The student loan market in India is a critical component of the country’s education financing ecosystem, providing financial support to students pursuing higher education. With a vast and diverse educational landscape encompassing universities, colleges, and vocational institutions, India’s student loan market offers various loan products tailored to the needs of students and their families. Government-sponsored loan schemes, private banks, and non-banking financial institutions (NBFCs) play pivotal roles in facilitating access to education financing for Indian students.

Meaning

The India student loan market refers to the financial sector that offers loans to Indian students pursuing higher education at domestic and international educational institutions. These loans cover tuition fees, accommodation, textbooks, and other education-related expenses. Student loans in India are available from government agencies, such as the Indian Banks’ Association (IBA), as well as private banks, NBFCs, and microfinance institutions.

Executive Summary

The India student loan market plays a crucial role in democratizing access to higher education and empowering students from diverse socioeconomic backgrounds to pursue their academic aspirations. Government-sponsored loan schemes, such as the Central Sector Interest Subsidy Scheme (CSIS) and the Pradhan Mantri Vidya Lakshmi Karyakram (PMVLK), provide low-interest loans with favorable repayment terms to eligible students. Private lenders also offer competitive loan products, scholarships, and financial aid packages to support students’ educational endeavors. Despite challenges such as rising tuition costs and loan default risks, the India student loan market presents opportunities for innovation, collaboration, and sustainable growth.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Government Support: The Indian government plays a proactive role in promoting education financing through initiatives like the CSIS, PMVLK, and other loan subsidy schemes. Government-sponsored loans offer interest subsidies, moratorium periods, and flexible repayment options to alleviate the financial burden on students and families.

Digital Disruption: Technological advancements and digital disruption have transformed the India student loan market, enabling online loan applications, digital document submissions, and mobile payment solutions. Fintech startups and digital lending platforms facilitate streamlined loan processing, real-time credit assessments, and borrower engagement.

Rising Tuition Costs: Tuition fees at Indian educational institutions have been steadily increasing, outpacing inflation rates and household income growth. Rising tuition costs pose affordability challenges for students and families, necessitating reliance on student loans to finance higher education expenses.

Employability Concerns: Employability and job market outcomes influence students’ decisions to pursue higher education and borrow student loans. Perceptions of return on investment (ROI), career prospects, and industry demand for specific skills shape borrower preferences for educational programs and loan repayment capacity.

Market Drivers

Government Subsidies: Government subsidies for education financing, including interest rate subsidies, loan moratorium periods, and repayment incentives, promote access to higher education for economically disadvantaged students. Subsidized loans with favorable terms reduce the financial barriers to education and improve social mobility.

Skill Development Initiatives: Skill development initiatives, vocational training programs, and industry partnerships aim to bridge the gap between education and employment in India. Student loans support students pursuing technical education, professional certifications, and specialized skills training aligned with industry demands.

International Education: Rising aspirations for international education among Indian students drive demand for student loans to fund overseas studies. Loans for study abroad programs cover tuition fees, living expenses, standardized test preparation, and travel costs for students seeking global academic experiences.

Financial Inclusion: Student loans promote financial inclusion by extending credit access to underserved segments of the population, including rural communities, women, minorities, and economically disadvantaged groups. Microfinance institutions and nonprofit organizations offer microloans and scholarships to empower marginalized students to pursue higher education.

Market Restraints

Loan Default Risks: The risk of loan defaults, delinquencies, and nonperforming assets (NPAs) poses challenges for lenders and government agencies administering student loan programs. High default rates strain loan recovery efforts, impair loan portfolio quality, and undermine the sustainability of education financing initiatives.

Regulatory Compliance: Compliance with regulatory guidelines, loan eligibility criteria, and documentation requirements imposes administrative burdens on lenders and borrowers in the student loan market. Regulatory changes, policy reforms, and audit scrutiny necessitate operational adjustments and risk management protocols.

Job Market Volatility: Economic downturns, industry disruptions, and job market volatility impact students’ employability and loan repayment capacity. Uncertain job prospects, wage stagnation, and underemployment challenges exacerbate borrower financial stress and loan default risks.

Social Stigma: Cultural attitudes towards debt, financial risk aversion, and social stigma associated with borrowing may deter some Indian students and families from utilizing student loans. Concerns about debt burden, repayment obligations, and creditworthiness influence borrowing decisions and loan utilization rates.

Market Opportunities

Digital Transformation: Accelerated digital transformation initiatives in the India student loan market present opportunities for lenders to enhance customer experience, improve operational efficiency, and reduce loan processing times. Digital lending platforms, mobile apps, and online loan marketplaces streamline borrower engagement and loan origination processes.

Alternative Financing Models: Alternative financing models such as income-share agreements (ISAs), crowdfunding platforms, and peer-to-peer lending networks offer innovative alternatives to traditional student loans. ISAs align repayment with post-graduation income levels and promote risk-sharing between students and investors.

Employer-Sponsored Education Benefits: Employer-sponsored education benefits, including tuition reimbursement programs, student loan repayment assistance, and education savings plans, enhance employee recruitment, retention, and talent development. Collaborations between employers and financial institutions expand access to education financing for working professionals.

Credit Risk Mitigation: Advanced credit risk mitigation strategies, including credit scoring models, loan securitization, and loan loss provisioning, help lenders mitigate default risks and maintain portfolio quality. Data analytics, machine learning algorithms, and predictive modeling techniques improve credit risk assessment and loan underwriting processes.

Market Dynamics

The India student loan market operates in a dynamic environment shaped by macroeconomic trends, regulatory reforms, technological innovations, and demographic shifts. These dynamics influence borrower behavior, lender strategies, market competition, and government policies governing education financing. Understanding the market dynamics is essential for stakeholders to adapt to changing conditions, identify opportunities, and mitigate risks effectively.

Regional Analysis

The India student loan market exhibits regional variations in loan demand, borrower demographics, educational infrastructure, and economic development. Major metropolitan areas and Tier 1 cities with concentrations of educational institutions, corporate hubs, and job opportunities experience higher demand for student loans. Tier 2 and Tier 3 cities, as well as rural regions, may face challenges related to access to education financing and employment opportunities.

Competitive Landscape

Leading Companies for India Student Loan Market:

State Bank of India (SBI)

HDFC Bank

ICICI Bank

Punjab National Bank (PNB)

Axis Bank

Canara Bank

Bank of Baroda (BOB)

IDBI Bank

Union Bank of India

Indian Bank

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Segmentation

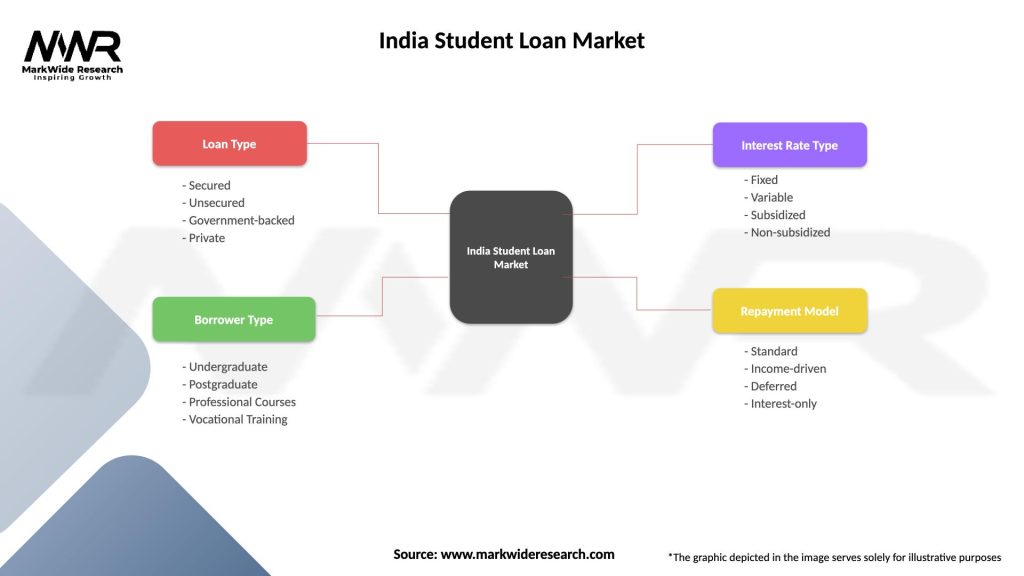

The India student loan market can be segmented based on various factors, including:

Loan Type: Segmentation by loan type may include government-sponsored loans, private loans, subsidized loans, and alternative financing options such as ISAs.

Borrower Profile: Segmentation by borrower profile may include undergraduate students, graduate students, international students, and working professionals pursuing continuing education.

Loan Purpose: Segmentation by loan purpose may include tuition loans, living expense loans, study abroad loans, and skill development loans for vocational training programs.

Geography: The market may be segmented into urban, semi-urban, and rural areas based on population density, educational infrastructure, and economic development indicators.

Segmentation enables lenders to tailor loan products, marketing strategies, and customer service offerings to specific borrower segments and market niches, enhancing customer satisfaction and loan portfolio performance.

Category-wise Insights

Government-Sponsored Loans: Government-sponsored loan schemes such as the Vidyalakshmi Education Loan Scheme, the Prime Minister’s Special Scholarship Scheme (PMSSS), and the National Scholarship Portal (NSP) provide subsidized loans, scholarships, and financial aid to eligible students from economically disadvantaged backgrounds. These loans cover tuition fees, living expenses, and other education-related costs for students pursuing higher education in India and abroad.

Private Student Loans: Private banks, NBFCs, and fintech startups offer private student loans to supplement government-sponsored loans and financial aid packages. Private loans may have higher borrowing limits, competitive interest rates, and flexible repayment terms tailored to individual borrower preferences and credit profiles.

Skill Development Loans: Skill development loans finance vocational training programs, professional certifications, and specialized skills courses aimed at enhancing employability and career prospects. Loans for skill development cover program fees, equipment costs, and living expenses for students enrolled in vocational institutes, training centers, and online learning platforms.

Study Abroad Loans: Study abroad loans support Indian students pursuing higher education programs at foreign universities and institutions. These loans cover tuition fees, accommodation, travel expenses, standardized test preparation, and other study-related costs for students seeking international academic experiences and cultural exchange opportunities.

Key Benefits for Industry Participants and Stakeholders

The India student loan market offers several benefits for industry participants and stakeholders:

Education Accessibility: Student loans promote access to higher education for students from diverse socioeconomic backgrounds, enabling them to pursue academic excellence and achieve their career aspirations.

Financial Inclusion: Student loans expand financial inclusion by extending credit access to underserved segments of the population, including rural communities, women, minorities, and economically disadvantaged groups. Microloans, scholarships, and financial aid empower marginalized students to pursue education and skill development opportunities.

Employability Enhancement: Student loans finance vocational training programs, professional certifications, and skill development courses aimed at enhancing employability and career readiness. Investments in education and skill development contribute to workforce development, economic growth, and poverty alleviation in India.

Market Growth Opportunities: The India student loan market presents growth opportunities for lenders, educational institutions, and government agencies through innovative loan products, strategic partnerships, and market expansion initiatives. Collaborations between stakeholders facilitate knowledge sharing, technology adoption, and best practices in education financing.

SWOT Analysis

A SWOT analysis provides insights into the India student loan market’s strengths, weaknesses, opportunities, and threats:

Regulatory compliance burdens and documentation requirements

Social stigma associated with borrowing and debt

Opportunities:

Digital transformation and fintech innovation

Alternative financing models such as ISAs and crowdfunding platforms

Employer-sponsored education benefits and tuition reimbursement programs

Threats:

Economic downturns and job market uncertainties

Rising tuition costs outpacing loan affordability

Increasing competition among lenders and financial institutions

Regulatory changes impacting loan eligibility criteria and interest rates

Understanding these factors through a SWOT analysis helps stakeholders capitalize on strengths, address weaknesses, leverage opportunities, and mitigate threats in the India student loan market.

Market Key Trends

Digital Disruption: Technological advancements and digital disruption are reshaping the India student loan market, driving the adoption of online loan applications, digital document submissions, and mobile payment solutions. Fintech startups and digital lending platforms leverage artificial intelligence, data analytics, and machine learning algorithms to streamline loan processing and enhance borrower experience.

Educational Technology: The COVID-19 pandemic accelerated the adoption of educational technology (edtech) platforms, online learning tools, and virtual classrooms in India. Distance learning options, hybrid education models, and remote education solutions influence student loan demand, educational delivery models, and market dynamics in the post-pandemic era.

Income-Contingent Repayment: Income-contingent repayment (ICR) models, income-share agreements (ISAs), and performance-based financing mechanisms offer innovative approaches to student loan repayment. These models align loan repayment with borrowers’ post-graduation income levels, reducing financial risks and promoting loan affordability.

Sustainable Finance: Sustainable finance initiatives, environmental, social, and governance (ESG) criteria, and impact investing principles are gaining traction in the India student loan market. Lenders prioritize environmental sustainability, social responsibility, and ethical lending practices in loan origination, portfolio management, and stakeholder engagement.

Covid-19 Impact

The COVID-19 pandemic had profound implications for the India student loan market, influencing borrower behavior, lender strategies, and government policies related to education financing. Key impacts of the pandemic include:

Remote Learning Shift: University closures, lockdown measures, and social distancing guidelines necessitated the transition to remote learning and online education platforms. The shift to virtual classrooms and distance learning options impacted student loan utilization, borrowing patterns, and repayment behavior.

Financial Hardship Relief: Government agencies, lenders, and educational institutions implemented financial hardship relief measures to support students and families facing economic challenges due to the pandemic. Loan forbearance programs, interest rate reductions, and debt restructuring options provided temporary relief from loan repayment obligations.

Employment Disruptions: Economic uncertainties, job market disruptions, and industry downturns affected students’ employment prospects and post-graduation plans. Job losses, wage reductions, and underemployment challenges impacted borrowers’ income levels, loan repayment capacity, and financial stability.

Digital Transformation Acceleration: The pandemic accelerated digital transformation initiatives in the India student loan market, prompting lenders and educational institutions to invest in online platforms, digital payment solutions, and remote customer support capabilities. Digital lending platforms, mobile apps, and virtual loan counseling services facilitated contactless loan origination and servicing.

Key Industry Developments

Virtual Loan Processing: Lenders implemented virtual loan processing solutions, online loan applications, and digital document submissions to facilitate remote loan origination and servicing during the pandemic. Virtual loan counseling sessions, video conferencing, and online chat support enhanced borrower engagement and satisfaction.

Financial Literacy Programs: Educational institutions, government agencies, and nonprofit organizations expanded financial literacy programs, online workshops, and educational resources to help students make informed decisions about education financing, budgeting, and debt management. Financial literacy initiatives promoted responsible borrowing behavior and empowered borrowers to navigate financial challenges effectively.

Emergency Financial Aid: The Indian government allocated emergency financial aid and relief funds to support students and families impacted by the pandemic. Emergency grants, scholarships, and income support programs provided temporary financial assistance to cover tuition fees, living expenses, and essential needs during times of crisis.

Health and Safety Measures: Universities, educational institutions, and student loan providers implemented health and safety measures to protect students, faculty, and staff from COVID-19 transmission. Enhanced cleaning protocols, social distancing guidelines, and remote work arrangements ensured continuity of educational services and loan administration operations.

Analyst Suggestions

Enhance Digital Accessibility: Stakeholders should prioritize digital accessibility and user experience enhancements to accommodate students with diverse needs and preferences. Mobile-friendly platforms, multilingual support, and assistive technologies improve access to education financing resources and services for all borrowers.

Expand Loan Forgiveness Programs: Government agencies and lenders should explore opportunities to expand loan forgiveness programs for graduates pursuing careers in high-need fields, such as healthcare, education, and public service. Loan forgiveness incentives can encourage students to enter critical workforce sectors and address societal needs.

Promote Financial Wellness: Educational institutions and employers should promote financial wellness initiatives and resources to support students’ holistic well-being. Financial wellness programs may include budgeting workshops, debt management counseling, and mental health support services to address the financial stressors associated with student loans.

Invest in Career Services: Universities and career centers should invest in career development services, job placement programs, and internship opportunities to enhance students’ employability and post-graduation outcomes. Access to career counseling, networking events, and industry partnerships facilitates successful transitions from education to employment.

Future Outlook

The future outlook for the India student loan market is influenced by various factors, including demographic trends, economic conditions, technological advancements, regulatory policies, and social dynamics. While challenges such as rising tuition costs, loan default risks, and job market uncertainties may impact market growth and borrower outcomes, there are opportunities for innovation, collaboration, and sustainable development. By addressing these challenges proactively and leveraging emerging trends, stakeholders can contribute to a more accessible, equitable, and resilient education financing system in India.

Conclusion

The India student loan market serves as a vital financial resource for students pursuing higher education and advancing their career aspirations. Despite facing challenges such as rising tuition costs, loan default risks, and job market uncertainties, the market offers opportunities for innovation, collaboration, and social impact. By promoting financial literacy, expanding loan options, and enhancing borrower support services, stakeholders can ensure that student loans remain a viable and accessible financing option for aspiring students in India. With strategic investments and partnerships, the India student loan market can contribute to the development of a skilled workforce, foster economic growth, and promote social mobility for future generations.

What is Student Loan?

A student loan is a type of loan designed to help students pay for their education-related expenses, including tuition, books, and living costs. In India, these loans are often provided by banks and financial institutions to support higher education.

What are the key players in the India Student Loan Market?

Key players in the India Student Loan Market include State Bank of India, HDFC Bank, Axis Bank, and Punjab National Bank, among others. These institutions offer various loan products tailored to the needs of students pursuing higher education.

What are the growth factors driving the India Student Loan Market?

The growth of the India Student Loan Market is driven by increasing enrollment in higher education, rising tuition costs, and a growing awareness of financial aid options among students and parents. Additionally, government initiatives to promote education financing contribute to market expansion.

What challenges does the India Student Loan Market face?

The India Student Loan Market faces challenges such as high default rates, lack of financial literacy among borrowers, and stringent eligibility criteria set by lenders. These factors can hinder access to loans for many potential students.

What opportunities exist in the India Student Loan Market?

Opportunities in the India Student Loan Market include the development of innovative loan products, partnerships with educational institutions, and the potential for digital platforms to streamline the application process. These advancements can enhance accessibility for students.

What trends are shaping the India Student Loan Market?

Trends in the India Student Loan Market include the rise of online loan applications, increased competition among lenders, and a focus on personalized loan offerings. Additionally, there is a growing emphasis on financial education to help students make informed borrowing decisions.

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.