444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Japan study of data center water consumption market represents a critical analysis sector focused on understanding and optimizing water usage patterns across Japan’s rapidly expanding digital infrastructure. As the nation continues its digital transformation journey, data centers have emerged as significant water consumers, prompting comprehensive research initiatives to monitor, analyze, and improve water efficiency metrics. This specialized market encompasses various stakeholders including environmental consultants, technology providers, government agencies, and data center operators who collaborate to develop sustainable water management strategies.

Market dynamics indicate that Japan’s data center water consumption studies have gained substantial momentum, driven by increasing environmental regulations and corporate sustainability commitments. The research sector focuses on analyzing cooling system efficiency, water recycling technologies, and alternative cooling methods that can reduce overall water dependency. Current trends show that approximately 78% of Japanese data centers are actively participating in water consumption monitoring programs, reflecting the industry’s commitment to environmental stewardship.

Regional concentration of data center water consumption studies is particularly pronounced in Tokyo, Osaka, and other major metropolitan areas where data center density is highest. The market encompasses both traditional water usage analysis and innovative research into closed-loop cooling systems, air-based cooling alternatives, and smart water management technologies that can significantly reduce consumption rates.

The Japan study of data center water consumption market refers to the comprehensive research ecosystem dedicated to analyzing, monitoring, and optimizing water usage patterns within Japan’s data center infrastructure. This market encompasses specialized consulting services, monitoring technologies, research methodologies, and analytical frameworks designed to understand how data centers consume water resources and identify opportunities for efficiency improvements.

Core components of this market include water usage auditing services, consumption pattern analysis, cooling system optimization studies, and environmental impact assessments. The research focuses on quantifying water consumption across different data center types, from hyperscale facilities to edge computing centers, providing actionable insights for operators seeking to reduce their environmental footprint while maintaining operational efficiency.

Market participants include environmental consulting firms, technology solution providers, academic research institutions, and government agencies that collaborate to develop comprehensive understanding of water consumption patterns and promote sustainable practices across Japan’s digital infrastructure landscape.

Japan’s data center water consumption research market has experienced significant growth as environmental consciousness and regulatory requirements drive demand for comprehensive water usage analysis. The market serves critical functions in helping data center operators understand their water footprint, comply with environmental regulations, and implement sustainable cooling technologies that reduce overall consumption.

Key market drivers include Japan’s commitment to carbon neutrality by 2050, increasing data center deployment across the nation, and growing awareness of water scarcity issues. Research indicates that approximately 65% of data center operators in Japan have implemented comprehensive water monitoring systems, demonstrating the market’s maturation and widespread adoption of sustainable practices.

Technology innovation within this market focuses on advanced monitoring systems, predictive analytics for water usage optimization, and integration of alternative cooling technologies. The market encompasses both established environmental consulting firms and emerging technology providers specializing in data center sustainability solutions.

Future prospects for the market remain robust, supported by continued data center expansion, evolving environmental regulations, and increasing corporate sustainability commitments across Japan’s technology sector.

Primary market insights reveal several critical trends shaping Japan’s data center water consumption research landscape:

Environmental regulations serve as the primary driver for Japan’s data center water consumption research market. The government’s increasingly stringent environmental standards require data center operators to monitor, report, and optimize their water usage patterns, creating sustained demand for specialized research and consulting services.

Digital transformation acceleration across Japan has led to unprecedented data center expansion, with new facilities requiring comprehensive water usage analysis from the planning stage through operational optimization. This growth creates continuous opportunities for water consumption research providers to support sustainable development practices.

Corporate sustainability commitments from major technology companies and data center operators drive significant investment in water consumption studies. Many organizations have established ambitious environmental targets that require detailed understanding of their water footprint and implementation of optimization strategies.

Water scarcity concerns in certain regions of Japan have heightened awareness of the need for efficient water management across all industrial sectors, including data centers. This awareness translates into increased demand for research services that can identify consumption reduction opportunities and alternative cooling technologies.

Technological advancement in monitoring and analytics capabilities enables more sophisticated water consumption analysis, creating new market opportunities for providers offering advanced research methodologies and real-time optimization solutions.

High implementation costs associated with comprehensive water monitoring and analysis systems can limit adoption among smaller data center operators, constraining market growth in certain segments. The initial investment required for advanced monitoring infrastructure and ongoing research services may exceed budget constraints for some organizations.

Technical complexity of modern data center cooling systems creates challenges for accurate water consumption measurement and analysis. The integration of multiple cooling technologies, varying operational conditions, and complex water flow patterns can complicate research efforts and limit the accuracy of consumption studies.

Limited standardization across the industry regarding water consumption measurement methodologies can create inconsistencies in research results and complicate comparative analysis between different facilities or operators. This lack of standardization may reduce the perceived value of research services.

Skilled workforce shortage in specialized areas of data center environmental analysis can constrain market growth, as the demand for qualified researchers and consultants exceeds available talent pools. This shortage may limit the ability of research providers to scale their operations effectively.

Data sensitivity concerns among data center operators regarding operational information sharing can limit the scope and effectiveness of water consumption research initiatives, particularly for comprehensive industry-wide studies that require detailed facility data.

Edge computing expansion across Japan creates significant opportunities for water consumption research providers to develop specialized analysis methodologies for smaller, distributed data center facilities. These edge locations often require different cooling approaches and water management strategies compared to traditional large-scale data centers.

Artificial intelligence integration in water consumption analysis presents opportunities for developing predictive models that can optimize cooling system performance and reduce water usage through intelligent automation. AI-powered analytics can identify consumption patterns and recommend optimization strategies with greater precision than traditional analysis methods.

Government incentive programs supporting environmental sustainability initiatives create opportunities for research providers to develop comprehensive water consumption reduction programs that qualify for financial incentives, making their services more attractive to data center operators.

International expansion of Japanese data center operators into other Asian markets creates demand for water consumption research expertise that can be applied across different regulatory environments and climate conditions, expanding the addressable market for specialized research providers.

Circular economy initiatives focused on water recycling and reuse present opportunities for developing innovative research methodologies that can quantify the benefits of closed-loop cooling systems and support business cases for sustainable technology investments.

Supply-demand dynamics in Japan’s data center water consumption research market reflect the balance between growing environmental awareness and the practical challenges of implementing comprehensive monitoring systems. Demand continues to outpace supply in specialized research capabilities, particularly for advanced analytics and optimization services.

Competitive dynamics involve both established environmental consulting firms expanding into data center specialization and new technology providers developing innovative monitoring and analysis solutions. This competition drives continuous innovation in research methodologies and service delivery approaches.

Technology evolution significantly impacts market dynamics, with advances in IoT sensors, cloud-based analytics platforms, and machine learning algorithms enabling more sophisticated water consumption analysis capabilities. These technological improvements create opportunities for differentiation among research providers.

Regulatory dynamics continue to shape market development, with evolving environmental standards and reporting requirements creating new demand for specialized research services. Policy changes often drive rapid market expansion as data center operators seek compliance support.

Economic dynamics influence market growth through their impact on data center investment and expansion plans. Economic conditions affect both the pace of new data center development and the budget allocation for environmental research and optimization initiatives.

Comprehensive research methodology employed in Japan’s data center water consumption studies encompasses multiple data collection and analysis approaches designed to provide accurate, actionable insights for stakeholders across the industry. The methodology integrates quantitative measurement techniques with qualitative assessment frameworks to deliver holistic understanding of water usage patterns.

Primary research methods include direct facility monitoring through advanced sensor networks, operational data collection from data center management systems, and structured interviews with facility operators and environmental managers. These primary sources provide real-time consumption data and operational insights that form the foundation of comprehensive analysis.

Secondary research approaches involve analysis of regulatory filings, industry reports, technology specifications, and comparative studies from international markets. This secondary research provides context for Japan-specific findings and enables benchmarking against global best practices in data center water management.

Data validation processes ensure research accuracy through multiple verification methods, including cross-referencing consumption data with utility records, conducting facility audits, and implementing statistical analysis techniques to identify and correct anomalies in collected data.

Analytical frameworks employed in the research incorporate water usage efficiency metrics, cooling system performance indicators, and environmental impact assessments that enable comprehensive evaluation of data center water consumption patterns and optimization opportunities.

Tokyo metropolitan area dominates Japan’s data center water consumption research market, accounting for approximately 45% of total research activity due to the high concentration of data center facilities and corporate headquarters. The region’s water stress conditions and stringent environmental regulations drive significant demand for comprehensive consumption analysis and optimization services.

Osaka region represents the second-largest market for data center water consumption research, with approximately 25% market share driven by substantial data center development and industrial water management initiatives. The region’s focus on sustainable manufacturing practices extends to data center operations, creating demand for specialized research services.

Kyushu region has emerged as a growing market for water consumption research, supported by increasing data center investment and favorable climate conditions that enable innovative cooling approaches. The region’s renewable energy resources and water availability create unique research opportunities for sustainable data center operations.

Northern regions including Hokkaido present specialized research opportunities focused on leveraging cold climate conditions for natural cooling systems that can significantly reduce water consumption requirements. These regions offer unique case studies for climate-optimized data center design and operation.

Coastal areas across Japan present specific research challenges and opportunities related to seawater cooling systems, humidity management, and corrosion resistance in data center cooling infrastructure, requiring specialized analysis methodologies and expertise.

Market leadership in Japan’s data center water consumption research sector is distributed among several categories of providers, each offering specialized capabilities and expertise:

Competitive differentiation occurs through specialized expertise in specific data center types, advanced analytics capabilities, regulatory compliance support, and integration of emerging technologies such as artificial intelligence and machine learning in consumption analysis.

Strategic partnerships between research providers, technology vendors, and data center operators create collaborative ecosystems that enhance research capabilities and accelerate the development of innovative water management solutions.

By Service Type:

By Data Center Type:

By Technology Focus:

Hyperscale data centers represent the most complex segment for water consumption research, requiring sophisticated analysis methodologies to understand the interaction between massive cooling systems, varying computational loads, and water usage patterns. These facilities often serve as testing grounds for innovative cooling technologies and water management approaches.

Enterprise data centers focus primarily on compliance-driven research initiatives, with emphasis on meeting corporate sustainability targets and regulatory requirements. Research in this segment often involves integration with broader corporate environmental management systems and alignment with enterprise sustainability reporting frameworks.

Edge computing facilities present unique research challenges due to their distributed nature, smaller scale, and often unmanned operation. Water consumption research for edge centers focuses on developing standardized monitoring approaches and identifying optimization opportunities that can be implemented across multiple small facilities.

Colocation centers require specialized research approaches that can accommodate multiple tenants with varying cooling requirements and sustainability commitments. Research in this segment often involves developing tenant-specific water usage allocation methodologies and shared optimization strategies.

Cloud service provider facilities drive innovation in water consumption research through their scale, technical sophistication, and sustainability commitments. These facilities often participate in advanced research initiatives that push the boundaries of water-efficient cooling technologies and operational practices.

Data center operators benefit from comprehensive water consumption research through improved operational efficiency, reduced environmental impact, and enhanced regulatory compliance. Research insights enable operators to optimize cooling system performance, reduce water costs, and demonstrate environmental stewardship to stakeholders and customers.

Environmental consultants gain access to specialized market opportunities and can develop expertise in the growing data center sustainability sector. The market provides opportunities for service expansion, technology integration, and development of innovative research methodologies that differentiate their offerings.

Technology providers benefit from market insights that inform product development, identify customer needs, and support sales efforts for water-efficient cooling technologies. Research data helps validate technology benefits and supports business cases for sustainable cooling solutions.

Government agencies receive valuable data for policy development, regulatory framework enhancement, and environmental impact assessment. Research insights support evidence-based decision-making for data center environmental regulations and sustainability initiatives.

Academic institutions gain opportunities for applied research, industry collaboration, and development of specialized expertise in data center environmental analysis. The market provides funding opportunities and real-world applications for research initiatives.

Investors and financial institutions benefit from comprehensive environmental risk assessment data that supports investment decisions and due diligence processes for data center projects and sustainability-focused investments.

Strengths:

Weaknesses:

Opportunities:

Threats:

Real-time monitoring integration has emerged as a dominant trend, with approximately 72% of new research projects incorporating continuous monitoring capabilities rather than periodic assessment approaches. This shift enables more accurate consumption analysis and immediate identification of optimization opportunities.

Artificial intelligence adoption in water consumption analysis is accelerating, with machine learning algorithms being deployed to identify consumption patterns, predict optimization opportunities, and automate monitoring processes. AI-powered analytics are becoming standard components of comprehensive research methodologies.

Integrated sustainability reporting is gaining prominence as organizations seek to combine water consumption analysis with broader environmental impact assessments. This trend drives demand for comprehensive research services that address multiple sustainability metrics simultaneously.

Alternative cooling technology research is expanding rapidly, with increased focus on immersion cooling, liquid cooling, and air-based alternatives that can significantly reduce water consumption requirements. Research providers are developing specialized expertise in these emerging cooling approaches.

Circular economy principles are being integrated into water consumption research, with emphasis on closed-loop systems, water recycling, and reuse opportunities that can minimize overall consumption and environmental impact.

Climate adaptation strategies are becoming integral to water consumption research, with analysis focused on maintaining cooling efficiency during extreme weather events while minimizing water dependency and ensuring operational resilience.

Advanced monitoring technology deployment has accelerated across Japan’s data center sector, with major operators implementing comprehensive sensor networks that provide real-time water consumption data and enable sophisticated analysis capabilities. These deployments support more accurate research and faster identification of optimization opportunities.

Regulatory framework enhancement by Japanese government agencies has strengthened environmental reporting requirements for data centers, creating increased demand for specialized water consumption research and compliance support services. New regulations emphasize transparency and continuous improvement in water usage efficiency.

Industry collaboration initiatives have emerged to develop standardized methodologies for water consumption measurement and analysis across the data center sector. These collaborative efforts aim to improve research consistency and enable meaningful comparative analysis between different facilities and operators.

International best practice adoption is increasing, with Japanese research providers incorporating methodologies and technologies from global leaders in data center sustainability. This knowledge transfer accelerates innovation and improves the sophistication of local research capabilities.

Academic research expansion in data center environmental analysis has grown significantly, with universities establishing specialized programs and research centers focused on sustainable data center technologies and water management optimization.

Technology vendor partnerships between research providers and cooling system manufacturers have strengthened, enabling integrated approaches to water consumption analysis that consider both current performance and future technology adoption opportunities.

MarkWide Research analysis indicates that market participants should prioritize development of standardized water consumption measurement methodologies to improve research consistency and enable meaningful comparative analysis across the industry. Standardization will enhance the value of research services and support more effective optimization strategies.

Investment in advanced analytics capabilities is essential for research providers seeking to differentiate their offerings and provide superior value to clients. Integration of artificial intelligence, machine learning, and predictive analytics will become increasingly important for competitive positioning in the market.

Strategic partnerships with technology vendors, data center operators, and academic institutions should be prioritized to enhance research capabilities and access to specialized expertise. Collaborative approaches will be essential for addressing the technical complexity of modern data center cooling systems.

Geographic expansion into emerging data center markets across Asia presents significant growth opportunities for Japanese research providers with established expertise in water consumption analysis. International expansion can leverage Japan’s advanced capabilities and regulatory experience.

Service portfolio diversification should include integration of water consumption research with broader sustainability consulting services, enabling comprehensive environmental impact assessment and optimization strategies that address multiple sustainability metrics simultaneously.

Workforce development initiatives are critical for addressing the skilled labor shortage in specialized data center environmental analysis. Investment in training programs and academic partnerships will be essential for supporting market growth and maintaining service quality.

Market growth prospects for Japan’s data center water consumption research sector remain robust, supported by continued data center expansion, evolving environmental regulations, and increasing corporate sustainability commitments. MWR projections indicate sustained growth in demand for specialized research services across all market segments.

Technology evolution will continue to drive market development, with advances in monitoring systems, analytics platforms, and cooling technologies creating new research opportunities and methodological requirements. The integration of artificial intelligence and machine learning will become standard practice in comprehensive consumption analysis.

Regulatory development is expected to strengthen environmental requirements for data centers, creating increased demand for compliance support and optimization services. Future regulations may introduce more stringent water usage efficiency standards and expanded reporting requirements.

Industry consolidation may occur as the market matures, with larger research providers acquiring specialized capabilities and smaller firms focusing on niche expertise areas. This consolidation could improve service quality and expand the range of available research capabilities.

International expansion opportunities will grow as Japanese data center operators expand into other Asian markets and international companies seek expertise in water consumption optimization. This expansion will create new revenue streams for established research providers.

Innovation acceleration in cooling technologies will require continuous adaptation of research methodologies and analysis frameworks. Research providers must maintain flexibility and invest in ongoing capability development to address emerging technologies and changing market requirements.

Japan’s data center water consumption research market represents a critical and rapidly evolving sector that plays an essential role in supporting sustainable digital infrastructure development. The market has demonstrated remarkable growth driven by environmental regulations, corporate sustainability commitments, and technological advancement in monitoring and analysis capabilities.

Key market strengths include strong regulatory framework support, advanced technology integration, and collaborative industry relationships that foster innovation and comprehensive research development. These strengths position the market for continued growth and expansion into new application areas and geographic regions.

Future success in this market will depend on continued investment in advanced analytics capabilities, development of standardized research methodologies, and strategic partnerships that enhance service offerings and market reach. Organizations that can effectively integrate emerging technologies while maintaining focus on practical optimization solutions will be best positioned for long-term success.

Market participants should prioritize workforce development, technology innovation, and service diversification to capitalize on growing opportunities in edge computing, alternative cooling technologies, and international expansion. The sector’s evolution toward more sophisticated, AI-powered research methodologies will create new competitive advantages for forward-thinking providers.

Overall market outlook remains highly positive, with sustained growth expected across all segments as Japan continues its digital transformation journey while maintaining strong commitment to environmental sustainability and resource optimization in its critical digital infrastructure.

What is Data Center Water Consumption?

Data Center Water Consumption refers to the amount of water used by data centers for cooling and other operational processes. This includes water used in cooling towers, chillers, and other systems that manage heat generated by servers and equipment.

What are the key players in the Japan Study Of Data Center Water Consumption Market?

Key players in the Japan Study Of Data Center Water Consumption Market include NTT Communications, Fujitsu, and SoftBank, among others. These companies are involved in optimizing water usage and implementing sustainable practices in their data center operations.

What are the growth factors driving the Japan Study Of Data Center Water Consumption Market?

The growth of the Japan Study Of Data Center Water Consumption Market is driven by the increasing demand for data processing, the expansion of cloud services, and the need for energy-efficient cooling solutions. Additionally, regulatory pressures for sustainability are pushing companies to adopt better water management practices.

What challenges does the Japan Study Of Data Center Water Consumption Market face?

Challenges in the Japan Study Of Data Center Water Consumption Market include the high cost of implementing advanced cooling technologies and the scarcity of water resources in certain regions. Furthermore, regulatory compliance can be complex and may vary by locality.

What opportunities exist in the Japan Study Of Data Center Water Consumption Market?

Opportunities in the Japan Study Of Data Center Water Consumption Market include the development of innovative cooling technologies and the integration of water recycling systems. Companies can also explore partnerships to enhance sustainability and reduce overall water usage.

What trends are shaping the Japan Study Of Data Center Water Consumption Market?

Trends in the Japan Study Of Data Center Water Consumption Market include the adoption of AI and IoT for monitoring water usage, the shift towards hybrid cooling solutions, and an increased focus on sustainability initiatives. These trends are helping data centers to optimize their water consumption and reduce environmental impact.

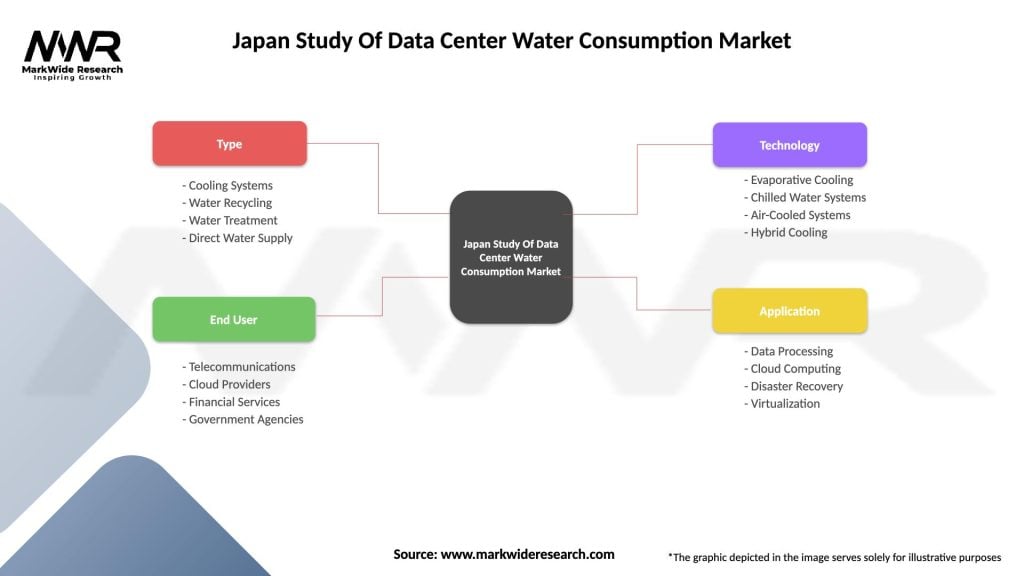

Japan Study Of Data Center Water Consumption Market

| Segmentation Details | Description |

|---|---|

| Type | Cooling Systems, Water Recycling, Water Treatment, Direct Water Supply |

| End User | Telecommunications, Cloud Providers, Financial Services, Government Agencies |

| Technology | Evaporative Cooling, Chilled Water Systems, Air-Cooled Systems, Hybrid Cooling |

| Application | Data Processing, Cloud Computing, Disaster Recovery, Virtualization |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Japan Study Of Data Center Water Consumption Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.