444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The inland container depot and dry port market represents a critical component of global logistics infrastructure, facilitating efficient cargo movement between seaports and inland destinations. These specialized facilities serve as intermediate hubs that extend port capabilities inland, reducing congestion at coastal ports while improving supply chain efficiency. Market dynamics indicate robust growth driven by increasing international trade volumes, urbanization pressures, and the need for sustainable transportation solutions.

Regional expansion of inland container depots has accelerated significantly, with developing economies investing heavily in dry port infrastructure to support economic growth. The market demonstrates strong momentum with projected growth rates of 8.2% CAGR through the forecast period, reflecting increasing recognition of these facilities’ strategic importance in modern logistics networks.

Technology integration within inland container depots continues advancing, incorporating automated handling systems, digital tracking solutions, and smart logistics platforms. These innovations enhance operational efficiency while reducing processing times and operational costs. Sustainability initiatives are increasingly driving market development, with facilities adopting green technologies and supporting modal shift from road to rail transportation.

The inland container depot and dry port market refers to the comprehensive ecosystem of inland facilities that provide container handling, storage, and logistics services away from traditional seaports. These facilities function as extended gateways, offering customs clearance, container maintenance, and multimodal transportation connections to support efficient cargo flow between international shipping routes and domestic distribution networks.

Dry ports specifically represent inland intermodal terminals directly connected to seaports via high-capacity transportation modes, typically rail or dedicated truck corridors. They provide seaport services at inland locations, including customs processing, container inspection, and temporary storage capabilities. Inland container depots encompass a broader category of facilities that may serve multiple functions including empty container repositioning, maintenance services, and regional distribution support.

Strategic positioning of these facilities creates significant value by decongesting coastal ports, reducing transportation costs, and improving supply chain resilience. They enable efficient cargo consolidation and deconsolidation while providing essential services that support international trade facilitation and domestic logistics optimization.

Market expansion in the inland container depot and dry port sector reflects fundamental shifts in global trade patterns and logistics requirements. Growing containerized cargo volumes, estimated to increase by 6.5% annually, drive demand for expanded inland handling capabilities. Infrastructure development initiatives across emerging markets particularly support market growth as governments recognize the economic benefits of efficient inland logistics hubs.

Technological advancement represents a key market differentiator, with facilities increasingly adopting automated systems, IoT sensors, and digital platforms to enhance operational efficiency. Sustainability concerns influence market development significantly, with approximately 72% of new facilities incorporating environmental considerations into their design and operations.

Regional diversification characterizes current market trends, with Asia-Pacific maintaining dominant market share while North America and Europe experience steady growth in facility modernization and capacity expansion. Public-private partnerships increasingly drive development projects, combining government infrastructure investment with private sector operational expertise to create efficient, sustainable inland logistics solutions.

Strategic location selection emerges as the primary success factor for inland container depot development, with proximity to major transportation corridors and industrial centers determining facility viability. MarkWide Research analysis indicates that facilities located within economic corridors demonstrate 40% higher utilization rates compared to standalone operations.

International trade growth serves as the fundamental driver for inland container depot expansion, with global containerized trade volumes continuing upward trajectory despite periodic disruptions. Port congestion at major coastal facilities creates urgent need for inland alternatives that can handle overflow capacity while maintaining service quality.

Urbanization pressures in coastal areas drive the relocation of logistics activities to inland locations where land costs remain manageable and environmental impacts can be better controlled. Government infrastructure initiatives across developing economies prioritize inland connectivity projects that support economic development and trade facilitation.

Supply chain resilience requirements, highlighted by recent global disruptions, encourage shippers to diversify their logistics networks through inland depot utilization. Environmental regulations increasingly favor inland facilities that can support modal shift from road to rail transportation, reducing carbon emissions and traffic congestion.

E-commerce growth creates demand for strategically located inland facilities that can support last-mile distribution networks while maintaining connection to international supply chains. Manufacturing relocation to inland areas, driven by cost considerations and government incentives, generates additional demand for nearby container handling capabilities.

High capital requirements for inland container depot development create significant barriers to entry, particularly for smaller operators seeking to establish new facilities. Infrastructure limitations in many regions, including inadequate rail connections and road networks, constrain facility development and operational efficiency.

Regulatory complexity surrounding customs operations, environmental compliance, and zoning requirements can delay project development and increase operational costs. Competition from established seaports that expand their own capacity and improve efficiency may reduce demand for inland alternatives in some markets.

Technology integration challenges require significant investment in systems and staff training, creating operational disruptions during implementation periods. Skilled labor shortages in logistics and technology sectors limit facility operational capabilities and growth potential.

Economic volatility affecting international trade volumes can impact facility utilization rates and revenue stability. Environmental concerns from local communities may create opposition to facility development, particularly in densely populated areas or environmentally sensitive locations.

Emerging market expansion presents substantial opportunities as developing economies invest in trade infrastructure to support economic growth. Belt and Road Initiative and similar international connectivity projects create demand for inland logistics facilities along new trade corridors.

Technology partnerships with automation providers, software developers, and logistics technology companies enable facility operators to enhance capabilities while sharing development costs. Green logistics initiatives create opportunities for facilities that can demonstrate environmental benefits and support corporate sustainability goals.

Public-private collaboration models enable facility development with shared investment and risk, particularly attractive for large-scale projects requiring significant infrastructure investment. Regional trade agreements that facilitate cross-border commerce increase demand for efficient inland customs and logistics processing capabilities.

Value-added service expansion including light manufacturing, packaging, and quality control services can significantly enhance facility revenue streams. Digital platform development creates opportunities to serve as logistics orchestrators, coordinating complex supply chain activities across multiple stakeholders.

Competitive intensity in the inland container depot market varies significantly by region, with established markets experiencing consolidation while emerging markets offer opportunities for new entrants. Service differentiation increasingly determines competitive advantage, with facilities competing on technology capabilities, processing speed, and value-added services rather than basic handling rates.

Customer expectations continue evolving toward integrated logistics solutions that provide visibility, flexibility, and reliability across the entire supply chain. Operational efficiency improvements through automation and digitalization enable facilities to handle growing cargo volumes while controlling labor costs and improving service quality.

Partnership strategies between inland depots, seaports, and transportation providers create integrated networks that offer seamless cargo flow and shared marketing advantages. Regulatory harmonization efforts in various regions simplify cross-border operations and reduce compliance complexity for facility operators.

Investment patterns show increasing preference for facilities that demonstrate strong environmental, social, and governance credentials, reflecting broader sustainability trends in logistics and infrastructure development. Market consolidation trends favor operators with strong financial resources and technology capabilities who can invest in facility modernization and expansion.

Primary research for inland container depot market analysis encompasses comprehensive interviews with facility operators, logistics service providers, port authorities, and government officials across major markets. Data collection methods include structured surveys, expert interviews, and facility site visits to gather operational insights and performance metrics.

Secondary research incorporates analysis of government trade statistics, port authority reports, industry publications, and company financial statements to establish market baselines and trend analysis. Market modeling techniques combine quantitative data with qualitative insights to project growth scenarios and identify key market drivers.

Geographic coverage spans major container shipping regions including Asia-Pacific, North America, Europe, Latin America, and emerging markets in Africa and the Middle East. Stakeholder analysis examines the perspectives and requirements of shippers, logistics providers, government agencies, and local communities affected by inland depot development.

Validation processes include cross-referencing multiple data sources, expert review panels, and market participant feedback to ensure accuracy and reliability of research findings. Trend analysis incorporates historical data spanning multiple economic cycles to identify sustainable growth patterns and cyclical variations in market performance.

Asia-Pacific region dominates the global inland container depot market, accounting for approximately 58% of global capacity, driven by China’s extensive inland logistics network and India’s growing infrastructure development. China’s inland depot network continues expanding rapidly, with new facilities supporting the country’s western development strategy and Belt and Road connectivity initiatives.

North America demonstrates steady market growth focused on facility modernization and capacity optimization rather than extensive new construction. United States inland ports benefit from strong intermodal rail networks and growing e-commerce distribution requirements, while Mexico’s border facilities support increasing nearshoring trends.

European market emphasizes sustainability and efficiency improvements, with facilities increasingly incorporating renewable energy and automated handling systems. Eastern European expansion supports growing trade volumes with Asia while Western European facilities focus on digitalization and service enhancement.

Latin America shows promising growth potential with Brazil and Colombia leading infrastructure development initiatives. Middle East and Africa represent emerging opportunities, with countries like UAE, Saudi Arabia, and South Africa investing in inland logistics capabilities to support economic diversification and trade facilitation goals.

Market leadership in the inland container depot sector includes both global logistics companies and regional specialists who understand local market conditions and regulatory requirements. Competitive positioning increasingly depends on technology capabilities, sustainability credentials, and integrated service offerings.

Strategic partnerships between terminal operators, rail companies, and logistics providers create competitive advantages through integrated service offerings and shared infrastructure investments. Technology differentiation increasingly separates market leaders from followers, with advanced facilities offering superior visibility, efficiency, and customer experience.

By Service Type: The market segments into full-service dry ports offering comprehensive customs and logistics capabilities, basic inland container depots providing storage and handling services, and specialized facilities focused on specific cargo types or value-added services. Full-service facilities command premium pricing but require higher capital investment and regulatory compliance.

By Transportation Mode: Rail-connected facilities dominate in markets with strong intermodal networks, while road-based facilities serve areas with limited rail infrastructure. Multimodal facilities integrating rail, road, and sometimes inland waterway connections demonstrate highest growth potential and operational flexibility.

By Ownership Structure: Public sector facilities focus on economic development and trade facilitation, while private operators emphasize profitability and operational efficiency. Public-private partnerships combine government infrastructure investment with private sector operational expertise, representing approximately 35% of new developments.

By Geographic Location: Border facilities serve international trade corridors, metropolitan area depots support urban distribution networks, and industrial zone facilities serve manufacturing clusters. Strategic location selection determines facility success more than ownership structure or service offerings.

Full-Service Dry Ports: These comprehensive facilities provide the highest value proposition by offering complete port services at inland locations. Customs integration capabilities enable direct cargo clearance, reducing supply chain complexity and transit times. Revenue potential remains highest in this category, but operational complexity and regulatory requirements create significant barriers to entry.

Basic Container Depots: Focused on storage and handling services, these facilities serve as cost-effective solutions for cargo consolidation and empty container management. Operational simplicity enables faster development and lower capital requirements, making them attractive for regional operators and emerging markets.

Specialized Facilities: Dedicated to specific cargo types such as automotive, agricultural products, or hazardous materials, these facilities command premium rates through specialized handling capabilities. Market niches provide protection from general competition while requiring specific expertise and equipment investments.

Value-Added Service Centers: Facilities incorporating light manufacturing, packaging, quality control, and distribution services generate higher revenue per container while supporting supply chain optimization. Service integration creates competitive advantages and customer loyalty through comprehensive logistics solutions.

Shippers and Importers benefit from reduced logistics costs, improved supply chain flexibility, and faster cargo processing through inland depot utilization. Cost savings of up to 25% in total logistics expenses can be achieved through strategic inland depot integration, particularly for high-volume shippers with predictable cargo flows.

Port Authorities gain capacity relief and improved operational efficiency by extending their service networks inland. Revenue enhancement opportunities arise through partnership arrangements and shared service offerings that maintain customer relationships while reducing facility congestion.

Transportation Providers benefit from improved asset utilization and reduced empty repositioning costs through inland depot networks. Rail operators particularly benefit from increased intermodal volumes and more efficient equipment cycling between coastal and inland locations.

Government Agencies achieve economic development objectives through job creation, tax revenue generation, and improved trade facilitation. Environmental benefits include reduced truck traffic in urban areas and lower carbon emissions through modal shift to rail transportation.

Local Communities benefit from employment opportunities, infrastructure improvements, and economic development while potentially experiencing reduced truck traffic and environmental impacts compared to coastal port expansion alternatives.

Strengths:

Weaknesses:

Opportunities:

Threats:

Digitalization acceleration transforms inland depot operations through IoT sensors, blockchain documentation, and artificial intelligence applications. MWR research indicates that 78% of new facilities incorporate comprehensive digital platforms from initial operations, compared to gradual adoption in older facilities.

Sustainability integration becomes standard practice rather than optional enhancement, with facilities incorporating renewable energy, green building standards, and carbon footprint reduction programs. Environmental certification increasingly influences customer selection criteria and government approval processes.

Automation adoption accelerates across handling operations, documentation processes, and facility management systems. Labor cost pressures and efficiency requirements drive investment in automated guided vehicles, robotic systems, and smart gate technologies.

Service diversification expands beyond basic container handling to include value-added logistics services, light manufacturing, and supply chain orchestration capabilities. Revenue optimization strategies focus on maximizing facility utilization through complementary service offerings.

Regional network development creates integrated inland depot systems serving multiple markets through coordinated operations and shared resources. Network effects provide competitive advantages and operational efficiencies that standalone facilities cannot achieve.

Infrastructure investment programs across multiple countries prioritize inland connectivity projects supporting economic development and trade facilitation. China’s western development strategy continues expanding inland depot networks while India’s infrastructure initiatives focus on improving connectivity between ports and industrial centers.

Technology partnerships between facility operators and solution providers accelerate innovation adoption and reduce implementation costs. Strategic alliances enable smaller operators to access advanced technologies while technology companies gain market access and operational insights.

Regulatory harmonization efforts in various regions simplify cross-border operations and reduce compliance complexity. Digital customs initiatives enable paperless processing and real-time cargo tracking, improving efficiency and reducing processing times.

Sustainability certifications become standard requirements for new facility development, with green building standards and environmental impact assessments mandatory in most markets. Carbon neutrality commitments from major logistics companies drive demand for environmentally responsible inland depot services.

Public-private partnership models evolve to address infrastructure financing challenges while ensuring operational efficiency. Risk-sharing arrangements enable large-scale projects that neither public nor private sectors could undertake independently.

Strategic location selection should prioritize proximity to major transportation corridors, industrial clusters, and population centers rather than lowest land costs. Market analysis indicates that well-located facilities achieve 60% higher utilization rates and command premium pricing despite higher initial investment costs.

Technology investment should focus on scalable platforms that can evolve with market requirements rather than point solutions addressing specific operational challenges. Digital integration capabilities increasingly determine competitive positioning and customer satisfaction levels.

Partnership development with seaports, rail operators, and logistics service providers creates competitive advantages through integrated service offerings and shared marketing efforts. Collaborative approaches reduce individual investment requirements while enhancing service capabilities.

Sustainability planning should be integrated from initial facility design rather than retrofitted later, as environmental requirements continue strengthening across all markets. Green credentials increasingly influence customer selection and government approval processes.

Service diversification beyond basic container handling creates revenue stability and competitive differentiation, particularly important during economic downturns or trade disruptions. Value-added services provide higher margins and stronger customer relationships than commodity handling operations.

Market expansion will continue driven by international trade growth, urbanization pressures, and infrastructure development initiatives across emerging economies. Growth projections indicate sustained expansion at 8.2% CAGR through the next decade, with emerging markets contributing disproportionately to capacity additions.

Technology integration will accelerate across all facility operations, with artificial intelligence, blockchain, and IoT becoming standard rather than innovative features. Automation levels are expected to reach 85% of handling operations in new facilities by 2030, driven by labor cost pressures and efficiency requirements.

Sustainability requirements will become mandatory rather than voluntary, with carbon neutrality and environmental certification standard for new developments. Green logistics initiatives will drive modal shift toward rail transportation and renewable energy adoption across facility operations.

Regional integration will create coordinated inland depot networks serving multiple markets through shared resources and standardized operations. Network development will favor operators with strong financial resources and technology capabilities who can invest in multi-facility systems.

Service evolution will transform inland depots from basic handling facilities to comprehensive logistics orchestrators providing integrated supply chain solutions. MarkWide Research projects that 65% of facilities will offer value-added services beyond container handling by 2028, reflecting changing customer requirements and competitive pressures.

The inland container depot and dry port market represents a dynamic and essential component of global logistics infrastructure, positioned for continued growth driven by international trade expansion, urbanization pressures, and sustainability requirements. Market fundamentals remain strong with increasing recognition of these facilities’ strategic value in modern supply chains.

Technology advancement and sustainability integration will define competitive success in the coming decade, as facilities that embrace digitalization and environmental responsibility gain advantages in customer attraction and regulatory compliance. Strategic positioning through location selection, service diversification, and partnership development will determine long-term viability and profitability.

Regional opportunities vary significantly, with emerging markets offering substantial growth potential while developed markets focus on modernization and efficiency improvements. Investment strategies should consider local market conditions, regulatory environments, and infrastructure capabilities when evaluating development opportunities.

Future success in the inland container depot market will require balanced focus on operational efficiency, technology integration, sustainability compliance, and customer service excellence. Market leaders will be those who can adapt to changing requirements while maintaining cost-effective operations and strong stakeholder relationships across the complex logistics ecosystem.

What is Inland Container Depot and Dry Port?

An Inland Container Depot and Dry Port is a facility that serves as a hub for the transfer of cargo containers between different modes of transport, such as trucks and trains, facilitating efficient logistics and supply chain operations.

What are the key players in the Inland Container Depot and Dry Port Market?

Key players in the Inland Container Depot and Dry Port Market include DP World, APM Terminals, and Container Corporation of India, among others.

What are the main drivers of growth in the Inland Container Depot and Dry Port Market?

The growth of the Inland Container Depot and Dry Port Market is driven by increasing international trade, the need for efficient logistics solutions, and the expansion of e-commerce, which demands faster and more reliable transportation options.

What challenges does the Inland Container Depot and Dry Port Market face?

Challenges in the Inland Container Depot and Dry Port Market include infrastructure limitations, regulatory hurdles, and competition from alternative transport modes, which can impact operational efficiency.

What opportunities exist in the Inland Container Depot and Dry Port Market?

Opportunities in the Inland Container Depot and Dry Port Market include the development of smart logistics technologies, increased investment in infrastructure, and the potential for expansion into emerging markets.

What trends are shaping the Inland Container Depot and Dry Port Market?

Trends in the Inland Container Depot and Dry Port Market include the adoption of automation and digitalization, a focus on sustainability practices, and the integration of multimodal transport solutions to enhance efficiency.

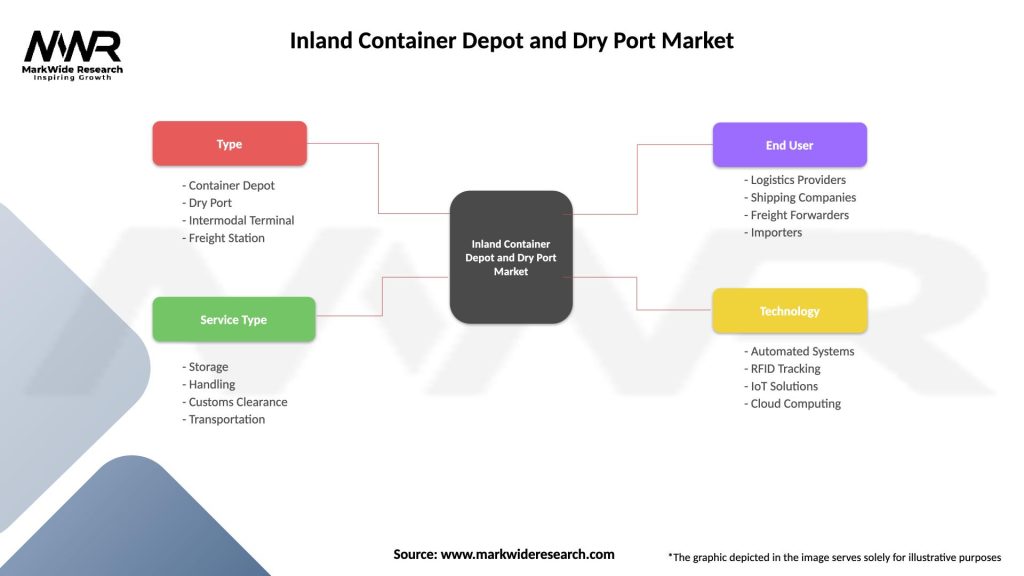

Inland Container Depot and Dry Port Market

| Segmentation Details | Description |

|---|---|

| Type | Container Depot, Dry Port, Intermodal Terminal, Freight Station |

| Service Type | Storage, Handling, Customs Clearance, Transportation |

| End User | Logistics Providers, Shipping Companies, Freight Forwarders, Importers |

| Technology | Automated Systems, RFID Tracking, IoT Solutions, Cloud Computing |

Please note: The segmentation can be entirely customized to align with our client’s needs.

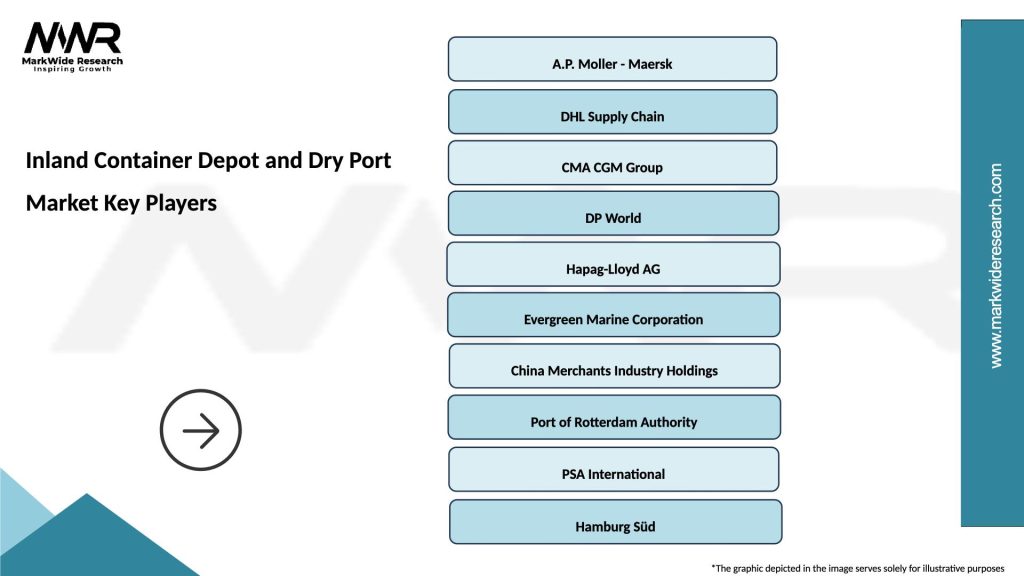

Leading companies in the Inland Container Depot and Dry Port Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

North America

o US

o Canada

o Mexico

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA