Income protection insurance, also known as disability income insurance, is a type of insurance policy that provides financial protection to individuals in the event they are unable to work due to illness, injury, or disability. This insurance coverage replaces a portion of the insured individual’s income, typically up to a specified percentage, for a defined period, helping them maintain their standard of living and meet their financial obligations during periods of incapacity.

Meaning:

Income protection insurance is designed to safeguard individuals against the financial consequences of losing their income due to unforeseen circumstances such as illness, injury, or disability. It provides a monthly benefit payment to policyholders who are unable to work and earn an income, ensuring they can cover essential expenses such as mortgage or rent payments, utility bills, groceries, and medical costs.

Executive Summary:

The income protection insurance market has witnessed steady growth in recent years, driven by increasing awareness of the importance of financial security, changing workforce dynamics, and rising demand for comprehensive insurance coverage. This market offers significant opportunities for insurers to develop innovative products, expand their customer base, and strengthen their market presence by addressing evolving customer needs and preferences.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights:

Growing Awareness: There is a growing awareness among individuals about the need for income protection insurance to safeguard their financial well-being in the event of unexpected disruptions to their income streams.

Changing Workforce Dynamics: The changing nature of work, including the rise of gig economy jobs, self-employment, and flexible work arrangements, has led to increased interest in income protection insurance among workers without traditional employer-sponsored benefits.

Pandemic Impact: The COVID-19 pandemic has highlighted the importance of income protection insurance, as it has underscored the vulnerability of individuals to unforeseen health crises and economic disruptions.

Advancements in Underwriting: Insurers are leveraging advancements in data analytics, predictive modeling, and risk assessment techniques to enhance underwriting processes and offer more tailored and competitive income protection insurance products.

Market Drivers:

Income Insecurity: Concerns about income insecurity due to job loss, illness, or injury drive individuals to seek income protection insurance coverage to mitigate financial risks and ensure financial stability for themselves and their families.

Regulatory Support: Regulatory initiatives aimed at promoting financial inclusion and consumer protection, such as mandated disability insurance provisions and tax incentives for purchasing income protection insurance, drive market growth and penetration.

Rising Healthcare Costs: The escalating costs of healthcare services and medical treatments incentivize individuals to invest in income protection insurance to offset potential income loss resulting from illness or injury-related medical expenses.

Employer Offerings: Increasingly, employers are recognizing the value of income protection insurance as part of their employee benefits packages to attract and retain talent, enhance employee satisfaction, and demonstrate commitment to employee well-being.

Market Restraints:

Affordability Concerns: Affordability concerns, including premium costs and coverage limitations, may deter some individuals from purchasing income protection insurance, especially those with limited discretionary income or competing financial priorities.

Complexity of Products: The complexity of income protection insurance products, including the variety of policy options, coverage features, and exclusions, may confuse consumers and deter them from exploring or purchasing coverage.

Underwriting Challenges: Underwriting income protection insurance policies for individuals with pre-existing health conditions or high-risk occupations poses challenges for insurers in assessing and pricing risk, potentially leading to higher premiums or coverage restrictions.

Distribution Channels: Limited awareness and availability of income protection insurance through traditional distribution channels, such as insurance agents and brokers, may hinder market penetration and reach among target customer segments.

Market Opportunities:

Product Innovation: Opportunities exist for insurers to develop innovative income protection insurance products tailored to specific customer segments, such as gig workers, freelancers, and self-employed individuals, addressing their unique needs and preferences.

Digital Distribution: Leveraging digital distribution channels, including online platforms, mobile apps, and direct-to-consumer channels, enables insurers to reach a broader audience, streamline the purchasing process, and enhance customer engagement and satisfaction.

Value-added Services: Offering value-added services, such as wellness programs, rehabilitation support, and return-to-work assistance, alongside income protection insurance coverage, enhances the value proposition for policyholders and differentiates insurers in the market.

Partnerships and Alliances: Collaborating with employers, trade associations, financial advisors, and healthcare providers can expand insurers’ distribution networks, increase market visibility, and enhance customer education and awareness about income protection insurance.

Market Dynamics:

The income protection insurance market operates in a dynamic environment shaped by various factors, including economic conditions, regulatory changes, technological advancements, and consumer behaviors. Understanding the market dynamics is essential for insurers to identify opportunities, address challenges, and capitalize on emerging trends to drive growth and profitability.

Regional Analysis:

The income protection insurance market exhibits regional variations in terms of market maturity, regulatory frameworks, consumer preferences, and distribution channels. While developed markets such as North America and Europe have well-established income protection insurance markets, emerging economies in Asia Pacific, Latin America, and Africa offer untapped growth opportunities due to rising income levels, increasing urbanization, and expanding insurance awareness.

Competitive Landscape:

Leading Companies in the Income Protection Insurance Market:

MetLife, Inc.

Aflac Incorporated

Unum Group

The Hartford Financial Services Group, Inc.

Cigna Corporation

Prudential Financial, Inc.

Guardian Life Insurance Company of America

Mutual of Omaha Insurance Company

Principal Financial Group

State Farm

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

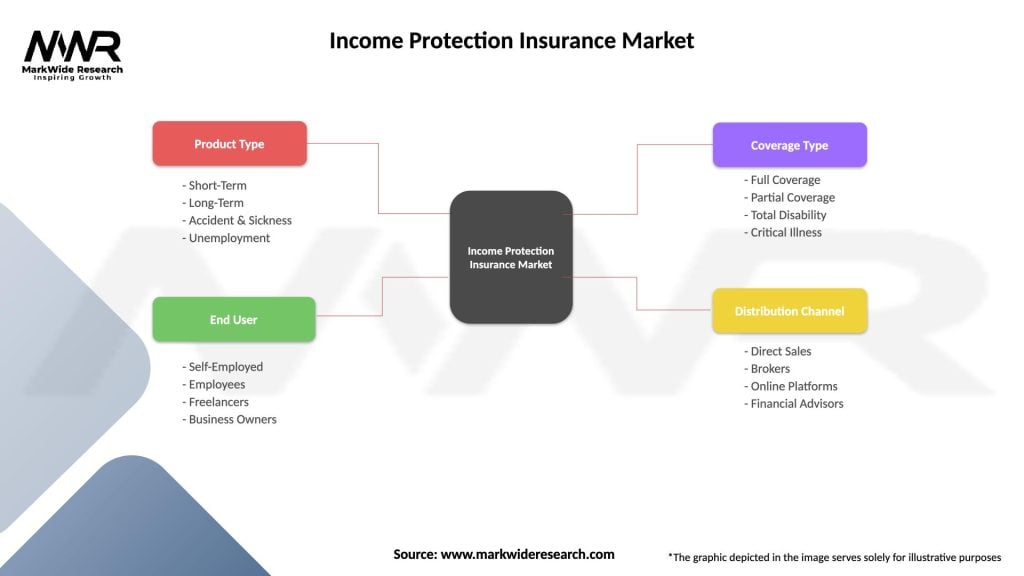

Segmentation:

The income protection insurance market can be segmented based on various factors such as:

Policy Type: Individual Income Protection Insurance, Group Income Protection Insurance, and Mortgage Protection Insurance.

Coverage Duration: Short-term Disability Insurance and Long-term Disability Insurance.

Occupational Class: Professional and White-collar Workers, Blue-collar Workers, and High-risk Occupations.

Distribution Channel: Insurance Agents and Brokers, Direct-to-Consumer Channels, Employer-sponsored Benefits, and Online Platforms.

Segmentation enables insurers to tailor their product offerings, pricing strategies, and marketing campaigns to specific customer segments, enhancing relevance and competitiveness in the market.

Category-wise Insights:

Individual Income Protection Insurance: Individual income protection insurance policies provide coverage to individuals, offering financial protection against income loss due to illness, injury, or disability, enabling policyholders to maintain their standard of living and financial security.

Group Income Protection Insurance: Group income protection insurance plans are typically offered by employers as part of their employee benefits packages, providing coverage to a group of employees, ensuring financial protection and peace of mind for both employers and employees.

Mortgage Protection Insurance: Mortgage protection insurance policies are designed to cover mortgage payments in the event of the insured individual’s disability, illness, or death, ensuring that their mortgage obligations are met, and their family’s home is protected from foreclosure.

Short-term Disability Insurance: Short-term disability insurance provides temporary income replacement for individuals unable to work due to a covered illness, injury, or medical condition, typically offering benefits for a limited duration, such as three to six months.

Long-term Disability Insurance: Long-term disability insurance provides ongoing income replacement for individuals with severe or long-lasting disabilities that prevent them from working for an extended period, typically until retirement age or the policy’s expiration.

Key Benefits for Policyholders:

Financial Security: Income protection insurance provides financial security and peace of mind to policyholders, ensuring they can maintain their standard of living and meet their financial obligations during periods of incapacity.

Income Replacement: Income protection insurance replaces a portion of the insured individual’s lost income, enabling them to cover essential expenses such as mortgage or rent payments, utility bills, groceries, and medical costs.

Flexibility: Income protection insurance offers flexibility in coverage options, benefit amounts, and duration, allowing policyholders to customize their coverage to meet their specific needs, preferences, and budget constraints.

Return-to-Work Support: Some income protection insurance policies offer additional services and support, such as vocational rehabilitation, return-to-work programs, and job retraining assistance, to help policyholders transition back to work and regain financial independence.

SWOT Analysis:

Strengths:

Financial Security and Peace of Mind

Customizable Coverage Options

Return-to-Work Support Services

Employer-sponsored Benefits

Weaknesses:

Affordability Concerns

Complexity of Products

Coverage Limitations

Underwriting Challenges

Opportunities:

Product Innovation

Digital Distribution Channels

Value-added Services

Emerging Markets

Threats:

Economic Uncertainty

Regulatory Changes

Competitive Pressures

Cybersecurity Risks

Market Key Trends:

Digital Transformation: Insurers are investing in digital transformation initiatives, including online platforms, mobile apps, and digital underwriting processes, to enhance customer experience, streamline operations, and improve distribution efficiency.

Personalization: The demand for personalized insurance solutions is increasing, with insurers leveraging data analytics, artificial intelligence, and machine learning to tailor products, pricing, and services to individual customer needs and preferences.

Wellness Programs: Insurers are offering wellness programs, health incentives, and lifestyle rewards to encourage policyholders to adopt healthier behaviors, reduce risks, and mitigate the likelihood of illness, injury, or disability.

Regulatory Compliance: Regulatory compliance remains a top priority for insurers, with ongoing scrutiny, enforcement actions, and regulatory changes shaping product design, sales practices, and customer communications in the income protection insurance market.

Covid-19 Impact:

The COVID-19 pandemic has had a significant impact on the income protection insurance market, highlighting the importance of financial security, risk management, and insurance coverage in uncertain times. Some key impacts of COVID-19 on the income protection insurance market include:

Increased Awareness: The pandemic has raised awareness of the need for income protection insurance, as individuals recognize the importance of financial security and income replacement in the event of illness, injury, or disability.

Rising Demand: The economic impact of the pandemic, including job losses, furloughs, and income instability, has driven increased demand for income protection insurance, as individuals seek to safeguard their financial well-being and mitigate income risks.

Shift in Coverage Priorities: The pandemic has prompted individuals to reassess their insurance coverage priorities, with a greater emphasis on income protection, disability insurance, and critical illness coverage to address new risks and uncertainties.

Claims Experience: Insurers have experienced changes in claims experience and risk profiles due to the pandemic, with fluctuations in claim volumes, durations, and severity levels, leading to adjustments in underwriting practices and pricing strategies.

Key Industry Developments:

Digital Innovation: Insurers are accelerating digital innovation initiatives, including digital underwriting, online claims processing, and virtual customer interactions, to adapt to changing customer preferences, enhance operational efficiency, and improve service delivery.

Product Enhancements: Insurers are enhancing income protection insurance products with new features, benefits, and riders, such as pandemic coverage, remote work disability benefits, and mental health support, to address emerging customer needs and market trends.

Customer Engagement: Insurers are investing in customer engagement initiatives, including educational campaigns, financial literacy programs, and interactive tools, to increase awareness, understanding, and uptake of income protection insurance among target customer segments.

Regulatory Compliance: Insurers are closely monitoring regulatory developments, including changes in disability insurance regulations, claims handling requirements, and consumer protection laws, to ensure compliance and mitigate regulatory risks in the income protection insurance market.

Analyst Suggestions:

Educational Outreach: Insurers should prioritize educational outreach and consumer awareness campaigns to educate individuals about the importance of income protection insurance, the benefits of coverage, and the options available to them.

Product Simplification: Insurers should simplify income protection insurance products, streamline policy options, and clarify coverage terms and conditions to make insurance more accessible, understandable, and appealing to consumers.

Digital Transformation: Insurers should embrace digital transformation initiatives, including online distribution channels, digital marketing strategies, and customer self-service portals, to enhance customer engagement, streamline operations, and improve the overall customer experience.

Collaborative Partnerships: Insurers should collaborate with employers, industry associations, and healthcare providers to promote income protection insurance, integrate insurance offerings into employee benefits packages, and leverage data insights to develop targeted marketing and distribution strategies.

Future Outlook:

The future outlook for the income protection insurance market remains positive, driven by factors such as increasing awareness of financial risks, changing workforce dynamics, and evolving regulatory priorities. As individuals prioritize financial security and risk management, the demand for income protection insurance is expected to grow, presenting opportunities for insurers to innovate, expand market reach, and enhance customer engagement.

Conclusion:

In conclusion, the income protection insurance market plays a vital role in providing financial security and peace of mind to individuals facing the risk of income loss due to illness, injury, or disability. As insurers navigate evolving market dynamics, regulatory challenges, and customer expectations, embracing digital innovation, enhancing product offerings, and fostering consumer education and engagement are essential for driving growth, profitability, and sustainability in the income protection insurance market. By addressing emerging trends, seizing opportunities, and meeting the evolving needs of customers, insurers can strengthen their market position, build customer trust, and contribute to a more resilient and inclusive insurance ecosystem.

What is Income Protection Insurance?

Income Protection Insurance is a type of insurance that provides financial support to individuals who are unable to work due to illness or injury. It typically covers a portion of the insured’s income, helping them manage living expenses during their recovery period.

What are the key players in the Income Protection Insurance Market?

Key players in the Income Protection Insurance Market include companies like Aviva, Legal & General, and Aegon, which offer various income protection products tailored to different consumer needs, among others.

What are the main drivers of growth in the Income Protection Insurance Market?

The main drivers of growth in the Income Protection Insurance Market include increasing awareness of financial security, rising healthcare costs, and a growing emphasis on employee benefits by employers. These factors contribute to a higher demand for income protection solutions.

What challenges does the Income Protection Insurance Market face?

The Income Protection Insurance Market faces challenges such as regulatory changes, the complexity of policy terms, and competition from alternative insurance products. These factors can hinder market growth and consumer understanding.

What opportunities exist in the Income Protection Insurance Market?

Opportunities in the Income Protection Insurance Market include the development of innovative products that cater to gig economy workers and the integration of technology for easier claims processing. Additionally, increasing consumer awareness presents a chance for market expansion.

What trends are shaping the Income Protection Insurance Market?

Trends shaping the Income Protection Insurance Market include the rise of digital platforms for policy management, personalized insurance offerings based on individual risk assessments, and a focus on mental health coverage. These trends reflect changing consumer preferences and technological advancements.

Leading Companies in the Income Protection Insurance Market:

MetLife, Inc.

Aflac Incorporated

Unum Group

The Hartford Financial Services Group, Inc.

Cigna Corporation

Prudential Financial, Inc.

Guardian Life Insurance Company of America

Mutual of Omaha Insurance Company

Principal Financial Group

State Farm

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.