444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Indian oil and gas market represents one of the most dynamic and rapidly evolving energy sectors in the Asia-Pacific region. India’s energy landscape is characterized by substantial domestic demand growth, strategic government initiatives, and increasing investments in both conventional and unconventional hydrocarbon resources. The market encompasses upstream exploration and production activities, midstream transportation and storage infrastructure, and downstream refining and marketing operations across the subcontinent.

Market dynamics in India’s oil and gas sector are driven by the country’s position as the world’s third-largest energy consumer and fastest-growing major economy. With a growing population exceeding 1.4 billion people and rapid industrialization, India’s energy consumption is projected to grow at a compound annual growth rate of 4.2% through the next decade. The sector benefits from supportive government policies, including the Hydrocarbon Exploration and Licensing Policy (HELP) and various fiscal incentives designed to attract foreign investment and enhance domestic production capabilities.

Domestic production currently meets approximately 15% of crude oil demand and 50% of natural gas requirements, creating significant opportunities for exploration companies and international partnerships. The market features a mix of state-owned enterprises, private domestic companies, and multinational corporations working collaboratively to develop India’s hydrocarbon potential across both onshore and offshore basins.

The Indian oil and gas market refers to the comprehensive ecosystem of hydrocarbon exploration, production, processing, transportation, and distribution activities within India’s territorial boundaries and exclusive economic zones. This market encompasses all aspects of the petroleum value chain, from upstream activities including seismic surveys, drilling operations, and field development, to midstream infrastructure such as pipelines, storage terminals, and processing facilities, and downstream operations including refineries, petrochemical plants, and retail distribution networks.

Market participants include national oil companies like Oil and Natural Gas Corporation (ONGC) and Oil India Limited (OIL), private sector entities such as Reliance Industries and Vedanta, and international majors including ExxonMobil, Shell, and BP. The market operates under regulatory frameworks established by the Ministry of Petroleum and Natural Gas, the Directorate General of Hydrocarbons (DGH), and the Petroleum and Natural Gas Regulatory Board (PNGRB).

India’s oil and gas market stands at a critical juncture of transformation, driven by ambitious energy security goals, environmental considerations, and technological advancement. The sector is experiencing unprecedented growth in natural gas infrastructure development, with the government targeting 15% natural gas share in the energy mix by 2030, up from the current 6.2%. This transition represents substantial opportunities for market participants across the entire value chain.

Key market trends include the accelerated development of city gas distribution networks, expansion of LNG import terminals, and increased focus on unconventional resources including shale gas and coalbed methane. The market benefits from supportive policy frameworks, including the Open Acreage Licensing Policy (OALP) and revenue-sharing models that have attracted significant international investment and technological expertise.

Strategic initiatives by major players focus on digital transformation, enhanced oil recovery techniques, and sustainable development practices. The market’s growth trajectory is supported by robust domestic demand, improving regulatory environment, and increasing integration with global energy markets through strategic partnerships and joint ventures.

Market intelligence reveals several critical insights shaping the Indian oil and gas landscape:

Economic growth serves as the primary driver for India’s oil and gas market expansion. The country’s GDP growth trajectory, urbanization trends, and industrial development create sustained demand for energy resources across multiple sectors. Transportation fuel demand continues to grow with increasing vehicle ownership, while industrial consumption rises with manufacturing sector expansion and petrochemical industry development.

Government policy support provides significant momentum through initiatives such as the National Gas Grid project, city gas distribution expansion programs, and exploration licensing reforms. The Pradhan Mantri Urja Ganga pipeline project and similar infrastructure developments create substantial market opportunities while enhancing energy access across rural and urban areas.

Energy security concerns drive strategic initiatives to reduce import dependency and enhance domestic production capabilities. The government’s target of reducing oil import dependency by 10% by 2030 creates strong incentives for exploration and production activities, while also promoting alternative energy sources and efficiency improvements.

Technological advancement enables access to previously uneconomical resources through enhanced oil recovery techniques, horizontal drilling, and hydraulic fracturing technologies. Digital transformation initiatives improve operational efficiency, reduce costs, and enhance safety performance across the value chain.

Geological challenges present significant constraints to market development, particularly in India’s complex geological formations and mature oil fields. Many of the country’s producing assets are experiencing natural decline rates, requiring substantial investment in enhanced oil recovery technologies and secondary development programs to maintain production levels.

Environmental regulations and compliance requirements create operational complexities and increase project costs. Stringent environmental clearance processes, coastal regulation zone restrictions, and emission standards require careful planning and substantial investment in environmental management systems.

Land acquisition challenges frequently delay project implementation, particularly for pipeline infrastructure and onshore exploration activities. Complex land ownership structures, regulatory approvals, and community engagement requirements can significantly extend project timelines and increase development costs.

Price volatility in global oil and gas markets creates uncertainty for long-term investment planning and project economics. Fluctuating commodity prices impact profitability, investment decisions, and the viability of marginal field developments across the sector.

Unconventional resources represent substantial untapped opportunities, with India’s shale gas potential estimated to be significant across several basins. The development of coalbed methane resources, tight gas formations, and gas hydrates could substantially enhance domestic production capabilities and reduce import dependency.

Deepwater exploration offers promising prospects, particularly in the Krishna-Godavari basin and other offshore areas where recent discoveries have demonstrated commercial viability. Advanced seismic technologies and deepwater drilling capabilities enable access to previously unexplored areas with significant hydrocarbon potential.

Natural gas infrastructure development presents extensive opportunities as the government promotes gas-based economy initiatives. The expansion of city gas distribution networks, LNG import terminals, and pipeline connectivity creates substantial market potential for infrastructure developers and service providers.

Digital transformation initiatives offer opportunities for technology providers and service companies to enhance operational efficiency, reduce costs, and improve safety performance. Applications include predictive maintenance, automated drilling systems, and real-time reservoir monitoring technologies.

Supply-demand dynamics in India’s oil and gas market are characterized by growing consumption outpacing domestic production growth. This fundamental imbalance creates ongoing opportunities for exploration and production companies while driving infrastructure development requirements across the midstream and downstream segments.

Competitive dynamics feature increasing collaboration between national oil companies, private sector participants, and international majors. Strategic partnerships, joint ventures, and technology sharing agreements are becoming more common as companies seek to leverage complementary capabilities and share development risks.

Regulatory dynamics continue to evolve with policy reforms aimed at attracting investment, enhancing operational efficiency, and promoting sustainable development practices. The transition from production sharing contracts to revenue sharing models has improved project economics and attracted increased international participation.

Technology dynamics are reshaping exploration and production activities through advanced seismic imaging, horizontal drilling techniques, and enhanced oil recovery methods. Digital technologies enable real-time monitoring, predictive analytics, and automated operations that improve efficiency and reduce operational costs.

Primary research methodologies employed in analyzing India’s oil and gas market include comprehensive interviews with industry executives, government officials, and technical experts across the value chain. Field surveys and site visits provide firsthand insights into operational challenges, technological implementations, and market dynamics affecting different segments of the industry.

Secondary research incorporates analysis of government publications, regulatory filings, company annual reports, and technical literature from industry associations and research institutions. Data sources include the Ministry of Petroleum and Natural Gas, Directorate General of Hydrocarbons, and various state-level petroleum development agencies.

Market modeling techniques utilize econometric analysis, scenario planning, and trend extrapolation to project future market developments and identify key growth drivers. Quantitative analysis incorporates production data, consumption patterns, infrastructure development timelines, and investment flow analysis.

Validation processes ensure data accuracy through cross-referencing multiple sources, expert consultations, and peer review procedures. Market intelligence is continuously updated to reflect changing regulatory environments, technological developments, and competitive dynamics.

Western India dominates oil and gas production, with Mumbai High and other offshore fields contributing approximately 70% of domestic crude oil production. The region benefits from established infrastructure, experienced workforce, and proximity to major consumption centers. Gujarat’s onshore fields and Rajasthan’s emerging production contribute significantly to regional output.

Eastern India shows substantial promise for natural gas development, particularly in the Krishna-Godavari basin where recent discoveries have demonstrated significant commercial potential. The region’s coalbed methane resources and shale gas prospects offer long-term development opportunities, while existing infrastructure supports both production and distribution activities.

Northern India serves as a major consumption center with extensive refining capacity and distribution networks. The region’s strategic location enables efficient product distribution across the country while supporting import operations through pipeline connections and transportation infrastructure.

Southern India combines significant consumption demand with emerging production opportunities. The region’s industrial base, including petrochemical complexes and manufacturing facilities, creates sustained demand for oil and gas products while supporting downstream value addition activities.

Market leadership in India’s oil and gas sector is characterized by a mix of state-owned enterprises, private companies, and international majors operating across different segments of the value chain:

Strategic partnerships and joint ventures are increasingly common as companies seek to leverage complementary capabilities, share development risks, and access new technologies. These collaborations often combine the local market knowledge of Indian companies with the technical expertise and financial resources of international partners.

By Activity Type:

By Resource Type:

By Geography:

By End-Use Application:

Exploration and Production activities in India focus increasingly on technology-driven approaches to enhance recovery rates and access challenging reservoirs. Enhanced oil recovery techniques, including polymer flooding and gas injection, are being deployed to maximize production from mature fields while maintaining operational efficiency.

Refining operations in India have achieved world-class efficiency standards with several facilities ranking among the most complex and efficient globally. The sector benefits from economies of scale, advanced process technologies, and strategic location advantages that enable both domestic supply and export opportunities.

Natural gas infrastructure development represents the fastest-growing segment, with city gas distribution networks expanding rapidly across tier-2 and tier-3 cities. According to MarkWide Research analysis, the natural gas distribution sector is experiencing annual growth rates exceeding 12% as infrastructure development accelerates.

Petrochemical integration provides significant value addition opportunities, with major refineries developing integrated petrochemical complexes to capture higher margins and serve growing domestic demand for polymer and chemical products.

Exploration companies benefit from improved geological understanding, advanced seismic technologies, and supportive regulatory frameworks that reduce exploration risks and enhance success rates. The Open Acreage Licensing Policy enables companies to select exploration areas based on their technical evaluation and strategic priorities.

Service providers gain from increasing activity levels across upstream, midstream, and downstream segments. Opportunities exist for drilling contractors, seismic survey companies, engineering firms, and technology providers as the market expands and modernizes its operations.

Infrastructure developers benefit from government support for pipeline networks, storage facilities, and distribution systems. The National Gas Grid project and city gas distribution expansion create substantial opportunities for construction companies, equipment suppliers, and facility operators.

Technology companies find growing demand for digital solutions, automation systems, and advanced analytics platforms that enhance operational efficiency, reduce costs, and improve safety performance across the oil and gas value chain.

Financial institutions benefit from increased lending opportunities as the sector attracts substantial investment for exploration, infrastructure development, and technology upgrades. Project financing, trade finance, and risk management services are in growing demand.

Strengths:

Weaknesses:

Opportunities:

Threats:

Digital transformation is revolutionizing operations across the oil and gas value chain, with companies implementing artificial intelligence, machine learning, and Internet of Things technologies to optimize production, reduce costs, and enhance safety performance. Predictive maintenance systems, automated drilling operations, and real-time reservoir monitoring are becoming standard practices.

Sustainability initiatives are gaining prominence as companies focus on reducing carbon emissions, improving energy efficiency, and implementing circular economy principles. Carbon capture and storage technologies, flare gas recovery systems, and renewable energy integration are increasingly important considerations in project planning and operations.

Strategic partnerships between domestic and international companies are expanding, driven by the need to share risks, access advanced technologies, and leverage complementary capabilities. Joint ventures, technology licensing agreements, and strategic alliances are becoming more sophisticated and comprehensive.

Infrastructure modernization focuses on enhancing pipeline networks, storage facilities, and distribution systems to improve efficiency and reduce losses. Smart pipeline technologies, automated monitoring systems, and advanced materials are being deployed to enhance infrastructure performance and reliability.

Recent discoveries in deepwater areas have demonstrated significant commercial potential, with several major finds announced in the Krishna-Godavari basin and other offshore regions. These discoveries are attracting increased investment in deepwater exploration and development capabilities.

Policy reforms continue to evolve, with the government introducing new licensing rounds, fiscal incentives, and regulatory simplifications designed to attract investment and enhance domestic production. The Hydrocarbon Exploration and Licensing Policy (HELP) and Open Acreage Licensing Policy (OALP) have transformed the exploration landscape.

Infrastructure projects are advancing rapidly, including the expansion of the National Gas Grid, development of new LNG import terminals, and construction of city gas distribution networks. These projects are creating substantial opportunities for equipment suppliers, construction companies, and service providers.

Technology deployments are accelerating across the sector, with companies implementing advanced drilling technologies, enhanced oil recovery techniques, and digital monitoring systems. MWR data indicates that technology investments have increased by 25% annually as companies seek to improve operational efficiency and reduce costs.

Investment priorities should focus on unconventional resource development, natural gas infrastructure expansion, and technology integration initiatives that enhance operational efficiency and reduce environmental impact. Companies should prioritize projects with strong economics, manageable risks, and alignment with government policy objectives.

Strategic partnerships with international companies can provide access to advanced technologies, financial resources, and global market expertise. Domestic companies should seek partnerships that complement their capabilities while providing opportunities for technology transfer and skill development.

Technology adoption should emphasize digital solutions that improve operational efficiency, reduce costs, and enhance safety performance. Companies should invest in data analytics platforms, automated systems, and predictive maintenance technologies that provide competitive advantages.

Risk management strategies should address commodity price volatility, regulatory changes, and environmental compliance requirements. Companies should develop flexible business models, diversified portfolios, and robust financial structures that can adapt to changing market conditions.

Long-term prospects for India’s oil and gas market remain positive, supported by sustained economic growth, urbanization trends, and industrial development. The government’s commitment to energy security, infrastructure development, and policy reforms creates a favorable environment for continued market expansion and investment attraction.

Production growth is expected to accelerate as new discoveries are developed, enhanced oil recovery techniques are deployed, and unconventional resources are commercialized. MarkWide Research projects that domestic oil production could increase by 15-20% over the next decade through technology deployment and new field development.

Natural gas development will likely experience the most rapid growth, driven by government initiatives to increase gas share in the energy mix, infrastructure development, and environmental considerations. The expansion of city gas distribution networks and industrial gas consumption will support sustained demand growth.

Technology integration will continue to transform operations, with artificial intelligence, automation, and digital monitoring systems becoming standard across the industry. These technologies will enable improved efficiency, reduced costs, and enhanced safety performance while supporting sustainable development objectives.

India’s oil and gas market represents one of the most dynamic and promising energy sectors globally, characterized by substantial growth potential, supportive government policies, and increasing international investment. The market benefits from strong domestic demand, improving regulatory frameworks, and technological advancement that enhance operational efficiency and resource accessibility.

Strategic opportunities exist across the entire value chain, from upstream exploration and production to midstream infrastructure and downstream operations. The development of unconventional resources, expansion of natural gas infrastructure, and integration of digital technologies provide substantial growth prospects for market participants.

Future success in India’s oil and gas market will depend on companies’ ability to adapt to changing market conditions, leverage technological innovations, and develop strategic partnerships that provide competitive advantages. The sector’s continued evolution toward greater efficiency, sustainability, and integration with global energy markets positions it for sustained growth and value creation in the years ahead.

What is Indian Oil and Gas?

Indian Oil and Gas refers to the exploration, extraction, refining, and distribution of oil and natural gas resources within India. This sector plays a crucial role in the country’s energy supply and economic development.

Who are the major players in the Indian Oil and Gas Market?

Major companies in the Indian Oil and Gas Market include Indian Oil Corporation, Reliance Industries, ONGC, and Bharat Petroleum, among others.

What are the key drivers of growth in the Indian Oil and Gas Market?

Key drivers of growth in the Indian Oil and Gas Market include increasing energy demand, government initiatives for energy security, and advancements in extraction technologies. Additionally, urbanization and industrialization contribute significantly to the sector’s expansion.

What challenges does the Indian Oil and Gas Market face?

The Indian Oil and Gas Market faces challenges such as fluctuating global oil prices, regulatory hurdles, and environmental concerns. These factors can impact investment and operational efficiency within the sector.

What opportunities exist in the Indian Oil and Gas Market?

Opportunities in the Indian Oil and Gas Market include the development of renewable energy sources, enhanced oil recovery techniques, and the expansion of natural gas infrastructure. These avenues can help diversify energy sources and improve sustainability.

What trends are shaping the Indian Oil and Gas Market?

Trends shaping the Indian Oil and Gas Market include the shift towards cleaner energy, digital transformation in operations, and increased investment in alternative fuels. These trends reflect a growing emphasis on sustainability and efficiency in the sector.

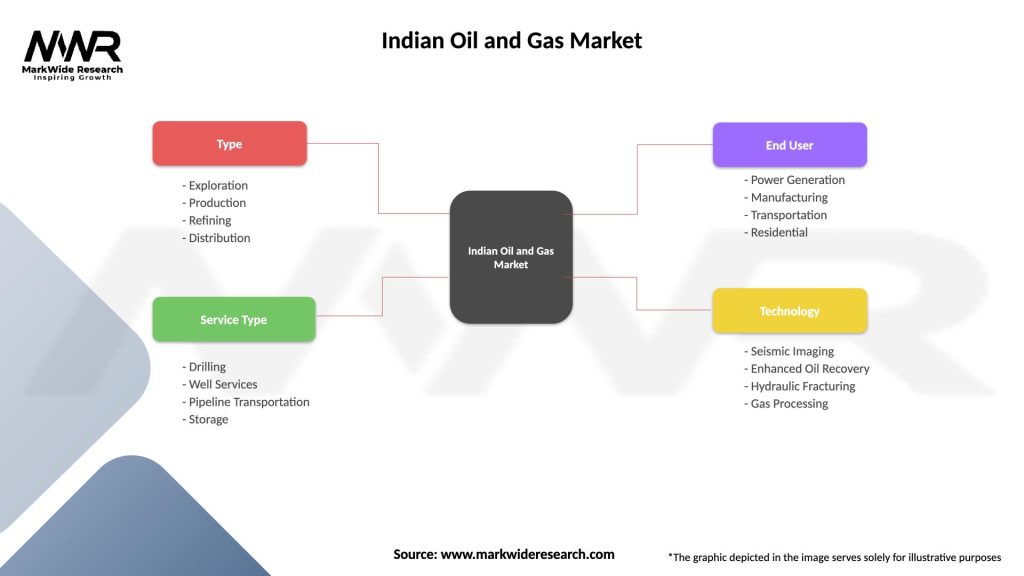

Indian Oil and Gas Market

| Segmentation Details | Description |

|---|---|

| Type | Exploration, Production, Refining, Distribution |

| Service Type | Drilling, Well Services, Pipeline Transportation, Storage |

| End User | Power Generation, Manufacturing, Transportation, Residential |

| Technology | Seismic Imaging, Enhanced Oil Recovery, Hydraulic Fracturing, Gas Processing |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Indian Oil and Gas Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.