444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Italy HVAC market represents a dynamic and evolving sector within the European heating, ventilation, and air conditioning industry. Italy’s HVAC market has experienced substantial transformation driven by stringent energy efficiency regulations, growing environmental consciousness, and increasing demand for smart building technologies. The market encompasses residential, commercial, and industrial applications, with energy-efficient systems gaining significant traction across all segments.

Market dynamics in Italy reflect the country’s commitment to reducing carbon emissions and achieving climate neutrality goals. The Italian government’s focus on green building initiatives and renovation programs has created substantial opportunities for HVAC manufacturers and service providers. Smart HVAC technologies are experiencing rapid adoption, with connected systems showing 35% growth in residential applications over recent years.

Regional variations within Italy significantly influence HVAC demand patterns, with northern regions requiring more heating solutions while southern areas focus on cooling systems. The market demonstrates strong resilience and adaptability, with heat pump technologies gaining 42% market share in new installations. MarkWide Research analysis indicates that Italy’s HVAC sector continues to evolve toward sustainable and intelligent climate control solutions.

The Italy HVAC market refers to the comprehensive ecosystem of heating, ventilation, and air conditioning systems, equipment, and services operating within Italian territory. This market encompasses the design, manufacturing, installation, maintenance, and replacement of climate control systems across residential, commercial, and industrial sectors throughout Italy.

HVAC systems in the Italian context include traditional heating solutions like boilers and radiators, modern heat pumps, air conditioning units, ventilation systems, and integrated smart climate control technologies. The market also covers energy recovery ventilation systems, geothermal solutions, and renewable energy-integrated HVAC applications that align with Italy’s sustainability objectives.

Market participants include international manufacturers, local equipment producers, installation contractors, maintenance service providers, and technology integrators. The Italian HVAC market operates within a regulatory framework emphasizing energy efficiency standards, environmental compliance, and building performance requirements that drive innovation and market evolution.

Italy’s HVAC market demonstrates robust growth potential driven by regulatory mandates, technological advancement, and changing consumer preferences toward sustainable climate solutions. The market benefits from strong government support through incentive programs and energy efficiency requirements that accelerate adoption of high-performance HVAC systems.

Key market drivers include Italy’s building renovation wave, increasing focus on indoor air quality, and growing demand for smart home technologies. The residential segment dominates market activity, accounting for approximately 58% of total installations, while commercial and industrial applications show steady expansion. Heat pump adoption represents a significant trend, with installations growing at 28% annually as consumers seek alternatives to traditional heating systems.

Technological innovation shapes market evolution, with IoT-enabled systems, artificial intelligence integration, and renewable energy compatibility becoming standard features. The market faces challenges including skilled labor shortages and supply chain complexities, but these are offset by strong demand fundamentals and supportive policy environment. Future growth prospects remain positive, supported by Italy’s commitment to energy transition and sustainable building practices.

Strategic insights reveal several critical trends shaping Italy’s HVAC landscape. The market demonstrates clear preference for energy-efficient solutions, with consumers increasingly prioritizing long-term operational savings over initial purchase costs. This shift drives demand for premium HVAC systems with advanced efficiency ratings and smart control capabilities.

Government incentives serve as primary catalysts for Italy’s HVAC market expansion. The Italian government’s Superbonus program and various tax deduction schemes significantly reduce consumer costs for energy-efficient HVAC installations. These initiatives create substantial market momentum by making premium systems financially accessible to broader consumer segments.

Energy cost concerns drive consumer interest in efficient HVAC solutions as Italian households and businesses seek to reduce utility expenses. Rising energy prices motivate investments in high-efficiency heat pumps, smart thermostats, and integrated renewable energy systems. The focus on operational cost reduction creates sustained demand for advanced HVAC technologies.

Climate change awareness influences purchasing decisions as Italian consumers increasingly prioritize environmental impact. The growing emphasis on carbon footprint reduction drives adoption of electric heat pumps, geothermal systems, and renewable energy-integrated HVAC solutions. Building renovation trends further accelerate market growth as property owners upgrade aging systems to meet modern efficiency standards and comfort expectations.

High initial costs represent significant barriers to HVAC market expansion in Italy. Premium energy-efficient systems require substantial upfront investments that may deter price-sensitive consumers despite long-term savings potential. The cost-benefit analysis often extends over several years, creating hesitation among potential buyers seeking immediate returns on investment.

Skilled labor shortages constrain market growth as the HVAC industry faces challenges finding qualified technicians for installation and maintenance services. The complexity of modern smart HVAC systems requires specialized training and certification, creating bottlenecks in service delivery. This shortage can lead to extended installation timelines and increased service costs.

Regulatory complexity creates challenges for market participants navigating multiple compliance requirements across different Italian regions. Varying local building codes, permit processes, and inspection requirements can complicate project execution and increase administrative burdens. Supply chain disruptions and component availability issues also impact market stability, particularly for imported HVAC equipment and specialized components.

Smart building integration presents substantial opportunities for HVAC market expansion in Italy. The growing adoption of building automation systems creates demand for connected HVAC solutions that integrate with broader facility management platforms. This trend opens new revenue streams for manufacturers offering IoT-enabled products and software services.

Retrofit market potential represents significant growth opportunities as Italy’s aging building stock requires modernization. Millions of Italian buildings need HVAC system upgrades to meet current efficiency standards and comfort expectations. The retrofit segment offers stable, long-term demand for replacement systems, maintenance services, and performance optimization solutions.

Renewable energy integration creates new market segments combining HVAC systems with solar panels, geothermal sources, and energy storage solutions. The Italian government’s support for renewable energy adoption encourages integrated approaches that maximize energy efficiency and reduce grid dependence. Commercial sector expansion in logistics, data centers, and healthcare facilities drives demand for specialized HVAC applications with unique performance requirements.

Supply and demand dynamics in Italy’s HVAC market reflect seasonal patterns, regulatory changes, and economic conditions. Demand fluctuations typically peak during spring and fall months when consumers prepare for seasonal climate changes. The market demonstrates resilience through diversified applications spanning residential, commercial, and industrial sectors.

Competitive dynamics intensify as international manufacturers compete with established Italian brands for market share. Price competition remains significant in standard product categories, while premium segments focus on technology differentiation and energy performance. The market rewards innovation, with companies investing heavily in R&D activities to develop next-generation HVAC solutions.

Technology adoption cycles influence market dynamics as consumers gradually embrace smart HVAC features and connectivity options. The transition from traditional systems to intelligent climate control creates opportunities for early adopters while challenging conventional manufacturers. MWR analysis indicates that market dynamics continue evolving toward integrated, sustainable, and user-centric HVAC solutions that deliver enhanced comfort and efficiency.

Comprehensive market analysis employs multiple research methodologies to ensure accurate and reliable insights into Italy’s HVAC market. Primary research includes extensive surveys of industry participants, including manufacturers, distributors, installers, and end-users across different market segments and geographic regions within Italy.

Secondary research incorporates analysis of industry reports, government statistics, trade association data, and regulatory documentation. Market sizing methodologies utilize bottom-up and top-down approaches to validate findings and ensure consistency across different data sources. Expert interviews with industry leaders provide qualitative insights into market trends and future developments.

Data validation processes include cross-referencing multiple sources, conducting follow-up interviews, and applying statistical analysis techniques to identify patterns and anomalies. Regional analysis considers variations across Italian provinces and municipalities to capture local market dynamics. The methodology ensures comprehensive coverage of all HVAC market segments while maintaining analytical rigor and objectivity throughout the research process.

Northern Italy dominates the HVAC market, accounting for approximately 45% of total demand due to higher population density, industrial activity, and colder climate conditions requiring extensive heating solutions. Cities like Milan, Turin, and Venice drive significant commercial and residential HVAC installations, with particular emphasis on energy-efficient heating systems and smart building technologies.

Central Italy represents a balanced market with moderate climate conditions requiring both heating and cooling solutions throughout the year. Rome and Florence lead regional demand, with growing focus on historic building renovations and modern HVAC system integration. The region shows strong adoption rates for heat pump technologies and renewable energy-integrated systems.

Southern Italy emphasizes cooling applications due to warmer climate conditions, with air conditioning systems representing the largest market segment. Naples, Bari, and Palermo drive regional demand, particularly in commercial and hospitality sectors. The region demonstrates increasing interest in energy-efficient cooling solutions and smart climate control systems. Island regions including Sicily and Sardinia show unique market characteristics with emphasis on standalone systems and renewable energy integration.

Market leadership in Italy’s HVAC sector includes both international corporations and established Italian manufacturers competing across different product categories and market segments. The competitive environment emphasizes technological innovation, energy efficiency, and comprehensive service offerings to differentiate market positions.

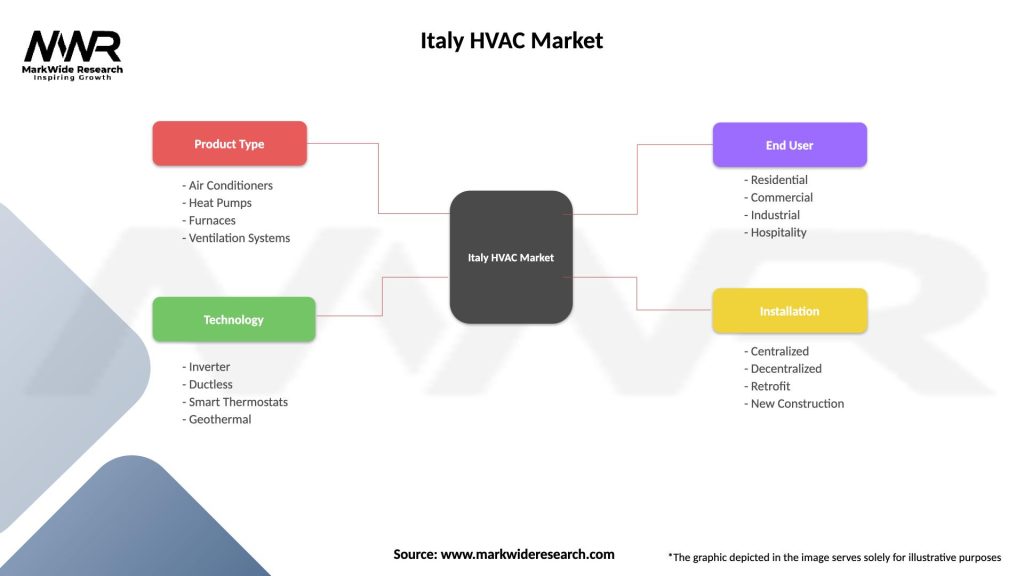

By Application: The Italian HVAC market segments into residential, commercial, and industrial applications, each with distinct requirements and growth patterns. Residential applications dominate overall market activity, driven by new construction, renovation projects, and replacement demand for aging systems.

By Product Type: Market segmentation includes heating systems (boilers, heat pumps, radiators), cooling systems (air conditioners, chillers), ventilation equipment, and integrated HVAC solutions. Heat pump systems show the fastest growth across all segments due to energy efficiency advantages and government incentives.

By Technology: Traditional systems compete with smart HVAC technologies featuring IoT connectivity, artificial intelligence, and remote monitoring capabilities. Energy recovery systems and renewable energy-integrated solutions represent growing market segments aligned with sustainability objectives.

By End-User: Segmentation covers homeowners, commercial building operators, industrial facilities, and institutional customers. Each segment demonstrates unique purchasing patterns, performance requirements, and service expectations that influence product development and marketing strategies.

Heating Systems Category: This segment leads Italy’s HVAC market with traditional boilers gradually being replaced by efficient heat pump technologies. Condensing boilers maintain significant market share in retrofit applications, while new installations increasingly favor air-source and ground-source heat pumps. The category benefits from government incentives promoting energy-efficient heating solutions.

Cooling Systems Category: Air conditioning demand grows steadily, particularly in southern Italian regions and commercial applications. Split-system air conditioners dominate residential cooling, while commercial buildings adopt VRF systems and centralized cooling solutions. Energy efficiency ratings significantly influence purchasing decisions as consumers seek to minimize operational costs.

Ventilation Category: Indoor air quality concerns drive ventilation system adoption, with mechanical ventilation with heat recovery gaining popularity in new construction. The category shows accelerated growth following increased awareness of airborne health risks and building performance standards requiring adequate ventilation rates.

Smart HVAC Category: Connected systems represent the fastest-growing segment, with smart thermostats and integrated building management systems showing strong adoption rates. This category appeals to tech-savvy consumers and commercial operators seeking operational optimization and remote monitoring capabilities.

Manufacturers benefit from Italy’s stable HVAC market demand driven by replacement cycles, renovation activities, and new construction projects. The market rewards innovation and efficiency, allowing companies with advanced technologies to command premium pricing and build customer loyalty through superior performance.

Installers and contractors enjoy consistent business opportunities across residential and commercial segments. The complexity of modern HVAC systems creates demand for specialized expertise, enabling qualified professionals to differentiate their services and maintain healthy profit margins through value-added offerings.

End-users gain access to increasingly efficient and comfortable climate control solutions that reduce energy costs and environmental impact. Smart HVAC technologies provide enhanced convenience, remote monitoring capabilities, and predictive maintenance features that improve system reliability and longevity.

Government stakeholders achieve energy efficiency and carbon reduction objectives through HVAC market development. The sector contributes to economic growth through job creation, technology innovation, and reduced energy import dependence as efficient systems decrease overall energy consumption.

Strengths:

Weaknesses:

Opportunities:

Threats:

Electrification trend dominates Italy’s HVAC market as consumers and businesses transition from fossil fuel-based heating systems to electric heat pumps and renewable energy-integrated solutions. This shift aligns with national decarbonization goals and creates substantial opportunities for manufacturers specializing in electric HVAC technologies.

Smart home integration drives demand for connected HVAC systems that communicate with other building systems and provide remote monitoring capabilities. Artificial intelligence and machine learning technologies enable predictive maintenance, energy optimization, and personalized comfort control that appeal to tech-savvy Italian consumers.

Indoor air quality focus intensifies following increased health awareness, driving adoption of advanced filtration systems, UV sterilization, and enhanced ventilation solutions. Commercial buildings particularly emphasize air quality improvements to ensure occupant health and comply with evolving workplace safety standards.

Circular economy principles influence HVAC market development as manufacturers focus on product longevity, recyclability, and service-based business models. Retrofit and upgrade services gain importance as alternatives to complete system replacement, extending equipment lifecycles and reducing environmental impact.

Technology partnerships between HVAC manufacturers and software companies accelerate development of intelligent climate control systems. These collaborations produce integrated solutions combining hardware excellence with advanced analytics and user interface capabilities that enhance system performance and user experience.

Manufacturing investments in Italy include new production facilities and research centers focused on developing next-generation HVAC technologies. International companies establish local operations to serve European markets while Italian manufacturers expand capabilities to compete globally in premium market segments.

Regulatory developments include updated energy efficiency standards and building codes that influence HVAC system requirements. The Italian government’s National Recovery and Resilience Plan allocates substantial funding for building efficiency improvements, creating additional market opportunities for HVAC providers.

Service innovation includes digital platforms for system monitoring, predictive maintenance, and performance optimization. MarkWide Research indicates that service-based revenue models gain traction as HVAC companies seek recurring income streams and customers value ongoing system optimization and support services.

Market participants should prioritize development of integrated solutions combining HVAC systems with renewable energy sources and smart building technologies. Investment in R&D focusing on artificial intelligence, IoT connectivity, and energy optimization will differentiate offerings in an increasingly competitive market environment.

Service capabilities represent critical success factors as customers seek comprehensive support throughout system lifecycles. Companies should develop digital service platforms enabling remote monitoring, predictive maintenance, and performance optimization to create recurring revenue streams and strengthen customer relationships.

Regional strategies should account for varying climate conditions, economic factors, and regulatory requirements across different Italian regions. Northern Italy requires focus on heating solutions while southern regions emphasize cooling applications, necessitating tailored product portfolios and marketing approaches.

Partnership strategies with local installers, distributors, and technology providers can accelerate market penetration and improve service delivery capabilities. Training programs for installation and maintenance personnel will address skilled labor shortages while ensuring proper system implementation and customer satisfaction.

Long-term growth prospects for Italy’s HVAC market remain positive, supported by ongoing building renovation activities, energy efficiency mandates, and technological advancement. The market will continue evolving toward intelligent, connected systems that provide superior comfort, efficiency, and environmental performance.

Technology integration will accelerate with artificial intelligence, machine learning, and IoT capabilities becoming standard features in premium HVAC systems. Renewable energy coupling will expand as solar panels, geothermal systems, and energy storage become more affordable and accessible to Italian consumers.

Market consolidation may occur as smaller manufacturers struggle to compete with technology investments required for next-generation products. Service-oriented business models will gain prominence as companies seek recurring revenue streams and customers value ongoing system optimization and support.

Regulatory evolution will continue driving market development through stricter efficiency standards, carbon reduction requirements, and building performance mandates. The Italian HVAC market is projected to maintain steady growth momentum with increasing emphasis on sustainability, intelligence, and user-centric design principles that define the future of climate control technology.

Italy’s HVAC market demonstrates remarkable resilience and growth potential driven by regulatory support, technological innovation, and evolving consumer preferences toward sustainable climate solutions. The market benefits from strong government incentives, growing environmental awareness, and increasing demand for smart building technologies that create substantial opportunities for industry participants.

Key success factors include technology differentiation, service excellence, and regional market understanding that enables companies to address diverse customer needs across Italy’s varied climate zones and economic conditions. The transition toward electrification and renewable energy integration represents both challenges and opportunities for market participants willing to invest in next-generation technologies.

Future market development will be characterized by increased intelligence, connectivity, and sustainability as Italian consumers and businesses prioritize energy efficiency, environmental responsibility, and enhanced comfort control. Companies that successfully navigate these trends while building strong service capabilities and regional partnerships will be well-positioned to capitalize on Italy’s evolving HVAC market landscape.

What is HVAC?

HVAC stands for Heating, Ventilation, and Air Conditioning, which refers to the technology used for indoor environmental comfort. It encompasses systems that provide heating and cooling to residential, commercial, and industrial buildings.

What are the key players in the Italy HVAC Market?

Key players in the Italy HVAC Market include companies like Daikin, Mitsubishi Electric, and Carrier, which offer a range of heating and cooling solutions. These companies are known for their innovative technologies and energy-efficient products, among others.

What are the main drivers of growth in the Italy HVAC Market?

The main drivers of growth in the Italy HVAC Market include increasing demand for energy-efficient systems, rising construction activities, and a growing focus on indoor air quality. Additionally, government initiatives promoting sustainable building practices are contributing to market expansion.

What challenges does the Italy HVAC Market face?

The Italy HVAC Market faces challenges such as high installation and maintenance costs, as well as regulatory compliance issues related to energy efficiency standards. Additionally, the market is impacted by fluctuating raw material prices and competition from alternative cooling solutions.

What opportunities exist in the Italy HVAC Market?

Opportunities in the Italy HVAC Market include the growing trend of smart home technologies and the increasing adoption of renewable energy sources. Furthermore, advancements in HVAC technology, such as IoT integration, present new avenues for growth.

What trends are shaping the Italy HVAC Market?

Trends shaping the Italy HVAC Market include a shift towards eco-friendly refrigerants, the rise of smart HVAC systems, and an emphasis on energy efficiency. Additionally, there is a growing interest in retrofitting existing systems to improve performance and reduce environmental impact.

Italy HVAC Market

| Segmentation Details | Description |

|---|---|

| Product Type | Air Conditioners, Heat Pumps, Furnaces, Ventilation Systems |

| Technology | Inverter, Ductless, Smart Thermostats, Geothermal |

| End User | Residential, Commercial, Industrial, Hospitality |

| Installation | Centralized, Decentralized, Retrofit, New Construction |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Italy HVAC Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.