The Latin America home mortgage finance market is a rapidly growing sector that plays a significant role in the region’s overall economic development. This market encompasses various financial institutions, including banks, credit unions, and mortgage lenders, that provide funding for individuals and families to purchase residential properties. The demand for mortgage financing in Latin America has been steadily increasing due to factors such as urbanization, rising incomes, and favorable government policies aimed at promoting homeownership. In this comprehensive market analysis, we will delve into the meaning of home mortgage finance, provide key insights, analyze market drivers, restraints, and opportunities, explore the market dynamics, conduct a regional analysis, assess the competitive landscape, highlight segmentation and category-wise insights, discuss the key benefits for industry participants and stakeholders, perform a SWOT analysis, evaluate the impact of Covid-19, examine key industry developments, present analyst suggestions, discuss the future outlook, and conclude with a summary of findings.

Meaning

Home mortgage finance refers to the financial products and services that enable individuals to purchase residential properties by borrowing funds from lending institutions. These funds are typically secured by the property itself, which serves as collateral for the mortgage loan. Home mortgage finance provides potential homeowners with the means to acquire a property without having to pay the full purchase price upfront. Instead, borrowers repay the loan amount, along with interest, through regular installments over an agreed-upon term, usually ranging from 15 to 30 years. The interest rates and terms of mortgage loans can vary based on factors such as the borrower’s creditworthiness, prevailing market conditions, and the specific mortgage product chosen. Home mortgage finance plays a crucial role in facilitating homeownership, promoting economic growth, and building wealth for individuals and families.

Executive Summary

The Latin America home mortgage finance market has experienced significant growth in recent years, driven by various factors such as urbanization, increasing disposable incomes, and supportive government policies. The market has witnessed a rising demand for mortgage loans, as more people aspire to own their homes and take advantage of favorable interest rates. This executive summary provides a concise overview of the key market insights, drivers, restraints, and opportunities, highlighting the dynamic nature of the market. Additionally, it presents a regional analysis, competitive landscape, segmentation, category-wise insights, and the key benefits for industry participants and stakeholders. The summary also includes a SWOT analysis, a discussion on the impact of Covid-19, key industry developments, analyst suggestions, and a glimpse into the future outlook of the Latin America home mortgage finance market.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

The Latin America home mortgage finance market is experiencing robust growth, driven by increasing urbanization and rising incomes, which are fueling the demand for residential properties.

Supportive government policies, such as mortgage subsidies, tax incentives, and regulatory reforms, are encouraging homeownership and facilitating access to mortgage financing.

The market is witnessing a shift towards more flexible mortgage products, including adjustable-rate mortgages and longer loan terms, to accommodate the diverse needs of borrowers.

Technology and digitalization are playing a crucial role in streamlining mortgage processes, enhancing customer experience, and improving operational efficiency for lenders.

Non-bank financial institutions, including mortgage lenders and fintech companies, are gaining prominence in the market, offering innovative mortgage solutions and expanding access to financing for underserved populations.

Risk management and regulatory compliance remain key challenges for mortgage lenders, requiring constant adaptation to changing regulations and ensuring responsible lending practices.

Sustainable and energy-efficient homes are gaining traction in the market, driven by environmental concerns and government initiatives promoting green housing.

Collaborations between mortgage lenders, real estate developers, and construction companies are becoming more common, facilitating integrated solutions and promoting the growth of the housing market.

Market Drivers

The Latin America home mortgage finance market is propelled by several key drivers that contribute to its growth and expansion:

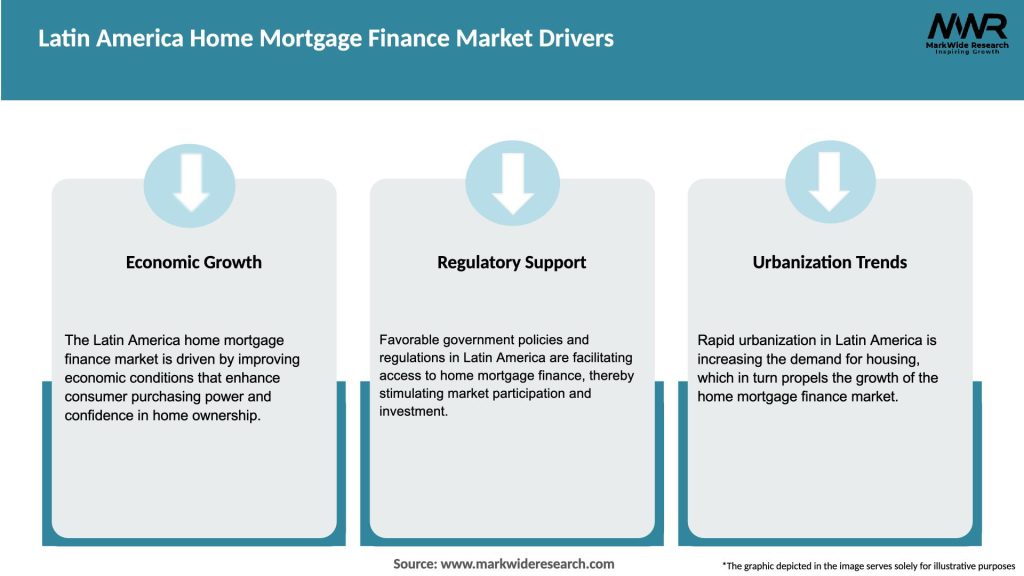

Urbanization and population growth: The rapid urbanization in Latin America has led to an increased demand for housing, driving the need for mortgage finance to facilitate property purchases.

Rising incomes and expanding middle class: As disposable incomes rise and the middle class expands, more individuals and families are aspiring to own their homes, boosting the demand for mortgage loans.

Supportive government policies: Governments across the region are implementing policies and initiatives to promote homeownership, including mortgage subsidies, tax incentives, and regulatory reforms that facilitate access to mortgage financing.

Low interest rates: Favorable interest rate environments incentivize borrowing, making mortgage financing more affordable and attractive to potential homeowners.

Growing financial inclusion: Efforts to enhance financial inclusion and expand access to formal financial services have resulted in more individuals gaining eligibility for mortgage loans, contributing to market growth.

Technological advancements: The adoption of technology and digitalization in the mortgage industry has improved the efficiency of loan origination, underwriting, and servicing processes, enhancing the overall customer experience.

Increasing awareness and demand for sustainable homes: The rising focus on environmental sustainability has fueled demand for energy-efficient homes, leading to the development of mortgage products that incentivize sustainable housing initiatives.

Market Restraints

While the Latin America home mortgage finance market shows promising growth prospects, it also faces certain challenges and restraints:

Economic volatility: Fluctuations in the macroeconomic environment, such as currency devaluations and inflation, can impact interest rates, borrower affordability, and creditworthiness, affecting the stability of the mortgage market.

Limited access to affordable housing: Despite the growing demand for housing, the availability of affordable housing units remains a challenge in many Latin American countries, affecting the overall market growth.

Insufficient credit history and informal employment: Limited credit histories and a significant portion of the population engaged in informal employment can hinder mortgage eligibility for potential borrowers, leading to lower market penetration.

Regulatory constraints and risk management: Compliance with regulatory requirements, including stringent lending standards and risk management practices, can pose challenges for mortgage lenders, increasing operational costs and limiting lending capabilities.

Lack of financial literacy: Limited financial literacy and understanding of mortgage products and processes among potential borrowers can impede market growth, hindering individuals from taking advantage of available financing options.

Vulnerability to external shocks: The Latin America home mortgage finance market can be sensitive to external factors such as global economic downturns, political instability, and natural disasters, impacting borrower confidence and creditworthiness.

Unequal income distribution: Income inequality in the region can create disparities in access to mortgage financing, as a significant portion of the population may struggle to meet the eligibility criteria for mortgage loans.

Market Opportunities

The Latin America home mortgage finance market presents several opportunities that can drive its growth and development:

Addressing the affordable housing gap: Closing the gap in affordable housing availability presents a significant opportunity for mortgage lenders to cater to the underserved market segment, partnering with developers and governments to create accessible financing solutions.

Expanding the product portfolio: Introducing innovative mortgage products, such as shared-equity mortgages, rent-to-own schemes, and micro-mortgages, can tap into new market segments and cater to the specific needs of different borrower profiles.

Enhancing financial literacy: Investing in financial education initiatives to improve the understanding of mortgage products, creditworthiness, and personal finance management can empower individuals to make informed decisions and increase market participation.

Leveraging technology for efficiency: Continual investment in technology and digitalization can streamline mortgage processes, reduce operational costs, and enhance the overall customer experience, attracting tech-savvy borrowers.

Collaborations with fintech companies: Partnering with fintech companies and leveraging their technological capabilities can enable traditional mortgage lenders to offer more accessible and streamlined digital mortgage solutions, reaching a wider customer base.

Green financing and sustainability: Capitalizing on the growing interest in sustainable homes, mortgage lenders can develop green mortgage products that incentivize energy-efficient housing initiatives and provide preferential terms for environmentally conscious borrowers.

Targeting underserved populations: Implementing strategies to expand access to mortgage financing for traditionally underserved populations, such as low-income earners, self-employed individuals, and rural communities, can unlock new market segments and foster inclusive growth.

Market Dynamics

The Latin America home mortgage finance market is characterized by dynamic interactions between various stakeholders, market forces, and regulatory frameworks. Understanding the market dynamics is crucial for industry participants and stakeholders to navigate the evolving landscape effectively.

Demand-supply dynamics: The market dynamics are influenced by the interplay between the demand for mortgage financing and the availability of funds from lending institutions. Changes in borrower preferences, economic conditions, and interest rates can affect the equilibrium between supply and demand, impacting lending volumes and market competitiveness.

Regulatory environment: Regulatory frameworks and policies governing mortgage lending practices, interest rates, and borrower eligibility criteria have a significant impact on market dynamics. Changes in regulations can impact the lending landscape, credit availability, and risk management practices.

Competitive landscape: The Latin America home mortgage finance market is highly competitive, with a mix of traditional banks, credit unions, mortgage lenders, and emerging fintech companies vying for market share. The competitive landscape is shaped by factors such as product offerings, interest rates, customer service, and technological capabilities.

Market segmentation: The market is segmented based on borrower profiles, loan types, interest rates, and geographical regions. Understanding the specific needs and preferences of different borrower segments is crucial for lenders to tailor their products and services effectively.

Technological advancements: Technology is reshaping the mortgage industry, driving operational efficiency, improving customer experience, and expanding access to financing. Embracing technological advancements, such as automation, artificial intelligence, and digital platforms, can provide a competitive edge and influence market dynamics.

Economic factors: The market dynamics are influenced by macroeconomic factors, including GDP growth rates, inflation, interest rates, and currency exchange rates. Changes in these economic variables can impact borrower affordability, interest rate levels, and the overall demand for mortgage financing.

Consumer behavior and preferences: Evolving consumer preferences, such as a preference for digital mortgage processes, sustainability considerations, and demand for customized mortgage products, shape market dynamics and drive product innovation.

Regional Analysis

The Latin America home mortgage finance market exhibits regional variations in terms of market size, growth rates, regulatory frameworks, and cultural factors. A regional analysis provides valuable insights into the specific dynamics and opportunities in different parts of the region.

North America: The North American region, comprising countries such as Mexico, the United States, and Canada, represents a mature and highly developed mortgage market. The market is characterized by a diverse range of mortgage products, sophisticated lending practices, and well-established regulatory frameworks.

Central America: Central American countries, including Costa Rica, Panama, and Guatemala, have seen significant growth in their mortgage markets in recent years. The market is driven by urbanization, increasing disposable incomes, and government initiatives to promote homeownership.

Caribbean: The Caribbean region offers a unique mortgage market landscape, with varying levels of development and market sophistication across different countries. Tourism-driven economies and foreign investment play a significant role in the housing markets of countries like the Dominican Republic, Jamaica, and the Bahamas.

South America: South American countries, such as Brazil, Argentina, and Chile, have witnessed substantial growth in their mortgage markets, driven by urbanization, rising incomes, and favorable government policies. The market presents both opportunities and challenges due to economic volatility, regulatory complexities, and varying levels of market development across countries.

Andean region: The Andean region, including countries like Peru, Colombia, and Ecuador, has experienced rapid growth in its mortgage markets. Increasing urbanization, a growing middle class, and supportive government policies have fueled market expansion.

Southern Cone: The Southern Cone region, encompassing countries like Argentina, Uruguay, and Chile, has a well-developed mortgage market with robust demand. These markets are driven by urbanization, rising incomes, and a cultural preference for homeownership.

Other regions: Other countries and territories in Latin America, such as Bolivia, Paraguay, and Puerto Rico, exhibit unique market dynamics and opportunities, influenced by factors such as economic conditions, government policies, and cultural norms.

Competitive Landscape

Leading Companies in the Latin America Home Mortgage Finance Market:

Banco do Brasil

Caixa Econômica Federal

Banco Santander Brasil

Itaú Unibanco Holding S.A.

Banorte

BBVA Bancomer

Banco de Crédito del Perú (BCP)

Banco de Chile

Banco Macro

Banco Galicia

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Segmentation

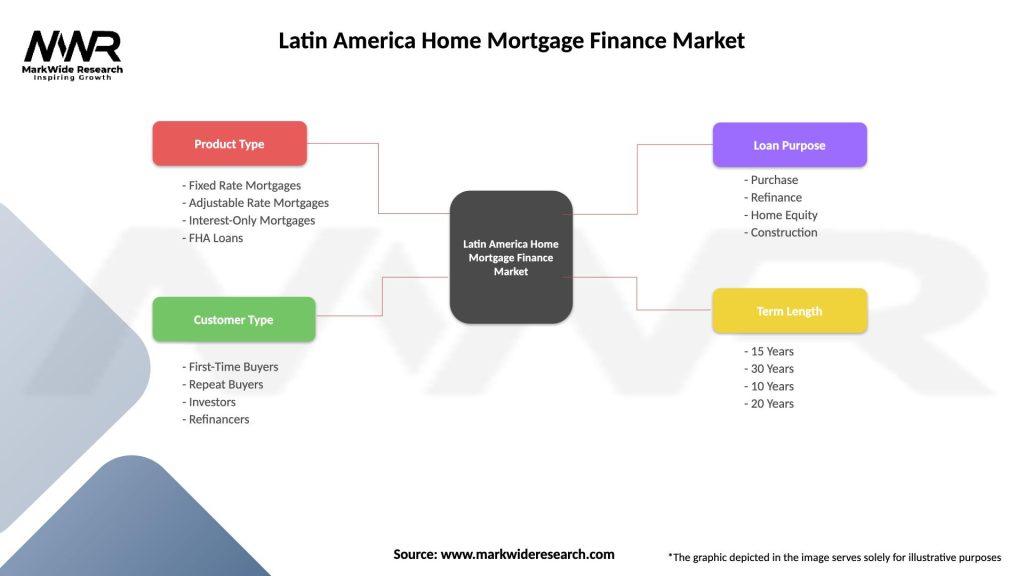

The Latin America home mortgage finance market can be segmented based on various factors, including borrower profiles, loan types, interest rate structures, and geographical regions. Understanding the different segments of the market helps lenders tailor their products and services to meet the specific needs and preferences of borrowers.

Borrower profiles: a. First-time homebuyers: This segment includes individuals or families purchasing their first residential property. They often have specific financing needs and may benefit from government incentives or programs aimed at promoting homeownership. b. Upgraders: This segment comprises borrowers who are looking to upgrade their current homes or move to larger properties. They may have built equity in their existing homes and require financing to facilitate the purchase of a new property. c. Investors: Investors in residential real estate form a distinct segment, seeking financing options to purchase properties for rental income or capital appreciation. Their financing needs may differ from those of owner-occupiers. d. Self-employed individuals: Self-employed borrowers face unique challenges in obtaining mortgage financing due to irregular income documentation. Lenders may offer specialized loan products tailored to the needs of self-employed individuals. e. Low-income earners: Providing mortgage financing to low-income earners is an important segment for inclusive growth. Specialized mortgage products, government subsidies, and down payment assistance programs cater to this segment’s needs.

Loan types: a. Fixed-rate mortgages: This loan type offers borrowers a fixed interest rate throughout the loan term, providing stability and predictability in monthly mortgage payments. b. Adjustable-rate mortgages (ARMs): ARMs have variable interest rates that adjust periodically based on market conditions. Borrowers may opt for ARMs to take advantage of lower initial interest rates or if they anticipate future interest rate decreases. c. Government-backed mortgages: Governments often provide mortgage programs that are insured or guaranteed by government institutions, such as the Federal Housing Administration (FHA) in the United States or the Brazilian National Housing Bank (Caixa Econômica Federal) in Brazil. d. Jumbo mortgages: Jumbo mortgages are loans that exceed the conventional loan limits set by government-sponsored entities. This loan type caters to borrowers purchasing high-value properties.

Interest rate structures: a. Fixed interest rate: Borrowers opt for a fixed interest rate when they seek stability and want to lock in a specific interest rate for the entire loan term. b. Variable interest rate: Borrowers may choose a variable interest rate if they are comfortable with market fluctuations and anticipate interest rate decreases in the future. c. Hybrid interest rate: Hybrid interest rate structures offer a combination of fixed and variable rates. For example, a 5/1 ARM loan has a fixed interest rate for the first five years, followed by adjustable rates for the remaining loan term.

Geographical regions: a. North America: This segment focuses on the mortgage finance market in North American countries such as Mexico, the United States, and Canada. b. Central America: Central American countries like Costa Rica, Panama, and Guatemala form a distinct geographical segment with unique market characteristics. c. Caribbean: The Caribbean region, including countries like the Dominican Republic, Jamaica, and the Bahamas, represents a distinct market segment with its own dynamics. d. South America: South American countries, including Brazil, Argentina, and Chile, exhibit specific market trends and opportunities. e. Andean region: The Andean region, comprising countries like Peru, Colombia, and Ecuador, has its own distinct market segment within Latin America. f. Southern Cone: Countries like Argentina, Uruguay, and Chile, located in the Southern Cone, form a separate segment characterized by specific market dynamics.

Category-wise Insights

Market size and growth: The Latin America home mortgage finance market has experienced significant growth in recent years, with a steady increase in the volume of mortgage loans and a growing number of borrowers entering the market.

Market penetration: Despite the market’s growth, mortgage penetration levels in Latin America remain relatively low compared to more developed regions. There is ample room for expansion and increasing market penetration.

Government policies and incentives: Governments in Latin America have implemented various policies and incentives to promote homeownership and facilitate access to mortgage financing. These include mortgage subsidies, tax incentives, and regulatory reforms aimed at fostering a vibrant housing market.

Market concentration: The market exhibits varying degrees of concentration across different countries and regions. In some countries, a few major banks dominate the mortgage market, while other countries have a more fragmented landscape with numerous lenders competing for market share.

Mortgage products and features: The market offers a range of mortgage products and features to cater to different borrower needs. These include fixed-rate mortgages, adjustable-rate mortgages, government-backed mortgages, and specialized products for low-income earners and self-employed individuals.

Digitalization and technology adoption: The mortgage industry in Latin America is undergoing a digital transformation, with increased adoption of technology to streamline processes, enhance customer experience, and improve operational efficiency. Digital platforms, online applications, and automated underwriting systems are becoming more prevalent.

Risk management and underwriting practices: Mortgage lenders employ various risk management and underwriting practices to assess borrower creditworthiness and mitigate default risk. These practices include thorough income verification, credit checks, and property appraisals.

Secondary mortgage market: The development of a secondary mortgage market, where mortgage loans are bundled and sold to investors, can improve liquidity in the market and provide additional funding sources for lenders.

Regulatory environment: The mortgage market operates within a regulatory framework that governs lending practices, interest rates, disclosure requirements, and consumer protection. Compliance with regulatory standards is essential for market participants to ensure fair and responsible lending practices.

Key Benefits for Industry Participants and Stakeholders

Lenders and financial institutions: a. Increased loan volumes and market share b. Diversification of loan portfolios c. Opportunities for cross-selling other financial products d. Building long-term customer relationships e. Expansion into underserved market segments f. Access to government incentives and support programs

Borrowers: a. Access to affordable mortgage financing b. Increased homeownership opportunities c. Favorable interest rates and terms d. Tailored mortgage products to meet specific needs e. Enhanced financial inclusion and access to formal credit

Real estate developers: a. Increased home sales and demand for properties b. Collaboration opportunities with mortgage lenders c. Integrated financing solutions for homebuyers d. Access to a larger pool of potential buyers

Government and policymakers: a. Promotion of homeownership and housing market growth b. Economic stimulus through increased construction and property transactions c. Addressing social housing needs and reducing inequality d. Job creation and economic development in the housing sector e. Stimulation of related industries, such as construction and home improvement

SWOT Analysis

A SWOT (Strengths, Weaknesses, Opportunities, and Threats) analysis provides a comprehensive assessment of the Latin America home mortgage finance market’s internal and external factors.

Strengths: a. Growing demand for mortgage financing b. Supportive government policies and incentives c. Increasing urbanization and rising incomes d. Advancements in technology and digitalization e. Diversification of mortgage products and features f. Established banking institutions and mortgage lenders

Weaknesses: a. Limited access to affordable housing b. Regulatory complexities and compliance challenges c. Insufficient financial literacy among potential borrowers d. Unequal income distribution and income volatility e. Vulnerability to external economic shocks

Opportunities: a. Closing the affordable housing gap b. Expanding product portfolios and innovative mortgage solutions c. Enhancing financial literacy and consumer education d. Leveraging technology for efficiency and improved customer experience e. Targeting underserved populations and low-income earners

Threats: a. Economic volatility and interest rate fluctuations b. Limited credit history and informal employment affecting mortgage eligibility c. Competition from non-traditional mortgage lenders and fintech companies d. Changing regulatory landscape and compliance requirements e. Disruptions from external factors such as natural disasters or political instability

Market Key Trends

Digital mortgage experience: The adoption of technology has transformed the mortgage process, with borrowers increasingly seeking digital solutions for mortgage applications, document submission, and loan servicing. Lenders are investing in user-friendly online platforms and mobile applications to cater to this trend.

Personalized mortgage products: Borrowers are seeking more tailored mortgage solutions that align with their financial goals and lifestyle. Lenders are offering customizable mortgage products, such as flexible repayment options, interest rate structures, and value-added services.

Green mortgages and sustainability: The demand for sustainable housing and environmentally friendly homes is growing. Lenders are introducing green mortgage products that offer incentives and preferential terms for energy-efficient properties and renovations.

Open banking and data integration: The integration of financial data through open banking initiatives enables lenders to access comprehensive borrower information, streamlining the mortgage application process and enhancing credit risk assessments.

Collaborations between traditional lenders and fintech companies: Traditional banks and mortgage lenders are partnering with fintech companies to leverage their technological capabilities, improve operational efficiency, and offer innovative mortgage solutions.

Remote and digital property valuations: The Covid-19 pandemic accelerated the adoption of remote property valuations, leveraging technology and data analytics to assess property values without physical inspections. This trend is likely to continue as it offers convenience and efficiency.

Non-traditional credit assessment: Lenders are exploring alternative credit assessment methods, such as analyzing rental payment history, utility bill payments, and other non-traditional data points, to assess borrower creditworthiness, particularly for underserved populations.

Covid-19 Impact

The Covid-19 pandemic has had a significant impact on the Latin America home mortgage finance market:

Economic challenges: The pandemic resulted in economic contractions, job losses, and reduced consumer confidence, affecting borrower affordability and creditworthiness. Mortgage lenders faced challenges in assessing borrower risk amidst economic uncertainty.

Regulatory changes: Governments introduced temporary measures, such as moratoriums on mortgage payments, loan restructuring options, and interest rate reductions, to alleviate financial burdens on borrowers and maintain stability in the mortgage market.

Digital acceleration: The pandemic accelerated the adoption of digital mortgage processes, as social distancing measures limited physical interactions. Lenders expedited the implementation of digital solutions for mortgage applications, document processing, and virtual property valuations.

Shift in borrower preferences: The pandemic prompted changes in borrower preferences, including increased demand for homes with dedicated workspaces, outdoor areas, and enhanced digital connectivity. Lenders adapted to these changing needs by providing financing options tailored to new homeowner requirements.

Mortgage market resilience: Despite the challenges, the mortgage market demonstrated resilience, aided by government support measures and low-interest rate environments. Market players adapted their underwriting practices and introduced flexible repayment options to accommodate borrowers facing financial hardships.

Housing market trends: The pandemic influenced housing market dynamics, with shifts in demand from urban to suburban areas, increased interest in single-family homes, and changing preferences for larger living spaces. Mortgage lenders monitored these trends to adjust their product offerings accordingly.

Key Industry Developments

Introduction of digital mortgage platforms: Mortgage lenders have increasingly invested in digital mortgage platforms, allowing borrowers to complete the entire mortgage process online, from application to closing. These platforms streamline the application process, enhance customer experience, and expedite loan approvals.

Expansion of non-bank lenders and fintech companies: Non-bank lenders and fintech companies have gained traction in the mortgage market, leveraging technology, and innovative approaches to provide competitive mortgage products and reach underserved borrowers.

Government initiatives to promote homeownership: Governments have introduced policies and incentives to encourage homeownership, including mortgage subsidies, down payment assistance programs, and regulatory reforms that facilitate access to mortgage financing.

Sustainable mortgage products: Lenders are offering green mortgage products that incentivize energy-efficient housing, providing preferential terms and lower interest rates for environmentally friendly properties. These products align with increasing consumer demand for sustainable housing options.

Expansion of credit scoring models: Mortgage lenders are exploring alternative credit scoring models that incorporate non-traditional data sources, such as rental payment history and utility bill payments. This enables a more comprehensive assessment of borrower creditworthiness, particularly for borrowers with limited credit history.

Integration of open banking and data sharing: The integration of open banking initiatives allows lenders to access a broader range of borrower financial data, enhancing credit risk assessments, and streamlining the mortgage application process.

Increased focus on financial literacy: Stakeholders in the mortgage market, including lenders and governments, are placing emphasis on financial literacy initiatives to improve borrower understanding of mortgage products, rights, and responsibilities.

Collaboration between real estate developers and mortgage lenders: Real estate developers and mortgage lenders are forming partnerships to offer integrated solutions, combining property sales with mortgage financing options. These collaborations enhance customer convenience and promote the growth of the housing market.

Analyst Suggestions

Embrace technology and digitalization: Mortgage lenders should invest in technology and digital platforms to streamline processes, enhance customer experience, and improve operational efficiency. This includes offering user-friendly online applications, digital document processing, and automated underwriting systems.

Enhance financial literacy: Industry participants should prioritize financial education initiatives to improve borrower understanding of mortgage products, credit management, and personal finance. This empowers borrowers to make informed decisions and improves market participation.

Collaborate with fintech companies: Traditional lenders should explore partnerships and collaborations with fintech companies to leverage their technological capabilities and innovative solutions. This enables lenders to enhance their offerings, reach new customer segments, and stay competitive.

Develop specialized mortgage products: Lenders should tailor their mortgage products to meet the specific needs of different borrower segments, such as first-time homebuyers, low-income earners, and self-employed individuals. Offering flexible terms, down payment assistance, and customized repayment options can attract and serve these segments effectively.

Monitor market trends and adapt offerings: It is crucial for industry participants to stay updated on market trends, such as changing borrower preferences, demand for sustainable housing, and emerging technological advancements. Adapting product offerings and underwriting practices to align with these trends can provide a competitive advantage.

Strengthen risk management and compliance: Mortgage lenders must prioritize robust risk management practices and ensure compliance with changing regulatory requirements. This includes adopting sound underwriting standards, monitoring credit quality, and implementing effective mechanisms for managing default risk.

Foster collaboration and partnerships: Collaboration between mortgage lenders, real estate developers, and government entities can unlock synergies and create integrated solutions that benefit borrowers, promote the growth of the housing market, and drive overall industry development.

Future Outlook

The Latin America home mortgage finance market is expected to continue its growth trajectory, driven by several factors:

Urbanization and population growth: Increasing urbanization and a growing population will continue to drive demand for housing and mortgage financing.

Favorable government policies: Governments will likely continue implementing policies and incentives to promote homeownership, expand access to mortgage financing, and support sustainable housing initiatives.

Technological advancements: The adoption of technology and digitalization will further transform the mortgage industry, enhancing customer experience, improving operational efficiency, and expanding access to financing.

Sustainable housing and green financing: The demand for sustainable homes and environmentally friendly financing options will continue to rise, leading to the development of more green mortgage products and incentives.

Market expansion and financial inclusion: Efforts to expand access to mortgage financing for underserved populations, such as low-income earners and self-employed individuals, will drive market expansion and foster financial inclusion.

Changing borrower preferences: Shifts in borrower preferences, such as the desire for more personalized and flexible mortgage products, will influence market dynamics and drive product innovation.

Economic recovery and stability: As economies recover from the Covid-19 pandemic, increased stability, job growth, and improving consumer confidence will positively impact the mortgage market.

Despite the positive outlook, challenges remain, including economic volatility, regulatory complexities, and the need to address the affordable housing gap. Market participants must remain agile, adapt to changing dynamics, and prioritize customer-centric approaches to capitalize on the growth opportunities in the Latin America home mortgage finance market.

Conclusion

The Latin America home mortgage finance market is witnessing significant growth, driven by factors such as urbanization, rising incomes, supportive government policies, and technological advancements. The market presents opportunities for lenders, borrowers, real estate developers, and governments to promote homeownership, expand access to financing, and stimulate economic growth. However, challenges such as limited access to affordable housing, regulatory complexities, and economic volatility must be addressed to sustain market development. By embracing technology, tailoring products to specific borrower segments, enhancing financial literacy, and fostering collaboration, industry participants can navigate the evolving landscape and unlock the market’s full potential. With a positive future outlook, the Latin America home mortgage finance market is poised for further expansion and transformation in the coming years.

What is Home Mortgage Finance?

Home Mortgage Finance refers to the various financial products and services that facilitate the borrowing of funds to purchase residential properties. This includes mortgages, refinancing options, and home equity loans, which are essential for homebuyers in Latin America.

What are the key players in the Latin America Home Mortgage Finance Market?

Key players in the Latin America Home Mortgage Finance Market include Banco do Brasil, BBVA, and Santander, which offer a range of mortgage products tailored to local consumers. These companies compete on interest rates, customer service, and innovative financing solutions, among others.

What are the main drivers of the Latin America Home Mortgage Finance Market?

The main drivers of the Latin America Home Mortgage Finance Market include increasing urbanization, rising disposable incomes, and government initiatives aimed at promoting home ownership. These factors contribute to a growing demand for mortgage financing across the region.

What challenges does the Latin America Home Mortgage Finance Market face?

The Latin America Home Mortgage Finance Market faces challenges such as high-interest rates, economic instability, and regulatory hurdles that can hinder access to financing. Additionally, a lack of financial literacy among potential borrowers can limit market growth.

What opportunities exist in the Latin America Home Mortgage Finance Market?

Opportunities in the Latin America Home Mortgage Finance Market include the expansion of digital mortgage platforms and the introduction of innovative financing products. As more consumers seek home ownership, lenders can leverage technology to streamline the application process and enhance customer experience.

What trends are shaping the Latin America Home Mortgage Finance Market?

Trends shaping the Latin America Home Mortgage Finance Market include the rise of fintech companies offering alternative lending solutions and the increasing use of data analytics to assess creditworthiness. Additionally, there is a growing emphasis on sustainable housing projects that align with environmental goals.

Leading Companies in the Latin America Home Mortgage Finance Market:

Banco do Brasil

Caixa Econômica Federal

Banco Santander Brasil

Itaú Unibanco Holding S.A.

Banorte

BBVA Bancomer

Banco de Crédito del Perú (BCP)

Banco de Chile

Banco Macro

Banco Galicia

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.