444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Indian power market stands as one of the world’s most dynamic and rapidly evolving energy sectors, representing a critical component of the nation’s economic infrastructure. India’s electricity sector has undergone remarkable transformation over the past decade, driven by ambitious government initiatives, technological advancements, and increasing energy demands from both industrial and residential consumers. The market encompasses diverse power generation sources, including thermal, renewable, nuclear, and hydroelectric facilities, creating a complex ecosystem that serves over 1.4 billion people.

Market dynamics in the Indian power sector reflect the country’s commitment to achieving energy security while transitioning toward sustainable power generation. The sector has witnessed substantial growth in renewable energy capacity, with solar and wind power installations experiencing unprecedented expansion. Government policies such as the National Solar Mission and various state-level renewable energy mandates have catalyzed this transformation, positioning India as a global leader in clean energy adoption.

Infrastructure development remains a cornerstone of the Indian power market, with significant investments in transmission and distribution networks. The market demonstrates robust growth potential, with electricity consumption growing at approximately 5.2% annually, reflecting the nation’s industrial expansion and improving rural electrification rates. Power generation capacity has expanded significantly, with renewable energy sources now contributing over 28% of total installed capacity, marking a substantial shift from traditional fossil fuel dependence.

The Indian power market refers to the comprehensive ecosystem encompassing electricity generation, transmission, distribution, and consumption across the Indian subcontinent. This market includes all stakeholders involved in the power value chain, from independent power producers and state electricity boards to transmission companies and end consumers. Power market dynamics in India operate within a complex regulatory framework that balances federal and state jurisdictions, creating unique challenges and opportunities for market participants.

Market structure in the Indian power sector combines both regulated and competitive elements, with electricity trading occurring through various mechanisms including bilateral contracts, power exchanges, and open access arrangements. The market encompasses diverse generation technologies, ranging from conventional thermal power plants to cutting-edge renewable energy installations, reflecting India’s commitment to energy diversification and sustainability.

Regulatory oversight is provided by the Central Electricity Regulatory Commission and various State Electricity Regulatory Commissions, ensuring fair market practices and consumer protection. The market’s evolution reflects India’s broader economic development goals, energy security objectives, and environmental commitments under international climate agreements.

India’s power market represents a transformative sector experiencing unprecedented growth and modernization. The market has demonstrated remarkable resilience and adaptability, successfully navigating challenges related to fuel supply, environmental regulations, and evolving consumer demands. Renewable energy integration has emerged as a defining characteristic, with solar and wind power installations contributing significantly to the nation’s generation capacity expansion.

Key market drivers include rapid urbanization, industrial growth, government electrification initiatives, and increasing focus on energy efficiency. The sector has witnessed substantial improvements in operational efficiency, with transmission and distribution losses decreasing to approximately 18.4%, though further optimization remains a priority. Digital transformation initiatives, including smart grid deployments and advanced metering infrastructure, are reshaping market operations and customer engagement.

Investment flows into the Indian power sector continue to strengthen, with both domestic and international investors recognizing the market’s long-term potential. The sector’s evolution toward a more competitive and transparent marketplace has created new opportunities for private sector participation while maintaining essential public service obligations. Energy storage solutions and grid modernization projects are gaining momentum, supporting the integration of variable renewable energy sources.

Strategic insights from the Indian power market reveal several critical trends shaping the sector’s future trajectory. The market demonstrates strong fundamentals driven by consistent demand growth, supportive policy frameworks, and technological innovation across the power value chain.

Primary market drivers in the Indian power sector stem from fundamental economic and demographic trends that create sustained demand for electricity infrastructure and services. Rapid urbanization continues to drive residential and commercial power consumption, with urban areas experiencing consistent growth in electricity demand across all consumer categories.

Industrial expansion represents a significant driver, with manufacturing sector growth, particularly in energy-intensive industries such as steel, aluminum, and chemicals, creating substantial electricity demand. The emergence of new industries, including electric vehicle manufacturing and data centers, is generating additional power requirements while driving demand for reliable and clean energy sources.

Government initiatives play a crucial role in market development, with policies promoting renewable energy adoption, rural electrification, and energy efficiency creating new market opportunities. The Atmanirbhar Bharat initiative has emphasized domestic manufacturing capabilities in the power sector, reducing import dependence and strengthening local supply chains.

Environmental regulations and climate commitments are driving the transition toward cleaner power generation technologies. India’s commitment to achieving 50% renewable energy capacity by 2030 has created substantial market opportunities for solar, wind, and energy storage technologies. Carbon reduction targets are influencing investment decisions and technology choices across the power value chain.

Significant challenges continue to impact the Indian power market despite its overall positive trajectory. Financial stress among state electricity boards remains a persistent concern, with accumulated losses affecting their ability to invest in infrastructure upgrades and purchase power at competitive rates. This financial strain creates ripple effects throughout the power value chain, impacting generator revenues and limiting system improvements.

Grid integration challenges pose technical constraints, particularly as renewable energy penetration increases. The intermittent nature of solar and wind power requires substantial investments in grid flexibility, energy storage, and demand response systems. Transmission bottlenecks in certain regions limit the efficient movement of power from generation centers to demand centers, creating market inefficiencies.

Land acquisition difficulties continue to delay power project development, particularly for large-scale solar and wind installations. Complex approval processes and environmental clearances can extend project timelines significantly, affecting investor confidence and project economics. Fuel supply constraints for thermal power plants, including coal transportation and quality issues, create operational challenges and cost pressures.

Regulatory complexities arising from the federal structure of electricity governance can create coordination challenges between central and state authorities. Varying state policies and regulations can complicate multi-state project development and power trading arrangements.

Emerging opportunities in the Indian power market span across multiple segments, driven by technological advancement, policy support, and evolving consumer needs. Energy storage systems represent a particularly promising opportunity, with battery costs declining and grid integration requirements increasing. The market for utility-scale storage solutions is expected to expand rapidly as renewable energy penetration grows.

Distributed energy resources offer substantial growth potential, including rooftop solar installations, microgrids, and behind-the-meter storage systems. The combination of declining technology costs and supportive net metering policies creates favorable conditions for distributed generation adoption across residential and commercial segments.

Electric vehicle infrastructure development presents new market opportunities as India pursues aggressive EV adoption targets. Charging infrastructure deployment will require substantial electricity infrastructure investments and create new demand patterns that favor flexible and clean power sources.

Green hydrogen production is emerging as a significant opportunity, with India positioning itself as a global hub for renewable hydrogen manufacturing. This sector could drive substantial additional renewable energy demand while creating export opportunities. Energy efficiency services continue to expand, with performance contracting models gaining acceptance across industrial and commercial sectors.

Complex market dynamics characterize the Indian power sector, reflecting the interplay between supply-side developments, demand growth patterns, and regulatory evolution. Supply-demand balance has improved significantly in recent years, with generation capacity additions outpacing demand growth, creating opportunities for more competitive power procurement and improved system reliability.

Price dynamics in the power market demonstrate increasing competitiveness, particularly for renewable energy sources. Solar and wind power tariffs have achieved grid parity in many regions, making renewable energy the preferred choice for new capacity additions. Power exchange trading volumes have grown substantially, reaching approximately 8.5% of total electricity consumption, indicating increasing market liquidity and price discovery mechanisms.

Technology disruption is reshaping market dynamics across all segments. Digital technologies, including artificial intelligence and machine learning, are optimizing power plant operations, grid management, and consumer services. Blockchain applications for peer-to-peer energy trading and renewable energy certificate management are gaining experimental traction.

Consumer behavior evolution reflects increasing awareness of energy choices and sustainability considerations. Commercial and industrial consumers are increasingly pursuing renewable energy procurement through various mechanisms, including open access arrangements and captive power development. Prosumer trends are emerging as distributed generation adoption increases, creating bidirectional power flows and new market dynamics.

Comprehensive research methodology employed for analyzing the Indian power market incorporates multiple data sources and analytical approaches to ensure accuracy and reliability. Primary research includes extensive interviews with industry stakeholders, including power generators, transmission companies, distribution utilities, equipment manufacturers, and regulatory officials.

Secondary research encompasses analysis of government publications, regulatory filings, industry reports, and financial statements from key market participants. Data validation processes ensure consistency and accuracy across multiple sources, with particular attention to capacity additions, generation statistics, and financial performance metrics.

Market modeling techniques incorporate both bottom-up and top-down approaches, analyzing demand drivers, supply-side developments, and policy impacts. Scenario analysis considers various growth trajectories and policy outcomes to provide comprehensive market projections. MarkWide Research analytical frameworks integrate quantitative and qualitative insights to deliver actionable market intelligence.

Regional analysis methodology accounts for significant variations in market conditions across different Indian states, including resource availability, policy frameworks, and demand characteristics. Technology assessment incorporates learning curve analysis and cost projections for various power generation and storage technologies.

Regional market dynamics across India demonstrate significant variations in power sector development, resource endowments, and policy approaches. Western India, including states like Gujarat, Maharashtra, and Rajasthan, leads in renewable energy development, accounting for approximately 45% of total solar capacity installations. These states benefit from excellent solar resources, supportive state policies, and well-developed transmission infrastructure.

Southern India represents a mature power market with states like Tamil Nadu, Karnataka, and Andhra Pradesh demonstrating strong renewable energy adoption and progressive regulatory frameworks. The region accounts for roughly 35% of wind power capacity, leveraging favorable wind resources along coastal areas. Power trading activity is particularly robust in southern states, with active participation in electricity exchanges.

Northern India encompasses major demand centers including Delhi, Punjab, and Uttar Pradesh, with substantial thermal power capacity and growing renewable energy installations. The region faces unique challenges related to air quality concerns and agricultural power subsidies, influencing market dynamics and policy decisions.

Eastern India contains significant coal resources and thermal power generation capacity, while also developing renewable energy projects. States like West Bengal and Odisha are balancing traditional thermal power operations with clean energy transitions. Northeastern states offer substantial hydroelectric potential and are increasingly connected to the national grid, creating new market opportunities.

Competitive dynamics in the Indian power market reflect a diverse ecosystem of public and private sector participants across generation, transmission, and distribution segments. The market structure combines large state-owned enterprises with growing private sector participation and international investments.

Market competition has intensified across all segments, with tariff-based competitive bidding becoming the norm for new capacity additions. Technology innovation and operational efficiency are key differentiators, with companies investing in digital technologies and advanced power plant designs.

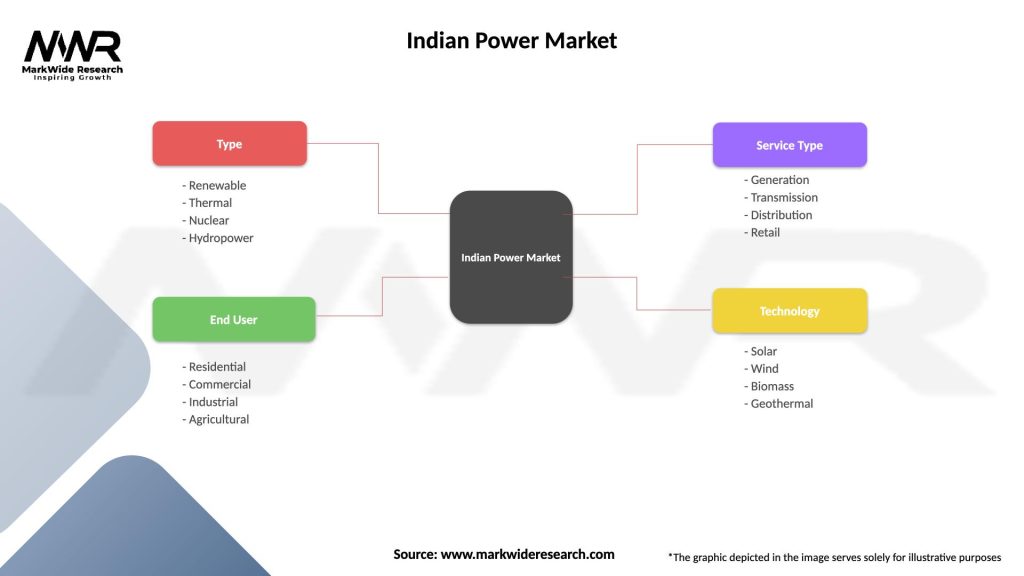

Market segmentation in the Indian power sector reflects diverse generation technologies, consumer categories, and operational models. By Generation Source, the market encompasses thermal power (coal, gas, diesel), renewable energy (solar, wind, hydro, biomass), and nuclear power, each serving specific market needs and regulatory requirements.

By Consumer Segment:

By Utility Function:

Renewable energy categories demonstrate exceptional growth dynamics within the Indian power market. Solar power has emerged as the fastest-growing segment, with capacity additions consistently exceeding targets and costs declining rapidly. Utility-scale solar projects dominate capacity additions, while rooftop solar adoption is accelerating across commercial and residential segments.

Wind power development continues to expand, particularly in states with favorable wind resources. Offshore wind represents an emerging opportunity with substantial potential along India’s extensive coastline. Technology improvements in wind turbine efficiency and capacity factors are enhancing project economics and market attractiveness.

Thermal power categories face evolving market conditions, with coal-based generation remaining dominant but experiencing slower growth rates. Supercritical and ultra-supercritical coal technologies are improving efficiency and reducing emissions from new thermal installations. Gas-based power serves peak demand and grid balancing functions, though fuel supply constraints limit expansion.

Energy storage categories are gaining momentum, with battery energy storage systems leading deployment. Pumped hydro storage projects are being developed to provide large-scale grid balancing services. Hybrid renewable projects combining solar, wind, and storage are becoming increasingly common, offering improved grid integration characteristics.

Substantial benefits accrue to various stakeholders participating in the Indian power market ecosystem. Power generators benefit from growing electricity demand, supportive policy frameworks, and access to competitive fuel sources. Long-term power purchase agreements provide revenue certainty, while competitive bidding processes ensure fair market access for efficient operators.

Equipment manufacturers and technology providers gain from substantial infrastructure investments and technology upgrades across the power value chain. Local manufacturing incentives and import substitution policies create opportunities for domestic production capabilities. Research and development investments in clean energy technologies receive government support and tax incentives.

Financial institutions and investors benefit from attractive returns in a growing market with government backing and regulatory stability. Green financing opportunities are expanding as environmental, social, and governance considerations gain prominence in investment decisions.

Consumers benefit from improved power supply reliability, competitive tariffs, and increasing access to clean energy options. Energy efficiency programs help reduce electricity costs while supporting environmental objectives. Digital services and smart grid technologies enhance customer experience and enable better energy management.

Strengths:

Weaknesses:

Opportunities:

Threats:

Transformative trends are reshaping the Indian power market landscape, driven by technological innovation, policy evolution, and changing consumer preferences. Renewable energy integration continues to accelerate, with hybrid projects combining multiple clean energy technologies becoming increasingly common. These projects offer improved capacity utilization and grid stability characteristics.

Digitalization trends are revolutionizing power sector operations, with artificial intelligence and machine learning applications optimizing generation dispatch, predictive maintenance, and demand forecasting. Smart grid deployments are expanding beyond pilot projects to commercial-scale implementations, enabling better grid management and consumer engagement.

Energy storage adoption is gaining momentum as costs decline and grid integration requirements increase. Battery storage systems are being deployed for both utility-scale and distributed applications, supporting renewable energy integration and grid stability services.

Decentralization trends are evident in growing rooftop solar adoption, microgrid development, and peer-to-peer energy trading experiments. Prosumer emergence is creating new market dynamics as consumers become electricity producers through distributed generation installations.

Sustainability focus is intensifying across all market segments, with environmental, social, and governance considerations influencing investment decisions and operational practices. Carbon accounting and emissions reduction targets are becoming standard business practices.

Recent industry developments highlight the dynamic nature of the Indian power market and its rapid evolution toward a more sustainable and efficient system. Major capacity additions in renewable energy continue to exceed government targets, with several gigawatt-scale solar and wind projects achieving commercial operation ahead of schedule.

Grid infrastructure investments have accelerated, with new transmission lines and substations improving inter-regional power transfer capabilities. The Green Energy Corridor projects are facilitating renewable energy evacuation from generation centers to demand centers across multiple states.

Policy developments include new regulations for energy storage, green hydrogen production, and carbon markets. Electricity market reforms are promoting competition and efficiency while maintaining universal service obligations. MarkWide Research analysis indicates that these policy initiatives are creating substantial new market opportunities.

Technology partnerships between Indian and international companies are accelerating knowledge transfer and local manufacturing capabilities. Joint ventures in renewable energy, energy storage, and smart grid technologies are strengthening the domestic supply chain while reducing import dependence.

Financial innovations include green bonds, blended financing mechanisms, and risk mitigation instruments that are improving project bankability and reducing capital costs. International cooperation on clean energy technologies is expanding through bilateral agreements and multilateral initiatives.

Strategic recommendations for market participants emphasize the importance of adapting to rapidly changing market conditions while capitalizing on emerging opportunities. Renewable energy developers should focus on hybrid project development, energy storage integration, and long-term power purchase agreement negotiations to maximize project value and grid integration benefits.

Traditional power generators should accelerate efficiency improvements, explore renewable energy diversification, and invest in flexible generation capabilities that can complement variable renewable energy sources. Retirement planning for aging thermal power assets should consider market conditions and environmental regulations.

Distribution utilities should prioritize grid modernization investments, demand response program development, and customer engagement initiatives. Financial sustainability improvements through operational efficiency and tariff rationalization remain critical for long-term market health.

Technology providers should focus on localization strategies, research and development investments, and partnership development with Indian companies. Digital solutions and energy storage technologies offer particularly attractive growth opportunities.

Investors should consider the long-term growth potential while carefully evaluating regulatory risks and project execution capabilities. ESG considerations are becoming increasingly important for investment decision-making and stakeholder acceptance.

Future prospects for the Indian power market remain exceptionally positive, supported by fundamental demand drivers, policy commitments, and technological advancement. Electricity demand growth is projected to continue at robust rates, driven by economic expansion, urbanization, and industrial development. The market is expected to maintain growth momentum of approximately 6.1% annually over the next decade.

Renewable energy dominance will continue to strengthen, with solar and wind power expected to account for the majority of new capacity additions. Energy storage deployment will accelerate significantly as costs decline and grid integration requirements increase. MWR projections indicate that storage capacity could grow at rates exceeding 40% annually through 2030.

Grid modernization initiatives will transform power system operations, enabling higher renewable energy penetration and improved efficiency. Smart grid technologies will become mainstream, supporting demand response, distributed generation, and electric vehicle integration.

Market structure evolution will continue toward greater competition and efficiency, with power exchanges playing an increasingly important role in price discovery and resource optimization. Regional market integration will strengthen, optimizing resource utilization across state boundaries.

International cooperation will expand, particularly in green hydrogen production, renewable energy equipment manufacturing, and technology transfer. India’s position as a global clean energy hub will strengthen, creating export opportunities and attracting international investments.

The Indian power market represents one of the world’s most dynamic and promising energy sectors, characterized by rapid growth, technological innovation, and strong policy support. Market transformation toward renewable energy sources, grid modernization, and improved efficiency creates substantial opportunities for all stakeholders while supporting India’s economic development and environmental objectives.

Key success factors for market participants include adaptability to changing market conditions, investment in advanced technologies, and alignment with sustainability goals. The market’s evolution toward greater competition and efficiency will reward innovative and efficient operators while maintaining essential public service obligations.

Long-term prospects remain highly favorable, supported by fundamental demand drivers, supportive policy frameworks, and India’s commitment to becoming a global leader in clean energy. The Indian power market will continue to play a crucial role in the nation’s economic growth while contributing to global climate objectives through its renewable energy transition and technological innovation.

What is Indian Power?

Indian Power refers to the generation, distribution, and consumption of electricity in India, encompassing various sources such as thermal, hydro, solar, and wind energy.

What are the key players in the Indian Power Market?

Key players in the Indian Power Market include Tata Power, Adani Power, NTPC Limited, and Reliance Power, among others.

What are the main drivers of growth in the Indian Power Market?

The main drivers of growth in the Indian Power Market include increasing energy demand due to urbanization, government initiatives for renewable energy, and investments in infrastructure.

What challenges does the Indian Power Market face?

The Indian Power Market faces challenges such as regulatory hurdles, financial instability of distribution companies, and the need for technological upgrades.

What opportunities exist in the Indian Power Market for future growth?

Opportunities in the Indian Power Market include the expansion of renewable energy projects, advancements in smart grid technology, and increased foreign investment in energy infrastructure.

What trends are shaping the Indian Power Market?

Trends shaping the Indian Power Market include a shift towards renewable energy sources, the adoption of energy storage solutions, and the integration of digital technologies for better energy management.

Indian Power Market

| Segmentation Details | Description |

|---|---|

| Type | Renewable, Thermal, Nuclear, Hydropower |

| End User | Residential, Commercial, Industrial, Agricultural |

| Service Type | Generation, Transmission, Distribution, Retail |

| Technology | Solar, Wind, Biomass, Geothermal |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Indian Power Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.