainable development initiatives.

Strengths:

Weaknesses:

Opportunities:

Threats:

Digitalization trends are transforming the MEA distributed solar power generation market through advanced monitoring, control, and optimization systems. Internet of Things integration enables real-time system monitoring and predictive maintenance, while artificial intelligence applications optimize energy production and consumption patterns.

Energy storage integration represents a critical trend enhancing distributed solar system value propositions. Battery storage adoption is growing at approximately 30% annually in key MEA markets, enabling energy independence, grid services participation, and enhanced system economics through time-of-use optimization.

Financing innovation continues to evolve with new models including solar-as-a-service, community solar programs, and green financing initiatives making distributed solar power generation more accessible. MarkWide Research analysis indicates that innovative financing mechanisms are expanding market reach to previously underserved segments.

Grid modernization efforts across MEA regions are improving conditions for distributed solar integration, with smart grid investments and advanced metering infrastructure supporting better distributed energy resource management. These improvements facilitate higher distributed solar penetration while maintaining grid stability.

Sustainability focus is driving increased corporate adoption of distributed solar power generation as businesses seek to meet environmental commitments and reporting requirements. Corporate renewable energy procurement is growing significantly, with distributed solar representing an attractive option for on-site clean energy generation.

Technology convergence with electric vehicle charging, smart buildings, and other distributed energy resources is creating integrated energy ecosystems that enhance overall system value and efficiency.

Recent technological advancement include development of higher-efficiency solar panels, advanced inverter technologies, and integrated energy management systems that enhance distributed solar power generation performance. These innovations are improving system economics while expanding application possibilities across diverse market segments.

Policy developments across MEA countries include implementation of net metering programs, renewable energy mandates, and distributed solar incentives that support market growth. Several countries have recently updated their renewable energy policies to specifically encourage distributed solar adoption.

Strategic partnerships between international technology providers and local companies are expanding market reach and improving service capabilities. These collaborations combine global expertise with local market knowledge to deliver comprehensive distributed solar solutions.

Financial market developments include launch of specialized solar financing programs, green bond issuances, and development of solar investment funds that support distributed solar power generation projects. These financial innovations are improving capital availability and reducing financing costs.

Infrastructure investments in grid modernization and energy storage are creating better conditions for distributed solar integration while supporting higher penetration levels. Utility companies are increasingly investing in distributed energy resource management capabilities.

Manufacturing expansion includes establishment of solar panel production facilities and component manufacturing in MEA regions, reducing costs and improving supply chain security for distributed solar power generation systems.

Market entry strategies should focus on understanding local regulatory frameworks, establishing strong local partnerships, and developing market-specific solutions that address regional needs and conditions. Success in MEA distributed solar power generation markets requires comprehensive understanding of diverse country-specific factors.

Technology providers should prioritize development of cost-effective, reliable solutions suitable for MEA climate conditions while building local service and support capabilities. Focus on modular, scalable systems that can serve diverse applications from residential to commercial installations.

Financial institutions should develop specialized distributed solar financing products that address local market conditions and customer needs. Innovative financing mechanisms including pay-as-you-go models and community solar programs can expand market accessibility.

Government stakeholders should focus on creating stable, supportive regulatory frameworks that encourage distributed solar power generation investment while ensuring grid stability and consumer protection. Consistent long-term policies are essential for market development.

Utility companies should proactively develop distributed energy resource management capabilities and explore new business models that incorporate distributed solar power generation. Collaboration with distributed solar providers can create mutual benefits and support grid modernization.

Investment considerations should include careful evaluation of country-specific risks, regulatory stability, and market maturity levels. Diversified regional approaches can help manage risks while capturing growth opportunities across different MEA markets.

Long-term projections indicate continued robust growth for the MEA distributed solar power generation market, supported by improving technology economics, supportive policies, and increasing environmental awareness. MarkWide Research forecasts suggest the market will maintain strong growth momentum with projected expansion rates of 14-16% annually over the next decade.

Technology evolution will continue driving market development through improvements in solar panel efficiency, energy storage integration, and smart grid connectivity. Emerging technologies including perovskite solar cells and advanced energy management systems may create new opportunities for distributed solar power generation applications.

Market maturation is expected across leading MEA countries, with established markets developing sophisticated distributed solar ecosystems while emerging markets experience rapid adoption growth. This maturation process will create opportunities for specialized service providers and technology innovators.

Regional integration initiatives may emerge to coordinate distributed solar power generation development across MEA countries, potentially including technology sharing, joint procurement programs, and coordinated policy development that supports regional market growth.

Sustainability imperatives will continue driving distributed solar adoption as countries and companies seek to meet climate commitments and environmental goals. The technology’s role in achieving carbon neutrality targets will support continued policy support and investment.

Economic development opportunities associated with distributed solar power generation include job creation, technology transfer, and industrial development that can contribute to broader economic growth across MEA regions. The sector’s potential for local value creation supports long-term government support and private investment.

The MEA distributed solar power generation market represents a dynamic and rapidly evolving sector with substantial growth potential driven by exceptional solar resources, supportive policies, and improving technology economics. The market demonstrates strong momentum across residential, commercial, and industrial applications, with diverse opportunities for technology providers, financial institutions, and service companies.

Key success factors include understanding local market conditions, developing appropriate technology solutions, and building strong partnerships with local stakeholders. The market’s complexity requires nuanced approaches that consider country-specific regulatory frameworks, economic conditions, and infrastructure capabilities while leveraging common regional trends and opportunities.

Future prospects remain highly positive, with continued technology advancement, policy support, and increasing environmental awareness supporting sustained market growth. The distributed solar power generation market’s contribution to energy security, economic development, and environmental sustainability positions it as a critical component of MEA’s energy future, offering substantial opportunities for stakeholders across the value chain.

What is Distributed Solar Power Generation?

Distributed Solar Power Generation refers to the production of solar energy from small-scale solar installations located close to the point of use. This can include residential rooftops, commercial buildings, and community solar projects, which contribute to local energy needs and reduce transmission losses.

What are the key players in the MEA Distributed Solar Power Generation Market?

Key players in the MEA Distributed Solar Power Generation Market include companies like First Solar, SunPower, and JinkoSolar, which are involved in manufacturing solar panels and providing solar solutions, among others.

What are the growth factors driving the MEA Distributed Solar Power Generation Market?

The growth of the MEA Distributed Solar Power Generation Market is driven by increasing energy demand, government incentives for renewable energy, and advancements in solar technology that enhance efficiency and reduce costs.

What challenges does the MEA Distributed Solar Power Generation Market face?

Challenges in the MEA Distributed Solar Power Generation Market include regulatory hurdles, high initial investment costs, and the intermittency of solar energy, which can affect reliability and grid integration.

What opportunities exist in the MEA Distributed Solar Power Generation Market?

Opportunities in the MEA Distributed Solar Power Generation Market include the expansion of solar energy policies, increasing corporate sustainability initiatives, and the potential for technological innovations in energy storage and smart grid solutions.

What trends are shaping the MEA Distributed Solar Power Generation Market?

Trends in the MEA Distributed Solar Power Generation Market include the rise of decentralized energy systems, increased adoption of energy storage solutions, and a growing focus on sustainability and carbon reduction initiatives.

MEA Distributed Solar Power Generation Market

| Segmentation Details | Description |

|---|---|

| Technology | Photovoltaic, Concentrated Solar Power, Bifacial Modules, Thin-Film |

| End User | Residential, Commercial, Industrial, Agricultural |

| Installation | Rooftop, Ground-Mounted, Carport, Floating |

| Service Type | Maintenance, Installation, Consulting, Financing |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the MEA Distributed Solar Power Generation Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.