444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The India commercial vehicle market represents one of the most dynamic and rapidly evolving segments within the global automotive industry. Commercial vehicles in India encompass a diverse range of transportation solutions including heavy-duty trucks, medium commercial vehicles, light commercial vehicles, buses, and specialized utility vehicles. The market has experienced remarkable transformation driven by infrastructure development, e-commerce expansion, and government initiatives promoting economic growth.

Market dynamics indicate substantial growth potential with the sector projected to expand at a robust CAGR of 8.2% over the forecast period. This growth trajectory reflects India’s position as a manufacturing hub and the increasing demand for efficient logistics solutions. The commercial vehicle ecosystem encompasses various stakeholders including original equipment manufacturers, component suppliers, fleet operators, and technology providers.

Infrastructure development initiatives such as the Bharatmala project and dedicated freight corridors have significantly boosted demand for commercial vehicles. The market benefits from favorable government policies, including the implementation of GST which has streamlined logistics operations and increased vehicle utilization rates. Digitalization trends and the adoption of telematics solutions are reshaping fleet management practices across the industry.

The India commercial vehicle market refers to the comprehensive ecosystem encompassing the manufacturing, sales, and operation of vehicles designed primarily for commercial purposes including goods transportation, passenger transit, and specialized applications across various industry sectors.

Commercial vehicles are categorized based on gross vehicle weight, application, and fuel type. The market includes heavy commercial vehicles exceeding 16 tons, medium commercial vehicles ranging from 3.5 to 16 tons, and light commercial vehicles under 3.5 tons. Passenger commercial vehicles comprise buses and other mass transit solutions serving urban and intercity transportation needs.

Market participants include domestic manufacturers, international brands, component suppliers, financing institutions, and service providers. The ecosystem supports various business models from individual truck ownership to large fleet operations, contributing significantly to India’s logistics infrastructure and economic development.

India’s commercial vehicle market stands as a cornerstone of the nation’s economic infrastructure, facilitating trade, commerce, and passenger transportation across diverse geographical regions. The market demonstrates resilience and adaptability, recovering strongly from pandemic-related disruptions and positioning itself for sustained growth.

Key market drivers include rapid urbanization, infrastructure development, e-commerce growth, and government initiatives promoting manufacturing and logistics efficiency. The sector benefits from increasing freight movement requirements, with road transport accounting for approximately 70% of total freight movement in India. Technological advancement and the integration of digital solutions are transforming traditional commercial vehicle operations.

Market segmentation reveals diverse opportunities across vehicle categories, with light commercial vehicles showing particularly strong growth due to last-mile delivery requirements. The transition toward cleaner fuel technologies, including CNG, electric, and hybrid solutions, represents a significant trend shaping future market dynamics. Regional variations in demand patterns reflect India’s diverse economic landscape and infrastructure development priorities.

Strategic market insights reveal several critical factors driving the India commercial vehicle market’s evolution and growth trajectory:

Economic growth serves as the primary catalyst for India’s commercial vehicle market expansion. The country’s GDP growth directly correlates with freight movement requirements, driving demand for efficient transportation solutions. Manufacturing sector growth and the government’s Make in India initiative have increased industrial output, necessitating robust logistics infrastructure.

Infrastructure development projects including highway construction, port modernization, and industrial corridor development create substantial demand for commercial vehicles. The Bharatmala Pariyojana and Sagarmala initiatives are transforming India’s transportation landscape, requiring significant commercial vehicle deployment for construction and subsequent operational activities.

E-commerce expansion has revolutionized last-mile delivery requirements, driving unprecedented demand for light commercial vehicles and specialized delivery solutions. The growth of online retail, food delivery, and quick commerce platforms has created new market segments and operational models. Urbanization trends and changing consumer preferences continue to fuel this demand trajectory.

Government policy support through initiatives like the vehicle scrappage policy, emission norms implementation, and infrastructure investment has created favorable market conditions. GST implementation has streamlined interstate transportation, improving vehicle utilization rates and operational efficiency across the logistics sector.

High acquisition costs represent a significant barrier for small and medium-sized fleet operators, particularly in the heavy commercial vehicle segment. The substantial capital investment required for modern commercial vehicles, coupled with financing challenges for smaller operators, can limit market accessibility and growth potential.

Regulatory compliance requirements including emission norms, safety standards, and operational regulations create ongoing challenges for market participants. The transition to BS-VI emission standards has increased vehicle costs and complexity, impacting adoption rates among price-sensitive customer segments.

Infrastructure limitations in certain regions, including inadequate road conditions, limited service networks, and insufficient charging infrastructure for alternative fuel vehicles, constrain market development. Traffic congestion and parking constraints in urban areas affect commercial vehicle operations and efficiency.

Economic volatility and cyclical demand patterns can impact commercial vehicle sales, particularly during economic downturns or policy transitions. Fuel price fluctuations significantly affect total cost of ownership calculations and purchasing decisions, creating market uncertainty for both manufacturers and operators.

Electric vehicle transition presents substantial opportunities for market transformation and growth. Government incentives, improving battery technology, and environmental consciousness are driving interest in electric commercial vehicles. Last-mile delivery electrification offers immediate opportunities for light commercial vehicle manufacturers and fleet operators.

Technology integration opportunities include telematics, fleet management systems, predictive maintenance, and autonomous driving capabilities. Digital transformation of logistics operations creates demand for connected and intelligent commercial vehicles that can optimize routes, reduce fuel consumption, and improve operational efficiency.

Rural market penetration represents significant untapped potential as agricultural modernization and rural economic development increase transportation requirements. Specialized vehicle segments including refrigerated transport, hazardous material handling, and construction equipment offer niche growth opportunities.

Export market development leverages India’s manufacturing capabilities and cost competitiveness to serve regional and global markets. After-sales service expansion and value-added services create recurring revenue opportunities for manufacturers and dealers throughout the vehicle lifecycle.

Supply chain dynamics within the India commercial vehicle market reflect complex interactions between manufacturers, suppliers, dealers, and end-users. The market operates through established distribution networks that have evolved to serve diverse geographical regions and customer segments effectively.

Competitive dynamics are characterized by intense rivalry among domestic and international players, driving innovation and competitive pricing strategies. Market consolidation trends are evident as smaller players face challenges competing with established manufacturers offering comprehensive product portfolios and service networks.

Customer behavior patterns show increasing sophistication in vehicle selection criteria, with operators focusing on total cost of ownership, fuel efficiency, and technology features rather than just initial purchase price. Financing dynamics play a crucial role in market accessibility, with innovative financing solutions enabling broader market participation.

Regulatory dynamics continue to shape market evolution through emission standards, safety requirements, and operational regulations. The implementation of new regulations creates both challenges and opportunities, driving technological advancement while potentially impacting market accessibility for certain customer segments.

Comprehensive market research for the India commercial vehicle market employs multiple data collection and analysis methodologies to ensure accuracy and reliability. Primary research includes extensive interviews with industry stakeholders, including manufacturers, dealers, fleet operators, and technology providers across different market segments and geographical regions.

Secondary research incorporates analysis of industry reports, government statistics, trade publications, and company financial statements to establish market trends and quantitative insights. Data triangulation methods validate findings across multiple sources to ensure consistency and accuracy in market assessment.

Market modeling techniques utilize statistical analysis and forecasting methodologies to project future market trends and growth patterns. Segmentation analysis examines market dynamics across vehicle categories, applications, regions, and customer segments to provide granular insights into market opportunities and challenges.

Expert validation processes involve consultation with industry experts and thought leaders to verify research findings and ensure practical relevance. Continuous monitoring of market developments ensures research remains current and reflects evolving market conditions and emerging trends.

Northern India represents the largest regional market for commercial vehicles, accounting for approximately 35% of total demand. This region benefits from strong industrial activity, agricultural production, and strategic location connecting major economic centers. Delhi NCR serves as a major hub for commercial vehicle distribution and operations.

Western India contributes significantly to market demand, driven by manufacturing concentration in states like Maharashtra and Gujarat. The region’s robust industrial base, port connectivity, and infrastructure development create substantial commercial vehicle requirements across multiple segments.

Southern India shows strong growth potential with expanding IT services, manufacturing, and agricultural sectors driving commercial vehicle demand. Bangalore and Chennai serve as major commercial vehicle markets, while the region’s focus on technology adoption creates opportunities for advanced vehicle solutions.

Eastern India presents emerging opportunities as infrastructure development and industrial growth accelerate. The region’s mineral resources, agricultural production, and improving connectivity create demand for specialized commercial vehicles and transportation solutions.

Market leadership in India’s commercial vehicle sector is characterized by strong domestic players and strategic international partnerships. The competitive environment drives continuous innovation and customer-focused solutions across all vehicle segments.

By Vehicle Type: The market segments into heavy commercial vehicles, medium commercial vehicles, light commercial vehicles, and passenger commercial vehicles. Light commercial vehicles show the highest growth rates due to e-commerce and last-mile delivery requirements.

By Application: Segmentation includes goods transportation, passenger transportation, construction, mining, and specialized applications. Goods transportation represents the largest segment, driven by India’s growing trade and commerce activities.

By Fuel Type: The market includes diesel, petrol, CNG, electric, and hybrid commercial vehicles. Diesel vehicles maintain dominant market share while alternative fuel adoption accelerates in urban areas and specific applications.

By End-User: Market segments encompass individual operators, fleet operators, logistics companies, construction companies, and government organizations. Fleet operators represent the fastest-growing segment as organized logistics services expand.

Heavy Commercial Vehicles serve as the backbone of India’s freight transportation system, handling long-distance and high-capacity cargo movement. This segment benefits from infrastructure development and industrial growth, with operators increasingly focusing on fuel efficiency and advanced safety features.

Medium Commercial Vehicles occupy a crucial position in regional distribution and specialized applications. These vehicles offer optimal balance between payload capacity and maneuverability, making them suitable for urban and semi-urban operations where heavy vehicles face restrictions.

Light Commercial Vehicles experience the most dynamic growth driven by e-commerce expansion and changing urban logistics requirements. Last-mile delivery applications have created new sub-segments including electric three-wheelers and small delivery vans optimized for urban environments.

Passenger Commercial Vehicles including buses and shared mobility solutions address India’s growing urban transportation needs. The segment benefits from government initiatives promoting public transportation and the emergence of organized bus operators serving intercity routes.

Manufacturers benefit from India’s large domestic market, cost-competitive manufacturing environment, and export opportunities to regional markets. The market offers opportunities for product innovation, technology development, and brand building across diverse customer segments.

Fleet operators gain access to advanced vehicle technologies, financing solutions, and service networks that improve operational efficiency and profitability. Digital transformation tools enable better fleet management, route optimization, and maintenance planning.

Component suppliers benefit from the growing market size and increasing local content requirements, creating opportunities for technology transfer and manufacturing expansion. The shift toward electric and connected vehicles opens new component categories and value chains.

Financial institutions find opportunities in vehicle financing, insurance, and related financial services as the market expands and formalizes. Government stakeholders benefit from improved logistics efficiency, economic growth, and employment generation across the commercial vehicle ecosystem.

Strengths:

Weaknesses:

Opportunities:

Threats:

Electrification trends are gaining momentum across commercial vehicle segments, driven by environmental concerns and government incentives. Electric light commercial vehicles are leading adoption in urban areas, while heavy-duty electric vehicles are being tested for specific applications and routes.

Connected vehicle technologies are transforming fleet operations through real-time monitoring, predictive maintenance, and route optimization. Telematics adoption has accelerated as operators recognize the value of data-driven decision making and operational efficiency improvements.

Shared mobility trends are creating new business models and vehicle requirements, particularly in urban passenger transportation. Fleet-as-a-Service models are emerging as alternatives to traditional vehicle ownership, offering flexibility and reduced capital requirements for operators.

Customization trends reflect diverse application requirements, with manufacturers offering specialized vehicle configurations for specific industries and use cases. Modular design approaches enable efficient customization while maintaining manufacturing economies of scale.

Technology partnerships between traditional manufacturers and technology companies are accelerating innovation in areas like electric powertrains, autonomous driving, and connected services. These collaborations combine automotive expertise with cutting-edge technology capabilities.

Manufacturing expansion initiatives include new production facilities, capacity increases, and technology upgrades to meet growing demand and evolving product requirements. Local manufacturing of electric vehicle components is receiving particular focus from both companies and government policy.

Service network expansion efforts aim to improve customer support and vehicle uptime across India’s diverse geographical regions. Digital service platforms are being deployed to enhance service efficiency and customer experience.

Regulatory developments including updated emission standards, safety requirements, and electric vehicle policies continue to shape industry direction and investment priorities. MarkWide Research analysis indicates that regulatory alignment with global standards is driving technology advancement across the sector.

Strategic focus on electric vehicle development and infrastructure is essential for long-term competitiveness. Companies should invest in electric powertrain technology, charging infrastructure partnerships, and customer education to capitalize on the transition toward sustainable transportation.

Technology integration should prioritize connected vehicle capabilities, data analytics, and customer-facing digital services. Digital transformation initiatives can differentiate offerings and create new revenue streams beyond traditional vehicle sales.

Market expansion strategies should target underserved regions and emerging customer segments, particularly in rural areas and specialized applications. Localized product development can address specific regional requirements and preferences.

Partnership strategies with technology companies, financial institutions, and service providers can enhance value propositions and market reach. Ecosystem development approaches that address complete customer needs beyond vehicle supply can create competitive advantages and customer loyalty.

Long-term growth prospects for India’s commercial vehicle market remain robust, supported by continued economic development, infrastructure investment, and technological advancement. MWR projections indicate sustained growth across all vehicle segments with particular strength in electric and connected vehicle categories.

Technology evolution will continue reshaping the market with autonomous driving capabilities, advanced safety systems, and integrated digital services becoming standard features. The convergence of automotive and technology sectors will create new business models and value propositions.

Sustainability focus will drive adoption of alternative fuel technologies and circular economy principles in vehicle design and manufacturing. Environmental regulations and customer preferences will accelerate the transition toward cleaner transportation solutions.

Market maturation is expected to bring greater consolidation, improved operational efficiency, and enhanced customer service standards. The evolution toward organized fleet operations and professional logistics services will create opportunities for premium vehicle offerings and value-added services.

India’s commercial vehicle market represents a dynamic and rapidly evolving sector with substantial growth potential driven by economic development, infrastructure investment, and technological advancement. The market’s transformation from traditional transportation solutions toward connected, sustainable, and efficient vehicle systems reflects broader changes in India’s economic landscape.

Strategic opportunities exist across all market segments, with particular promise in electric vehicles, connected technologies, and specialized applications. Success in this market requires understanding diverse customer needs, regulatory requirements, and regional variations while maintaining focus on innovation and operational excellence.

Future success will depend on companies’ ability to adapt to changing market conditions, embrace new technologies, and develop comprehensive solutions that address evolving customer requirements. The India commercial vehicle market is positioned to play a crucial role in the country’s economic growth and transformation toward sustainable transportation systems.

What is Commercial Vehicle (CV)?

Commercial vehicles (CV) refer to motor vehicles designed primarily for transporting goods or passengers for commercial purposes. This includes trucks, buses, and vans used in various industries such as logistics, construction, and public transport.

What are the key players in the India Commercial Vehicle (CV) Market?

Key players in the India Commercial Vehicle (CV) Market include Tata Motors, Ashok Leyland, Mahindra & Mahindra, and Eicher Motors, among others. These companies are known for their diverse range of commercial vehicles catering to different sectors.

What are the growth factors driving the India Commercial Vehicle (CV) Market?

The growth of the India Commercial Vehicle (CV) Market is driven by increasing urbanization, rising demand for goods transportation, and government initiatives to improve infrastructure. Additionally, the expansion of e-commerce is significantly boosting the need for logistics and delivery vehicles.

What challenges does the India Commercial Vehicle (CV) Market face?

The India Commercial Vehicle (CV) Market faces challenges such as fluctuating fuel prices, stringent emission regulations, and competition from alternative transport modes. These factors can impact profitability and operational efficiency for manufacturers and operators.

What opportunities exist in the India Commercial Vehicle (CV) Market?

Opportunities in the India Commercial Vehicle (CV) Market include the adoption of electric vehicles, advancements in telematics, and the growing demand for last-mile delivery solutions. These trends are expected to shape the future of commercial transportation in the country.

What trends are shaping the India Commercial Vehicle (CV) Market?

Trends in the India Commercial Vehicle (CV) Market include the shift towards sustainable transportation solutions, the integration of smart technologies, and the increasing focus on safety features. These innovations are enhancing vehicle performance and meeting evolving consumer expectations.

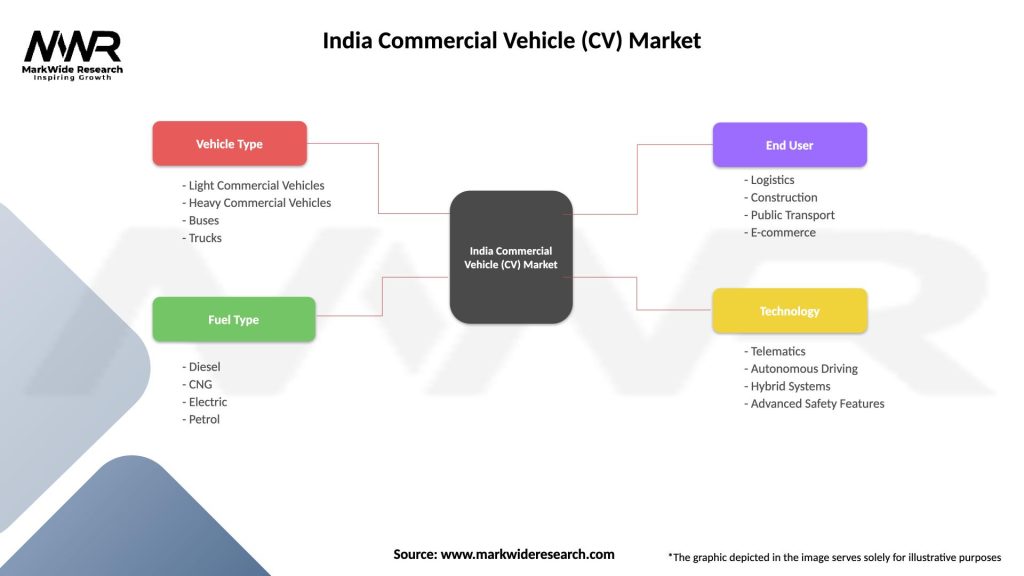

India Commercial Vehicle (CV) Market

| Segmentation Details | Description |

|---|---|

| Vehicle Type | Light Commercial Vehicles, Heavy Commercial Vehicles, Buses, Trucks |

| Fuel Type | Diesel, CNG, Electric, Petrol |

| End User | Logistics, Construction, Public Transport, E-commerce |

| Technology | Telematics, Autonomous Driving, Hybrid Systems, Advanced Safety Features |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the India Commercial Vehicle (CV) Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.