444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The MEA alcoholic beverages market represents a dynamic and evolving landscape characterized by diverse consumer preferences, regulatory frameworks, and cultural considerations across the Middle East and Africa region. This market encompasses a wide range of alcoholic products including beer, wine, spirits, and traditional fermented beverages, each catering to distinct demographic segments and consumption patterns.

Market dynamics in the MEA region are significantly influenced by religious and cultural factors, with varying levels of acceptance and consumption across different countries. While some nations maintain strict regulations on alcohol production and consumption, others have developed thriving hospitality and tourism sectors that drive substantial demand for premium alcoholic beverages.

Growth trajectories across the region show promising developments, with the market experiencing a compound annual growth rate of 4.2% driven by urbanization, rising disposable incomes, and evolving lifestyle preferences among younger demographics. The tourism industry, particularly in countries like the UAE, South Africa, and Morocco, serves as a significant catalyst for market expansion.

Regional variations are particularly pronounced, with North African countries showing different consumption patterns compared to Sub-Saharan Africa and Gulf Cooperation Council nations. South Africa emerges as a dominant market within the region, contributing approximately 45% of total regional consumption, while emerging markets in East and West Africa present substantial growth opportunities.

The MEA alcoholic beverages market refers to the comprehensive ecosystem of production, distribution, and consumption of fermented and distilled alcoholic products across the Middle East and Africa region. This market encompasses all categories of alcoholic beverages including beer, wine, spirits, liqueurs, and traditional fermented drinks that contain ethyl alcohol and are intended for human consumption.

Market scope includes both domestic production facilities and imported products, covering retail sales through various channels including supermarkets, specialty stores, restaurants, bars, hotels, and online platforms. The definition extends to encompass the entire value chain from raw material sourcing and production to final consumer purchase and consumption.

Geographic boundaries of this market include all countries within the Middle East and Africa region, recognizing the diverse regulatory environments, cultural contexts, and economic conditions that influence market dynamics. This includes major markets such as South Africa, Nigeria, Kenya, Morocco, Egypt, UAE, and other emerging economies across the continent.

Strategic positioning of the MEA alcoholic beverages market reflects a complex interplay of cultural acceptance, economic development, and regulatory frameworks that create both opportunities and challenges for industry participants. The market demonstrates resilience and adaptability, with companies successfully navigating diverse operating environments across the region.

Key performance indicators reveal sustained growth momentum, with beer representing the largest category by volume, accounting for approximately 68% of total alcoholic beverage consumption in the region. Premium and craft segments show particularly strong growth potential, driven by increasing consumer sophistication and willingness to pay for quality products.

Investment trends indicate growing confidence in the region’s long-term prospects, with major international brands establishing local production facilities and distribution networks. Local breweries and distilleries are also expanding their operations, contributing to job creation and economic development across multiple countries.

Market consolidation activities continue to shape the competitive landscape, with strategic acquisitions and partnerships enabling companies to achieve greater scale and market penetration. The focus on sustainability and responsible consumption practices is becoming increasingly important for brand positioning and consumer acceptance.

Consumer behavior patterns across the MEA region reveal significant generational differences, with younger demographics showing greater openness to alcoholic beverage consumption and experimentation with different product categories. Urban populations demonstrate higher consumption rates compared to rural areas, reflecting lifestyle differences and product availability.

Premium segment growth represents one of the most significant trends, with consumers increasingly seeking high-quality, authentic products that offer unique experiences. This trend is particularly pronounced in major metropolitan areas and tourist destinations where disposable incomes are higher.

Economic development across the MEA region serves as a fundamental driver for alcoholic beverage market growth, with rising GDP per capita and expanding middle-class populations creating increased purchasing power for discretionary spending on premium beverages.

Urbanization trends significantly impact consumption patterns, as urban populations typically demonstrate higher acceptance and consumption rates of alcoholic beverages. The migration from rural to urban areas continues to expand the addressable market for industry participants.

Tourism industry growth represents a critical driver, particularly in countries that have developed significant hospitality sectors. International visitors contribute substantially to consumption volumes, while also influencing local preferences and introducing new product categories to domestic markets.

Cultural evolution among younger demographics shows increasing acceptance of moderate alcohol consumption as part of social activities and lifestyle choices. This generational shift is particularly evident in urban areas and among educated populations.

Infrastructure development in distribution and retail networks enables better product availability and market penetration. Improved cold chain logistics and modern retail formats facilitate the expansion of temperature-sensitive products like beer and wine.

Regulatory liberalization in select markets has opened new opportunities for both domestic and international players. Countries that have modernized their alcohol policies have typically seen increased investment and market development.

Religious and cultural barriers represent the most significant constraint on market development across many MEA countries. Islamic principles prohibiting alcohol consumption create fundamental limitations on market size and growth potential in predominantly Muslim nations.

Regulatory restrictions vary significantly across the region, with some countries maintaining complete prohibition while others impose heavy taxation, limited distribution channels, or restrictive licensing requirements that constrain market development.

Economic volatility in various MEA markets creates uncertainty for long-term investment planning and can impact consumer spending on discretionary items like alcoholic beverages during economic downturns or currency devaluations.

Infrastructure limitations in some markets affect distribution efficiency and product quality maintenance, particularly for temperature-sensitive products that require sophisticated cold chain logistics throughout the supply chain.

Social stigma associated with alcohol consumption in certain communities can limit market penetration and brand marketing opportunities, requiring companies to adopt sensitive and culturally appropriate marketing strategies.

Import dependencies for raw materials and finished products expose market participants to currency fluctuations, trade policy changes, and supply chain disruptions that can impact profitability and market stability.

Emerging market penetration presents substantial opportunities as several African countries experience rapid economic growth and urbanization. Countries like Ethiopia, Ghana, and Tanzania show promising demographic trends and increasing consumer sophistication.

Premium product positioning offers significant value creation potential as consumers increasingly seek authentic, high-quality experiences. Craft beer, artisanal spirits, and boutique wines represent high-growth segments with attractive profit margins.

Local production expansion provides opportunities to reduce costs, improve supply chain efficiency, and create products tailored to local tastes and preferences. Government incentives for local manufacturing can enhance the attractiveness of these investments.

Digital transformation enables new business models including direct-to-consumer sales, subscription services, and personalized marketing approaches that can improve customer engagement and loyalty.

Sustainability initiatives align with growing consumer awareness and can differentiate brands while potentially reducing operational costs through improved resource efficiency and waste reduction.

Tourism sector partnerships offer opportunities to reach high-value consumer segments and create brand experiences that drive both immediate sales and long-term brand loyalty among domestic consumers.

Supply chain evolution continues to reshape the MEA alcoholic beverages market, with companies investing in local production capabilities and regional distribution networks to improve efficiency and reduce dependency on imports. This transformation is particularly evident in larger markets like South Africa and Nigeria.

Consumer preferences are shifting toward premium and craft products, with traditional mass-market brands facing increased competition from artisanal and boutique producers. This trend is driving innovation in product development and marketing strategies across all beverage categories.

Competitive intensity varies significantly across different market segments and geographic regions. While established international brands maintain strong positions in premium segments, local producers are gaining market share through competitive pricing and products tailored to local preferences.

Technology adoption is accelerating across the value chain, from production automation and quality control systems to digital marketing and e-commerce platforms. Companies that successfully leverage technology demonstrate improved operational efficiency and customer engagement.

Regulatory landscape changes create both opportunities and challenges, with some countries liberalizing policies while others maintain or strengthen restrictions. Market participants must remain agile and adaptable to navigate these evolving regulatory environments.

Economic cycles significantly impact consumption patterns, with premium products typically showing greater sensitivity to economic conditions compared to value-oriented offerings. Understanding these dynamics is crucial for strategic planning and market positioning.

Primary research activities encompass comprehensive field studies across key MEA markets, including structured interviews with industry executives, distributors, retailers, and consumers to gather firsthand insights into market dynamics, consumer behavior, and competitive positioning.

Secondary research sources include government statistical databases, industry association reports, trade publications, and regulatory filings to establish market baselines and validate primary research findings. This approach ensures comprehensive coverage of both quantitative and qualitative market aspects.

Data collection methodology employs multiple approaches including online surveys, focus group discussions, retail audits, and trade channel analysis to capture diverse perspectives and ensure representative sampling across different market segments and geographic regions.

Analytical frameworks utilize advanced statistical techniques and market modeling approaches to identify trends, correlations, and predictive indicators that inform strategic recommendations and market forecasts.

Quality assurance protocols include data triangulation, expert validation, and peer review processes to ensure accuracy and reliability of research findings. All data sources are carefully evaluated for credibility and relevance to the specific market context.

Market segmentation analysis employs both demographic and psychographic variables to identify distinct consumer groups and their specific preferences, purchasing behaviors, and brand loyalties across different product categories and price points.

South Africa dominates the regional market, representing the most mature and developed alcoholic beverages market in the MEA region. The country benefits from established production infrastructure, sophisticated distribution networks, and relatively liberal regulatory frameworks that support market growth.

North African markets including Morocco, Tunisia, and Egypt show varying degrees of market development, with Morocco leading in wine production and consumption due to its established viticulture industry. These markets benefit from tourism sectors that drive demand for premium alcoholic beverages.

West African countries such as Nigeria, Ghana, and Ivory Coast represent high-growth markets with expanding urban populations and increasing disposable incomes. Nigeria, in particular, shows strong potential with its large population and growing middle class, contributing approximately 15% of regional market share.

East African markets including Kenya, Tanzania, and Ethiopia are experiencing rapid economic development and urbanization, creating new opportunities for market expansion. Kenya leads this sub-region with well-established local brewing industries and growing consumer sophistication.

Gulf Cooperation Council countries present unique market dynamics, with the UAE serving as a regional hub for premium alcoholic beverages due to its significant expatriate population and thriving tourism sector. These markets typically focus on high-end products and luxury experiences.

Central African markets remain largely underdeveloped but show potential for future growth as economic conditions improve and infrastructure development progresses. Traditional fermented beverages maintain strong cultural significance in these markets.

Market leadership in the MEA alcoholic beverages sector is characterized by a mix of international beverage conglomerates and strong regional players who have developed deep understanding of local market dynamics and consumer preferences.

Competitive strategies focus on local market adaptation, strategic partnerships with regional distributors, and investment in production facilities that can serve multiple markets efficiently. Brand building and consumer education represent critical success factors.

Innovation initiatives include development of products tailored to local tastes, packaging innovations for challenging distribution environments, and digital marketing strategies that respect cultural sensitivities while building brand awareness.

By Product Type: The market segmentation reveals distinct categories with beer maintaining the largest share, followed by spirits, wine, and traditional fermented beverages. Each category serves different consumer occasions and price points.

By Price Segment: Market stratification shows clear differentiation between value, mainstream, premium, and super-premium categories, with each serving distinct consumer demographics and occasions.

By Distribution Channel: Multiple pathways serve different consumer needs and preferences, from traditional retail to modern trade and on-premise consumption venues.

By Consumer Demographics: Age, income, education, and lifestyle factors create distinct market segments with specific product preferences and purchasing behaviors.

Beer Category Analysis reveals strong performance across the region, with local brands often outperforming international brands in terms of volume sales. Consumer preferences lean toward lighter, refreshing styles suitable for warm climates, though craft beer segments show growing sophistication.

Wine Market Dynamics show interesting regional variations, with North African countries demonstrating stronger wine cultures due to historical viticulture traditions. South Africa leads in both production and consumption, while imported wines capture premium segments across the region.

Spirits Segment Performance indicates growing demand for premium and super-premium categories, particularly in urban markets and tourist destinations. Local spirits production is expanding, with companies developing products that blend international quality standards with local flavor preferences.

Traditional Beverages maintain cultural importance and represent opportunities for formalization and quality improvement. These products often serve as entry points for companies seeking to understand local market dynamics and consumer preferences.

Low-Alcohol Products are gaining traction among health-conscious consumers and those seeking moderation in alcohol consumption. This segment shows particular promise in markets where traditional alcohol consumption faces cultural or religious constraints.

Packaging Innovation across all categories focuses on durability, cost-effectiveness, and environmental sustainability while maintaining product quality and brand appeal in challenging distribution environments.

Revenue Growth Opportunities abound for companies that successfully navigate the complex MEA market landscape, with potential for substantial returns on investment in markets experiencing rapid economic development and urbanization.

Market Diversification benefits enable companies to reduce dependency on mature markets while accessing high-growth regions with favorable demographic trends and increasing consumer purchasing power.

Brand Building Potential exists for companies that invest in long-term market development, consumer education, and culturally sensitive marketing strategies that build trust and loyalty among local consumers.

Supply Chain Optimization opportunities arise from local production investments that reduce costs, improve product freshness, and enable customization for local market preferences while supporting economic development.

Innovation Platforms emerge from diverse consumer needs and preferences across the region, driving product development that can potentially be scaled to other emerging markets globally.

Partnership Opportunities with local distributors, retailers, and hospitality operators provide market access and cultural insights that accelerate market penetration and reduce operational risks.

Sustainability Leadership positions enable companies to differentiate their brands while contributing to environmental and social development goals that resonate with increasingly conscious consumers.

Strengths:

Weaknesses:

Opportunities:

Threats:

Premiumization Movement continues to gain momentum across the MEA region, with consumers increasingly willing to pay higher prices for products that offer superior quality, unique experiences, or authentic heritage. This trend is particularly pronounced in urban areas and among younger demographics.

Craft and Artisanal Products are experiencing significant growth as consumers seek authentic, locally-produced alternatives to mass-market brands. Small-scale breweries and distilleries are emerging across the region, often incorporating local ingredients and traditional production methods.

Health and Wellness Focus is influencing product development, with increasing demand for low-alcohol, organic, and natural products. Consumers are becoming more conscious of ingredient transparency and production methods, driving innovation in healthier alcoholic beverage options.

Digital Commerce Expansion is transforming distribution channels, with online sales platforms and delivery services gaining acceptance, particularly in urban markets. The COVID-19 pandemic accelerated this trend, with many consumers now comfortable purchasing alcoholic beverages online.

Sustainability Initiatives are becoming increasingly important for brand positioning and consumer acceptance. Companies are investing in environmentally friendly packaging, water conservation, renewable energy, and sustainable sourcing practices.

Local Flavor Integration represents a growing trend where international brands incorporate local ingredients, flavors, or production techniques to appeal to regional tastes while maintaining global quality standards.

Production Facility Investments continue across the region, with major international companies establishing or expanding local manufacturing capabilities to serve growing demand while reducing costs and improving supply chain efficiency.

Strategic Acquisitions and partnerships are reshaping the competitive landscape, with companies seeking to gain market access, local expertise, and established distribution networks through targeted transactions and joint ventures.

Regulatory Modernization in select markets is creating new opportunities for industry growth, with some countries updating alcohol policies to support economic development while maintaining appropriate controls and social responsibility measures.

Technology Integration is advancing across all aspects of the value chain, from automated production systems and quality control technologies to digital marketing platforms and customer relationship management systems.

Sustainability Programs are expanding beyond environmental considerations to include social responsibility initiatives, community development projects, and responsible consumption campaigns that build brand trust and social license to operate.

Product Innovation continues to drive market differentiation, with companies launching new products that address specific consumer needs, local preferences, or emerging trends such as low-alcohol options and functional beverages.

Market Entry Strategies should prioritize understanding local cultural contexts, regulatory requirements, and consumer preferences before making significant investments. MarkWide Research analysis indicates that successful market entry typically requires 18-24 months of market preparation and relationship building.

Investment Prioritization should focus on markets with favorable demographic trends, growing tourism sectors, and supportive regulatory environments. Countries showing GDP growth rates above 5% annually typically demonstrate stronger alcoholic beverage market performance.

Product Portfolio Optimization requires balancing international brand appeal with local market adaptation. Companies should consider developing region-specific products that incorporate local ingredients or production methods while maintaining global quality standards.

Distribution Strategy Development must account for infrastructure limitations and cultural considerations in different markets. Multi-channel approaches that combine traditional and modern trade channels typically achieve better market penetration.

Brand Building Approaches should emphasize cultural sensitivity, responsible consumption messaging, and authentic storytelling that resonates with local consumers while building long-term brand equity and social acceptance.

Partnership Development with local distributors, retailers, and hospitality operators provides essential market access and cultural insights that can accelerate growth while reducing operational risks and regulatory compliance challenges.

Growth Projections for the MEA alcoholic beverages market remain positive, with MWR forecasting continued expansion driven by demographic trends, economic development, and evolving consumer preferences. The market is expected to maintain steady growth momentum over the next five years.

Demographic Advantages will continue to support market expansion, with young, urbanizing populations across the region demonstrating increasing acceptance of moderate alcohol consumption as part of modern lifestyles and social activities.

Technology Integration will accelerate across all market segments, from production automation and quality control to digital marketing and e-commerce platforms. Companies that successfully leverage technology will gain competitive advantages in efficiency and customer engagement.

Sustainability Focus will become increasingly important for market success, with consumers and regulators placing greater emphasis on environmental responsibility, social impact, and ethical business practices throughout the value chain.

Market Consolidation is expected to continue as companies seek scale advantages and market access through strategic acquisitions and partnerships. This trend will likely result in stronger, more efficient market players with enhanced capabilities.

Innovation Acceleration will drive product development and market differentiation, with companies investing in new product categories, packaging solutions, and consumer experiences that address evolving market needs and preferences.

Strategic positioning in the MEA alcoholic beverages market requires a nuanced understanding of diverse cultural, regulatory, and economic environments across the region. Companies that successfully navigate these complexities while building authentic relationships with local stakeholders will be best positioned for long-term success.

Market fundamentals remain strong, supported by favorable demographic trends, economic development, and evolving consumer preferences that create substantial opportunities for growth and value creation. The region’s young, urbanizing population represents a significant long-term growth driver for the industry.

Investment opportunities abound for companies willing to take a long-term perspective and invest in market development, local partnerships, and culturally appropriate brand building strategies. Success requires patience, cultural sensitivity, and commitment to responsible business practices.

Future success in the MEA alcoholic beverages market will depend on companies’ ability to balance global expertise with local market adaptation, while maintaining high standards of quality, sustainability, and social responsibility that build trust and acceptance among consumers and stakeholders across the region.

What is MEA Alcoholic Beverages?

MEA Alcoholic Beverages refers to a wide range of alcoholic drinks produced and consumed in the Middle East and Africa region, including beer, wine, and spirits. This market encompasses various segments catering to diverse consumer preferences and cultural practices.

What are the key players in the MEA Alcoholic Beverages Market?

Key players in the MEA Alcoholic Beverages Market include Diageo, Pernod Ricard, and Castel Group, among others. These companies are known for their extensive portfolios and strong distribution networks across the region.

What are the growth factors driving the MEA Alcoholic Beverages Market?

The MEA Alcoholic Beverages Market is driven by factors such as increasing disposable incomes, changing consumer lifestyles, and the growing acceptance of alcoholic beverages in various cultures. Additionally, the rise of e-commerce is facilitating easier access to these products.

What challenges does the MEA Alcoholic Beverages Market face?

The MEA Alcoholic Beverages Market faces challenges such as strict regulations on alcohol sales in certain countries, cultural restrictions, and competition from non-alcoholic beverages. These factors can limit market growth and consumer access.

What opportunities exist in the MEA Alcoholic Beverages Market?

Opportunities in the MEA Alcoholic Beverages Market include the potential for product innovation, such as low-alcohol and flavored beverages, and the expansion of craft breweries. Additionally, increasing tourism in the region presents a chance for growth in the hospitality sector.

What trends are shaping the MEA Alcoholic Beverages Market?

Trends in the MEA Alcoholic Beverages Market include a growing preference for premium and craft products, as well as a rise in health-conscious choices among consumers. Sustainability practices are also becoming more important, influencing production and packaging decisions.

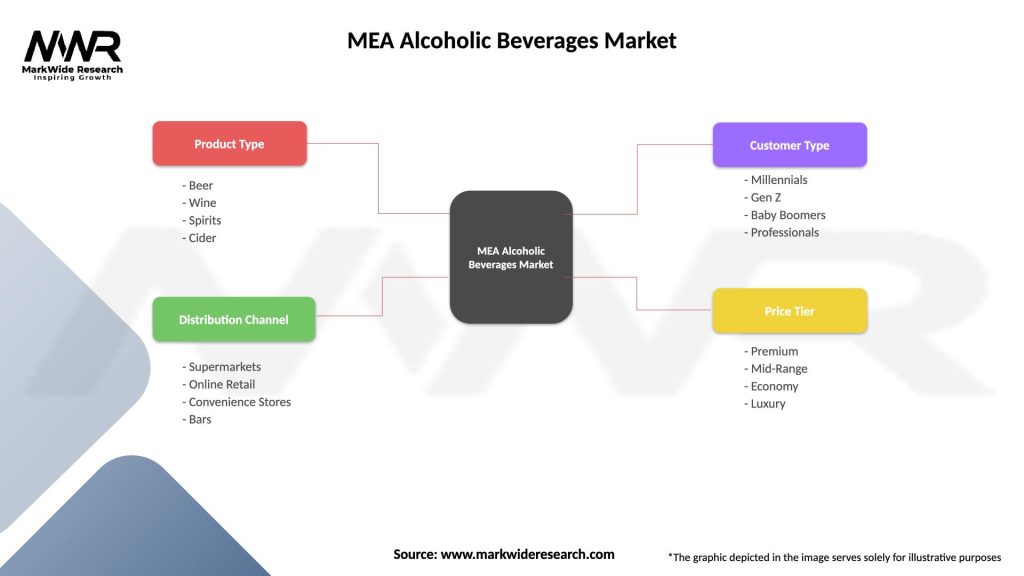

MEA Alcoholic Beverages Market

| Segmentation Details | Description |

|---|---|

| Product Type | Beer, Wine, Spirits, Cider |

| Distribution Channel | Supermarkets, Online Retail, Convenience Stores, Bars |

| Customer Type | Millennials, Gen Z, Baby Boomers, Professionals |

| Price Tier | Premium, Mid-Range, Economy, Luxury |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the MEA Alcoholic Beverages Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.