444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Latin America neo banking services market represents a transformative shift in the regional financial landscape, driven by rapid digital adoption and evolving consumer preferences. Neo banks, also known as digital-only banks or challenger banks, are revolutionizing traditional banking by offering comprehensive financial services through mobile applications and digital platforms without physical branch networks. The market demonstrates exceptional growth momentum with a projected compound annual growth rate of 18.5% CAGR through the forecast period.

Digital transformation initiatives across Latin American countries have accelerated the adoption of neo banking solutions, particularly in Brazil, Mexico, Argentina, and Colombia. These markets showcase significant penetration rates with mobile banking adoption reaching 72% of the adult population in key metropolitan areas. The region’s young demographic profile, with 65% of the population under 35 years old, creates favorable conditions for digital banking acceptance and usage.

Regulatory frameworks across Latin America have evolved to accommodate innovative financial technologies, enabling neo banks to operate under specific licensing structures. Countries like Brazil and Mexico have implemented regulatory sandboxes that facilitate fintech innovation while maintaining consumer protection standards. This regulatory support has contributed to the establishment of over 150 active neo banking platforms across the region.

The Latin America neo banking services market refers to the comprehensive ecosystem of digital-first financial institutions that provide banking services exclusively through mobile applications and online platforms without maintaining traditional physical branch networks. Neo banks leverage advanced technologies including artificial intelligence, machine learning, and cloud computing to deliver personalized financial solutions, streamlined account opening processes, and enhanced user experiences.

Core characteristics of neo banking services include fully digital onboarding processes, real-time transaction notifications, advanced spending analytics, and integrated financial management tools. These platforms typically offer basic banking services such as checking and savings accounts, payment processing, money transfers, and increasingly sophisticated features like investment products, lending solutions, and insurance services.

Market participants range from pure-play digital banks to hybrid models that combine digital-first approaches with selective physical touchpoints. The ecosystem encompasses various business models including business-to-consumer (B2C) platforms, business-to-business (B2B) banking solutions, and specialized niche services targeting specific demographic segments or industry verticals.

Market dynamics in the Latin America neo banking services sector reflect a paradigm shift toward digital financial inclusion and enhanced customer experiences. The region’s traditional banking infrastructure gaps have created substantial opportunities for neo banks to address underserved populations and provide accessible financial services. Key growth drivers include increasing smartphone penetration, improving internet connectivity, and growing consumer comfort with digital financial transactions.

Competitive landscape features both regional players and international neo banking platforms expanding into Latin American markets. Brazilian neo banks lead market development, followed by significant growth in Mexico and Colombia. Investment activity remains robust with venture capital and private equity firms recognizing the sector’s potential, contributing to 45% year-over-year growth in funding for neo banking startups.

Technological innovation drives differentiation among market participants, with advanced features including biometric authentication, AI-powered financial advice, and integrated cryptocurrency services. The market demonstrates strong momentum toward comprehensive financial ecosystems that extend beyond traditional banking into payments, lending, investments, and insurance products.

Strategic insights reveal several critical factors shaping the Latin America neo banking services market evolution:

Primary growth drivers propelling the Latin America neo banking services market include accelerating digital transformation across the region. Smartphone adoption rates have reached critical mass with over 80% penetration in urban areas, creating the necessary infrastructure for mobile banking services. Consumers increasingly prefer digital channels for financial transactions, driven by convenience, accessibility, and enhanced user experiences.

Financial inclusion initiatives represent another significant driver as neo banks address traditional banking sector limitations in serving underbanked populations. These platforms offer simplified account opening processes, lower minimum balance requirements, and accessible financial products that appeal to previously excluded demographic segments. Government support for financial digitization further accelerates market development through favorable regulatory policies and digital payment infrastructure investments.

Generational preferences strongly favor digital banking solutions, with millennials and Generation Z consumers demonstrating high comfort levels with mobile financial services. This demographic shift creates sustained demand for innovative banking experiences that prioritize user interface design, real-time functionality, and integrated financial management tools. COVID-19 pandemic impacts have permanently altered consumer behavior, accelerating the transition from traditional banking channels to digital platforms.

Regulatory challenges present significant constraints for neo banking market expansion across Latin America. Complex compliance requirements, varying regulatory frameworks between countries, and evolving licensing structures create operational complexities for market participants. Traditional banking sector resistance and established market incumbents leverage regulatory influence to maintain competitive advantages and limit neo banking market access.

Infrastructure limitations in certain regions restrict market penetration, particularly in rural areas with limited internet connectivity and lower smartphone adoption rates. Cybersecurity concerns among consumers create adoption barriers, especially for older demographic segments who remain skeptical of digital financial services. Trust-building remains a critical challenge for neo banks seeking to establish credibility in markets dominated by established financial institutions.

Economic volatility across Latin American markets impacts consumer spending patterns and financial service demand. Currency fluctuations, inflation pressures, and political instability create challenging operating environments for neo banking platforms. Funding constraints may limit growth opportunities as venture capital markets become more selective and traditional funding sources remain cautious about fintech investments.

Expansion opportunities in the Latin America neo banking services market center on addressing substantial unbanked populations across the region. Financial inclusion initiatives supported by government programs and international development organizations create favorable conditions for neo banking growth. These platforms can leverage technology to provide accessible financial services to previously underserved communities through simplified digital onboarding and mobile-first service delivery.

Corporate banking solutions represent significant untapped potential as small and medium enterprises (SMEs) seek digital financial services that traditional banks often overlook. Neo banks can develop specialized B2B platforms offering streamlined business account management, integrated payment processing, and automated financial reporting tools. Cross-border payment services present additional opportunities given the region’s substantial remittance flows and international trade activities.

Partnership strategies with established financial institutions, telecommunications companies, and retail networks can accelerate market penetration and service distribution. Embedded finance solutions integrated into e-commerce platforms, ride-sharing applications, and digital marketplaces create new revenue streams and customer acquisition channels. The growing cryptocurrency adoption in Latin America offers opportunities for neo banks to integrate digital asset services and capture emerging market segments.

Competitive dynamics in the Latin America neo banking services market reflect intense competition between pure-play digital banks, traditional bank digital initiatives, and international platform expansions. Market consolidation trends are emerging as successful neo banks acquire smaller competitors and expand their service portfolios through strategic partnerships. Customer acquisition costs remain elevated as platforms compete for market share through aggressive marketing campaigns and promotional offerings.

Technology evolution drives continuous platform enhancement with artificial intelligence, machine learning, and advanced analytics becoming standard features. User experience optimization remains a critical differentiator as consumers expect intuitive interfaces, fast transaction processing, and comprehensive financial management tools. Neo banks invest heavily in mobile application development and digital infrastructure to maintain competitive advantages.

Regulatory evolution continues shaping market dynamics as governments balance innovation promotion with consumer protection requirements. Open banking initiatives in several Latin American countries create opportunities for neo banks to integrate with traditional financial institutions and access broader financial data ecosystems. According to MarkWide Research analysis, regulatory clarity improvements have contributed to 35% growth in neo banking license applications across major regional markets.

Comprehensive research methodology employed for analyzing the Latin America neo banking services market incorporates multiple data collection approaches and analytical frameworks. Primary research activities include structured interviews with industry executives, regulatory officials, and technology providers across key regional markets. Survey research captures consumer preferences, adoption patterns, and satisfaction levels with existing neo banking services.

Secondary research components encompass analysis of regulatory filings, financial reports, industry publications, and market intelligence databases. Quantitative analysis utilizes statistical modeling techniques to project market trends, growth trajectories, and competitive positioning dynamics. Data validation processes ensure accuracy and reliability through cross-referencing multiple information sources and expert verification.

Market segmentation analysis employs demographic, geographic, and behavioral criteria to identify distinct customer segments and service categories. Competitive intelligence gathering includes platform feature analysis, pricing strategy evaluation, and market positioning assessment. The methodology incorporates scenario planning techniques to evaluate potential market developments under various economic and regulatory conditions.

Brazil dominates the Latin America neo banking services market with the most mature ecosystem and highest adoption rates. The country’s progressive regulatory framework, large unbanked population, and advanced digital infrastructure create optimal conditions for neo banking growth. Brazilian neo banks have achieved significant market penetration with over 25 million active users across major platforms, representing substantial market share gains from traditional banking institutions.

Mexico represents the second-largest market opportunity with rapid growth in digital banking adoption and supportive regulatory developments. The country’s large remittance market and growing e-commerce sector provide favorable conditions for neo banking expansion. Colombian markets demonstrate strong growth potential driven by government financial inclusion initiatives and increasing smartphone penetration rates reaching 78% of the adult population.

Argentina and Chile show promising development trajectories despite economic challenges, with neo banks focusing on inflation-resistant financial products and cross-border payment solutions. Smaller regional markets including Peru, Uruguay, and Costa Rica present niche opportunities for specialized neo banking services. MWR data indicates that regional market distribution shows Brazil commanding 45% market share, followed by Mexico at 28%, and other markets collectively representing 27% of regional activity.

Market leadership in the Latin America neo banking services sector features a diverse mix of regional champions and international platform expansions. Key market participants include:

Competitive strategies focus on customer acquisition through superior user experiences, competitive pricing, and comprehensive service portfolios. Platform differentiation emphasizes advanced technology features, personalized financial insights, and integrated lifestyle services that extend beyond traditional banking functions.

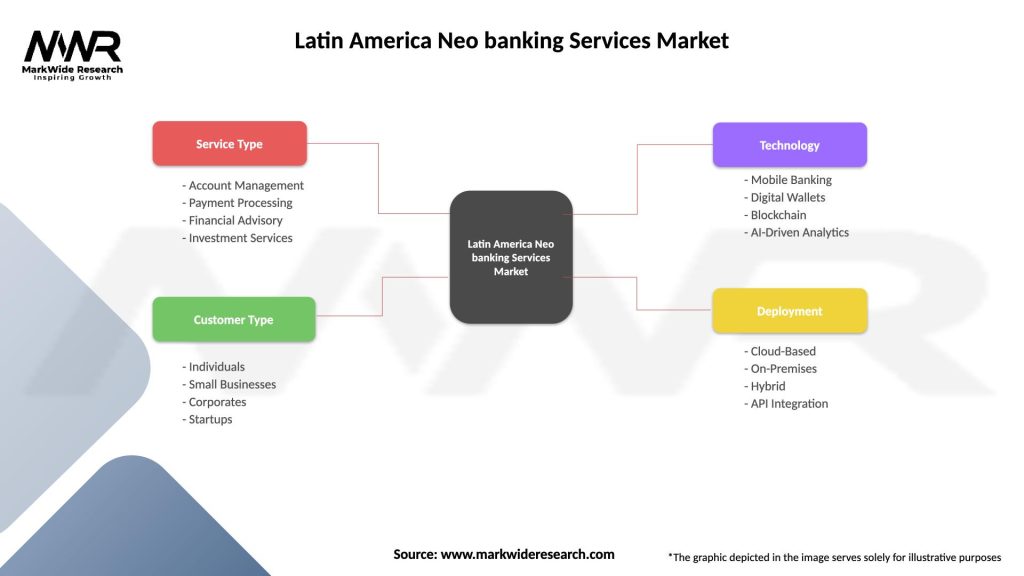

Market segmentation analysis reveals distinct categories based on service offerings, target demographics, and business models:

By Service Type:

By Target Segment:

Consumer banking categories demonstrate varying growth patterns and adoption rates across the Latin America neo banking services market. Basic banking services including checking accounts and payment processing represent the largest segment by user volume, with simplified onboarding processes and fee-free structures driving rapid adoption among price-sensitive consumers.

Lending solutions show substantial growth potential as neo banks leverage alternative credit scoring methodologies and real-time financial data analysis. Personal loan products tailored to gig economy workers and informal sector participants address significant market gaps left by traditional banking institutions. Credit card offerings emphasize transparency, competitive rates, and integrated financial management tools.

Investment services represent emerging high-value segments as neo banks expand into wealth management and trading platforms. Micro-investment features and automated savings programs appeal to younger demographics seeking accessible entry points into financial markets. Business banking solutions demonstrate strong growth momentum with SME-focused platforms offering integrated accounting, payment processing, and cash flow management tools.

Financial institutions participating in the Latin America neo banking services market gain access to previously underserved customer segments and new revenue streams. Cost advantages from digital-first operations enable competitive pricing strategies and improved profit margins compared to traditional branch-based banking models. Technology platforms provide comprehensive customer data insights that enhance risk management, product development, and personalized service delivery.

Consumers benefit from enhanced accessibility, convenience, and transparency in financial services. 24/7 availability through mobile applications eliminates traditional banking hour limitations and geographic constraints. Lower fees, simplified processes, and real-time financial insights empower consumers to make informed financial decisions and improve their overall financial health.

Regulatory authorities achieve financial inclusion objectives through neo banking platform expansion into underbanked populations. Digital transaction monitoring capabilities enhance anti-money laundering compliance and financial crime prevention. Government initiatives promoting cashless economies benefit from neo banking infrastructure development and digital payment system adoption.

Technology providers and fintech companies find substantial opportunities in supporting neo banking platform development through cloud infrastructure, security solutions, and specialized financial software. Partnership ecosystems create mutual benefits through integrated service offerings and expanded market reach.

Strengths:

Weaknesses:

Opportunities:

Threats:

Artificial intelligence integration represents a dominant trend shaping the Latin America neo banking services market evolution. AI-powered features including chatbots, personalized financial advice, and predictive analytics enhance customer experiences while reducing operational costs. Machine learning algorithms improve fraud detection, credit scoring accuracy, and risk management capabilities across neo banking platforms.

Super app development trends show neo banks expanding beyond traditional banking services into comprehensive lifestyle platforms. Integrated ecosystems combine financial services with e-commerce, transportation, food delivery, and entertainment options. This approach increases customer engagement, reduces acquisition costs, and creates multiple revenue streams through platform monetization strategies.

Cryptocurrency integration emerges as a significant trend with neo banks offering digital asset trading, storage, and payment capabilities. Blockchain technology adoption enables cross-border payments, smart contract functionality, and enhanced security features. MarkWide Research findings indicate that 42% of neo banking platforms plan to integrate cryptocurrency services within the next two years.

Embedded finance solutions represent growing trends where neo banking services integrate directly into non-financial platforms and applications. API-first architectures enable seamless integration with e-commerce sites, gig economy platforms, and digital marketplaces, creating new customer touchpoints and acquisition channels.

Recent industry developments highlight accelerating innovation and market expansion across the Latin America neo banking services sector. Regulatory milestone achievements include Brazil’s Central Bank approval of additional digital banking licenses and Mexico’s implementation of comprehensive fintech regulations that clarify operational requirements for neo banking platforms.

Strategic partnerships between neo banks and established financial institutions create hybrid service models combining digital innovation with traditional banking infrastructure. Technology collaborations with cloud computing providers, cybersecurity firms, and artificial intelligence companies enhance platform capabilities and operational scalability.

Investment activities continue demonstrating strong market confidence with several neo banking platforms securing substantial funding rounds for regional expansion and product development initiatives. Acquisition trends show market consolidation as successful platforms acquire complementary fintech companies and smaller competitors to expand service portfolios.

International expansion activities include established neo banks from developed markets entering Latin American countries through local partnerships and regulatory compliance initiatives. Cross-border collaboration agreements facilitate knowledge transfer and technology sharing between regional and international neo banking platforms.

Strategic recommendations for neo banking market participants emphasize the importance of sustainable customer acquisition strategies that balance growth with profitability. Focus areas should include developing comprehensive financial ecosystems that increase customer lifetime value and reduce churn rates through integrated service offerings and superior user experiences.

Regulatory compliance remains critical for long-term success, requiring neo banks to invest in robust compliance infrastructure and maintain proactive relationships with regulatory authorities. Risk management capabilities must evolve to address cybersecurity threats, fraud prevention, and credit risk assessment in digital-first operating environments.

Technology investment priorities should emphasize artificial intelligence, machine learning, and advanced analytics capabilities that enable personalized services and operational efficiency improvements. Partnership strategies with traditional financial institutions, technology providers, and distribution partners can accelerate market penetration and service expansion.

Market differentiation requires neo banks to identify specific customer segments and develop tailored solutions that address unique needs and preferences. Financial inclusion initiatives targeting underbanked populations present significant opportunities for sustainable growth and positive social impact.

Long-term prospects for the Latin America neo banking services market remain highly positive, driven by continued digital transformation, demographic trends, and evolving consumer preferences. Market maturation is expected to result in consolidation among smaller players while successful platforms expand their geographic reach and service portfolios.

Technology advancement will continue driving innovation with emerging technologies including blockchain, quantum computing, and advanced biometrics enhancing security, efficiency, and user experiences. Regulatory frameworks are anticipated to become more standardized across the region, facilitating cross-border operations and reducing compliance complexities.

Service evolution trends indicate neo banks will increasingly function as comprehensive financial ecosystems rather than traditional banking alternatives. Integration capabilities with emerging technologies and lifestyle services will determine competitive positioning and market success. The market is projected to maintain robust growth momentum with sustained CAGR performance exceeding 15% annually through the next decade.

Competitive landscape evolution will likely feature increased collaboration between neo banks and traditional financial institutions, creating hybrid models that combine digital innovation with established market presence. International expansion opportunities will continue attracting global neo banking platforms seeking growth in emerging markets with favorable demographic and economic conditions.

The Latin America neo banking services market represents a transformative force reshaping the regional financial services landscape through digital innovation, enhanced accessibility, and customer-centric service delivery. Market dynamics reflect strong growth momentum driven by favorable demographic trends, regulatory support, and increasing consumer acceptance of digital financial solutions.

Key success factors for market participants include developing comprehensive technology platforms, maintaining regulatory compliance, and creating sustainable competitive advantages through superior user experiences and integrated service ecosystems. Financial inclusion opportunities remain substantial as neo banks continue addressing underserved populations across the region.

Future market development will be characterized by continued innovation, strategic partnerships, and geographic expansion as successful platforms leverage their capabilities to capture emerging opportunities. The Latin America neo banking services market is positioned for sustained growth, offering significant value creation potential for stakeholders while advancing financial inclusion and digital transformation objectives across the region.

What is Neo banking Services?

Neo banking Services refer to digital-only banking solutions that operate without traditional physical branches. These services typically include online account management, payment processing, and financial planning tools, catering to tech-savvy consumers seeking convenience and efficiency.

What are the key players in the Latin America Neo banking Services Market?

Key players in the Latin America Neo banking Services Market include Nubank, Banco Inter, and C6 Bank, which offer a range of digital banking services such as personal loans, credit cards, and investment options, among others.

What are the growth factors driving the Latin America Neo banking Services Market?

The growth of the Latin America Neo banking Services Market is driven by increasing smartphone penetration, a growing preference for digital transactions, and the demand for financial inclusion among unbanked populations.

What challenges does the Latin America Neo banking Services Market face?

Challenges in the Latin America Neo banking Services Market include regulatory hurdles, cybersecurity threats, and competition from established banks that are enhancing their digital offerings.

What opportunities exist in the Latin America Neo banking Services Market?

Opportunities in the Latin America Neo banking Services Market include the potential for partnerships with fintech companies, the expansion of services to underserved regions, and the integration of advanced technologies like AI for personalized banking experiences.

What trends are shaping the Latin America Neo banking Services Market?

Trends shaping the Latin America Neo banking Services Market include the rise of open banking, increased focus on customer experience, and the adoption of blockchain technology for secure transactions.

Latin America Neo banking Services Market

| Segmentation Details | Description |

|---|---|

| Service Type | Account Management, Payment Processing, Financial Advisory, Investment Services |

| Customer Type | Individuals, Small Businesses, Corporates, Startups |

| Technology | Mobile Banking, Digital Wallets, Blockchain, AI-Driven Analytics |

| Deployment | Cloud-Based, On-Premises, Hybrid, API Integration |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Latin America Neo banking Services Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.