444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Hong Kong data center rack market represents a critical infrastructure component driving the region’s digital transformation and cloud computing expansion. Hong Kong’s strategic position as Asia’s financial hub and gateway to mainland China has positioned it as a premier data center destination, creating substantial demand for advanced rack solutions. The market encompasses various rack types including open frame racks, enclosed server racks, wall-mount racks, and specialized cooling-integrated systems designed to support high-density computing environments.

Market dynamics indicate robust growth driven by increasing digitalization across financial services, telecommunications, and e-commerce sectors. The territory’s data center infrastructure continues expanding to meet growing demands for cloud services, artificial intelligence applications, and edge computing solutions. Colocation facilities and hyperscale data centers are driving significant rack deployment, with operators seeking energy-efficient and space-optimized solutions to maximize operational efficiency.

Regional advantages including excellent connectivity, political stability, and proximity to major Asian markets have attracted international cloud service providers and enterprises to establish data center operations in Hong Kong. This influx has created sustained demand for high-quality rack systems capable of supporting mission-critical applications and ensuring optimal performance in Hong Kong’s challenging climate conditions.

The Hong Kong data center rack market refers to the comprehensive ecosystem of physical infrastructure solutions designed to house, organize, and support IT equipment within data center facilities across the Hong Kong Special Administrative Region. These rack systems serve as the fundamental building blocks for data center operations, providing structured mounting solutions for servers, storage devices, networking equipment, and power distribution units.

Data center racks in Hong Kong’s market encompass various configurations including standard 19-inch racks, 23-inch telecommunications racks, open frame designs, and enclosed cabinets with integrated cooling and power management systems. The market includes both traditional rack solutions and innovative designs incorporating advanced features such as intelligent monitoring, modular components, and enhanced airflow management to address Hong Kong’s specific environmental and operational requirements.

Market scope extends beyond basic rack hardware to include complementary solutions such as cable management systems, power distribution units, cooling accessories, and monitoring technologies that collectively enable efficient data center operations in Hong Kong’s competitive landscape.

Hong Kong’s data center rack market demonstrates exceptional growth momentum driven by the territory’s position as a regional digital hub and increasing enterprise cloud adoption. The market benefits from strong government support for digital infrastructure development and Hong Kong’s role as a preferred location for international data center investments targeting the Asia-Pacific region.

Key market drivers include the rapid expansion of financial technology services, growing demand for low-latency connectivity to mainland China, and increasing adoption of hybrid cloud architectures by multinational corporations. The market shows 65% preference for enclosed rack solutions among enterprise customers, reflecting heightened security and environmental control requirements in Hong Kong’s data center facilities.

Technological advancement remains a critical factor, with operators increasingly demanding intelligent rack systems featuring integrated monitoring, automated management capabilities, and enhanced energy efficiency. The market exhibits strong growth in high-density rack configurations as organizations seek to maximize computing power within limited real estate footprints, particularly relevant given Hong Kong’s premium property costs.

Competitive landscape features both international rack manufacturers and regional suppliers, with customers prioritizing reliability, local support capabilities, and compliance with international standards. Market projections indicate continued expansion driven by 5G network deployment, edge computing requirements, and increasing data sovereignty considerations among enterprises operating in the region.

Strategic positioning of Hong Kong as Asia’s data center gateway continues driving rack market expansion, with several key insights shaping market development:

Digital transformation initiatives across Hong Kong’s economy serve as the primary catalyst for data center rack market expansion. Financial institutions are modernizing their IT infrastructure to support digital banking services, algorithmic trading platforms, and regulatory compliance systems, creating substantial demand for high-performance rack solutions capable of supporting mission-critical applications.

Cloud adoption acceleration among enterprises has significantly increased data center capacity requirements. Organizations are implementing hybrid cloud strategies that combine on-premises infrastructure with public cloud services, necessitating flexible rack configurations that can accommodate diverse equipment types and evolving technology requirements. This trend has driven 58% growth in modular rack system adoption among Hong Kong enterprises.

Government digitalization programs and smart city initiatives are creating new infrastructure demands. The Hong Kong government’s commitment to digital governance and citizen services requires robust data center capabilities, driving public sector investment in secure, reliable rack systems that meet stringent performance and security standards.

International connectivity requirements position Hong Kong as a critical hub for cross-border data flows. The territory’s unique position facilitating communication between international markets and mainland China creates demand for high-capacity rack systems supporting international submarine cable landing stations and carrier-neutral facilities.

Artificial intelligence and machine learning applications are driving demand for specialized rack configurations optimized for GPU-intensive workloads. Financial services firms, research institutions, and technology companies are deploying AI systems requiring high-density rack solutions with enhanced cooling and power distribution capabilities.

Real estate constraints represent the most significant challenge facing Hong Kong’s data center rack market. The territory’s limited land availability and extremely high property costs create pressure for maximum space utilization, potentially limiting data center expansion and constraining rack deployment opportunities. Operators must carefully balance capacity requirements with available real estate, often requiring premium-priced solutions to achieve desired density levels.

Power infrastructure limitations pose ongoing challenges for data center operations. Hong Kong’s electricity costs rank among the world’s highest, creating pressure for energy-efficient rack designs while potentially limiting the scale of high-power density deployments. Grid capacity constraints in certain areas may restrict data center development, indirectly impacting rack market growth potential.

Skilled workforce shortage affects data center operations and maintenance capabilities. The specialized nature of modern rack systems requires trained technicians for installation, configuration, and ongoing maintenance. Limited local expertise in advanced rack technologies may slow adoption of sophisticated solutions and increase operational costs for data center operators.

Regulatory complexity surrounding cross-border data flows creates uncertainty for international operators. Evolving data sovereignty requirements and compliance obligations may influence rack configuration decisions, potentially favoring certain technologies or vendors over others. Compliance costs associated with meeting multiple regulatory frameworks can impact overall project economics.

Supply chain vulnerabilities have become increasingly apparent, particularly for specialized rack components and accessories. Global semiconductor shortages and logistics disruptions can delay rack deliveries and increase costs, potentially impacting data center deployment schedules and project timelines.

Edge computing expansion presents substantial opportunities for rack market growth as organizations deploy distributed computing infrastructure closer to end users. The proliferation of IoT devices and demand for low-latency applications creates need for edge data centers throughout Hong Kong, requiring specialized rack solutions optimized for smaller footprints and remote management capabilities.

Greater Bay Area integration offers significant growth potential as Hong Kong strengthens economic ties with mainland Chinese cities. Cross-border business expansion creates demand for standardized rack systems that can support consistent IT infrastructure across multiple locations while meeting varying regulatory requirements in different jurisdictions.

Sustainable technology adoption creates opportunities for innovative rack solutions incorporating advanced cooling technologies, renewable energy integration, and circular economy principles. Organizations increasingly prioritize environmental sustainability, creating market demand for rack systems that demonstrate measurable efficiency improvements and reduced environmental impact.

Artificial intelligence infrastructure requirements continue expanding, creating opportunities for specialized rack configurations optimized for AI workloads. The growing adoption of machine learning applications across financial services, healthcare, and logistics sectors drives demand for high-performance computing infrastructure requiring advanced rack solutions.

5G network deployment creates new infrastructure requirements for telecommunications operators and enterprises. The rollout of 5G services necessitates distributed antenna systems and edge computing capabilities, creating opportunities for rack solutions designed specifically for telecommunications applications and small cell deployments.

Disaster recovery and business continuity planning has gained increased attention, creating opportunities for rack solutions supporting redundant infrastructure and rapid deployment capabilities. Organizations seek resilient rack systems that can support critical operations during disruptions and facilitate quick recovery procedures.

Supply and demand dynamics in Hong Kong’s data center rack market reflect the territory’s unique position as a regional technology hub. Demand patterns show strong correlation with broader economic cycles, financial market activity, and technology adoption trends across Asia-Pacific markets. The market demonstrates 43% seasonal variation aligned with corporate budget cycles and major technology refresh periods.

Pricing dynamics are influenced by multiple factors including raw material costs, logistics expenses, and local market competition. Premium pricing for advanced rack solutions reflects Hong Kong’s position as a high-value market where performance and reliability often outweigh cost considerations. Customers demonstrate willingness to invest in superior solutions that deliver operational advantages and long-term value.

Technology evolution drives continuous market transformation as rack manufacturers introduce innovative features addressing emerging requirements. Intelligent rack systems incorporating IoT sensors, automated management capabilities, and predictive maintenance features are gaining traction among sophisticated operators seeking operational efficiency improvements.

Competitive dynamics feature both established international vendors and emerging regional suppliers competing across different market segments. Market consolidation trends are evident as larger vendors acquire specialized companies to expand their solution portfolios and strengthen their position in Hong Kong’s competitive landscape.

Customer behavior patterns show increasing sophistication in procurement processes, with buyers conducting detailed technical evaluations and requiring comprehensive support services. Long-term partnerships between rack suppliers and data center operators are becoming more common as both parties seek to optimize total cost of ownership and operational performance.

Comprehensive market analysis for Hong Kong’s data center rack market employed multiple research methodologies to ensure accuracy and completeness of findings. Primary research activities included structured interviews with data center operators, rack manufacturers, system integrators, and end-user organizations across various industry sectors to gather firsthand insights into market trends, challenges, and opportunities.

Secondary research encompassed analysis of industry reports, government publications, trade association data, and company financial statements to establish market context and validate primary research findings. MarkWide Research analysts conducted extensive review of regulatory frameworks, infrastructure development plans, and economic indicators affecting Hong Kong’s data center industry.

Market sizing methodology utilized bottom-up analysis combining data center capacity assessments, rack density calculations, and replacement cycle analysis to establish comprehensive market parameters. Quantitative analysis incorporated statistical modeling to project growth trends and identify key market drivers based on historical data and forward-looking indicators.

Competitive landscape analysis involved detailed evaluation of major market participants including product portfolios, market positioning, and strategic initiatives. Technology assessment examined emerging trends, innovation patterns, and adoption rates across different customer segments to identify future market directions.

Data validation processes included cross-referencing multiple sources, conducting follow-up interviews, and applying statistical techniques to ensure research accuracy and reliability. Expert panel reviews provided additional validation and insights from industry specialists with extensive Hong Kong market experience.

Hong Kong Island represents the premium segment of the data center rack market, hosting the majority of financial services data centers and international carrier facilities. Central and Admiralty districts concentrate high-value deployments requiring advanced rack solutions with enhanced security features and premium support services. This area accounts for approximately 38% of total rack deployments despite limited physical space, reflecting the high-density, high-value nature of operations.

Kowloon Peninsula serves as a major data center hub with several large colocation facilities and carrier-neutral data centers. Kwai Tsing and Tsuen Wan areas have emerged as preferred locations for hyperscale deployments due to better land availability and proximity to submarine cable landing points. The region shows rapid growth in standardized rack deployments supporting multi-tenant facilities and cloud service provider operations.

New Territories represents the fastest-growing segment for data center development, offering more space for large-scale facilities at relatively lower costs. Tseung Kwan O has become a major data center cluster with several international operators establishing significant presence, driving demand for large-scale rack deployments. The area accounts for 45% of new rack installations as operators seek cost-effective expansion opportunities.

Cross-border connectivity zones near the mainland China border are gaining importance for data centers supporting cross-border business operations. Specialized rack configurations in these areas must accommodate equipment from multiple vendors and support diverse connectivity requirements for international and domestic networks.

Edge computing locations distributed throughout Hong Kong’s urban areas are creating demand for smaller-scale rack deployments. Retail locations, office buildings, and telecommunications facilities increasingly require compact rack solutions supporting distributed computing infrastructure and 5G network equipment.

Market leadership in Hong Kong’s data center rack sector is characterized by intense competition among international vendors and specialized regional suppliers. The competitive environment reflects customers’ demanding requirements for reliability, performance, and comprehensive support services in this critical infrastructure market.

Competitive strategies focus on differentiation through technology innovation, local support capabilities, and comprehensive solution portfolios. Market leaders are investing in research and development to address emerging requirements such as edge computing, AI workloads, and sustainability objectives while maintaining strong relationships with major data center operators and system integrators.

By Product Type:

By Rack Unit Size:

By End-User Industry:

By Deployment Type:

Enterprise Segment Analysis:

Financial services organizations dominate the premium rack market segment, requiring solutions that combine high performance with stringent security features. These customers typically specify enclosed rack systems with advanced access controls, environmental monitoring, and integration capabilities for sophisticated management systems. Investment banks and trading firms show particular preference for high-density configurations supporting low-latency computing infrastructure.

Colocation Market Dynamics:

Third-party data center operators represent the fastest-growing customer segment, driving demand for standardized rack solutions that can accommodate diverse tenant requirements. Modular rack systems with flexible configuration options are increasingly popular, allowing operators to adapt quickly to changing customer needs while maintaining operational efficiency. This segment shows 67% preference for rack solutions with integrated power and cooling management capabilities.

Edge Computing Requirements:

Distributed computing deployments are creating new demand patterns for compact, intelligent rack solutions. Edge data centers require rack systems optimized for remote management, minimal maintenance requirements, and operation in diverse environmental conditions. Telecommunications operators are major drivers of this segment as they deploy 5G infrastructure and edge computing capabilities throughout Hong Kong’s urban areas.

Cloud Provider Preferences:

Hyperscale cloud operators establishing Hong Kong presence prioritize standardized rack configurations that align with their global infrastructure strategies. These customers typically require high-volume deployments of standardized rack units with emphasis on operational efficiency, automated management capabilities, and total cost of ownership optimization.

Data Center Operators benefit from advanced rack solutions through improved operational efficiency, enhanced equipment protection, and simplified management processes. Intelligent rack systems provide real-time monitoring capabilities, automated environmental controls, and predictive maintenance features that reduce operational costs and minimize downtime risks. Standardized rack configurations enable operators to achieve economies of scale in procurement, maintenance, and staff training.

Enterprise Customers gain significant advantages from modern rack solutions including improved IT infrastructure reliability, enhanced security features, and better space utilization. Modular rack designs provide flexibility to adapt to changing technology requirements without major infrastructure modifications. Integrated power and cooling management helps organizations optimize energy consumption and reduce operational expenses.

System Integrators benefit from comprehensive rack ecosystems that simplify installation processes, reduce project complexity, and improve customer satisfaction. Standardized mounting systems and cable management solutions accelerate deployment schedules and reduce labor costs. Vendor partnerships with rack manufacturers provide access to technical support, training programs, and preferential pricing arrangements.

Technology Vendors gain market access through partnerships with established rack manufacturers and benefit from standardized mounting solutions that simplify equipment design and certification processes. Rack compatibility standards enable vendors to focus on core technology development while ensuring their products integrate seamlessly with industry-standard infrastructure.

Government Stakeholders benefit from robust data center infrastructure supporting digital government initiatives, economic development, and Hong Kong’s position as a regional technology hub. Reliable rack systems contribute to overall infrastructure resilience and support the territory’s strategic objectives for digital transformation and smart city development.

Strengths:

Weaknesses:

Opportunities:

Threats:

Intelligent Infrastructure Adoption represents a major trend as data center operators seek rack solutions with integrated monitoring, automated management, and predictive maintenance capabilities. IoT-enabled rack systems provide real-time visibility into environmental conditions, power consumption, and equipment status, enabling proactive management and optimization of data center operations.

Sustainability Integration is becoming increasingly important as organizations prioritize environmental responsibility and operational efficiency. Energy-efficient rack designs incorporating advanced cooling technologies, recyclable materials, and circular economy principles are gaining traction among environmentally conscious operators. Carbon footprint reduction initiatives are influencing procurement decisions and vendor selection processes.

Modular and Scalable Solutions are gaining popularity as organizations seek flexibility to adapt to changing technology requirements and business needs. Modular rack systems enable rapid deployment, easy reconfiguration, and cost-effective scaling as data center requirements evolve. This trend particularly benefits colocation operators and enterprises with dynamic infrastructure needs.

Edge Computing Optimization is driving development of specialized rack solutions designed for distributed computing environments. Compact, intelligent rack systems optimized for remote management and minimal maintenance requirements are essential for edge data center deployments throughout Hong Kong’s urban environment.

Security Enhancement continues as a critical trend with increasing emphasis on physical security features, access controls, and monitoring capabilities. Advanced security systems integrated into rack solutions provide multiple layers of protection for sensitive equipment and data, addressing growing cybersecurity and compliance requirements.

High-Density Computing Support reflects the growing deployment of AI, machine learning, and high-performance computing applications requiring specialized rack configurations. GPU-optimized rack systems with enhanced cooling and power distribution capabilities are becoming essential for organizations implementing advanced computing workloads.

Major Infrastructure Investments by international cloud service providers have significantly impacted Hong Kong’s data center rack market. Hyperscale operators establishing regional presence have driven large-scale rack deployments and influenced market standards for performance, reliability, and operational efficiency.

Government Digital Infrastructure Initiatives have created new opportunities for rack suppliers as public sector organizations modernize their IT infrastructure. Smart city projects and digital government services require robust data center capabilities, driving demand for secure, reliable rack solutions meeting government specifications and compliance requirements.

Submarine Cable Landing Expansions have reinforced Hong Kong’s position as a regional connectivity hub, creating demand for specialized rack solutions supporting international telecommunications infrastructure. New cable systems connecting Hong Kong to global networks require advanced rack configurations optimized for carrier equipment and high-capacity networking gear.

5G Network Deployment by telecommunications operators has created new infrastructure requirements throughout Hong Kong. Distributed antenna systems and edge computing capabilities necessary for 5G services require specialized rack solutions designed for telecommunications applications and small cell deployments.

Financial Services Technology Upgrades continue driving demand for high-performance rack solutions as banks and financial institutions modernize their trading systems, risk management platforms, and customer service infrastructure. Regulatory compliance requirements and competitive pressures maintain strong demand for premium rack solutions in this sector.

Cross-Border Business Expansion related to Greater Bay Area integration has created new infrastructure requirements for organizations operating across Hong Kong and mainland China. Standardized rack solutions that can support consistent IT infrastructure across multiple jurisdictions are increasingly important for multinational operations.

Strategic Focus Areas for market participants should prioritize sustainability, intelligence, and flexibility as key differentiators in Hong Kong’s competitive rack market. MarkWide Research analysis indicates that vendors emphasizing environmental efficiency and smart management capabilities are best positioned for long-term success in this demanding market environment.

Product Development Priorities should address Hong Kong’s specific challenges including space constraints, high power costs, and challenging climate conditions. Compact, high-density solutions with integrated cooling and power management capabilities will likely achieve strong market acceptance among cost-conscious operators seeking maximum efficiency.

Market Entry Strategies for new vendors should emphasize local partnerships, comprehensive support services, and demonstrated reliability in mission-critical applications. Established relationships with major data center operators and system integrators are essential for success in Hong Kong’s relationship-driven business environment.

Customer Engagement Approaches should focus on total cost of ownership value propositions rather than initial purchase price considerations. Long-term partnerships providing ongoing support, maintenance services, and technology upgrades are increasingly valued by sophisticated customers seeking operational excellence.

Technology Investment Areas should prioritize intelligent monitoring systems, automated management capabilities, and integration with broader data center infrastructure management platforms. API-enabled rack systems that integrate seamlessly with existing management tools will likely gain competitive advantages in enterprise and colocation markets.

Regional Expansion Considerations should leverage Hong Kong as a gateway to broader Asia-Pacific markets while recognizing the territory’s unique requirements and customer preferences. Cross-border business opportunities related to Greater Bay Area integration may provide additional growth avenues for established Hong Kong market participants.

Long-term growth prospects for Hong Kong’s data center rack market remain positive despite near-term challenges related to space constraints and high operational costs. Digital transformation trends across Asia-Pacific markets continue supporting demand for advanced data center infrastructure, with Hong Kong maintaining its strategic importance as a regional hub for international operations.

Technology evolution will likely drive continued market transformation as rack systems become increasingly intelligent, automated, and integrated with broader infrastructure management platforms. Artificial intelligence applications in data center operations will create new requirements for smart rack solutions capable of supporting autonomous management and optimization capabilities.

Market consolidation trends may accelerate as larger vendors acquire specialized companies to expand their solution portfolios and strengthen their competitive positions. Comprehensive solution providers offering integrated rack, power, cooling, and management systems are likely to gain market share at the expense of single-product vendors.

Sustainability requirements will become increasingly important as organizations face growing pressure to reduce environmental impact and achieve carbon neutrality objectives. Circular economy principles including equipment reuse, recycling, and sustainable manufacturing processes will likely influence purchasing decisions and vendor selection criteria.

Edge computing expansion will create new market segments requiring specialized rack solutions optimized for distributed deployments. 5G network evolution and IoT application growth will drive demand for edge data centers throughout Hong Kong, creating opportunities for vendors with appropriate product portfolios and support capabilities.

Cross-border integration with mainland China through Greater Bay Area initiatives may create new opportunities for standardized infrastructure solutions supporting multinational operations. Regulatory harmonization and improved connectivity could expand the addressable market for Hong Kong-based data center operations and associated rack deployments.

Hong Kong’s data center rack market represents a dynamic and strategically important segment of the territory’s digital infrastructure ecosystem. The market benefits from Hong Kong’s unique position as Asia’s financial center and regional connectivity hub, creating sustained demand for high-performance rack solutions supporting mission-critical applications across multiple industry sectors.

Market fundamentals remain strong despite challenges related to space constraints and high operational costs. The territory’s advanced telecommunications infrastructure, political stability, and strategic location continue attracting international data center investments, driving consistent demand for premium rack solutions that deliver superior performance and reliability.

Future growth opportunities are substantial, driven by digital transformation initiatives, edge computing expansion, 5G network deployment, and Greater Bay Area integration. Organizations increasingly recognize the critical importance of robust data center infrastructure in supporting their digital strategies, creating favorable conditions for continued Hong Kong data center rack market expansion and evolution.

What is Data Center Rack?

Data Center Rack refers to a standardized frame or enclosure that houses servers, networking equipment, and other hardware in a data center environment. These racks are designed to optimize space, cooling, and accessibility for IT infrastructure.

What are the key players in the Hong Kong Data Center Rack Market?

Key players in the Hong Kong Data Center Rack Market include companies like Schneider Electric, Vertiv, and Huawei, which provide a range of solutions for data center infrastructure and management, among others.

What are the growth factors driving the Hong Kong Data Center Rack Market?

The growth of the Hong Kong Data Center Rack Market is driven by the increasing demand for cloud computing, the rise of big data analytics, and the need for efficient data storage solutions across various industries.

What challenges does the Hong Kong Data Center Rack Market face?

Challenges in the Hong Kong Data Center Rack Market include high energy consumption, the need for advanced cooling solutions, and the rapid pace of technological change that requires constant upgrades to infrastructure.

What future opportunities exist in the Hong Kong Data Center Rack Market?

Future opportunities in the Hong Kong Data Center Rack Market include the adoption of modular data center designs, advancements in energy-efficient technologies, and the growing trend of edge computing, which requires localized data processing.

What trends are shaping the Hong Kong Data Center Rack Market?

Trends shaping the Hong Kong Data Center Rack Market include the increasing integration of IoT devices, the shift towards hyper-converged infrastructure, and the emphasis on sustainability and energy efficiency in data center operations.

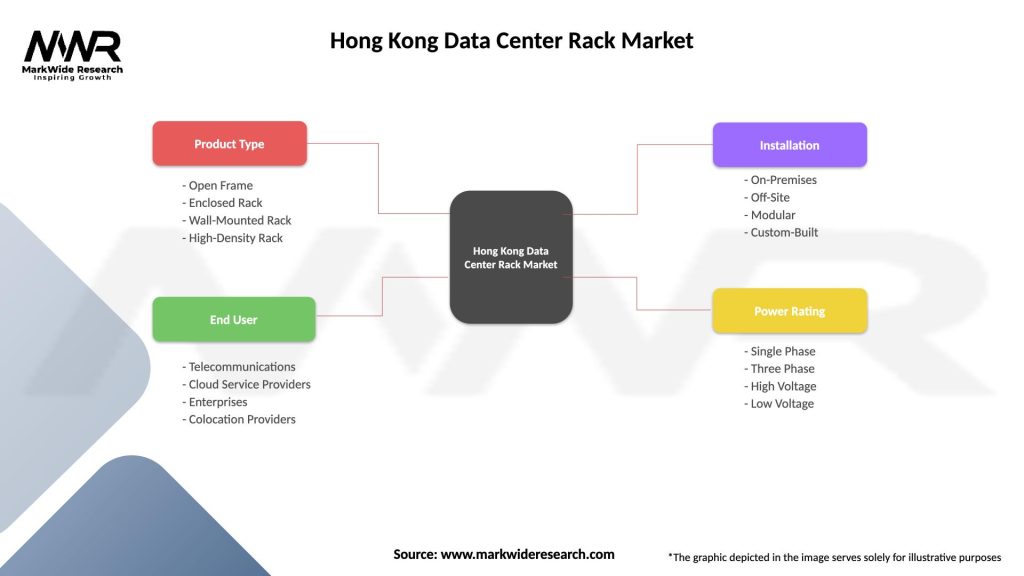

Hong Kong Data Center Rack Market

| Segmentation Details | Description |

|---|---|

| Product Type | Open Frame, Enclosed Rack, Wall-Mounted Rack, High-Density Rack |

| End User | Telecommunications, Cloud Service Providers, Enterprises, Colocation Providers |

| Installation | On-Premises, Off-Site, Modular, Custom-Built |

| Power Rating | Single Phase, Three Phase, High Voltage, Low Voltage |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Hong Kong Data Center Rack Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.