444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

Market Overview

The LNG marine engine market has witnessed significant growth in recent years due to the increasing demand for cleaner and more sustainable fuel options in the shipping industry. LNG (liquefied natural gas) has emerged as a viable alternative to traditional marine fuels, such as heavy fuel oil and diesel, as it offers lower emissions and compliance with stringent environmental regulations. This market analysis aims to provide key insights into the LNG marine engine market, including market drivers, restraints, opportunities, regional analysis, competitive landscape, and future outlook.

Meaning

LNG marine engines are specifically designed to run on liquefied natural gas, which is stored in cryogenic tanks onboard ships. These engines use natural gas as a fuel source and produce lower emissions compared to conventional marine engines. The adoption of LNG marine engines has gained momentum as shipowners and operators seek to reduce their carbon footprint and comply with international emission standards.

Executive Summary

The LNG marine engine market is experiencing steady growth, driven by the need for cleaner and more sustainable marine propulsion systems. The market offers significant opportunities for engine manufacturers, shipbuilders, and other industry participants. However, certain challenges and restraints must be addressed to ensure widespread adoption of LNG marine engines.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Market Drivers

Market Restraints

Market Opportunities

Market Dynamics

The LNG marine engine market is driven by a combination of regulatory, environmental, and economic factors. The implementation of IMO regulations and the need for emission compliance are compelling shipowners to explore cleaner fuel options. The availability of LNG infrastructure and the expansion of bunkering facilities are crucial for the widespread adoption of LNG marine engines. Market dynamics also include technological advancements in LNG engine design, improved safety measures, and the development of innovative LNG supply chains.

Regional Analysis

The LNG marine engine market can be segmented into key regions, including North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. Each region has its own set of market drivers, challenges, and opportunities. North America and Europe are leading in terms of LNG infrastructure development, while Asia Pacific is witnessing significant growth due to the presence of major shipbuilding nations and rising environmental concerns.

Competitive Landscape

Leading Companies in the LNG Marine Engine Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Segmentation

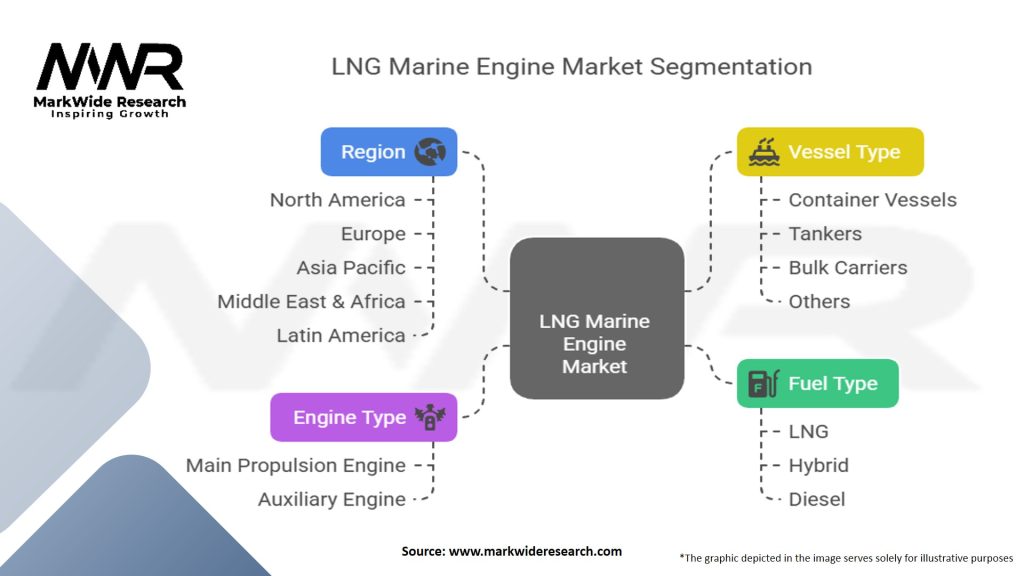

The market can be segmented based on engine type, vessel type, power range, and application. Engine types include low-speed, medium-speed, and high-speed engines. Vessel types comprise container ships, tankers, bulk carriers, ferries, and others. Power range categorizes engines based on their output capacity, while applications encompass propulsion and auxiliary power systems.

Category-wise Insights

Key Benefits for Industry Participants and Stakeholders

SWOT Analysis

Strengths:

Weaknesses:

Opportunities:

Threats:

Market Key Trends

Covid-19 Impact

The COVID-19 pandemic has had a mixed impact on the LNG marine engine market. On one hand, it has disrupted global trade and led to a temporary decline in shipping activities, affecting new vessel orders. On the other hand, the pandemic has highlighted the importance of sustainable and resilient supply chains, driving the need for cleaner fuel options. The long-term impact of the pandemic on the LNG marine engine market will depend on the pace of global economic recovery and the shipping industry’s commitment to environmental sustainability.

Key Industry Developments

Analyst Suggestions

Future Outlook

The LNG marine engine market is expected to witness significant growth in the coming years as the shipping industry increasingly adopts cleaner fuel options. Technological advancements, supportive government policies, and the expansion of LNG infrastructure will drive market expansion. However, challenges such as high initial costs and limited bunkering infrastructure need to be addressed. The market will also see increased integration of digital technologies and the emergence of innovative propulsion systems, paving the way for a sustainable and greener shipping industry.

Conclusion

The LNG marine engine market presents lucrative opportunities for engine manufacturers, shipbuilders, and other industry participants. The demand for cleaner and more sustainable marine propulsion systems, driven by stringent emission regulations and environmental concerns, is fueling market growth. However, challenges such as high costs and limited infrastructure need to be overcome for widespread adoption of LNG marine engines. With continuous innovation, strategic partnerships, and a focus on customer education, the market is poised for significant expansion and a greener future for the shipping industry.

What is an LNG marine engine?

An LNG marine engine is a type of engine that uses liquefied natural gas (LNG) as fuel for marine vessels. These engines are designed to reduce emissions and improve fuel efficiency compared to traditional marine engines that use heavy fuel oil.

What are the key companies in the LNG Marine Engine Market?

Key companies in the LNG Marine Engine Market include Wärtsilä, MAN Energy Solutions, Rolls-Royce, and Caterpillar, among others.

What are the growth factors driving the LNG Marine Engine Market?

The growth of the LNG Marine Engine Market is driven by increasing environmental regulations, the demand for cleaner fuels, and the rising adoption of LNG as a marine fuel due to its lower emissions compared to traditional fuels.

What challenges does the LNG Marine Engine Market face?

Challenges in the LNG Marine Engine Market include the high initial investment costs for LNG infrastructure, limited availability of LNG bunkering facilities, and the need for technological advancements to improve engine performance.

What opportunities exist in the LNG Marine Engine Market?

Opportunities in the LNG Marine Engine Market include the expansion of LNG bunkering infrastructure, increasing investments in cleaner shipping technologies, and the potential for retrofitting existing vessels with LNG engines.

What trends are shaping the LNG Marine Engine Market?

Trends in the LNG Marine Engine Market include the growing focus on sustainability, advancements in dual-fuel engine technology, and the increasing collaboration between shipping companies and fuel suppliers to promote LNG adoption.

LNG Marine Engine Market

| Segmentation | Details |

|---|---|

| By Fuel Type | LNG, Hybrid, Diesel |

| By Engine Type | Main Propulsion Engine, Auxiliary Engine |

| By Vessel Type | Container Vessels, Tankers, Bulk Carriers, Others |

| By Region | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading Companies in the LNG Marine Engine Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

North America

o US

o Canada

o Mexico

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA