444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

Market Overview

The Industrial Non IC Card Water Smart Meter Sales Market involves the distribution and adoption of smart metering solutions specifically designed for industrial water consumption monitoring and management. These meters utilize advanced technology to accurately measure water usage, promote efficiency, and enable data-driven decision-making in industries such as manufacturing, mining, and utilities.

Meaning

Industrial Non IC Card Water Smart Meters are sophisticated devices used for measuring and monitoring water consumption in industrial settings without requiring insertion or interaction with an integrated circuit (IC) card. These meters employ smart technology to provide real-time data on water usage, improve billing accuracy, detect leaks, and optimize water resource management in industrial facilities.

Executive Summary

The global Industrial Non IC Card Water Smart Meter Sales Market is experiencing significant growth driven by the need for efficient water management solutions, regulatory pressures on water conservation, and advancements in IoT (Internet of Things) technology. Key market players are focusing on innovation, strategic partnerships, and expanding their product portfolios to capitalize on emerging opportunities across diverse industrial sectors.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Market Drivers

Market Restraints

Market Opportunities

Market Dynamics

The Industrial Non IC Card Water Smart Meter Sales Market is influenced by several dynamic factors:

Regional Analysis

The global Industrial Non IC Card Water Smart Meter Sales Market can be segmented into key regions:

Competitive Landscape

Leading Companies in Industrial Non IC Card Water Smart Meter Sales Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Segmentation

The market can be segmented based on:

Category-wise Insights

Key Benefits for Industry Participants and Stakeholders

Industry participants benefit from:

SWOT Analysis

Strengths:

Weaknesses:

Opportunities:

Threats:

Market Key Trends

Covid-19 Impact

The Covid-19 pandemic has influenced the Industrial Non IC Card Water Smart Meter Sales Market:

Key Industry Developments

Analyst Suggestions

Based on market trends and developments, analysts suggest the following strategies:

Future Outlook

The future outlook for the Industrial Non IC Card Water Smart Meter Sales Market is optimistic, driven by increasing industrialization, urbanization, and sustainability initiatives worldwide. Continued advancements in smart metering technologies, along with supportive regulatory frameworks and strategic partnerships, are expected to propel market growth and adoption across diverse industrial applications.

Conclusion

In conclusion, the Industrial Non IC Card Water Smart Meter Sales Market is poised for significant growth, driven by the imperative for water conservation, regulatory compliance, and operational efficiency in industrial sectors. Despite challenges posed by initial costs, technical complexities, and market competition, smart metering solutions offer substantial benefits in terms of resource optimization, cost savings, and environmental sustainability. Industry stakeholders can capitalize on emerging opportunities through innovation, strategic partnerships, and proactive market strategies to achieve sustainable growth and leadership in the global smart metering market.

What is Industrial Non IC Card Water Smart Meter?

Industrial Non IC Card Water Smart Meters are advanced devices used for measuring water consumption in industrial settings without the use of integrated circuit cards. They provide accurate readings, facilitate remote monitoring, and help in efficient water management.

What are the key players in the Industrial Non IC Card Water Smart Meter Sales Market?

Key players in the Industrial Non IC Card Water Smart Meter Sales Market include companies like Itron, Sensus, and Kamstrup, which are known for their innovative metering solutions and technologies, among others.

What are the growth factors driving the Industrial Non IC Card Water Smart Meter Sales Market?

The growth of the Industrial Non IC Card Water Smart Meter Sales Market is driven by increasing demand for efficient water management, the need for accurate billing systems, and the rising awareness of water conservation practices in various industries.

What challenges does the Industrial Non IC Card Water Smart Meter Sales Market face?

Challenges in the Industrial Non IC Card Water Smart Meter Sales Market include high initial installation costs, the need for skilled personnel for maintenance, and potential resistance from industries accustomed to traditional metering methods.

What opportunities exist in the Industrial Non IC Card Water Smart Meter Sales Market?

Opportunities in the Industrial Non IC Card Water Smart Meter Sales Market include advancements in IoT technology, increasing government initiatives for smart water management, and the potential for integration with renewable energy sources for enhanced efficiency.

What trends are shaping the Industrial Non IC Card Water Smart Meter Sales Market?

Trends in the Industrial Non IC Card Water Smart Meter Sales Market include the adoption of smart grid technologies, the integration of data analytics for better decision-making, and the growing emphasis on sustainability and environmental impact reduction.

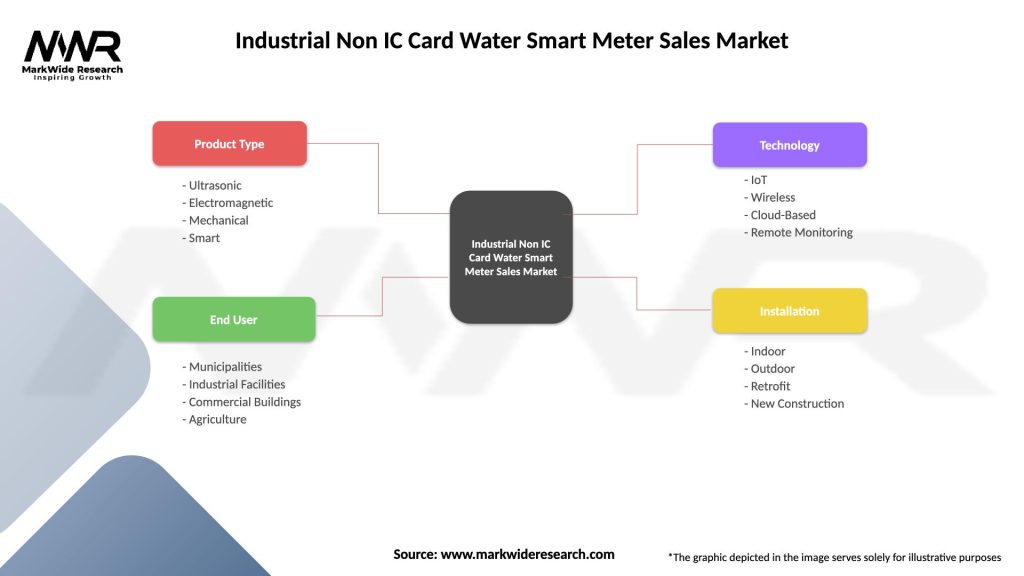

Industrial Non IC Card Water Smart Meter Sales Market

| Segmentation Details | Description |

|---|---|

| Product Type | Ultrasonic, Electromagnetic, Mechanical, Smart |

| End User | Municipalities, Industrial Facilities, Commercial Buildings, Agriculture |

| Technology | IoT, Wireless, Cloud-Based, Remote Monitoring |

| Installation | Indoor, Outdoor, Retrofit, New Construction |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

North America

o US

o Canada

o Mexico

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA