444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

Market Overview

The hydroclassifier market plays a crucial role in the mineral processing industry, providing efficient separation and classification of particles based on their size, shape, and density. Hydroclassifiers, also known as hydraulic classifiers, utilize the principle of fluid dynamics to separate particles in a slurry based on their settling rates. These systems are widely used in various applications, including ore beneficiation, sand and aggregate processing, and wastewater treatment.

Meaning

Hydroclassifiers are mechanical devices used for the separation and classification of particles in a slurry based on their settling characteristics. These systems utilize the principle of fluid dynamics, typically employing water or another liquid medium, to create a controlled environment where particles of different sizes and densities settle at different rates. Hydroclassifiers are used in mineral processing operations to efficiently separate valuable minerals from gangue materials, as well as in other industries for particle classification and separation purposes.

Executive Summary

The hydroclassifier market has witnessed significant growth due to increasing demand for efficient particle separation technologies in industries such as mining, construction, and environmental engineering. Hydroclassifiers offer advantages such as high efficiency, low maintenance requirements, and versatility in handling a wide range of particle sizes and densities. Despite market growth, challenges such as regulatory compliance, technological limitations, and competition from alternative separation methods need to be addressed. Understanding key market insights, trends, and dynamics is essential for stakeholders to capitalize on growth opportunities and overcome market challenges effectively.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Market Drivers

Market Restraints

Market Opportunities

Market Dynamics

The hydroclassifier market dynamics are shaped by technological innovations, regulatory compliance, and industry-specific applications across mining, wastewater treatment, and recycling sectors. Market players focus on sustainable practices, operational efficiency, and customer-centric solutions to maintain competitive advantage and foster market growth.

Regional Analysis

Competitive Landscape

Leading Companies in Hydroclassifier Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

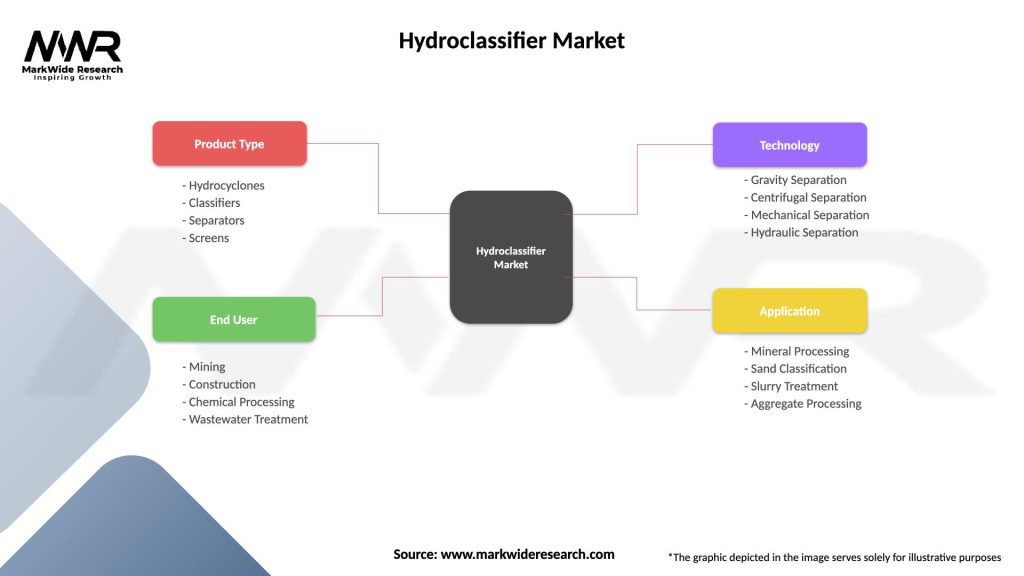

Segmentation

The hydroclassifier market can be segmented based on:

Category-wise Insights

Key Benefits for Industry Participants and Stakeholders

SWOT Analysis

Market Key Trends

Covid-19 Impact

The Covid-19 pandemic underscored the importance of resilient supply chains and operational continuity in the hydroclassifier market. Manufacturers adapted to remote work protocols, implemented safety measures, and ensured business continuity to meet critical infrastructure demands amid global disruptions.

Key Industry Developments

Analyst Suggestions

Future Outlook

The hydroclassifier market is poised for growth, driven by technological advancements, environmental sustainability initiatives, and increasing industrial automation. Stakeholders focusing on innovation, market expansion, and sustainability will navigate competitive landscapes successfully, contributing to enhanced process efficiency and environmental stewardship globally.

Conclusion

The hydroclassifier market plays a pivotal role in industrial particle separation and environmental management, ensuring operational efficiency, regulatory compliance, and sustainability across diverse sectors. Despite challenges, including cost constraints and competitive pressures, market outlook remains optimistic with rising demand for efficient particle classification solutions. Stakeholders embracing technological innovations, sustainability practices, and customer-centric strategies will drive market evolution and foster resilient infrastructure development worldwide.

What is Hydroclassifier?

A Hydroclassifier is a type of equipment used in the mineral processing industry to separate particles based on their size and density. It utilizes water as a medium to classify materials, making it essential for applications in mining, aggregates, and recycling.

What are the key players in the Hydroclassifier Market?

Key players in the Hydroclassifier Market include companies such as Metso Outotec, FLSmidth, Weir Group, and Schenck Process, among others. These companies are known for their innovative solutions and technologies in mineral processing.

What are the growth factors driving the Hydroclassifier Market?

The Hydroclassifier Market is driven by increasing demand for efficient mineral processing solutions, the growth of the mining industry, and the need for sustainable practices in resource extraction. Additionally, advancements in technology are enhancing the performance of hydroclassifiers.

What challenges does the Hydroclassifier Market face?

Challenges in the Hydroclassifier Market include the high initial investment costs for advanced equipment and the need for skilled operators to manage complex systems. Furthermore, fluctuations in raw material prices can impact market stability.

What opportunities exist in the Hydroclassifier Market?

Opportunities in the Hydroclassifier Market include the development of eco-friendly technologies and the expansion of applications in waste management and recycling. Additionally, emerging markets present new avenues for growth.

What trends are shaping the Hydroclassifier Market?

Trends in the Hydroclassifier Market include the integration of automation and digital technologies to enhance operational efficiency. There is also a growing focus on sustainability, with companies seeking to reduce water usage and improve energy efficiency.

Hydroclassifier Market

| Segmentation Details | Description |

|---|---|

| Product Type | Hydrocyclones, Classifiers, Separators, Screens |

| End User | Mining, Construction, Chemical Processing, Wastewater Treatment |

| Technology | Gravity Separation, Centrifugal Separation, Mechanical Separation, Hydraulic Separation |

| Application | Mineral Processing, Sand Classification, Slurry Treatment, Aggregate Processing |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading Companies in Hydroclassifier Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

North America

o US

o Canada

o Mexico

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA