The Low-Earth Orbit (LEO) satellite market is a dynamic segment within the aerospace industry, characterized by the deployment of satellites in orbits closer to Earth’s surface. LEO satellites offer advantages such as lower latency, higher data speeds, and increased coverage compared to traditional geostationary satellites. This market is driven by the growing demand for high-speed internet connectivity, remote sensing applications, and global communication networks.

Meaning:

Low-Earth Orbit satellites are spacecraft deployed in orbits around Earth at altitudes ranging from 160 to 2,000 kilometers. These satellites orbit closer to the Earth’s surface than geostationary satellites, enabling faster data transmission, reduced signal latency, and improved coverage for various applications such as telecommunications, remote sensing, Earth observation, and scientific research.

Executive Summary:

The Low-Earth Orbit satellite market is experiencing rapid growth fueled by advancements in satellite technology, increasing demand for high-speed internet connectivity in remote areas, and the emergence of new applications such as Earth observation, environmental monitoring, and space-based services. Key players in the market are investing in satellite constellation deployments, launch vehicle development, and ground infrastructure to capitalize on growing market opportunities and gain a competitive edge.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights:

Satellite Constellations: Leading companies are deploying constellations of LEO satellites to provide global coverage for broadband internet services, mobile communications, and Earth observation applications. These constellations leverage interconnected networks of small satellites to deliver high-speed connectivity and real-time data services.

Launch Vehicle Innovation: Advances in launch vehicle technology, including reusable rockets and small satellite launchers, are lowering the cost of accessing space and accelerating the deployment of LEO satellite constellations. Companies are partnering with commercial launch providers to streamline satellite deployment and reduce time-to-market.

Regulatory Environment: Regulatory frameworks governing satellite communications, spectrum allocation, and space traffic management play a critical role in shaping the LEO satellite market. Governments and international organizations are working to establish clear guidelines for satellite operations, orbital debris mitigation, and spectrum coordination to ensure safe and sustainable space activities.

Market Competition: Competition among satellite operators, aerospace companies, and technology providers is intensifying as new players enter the LEO satellite market. Key players are investing in satellite manufacturing, ground segment infrastructure, and service offerings to differentiate their offerings and capture market share.

Market Drivers:

Global Connectivity Demand: The increasing demand for high-speed internet connectivity in remote and underserved areas is driving the deployment of LEO satellite constellations to provide broadband services to residential, commercial, and government users worldwide.

Internet-of-Things (IoT) Applications: The proliferation of IoT devices and sensors across industries such as agriculture, transportation, energy, and logistics is fueling demand for satellite-based connectivity solutions capable of supporting massive machine-to-machine communication networks.

Earth Observation Needs: The growing need for real-time Earth observation data for environmental monitoring, disaster response, urban planning, and resource management is driving investments in LEO satellite constellations equipped with high-resolution imaging sensors and remote sensing payloads.

Emerging Space Markets: The emergence of new space markets, including space tourism, space-based manufacturing, lunar exploration, and asteroid mining, is creating opportunities for LEO satellite operators to support emerging space missions, infrastructure development, and commercial activities.

Market Restraints:

Technical Challenges: Overcoming technical challenges such as satellite design complexity, orbital dynamics, radiation exposure, and space debris mitigation poses significant hurdles for LEO satellite operators seeking to deploy and maintain large-scale satellite constellations in orbit.

Spectrum Allocation Issues: Spectrum allocation constraints and regulatory hurdles related to radio frequency interference, spectrum sharing, and orbital slot coordination may limit the growth of LEO satellite services and constrain the deployment of new satellite constellations.

Competition from Other Technologies: Competition from terrestrial technologies such as 5G networks, fiber-optic cables, and high-altitude platforms (HAPs) for broadband internet connectivity may impact the market viability and business case for LEO satellite operators, particularly in densely populated urban areas.

Financial Viability: Achieving financial viability and return on investment for LEO satellite constellations requires significant upfront capital investment, long-term revenue generation, and cost-effective satellite manufacturing, launch, and operations.

Market Opportunities:

Global Broadband Expansion: Opportunities for LEO satellite operators to expand broadband internet access to underserved and remote regions through satellite constellation deployments, partnerships with telecommunications providers, and government-funded initiatives aimed at bridging the digital divide.

IoT Connectivity Solutions: Opportunities to provide satellite-based IoT connectivity solutions for industries such as agriculture, mining, oil and gas, maritime, and environmental monitoring, enabling remote asset tracking, telemetry, and control applications.

Earth Observation Services: Opportunities to offer satellite-based Earth observation services for applications such as precision agriculture, disaster management, urban planning, climate monitoring, and natural resource management, leveraging high-resolution imaging, multispectral, and synthetic aperture radar (SAR) sensors.

Space-Based Services: Opportunities to develop space-based services such as satellite communications, navigation, remote sensing, and space tourism, catering to government, commercial, and consumer markets with innovative solutions for space-based connectivity, navigation, and exploration.

Market Dynamics:

The Low-Earth Orbit satellite market operates in a dynamic environment influenced by technological advancements, market trends, regulatory developments, and competitive forces. Key market dynamics include:

Technological Advancements: Advances in satellite technology, propulsion systems, miniaturization, and onboard electronics are driving innovation in LEO satellite design, manufacturing, and operations, enabling new applications and business models.

Market Trends: Emerging trends such as mega-constellations, satellite-as-a-service (SAAS) models, software-defined satellites, and on-orbit servicing are shaping the future of the LEO satellite market, offering opportunities for disruptive innovation and market differentiation.

Regulatory Developments: Regulatory frameworks governing spectrum allocation, space traffic management, orbital debris mitigation, and satellite licensing impact market dynamics and influence the strategic decisions of satellite operators, manufacturers, and service providers.

Competitive Landscape: Intense competition among established players and new entrants in the LEO satellite market drives innovation, price competition, and market consolidation, as companies vie for market share, strategic partnerships, and government contracts.

Regional Analysis:

The Low-Earth Orbit satellite market exhibits regional variations influenced by factors such as government policies, market demand, infrastructure development, and technological capabilities. Key regions driving market growth include:

North America: North America dominates the LEO satellite market, driven by the presence of leading satellite operators, aerospace companies, technology providers, and government agencies. The region’s robust space industry ecosystem, favorable regulatory environment, and strong demand for satellite-based services contribute to market growth.

Europe: Europe is a significant player in the LEO satellite market, characterized by investments in satellite manufacturing, launch services, and ground infrastructure. The European Space Agency (ESA), satellite manufacturers, and telecommunications operators play key roles in advancing Europe’s position in the global satellite market.

Asia Pacific: Asia Pacific is a growing market for LEO satellites, driven by rapid urbanization, economic growth, and increasing demand for satellite-based services in sectors such as telecommunications, agriculture, and environmental monitoring. Countries such as China, India, Japan, and Australia are investing in satellite constellations, launch capabilities, and space exploration initiatives.

Latin America: Latin America is emerging as a market for LEO satellite services, with opportunities in telecommunications, remote sensing, and environmental monitoring. Government initiatives, public-private partnerships, and investments in satellite infrastructure contribute to market growth in the region.

Middle East and Africa: The Middle East and Africa region offer opportunities for LEO satellite operators to provide connectivity solutions, remote sensing services, and space-based applications for sectors such as oil and gas, mining, agriculture, and disaster management. Government investments in satellite programs, satellite manufacturing, and space exploration drive market growth in the region.

Competitive Landscape:

Leading Companies in the Low-Earth Orbit Satellite Market:

SpaceX

OneWeb

Amazon (Project Kuiper)

Telesat

LeoSat Enterprises

Iridium Communications Inc.

SES S.A.

Intelsat S.A.

Globalstar, Inc.

O3b Networks (a subsidiary of SES S.A.)

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Segmentation:

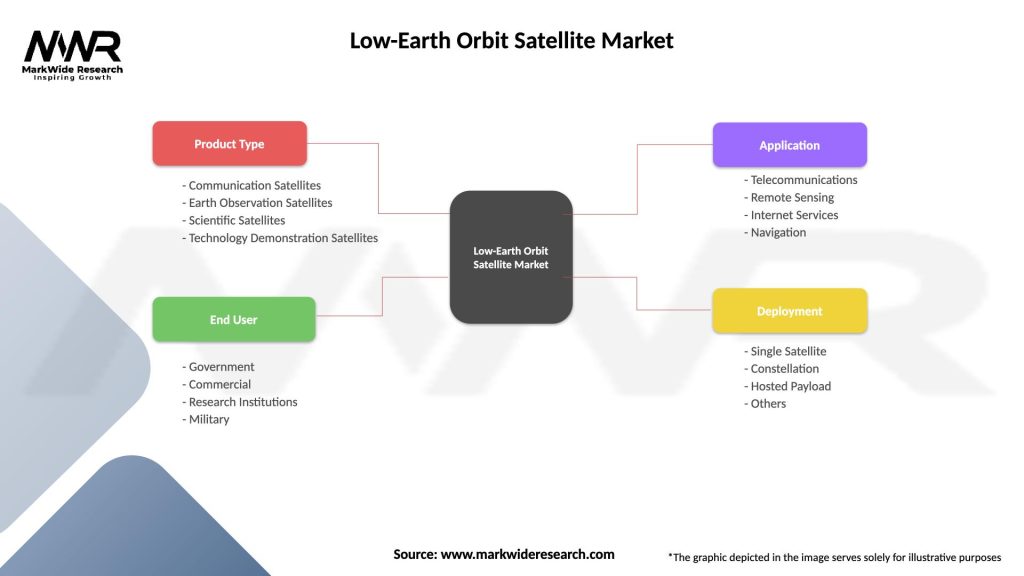

The Low-Earth Orbit satellite market can be segmented based on various factors such as:

Application: Segmentation by application includes telecommunications, Earth observation, remote sensing, navigation, scientific research, and space exploration.

End-User: Segmentation by end-user includes government and defense, commercial enterprises, telecommunications operators, research institutions, and non-profit organizations.

Satellite Type: Segmentation by satellite type includes communication satellites, Earth observation satellites, navigation satellites, scientific research satellites, and technology demonstration satellites.

Orbit Altitude: Segmentation by orbit altitude includes Low-Earth Orbit (LEO), Medium-Earth Orbit (MEO), and Polar Orbit satellites, each offering unique advantages and applications.

Segmentation provides a deeper understanding of market dynamics, customer needs, and competitive landscapes, enabling companies to tailor their strategies, product offerings, and marketing efforts to specific market segments and target audiences.

Category-wise Insights:

Telecommunications: LEO satellite constellations offer opportunities for telecommunications operators to expand their broadband internet services, mobile connectivity, and satellite TV offerings to remote and underserved areas.

Earth Observation: LEO satellites equipped with high-resolution imaging sensors, multispectral cameras, and SAR payloads provide valuable Earth observation data for applications such as environmental monitoring, disaster management, urban planning, and agriculture.

Remote Sensing: LEO satellite data is used for remote sensing applications such as weather forecasting, climate monitoring, oceanography, land cover mapping, and natural resource management, supporting scientific research, commercial activities, and government initiatives.

Navigation and Positioning: LEO satellite navigation systems such as GPS, Galileo, and GLONASS provide accurate positioning, navigation, and timing services for terrestrial, maritime, and aviation applications, enabling precise navigation, asset tracking, and timing synchronization worldwide.

Key Benefits for Industry Participants and Stakeholders:

Global Connectivity: LEO satellite constellations provide global broadband internet coverage, mobile connectivity, and satellite-based services, enabling seamless communication and data exchange worldwide.

Low Latency: LEO satellites offer low-latency communication links, reducing signal delay and improving responsiveness for applications such as voice calls, video conferencing, online gaming, and real-time data transmission.

High Data Rates: LEO satellite constellations deliver high-speed internet access and data rates, enabling users to stream video content, download large files, and access cloud-based services with ease.

Coverage Flexibility: LEO satellites provide flexible coverage and capacity allocation, allowing operators to dynamically adjust satellite resources based on changing demand, traffic patterns, and user requirements.

Resilience and Redundancy: LEO satellite networks offer resilience and redundancy against terrestrial disruptions, natural disasters, and cyber threats, ensuring continuity of communication and data services in adverse conditions.

SWOT Analysis:

A SWOT analysis provides insights into the strengths, weaknesses, opportunities, and threats facing the Low-Earth Orbit satellite market:

Strengths:

Lower latency and higher data speeds compared to geostationary satellites.

Global coverage and flexibility for broadband internet and communication services.

Diverse applications in telecommunications, Earth observation, navigation, and remote sensing.

Potential for disruptive innovation and market differentiation through satellite constellation deployments.

Weaknesses:

Technical challenges such as satellite design complexity and space debris mitigation.

Spectrum allocation constraints and regulatory hurdles for satellite operations.

Competition from terrestrial technologies and alternative connectivity solutions.

Financial viability and return on investment for satellite operators and investors.

Opportunities:

Global expansion of broadband internet services to unserved and underserved areas.

Emerging applications in IoT connectivity, Earth observation, and space-based services.

Strategic partnerships, government contracts, and public-private collaborations.

Advancements in satellite technology, launch vehicle innovation, and ground infrastructure.

Threats:

Regulatory uncertainties and spectrum allocation issues impacting market growth.

Competition from terrestrial broadband providers, 5G networks, and high-altitude platforms.

Technical risks associated with satellite manufacturing, launch, and operations.

Geopolitical tensions, trade disputes, and international regulations affecting satellite operations and market access.

Understanding these factors through a SWOT analysis helps stakeholders identify strategic priorities, mitigate risks, capitalize on opportunities, and navigate challenges in the Low-Earth Orbit satellite market.

Market Key Trends:

Satellite Constellations: Mega-constellations of LEO satellites are being deployed to provide global broadband internet coverage, creating opportunities for satellite operators, launch providers, and ground infrastructure suppliers.

Satellite-as-a-Service (SAAS): Satellite-as-a-service models are emerging, allowing users to lease satellite capacity, data transmission, and value-added services on-demand, enabling flexible and cost-effective access to satellite resources.

Software-Defined Satellites: Software-defined satellites with reconfigurable payloads, adaptive antennas, and onboard processing capabilities enable dynamic allocation of satellite resources, providing greater flexibility and scalability for satellite operators.

On-Orbit Servicing: On-orbit servicing missions, including satellite refueling, repair, and deorbiting services, are gaining traction, offering opportunities for satellite operators to extend the operational lifespan of satellites and reduce mission costs.

Covid-19 Impact:

The COVID-19 pandemic has impacted the Low-Earth Orbit satellite market in several ways:

Supply Chain Disruptions: Disruptions in the global supply chain have affected satellite manufacturing, launch vehicle production, and ground infrastructure deployment, leading to delays and cost overruns for satellite projects.

Remote Workforce Challenges: Remote work arrangements and travel restrictions have affected satellite operations, mission control, and ground station activities, requiring satellite operators to adapt to remote monitoring and management practices.

Demand Shifts: Changes in consumer behavior, travel restrictions, and economic uncertainty have impacted demand for satellite-based services such as broadband internet, satellite TV, and remote sensing applications, requiring operators to adjust service offerings and pricing models.

Government Support: Government stimulus packages, investment incentives, and regulatory relief measures have supported satellite operators, aerospace companies, and technology providers affected by the pandemic, facilitating continuity of satellite programs and infrastructure projects.

Key Industry Developments:

Satellite Mega-Constellations: Deployment of satellite mega-constellations by companies such as SpaceX, OneWeb, Amazon, and Telesat is reshaping the global satellite market, offering opportunities for global broadband internet coverage and satellite-based services.

Launch Vehicle Innovation: Advancements in launch vehicle technology, including reusable rockets, small satellite launchers, and dedicated rideshare missions, are lowering the cost of access to space and accelerating satellite constellation deployments.

Ground Segment Advancements: Investments in ground segment infrastructure, including satellite ground stations, gateway antennas, and network operations centers, are enhancing satellite communication, data processing, and service delivery capabilities.

Space Policy and Regulation: Policy developments related to spectrum allocation, space traffic management, orbital debris mitigation, and commercial space activities are shaping the regulatory landscape for LEO satellite operators, launch providers, and satellite manufacturers.

Analyst Suggestions:

Diversification Strategies: Satellite operators should diversify their service offerings, target multiple market segments, and explore new applications such as IoT connectivity, Earth observation, and space-based services to mitigate risks and capture growth opportunities.

Cost Optimization: Satellite operators should focus on cost optimization, operational efficiency, and supply chain resilience to reduce mission costs, improve profit margins, and enhance competitiveness in the global satellite market.

Partnerships and Collaborations: Satellite operators should form strategic partnerships, alliances, and consortia with launch providers, ground segment suppliers, technology vendors, and government agencies to leverage complementary capabilities, share resources, and accelerate market penetration.

Future Outlook

Regulatory Compliance: Satellite operators should ensure compliance with international regulations, spectrum allocation guidelines, and space debris mitigation standards to maintain market access, secure government contracts, and mitigate legal and regulatory risks.

Innovation and Differentiation: Satellite operators should invest in innovation, research, and development to differentiate their offerings, enhance satellite performance, and address emerging market needs, positioning themselves as market leaders in the rapidly evolving space industry.

Conclusion:

The Low-Earth Orbit satellite market presents significant opportunities for satellite operators, aerospace companies, technology providers, and government agencies to capitalize on the growing demand for high-speed internet connectivity, remote sensing applications, and space-based services. Mega-constellations of LEO satellites, launch vehicle innovation, ground segment advancements, and regulatory reforms are reshaping the global satellite market landscape, creating opportunities for disruptive innovation, market differentiation, and strategic partnerships. Despite challenges such as technical complexity, regulatory constraints, and competitive pressures, the LEO satellite market is poised for continued growth, driven by advancements in satellite technology, increasing demand for satellite-based services, and evolving market dynamics. By embracing innovation, collaboration, and customer-centric strategies, industry participants can navigate the complexities of the LEO satellite market, unlock new revenue streams, and contribute to the development of a connected, sustainable, and resilient space ecosystem.

What is Low-Earth Orbit Satellite?

Low-Earth Orbit Satellite refers to satellites that orbit the Earth at altitudes typically between one hundred to two thousand kilometers. These satellites are used for various applications, including telecommunications, Earth observation, and scientific research.

What are the key players in the Low-Earth Orbit Satellite Market?

Key players in the Low-Earth Orbit Satellite Market include SpaceX, OneWeb, and Planet Labs, among others. These companies are actively involved in launching and operating satellite constellations to provide global internet coverage and data services.

What are the main drivers of the Low-Earth Orbit Satellite Market?

The main drivers of the Low-Earth Orbit Satellite Market include the increasing demand for high-speed internet access, advancements in satellite technology, and the growing need for real-time data for applications such as agriculture and disaster management.

What challenges does the Low-Earth Orbit Satellite Market face?

The Low-Earth Orbit Satellite Market faces challenges such as space debris management, regulatory hurdles, and the high costs associated with satellite launches and maintenance. These factors can hinder the growth and sustainability of satellite operations.

What opportunities exist in the Low-Earth Orbit Satellite Market?

Opportunities in the Low-Earth Orbit Satellite Market include the potential for new applications in remote sensing, global internet services, and enhanced communication capabilities for underserved regions. The expansion of satellite constellations presents significant growth potential.

What trends are shaping the Low-Earth Orbit Satellite Market?

Trends shaping the Low-Earth Orbit Satellite Market include the rise of mega-constellations, increased collaboration between private and public sectors, and advancements in miniaturization and launch technologies. These trends are driving innovation and competition in the industry.

Leading Companies in the Low-Earth Orbit Satellite Market:

SpaceX

OneWeb

Amazon (Project Kuiper)

Telesat

LeoSat Enterprises

Iridium Communications Inc.

SES S.A.

Intelsat S.A.

Globalstar, Inc.

O3b Networks (a subsidiary of SES S.A.)

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.