The High Sulfur Fuel Oil (HSFO) market is undergoing significant changes driven by regulatory mandates, technological advancements, and shifting dynamics in the global energy landscape. HSFO, also known as bunker fuel, is a heavy, residual fuel oil with high sulfur content, primarily used in marine vessels and industrial applications. The market for HSFO is influenced by factors such as international shipping regulations, energy demand, crude oil prices, and environmental concerns related to air pollution and greenhouse gas emissions.

Meaning

High Sulfur Fuel Oil (HSFO) refers to a type of residual fuel oil derived from crude oil refining processes, characterized by its high sulfur content typically exceeding 3.5%. HSFO is primarily used as bunker fuel for marine vessels, providing energy for propulsion and onboard operations. However, HSFO is facing increasing scrutiny and regulation due to its environmental impact, particularly its contribution to sulfur dioxide (SO2) emissions and air pollution.

Executive Summary

The High Sulfur Fuel Oil (HSFO) market is undergoing a transition phase due to regulatory changes such as the International Maritime Organization’s (IMO) sulfur cap regulations, which mandate a significant reduction in sulfur content in marine fuels. This has led to a shift towards low sulfur alternatives such as marine gasoil (MGO), marine diesel oil (MDO), and compliant fuels like Very Low Sulfur Fuel Oil (VLSFO) and Marine Gasoline Oil (MGO). Despite these challenges, HSFO continues to play a significant role in certain regions and industries, particularly in regions with limited access to low sulfur alternatives.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

The HSFO market is experiencing a decline in demand and market share due to regulatory pressures, environmental concerns, and the emergence of alternative fuels with lower sulfur content.

Implementation of IMO sulfur regulations has led to increased demand for low sulfur alternatives such as VLSFO, MGO, and MDO, resulting in a surplus of HSFO and price differentials between high and low sulfur fuels.

Market players are exploring strategies to manage the transition to low sulfur fuels, including fuel blending, scrubber installations, fuel switching, and investment in alternative energy sources such as liquefied natural gas (LNG) and hydrogen.

Market Drivers

Several factors are driving the dynamics of the HSFO market:

Regulatory mandates: IMO regulations, such as the global sulfur cap of 0.50% implemented in January 2020, are driving the transition towards cleaner, low sulfur marine fuels and reducing demand for HSFO.

Environmental concerns: HSFO combustion releases sulfur dioxide (SO2) emissions, particulate matter (PM), and other pollutants, contributing to air pollution, acid rain, and adverse health effects, driving regulatory measures to mitigate emissions.

Energy demand: Despite the decline in demand for HSFO in maritime transport, HSFO continues to be used in industrial applications such as power generation, heating, and asphalt production, particularly in regions with limited access to cleaner alternatives.

Market Restraints

The HSFO market faces several challenges:

Regulatory compliance costs: Meeting IMO sulfur regulations requires investments in fuel treatment technologies such as scrubbers, fuel switching, or purchasing low sulfur fuels, leading to increased operational costs for vessel owners and operators.

Market volatility: Fluctuations in crude oil prices, supply-demand dynamics, geopolitical tensions, and regulatory uncertainties contribute to market volatility and price fluctuations for HSFO and alternative fuels.

Technological limitations: Retrofitting vessels with exhaust gas cleaning systems (scrubbers) or switching to alternative fuels may require significant investments, infrastructure upgrades, and operational changes, posing challenges for vessel owners and operators.

Market Opportunities

Despite the challenges, the HSFO market presents opportunities for adaptation and innovation:

Fuel blending: Blending HSFO with low sulfur fuels or additives can help meet sulfur regulations while optimizing fuel properties, performance, and cost-effectiveness.

Scrubber installations: Investing in exhaust gas cleaning systems (scrubbers) enables vessels to continue using HSFO while complying with sulfur regulations, offering potential cost savings and operational flexibility.

Fuel switching: Transitioning to alternative fuels such as LNG, biofuels, hydrogen, or ammonia offers long-term sustainability benefits and regulatory compliance while reducing emissions and environmental impact.

Market diversification: Exploring new markets, applications, and industries for HSFO, such as power generation, heating, and industrial processes, can help mitigate the impact of declining demand in maritime transport.

Market Dynamics

The HSFO market is influenced by dynamic trends and factors:

Regulatory landscape: IMO sulfur regulations, regional emissions standards, and climate policies drive market dynamics, influencing fuel choice, compliance strategies, and investment decisions for vessel owners and operators.

Technological advancements: Innovations in fuel treatment technologies, alternative fuels, and propulsion systems enable vessel operators to meet regulatory requirements, improve fuel efficiency, and reduce emissions while maintaining operational performance.

Economic factors: Crude oil prices, refining margins, supply-demand dynamics, and geopolitical developments impact the cost competitiveness and availability of HSFO and alternative fuels, shaping market trends and investment decisions.

Regional Analysis

The HSFO market varies by region, influenced by factors such as regulatory frameworks, energy demand, economic development, and infrastructure:

Asia Pacific: The Asia Pacific region is a major consumer of HSFO, driven by the maritime transport industry, industrial activities, and power generation in countries such as China, Japan, South Korea, and Singapore.

Europe: Europe has implemented stringent sulfur regulations, driving the transition towards low sulfur marine fuels and reducing demand for HSFO in maritime transport, while HSFO continues to be used in industrial applications and heating.

North America: North America has implemented sulfur regulations in emission control areas (ECAs), leading to the adoption of low sulfur marine fuels and alternative compliance options such as scrubbers, LNG, and shore power, reducing demand for HSFO.

Middle East and Africa: The Middle East and Africa region is a major producer and exporter of HSFO, serving domestic and international markets for maritime transport, power generation, and industrial applications.

Competitive Landscape

Leading Companies in the High Sulfur Fuel Oil (HSFO) Market:

Exxon Mobil Corporation

BP plc

Royal Dutch Shell plc

TotalEnergies SE

Chevron Corporation

Saudi Arabian Oil Company (Saudi Aramco)

PetroChina Company Limited

LUKOIL

Sinopec Corp.

Valero Energy Corporation

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Segmentation

The HSFO market can be segmented based on various factors, including:

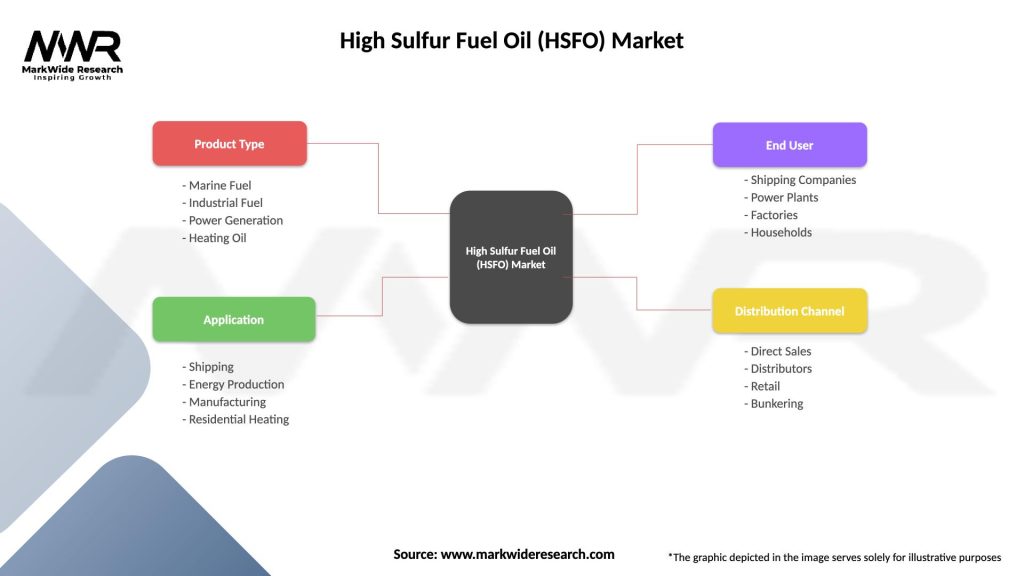

Application: Maritime transport, power generation, industrial heating, asphalt production, others

Region: Asia Pacific, Europe, North America, Middle East and Africa, Latin America

Category-wise Insights

Maritime transport: HSFO is primarily used as bunker fuel for maritime vessels, providing energy for propulsion and onboard operations, with demand declining due to regulatory mandates and the adoption of low sulfur alternatives.

Power generation: HSFO is used in power plants and industrial facilities for electricity generation, heating, and steam production, particularly in regions with limited access to natural gas or renewable energy sources.

Industrial heating: HSFO is used in industrial boilers, furnaces, and heating systems for manufacturing processes, space heating, and hot water production, providing a cost-effective and reliable energy source.

Asphalt production: HSFO is used as a binder in asphalt production for road construction and paving applications, providing viscosity and durability to asphalt mixtures.

Key Benefits for Industry Participants and Stakeholders

Cost-effectiveness: HSFO offers a cost-effective energy source for maritime transport, power generation, and industrial applications, particularly in regions with limited access to low sulfur alternatives.

Operational reliability: HSFO provides a reliable and consistent source of energy for vessels, power plants, and industrial processes, maintaining operational performance and uptime.

Market flexibility: HSFO market dynamics offer opportunities for fuel blending, scrubber installations, and alternative compliance options, enabling flexibility and adaptability for vessel owners and operators.

Supply chain resilience: HSFO supply chains are well-established and globally distributed, providing access to fuel sources, storage facilities, and bunkering services in major maritime hubs and ports worldwide.

SWOT Analysis

Strengths: Cost-effectiveness, energy density, global availability, well-established supply chains

Transition towards low sulfur alternatives: Increasing adoption of VLSFO, MGO, and MDO as compliant fuels for maritime transport, reducing demand for HSFO and driving market shifts and price differentials.

Scrubber installations: Growing demand for exhaust gas cleaning systems (scrubbers) enables vessels to continue using HSFO while complying with sulfur regulations, offering potential cost savings and operational flexibility.

Fuel switching: Shift towards alternative fuels such as LNG, biofuels, hydrogen, or ammonia offers long-term sustainability benefits and emissions reductions, particularly for vessels operating in emission control areas (ECAs) and environmentally sensitive regions.

Market consolidation: Consolidation among refiners, suppliers, and bunker providers, along with strategic alliances and partnerships, reshapes the competitive landscape and supply chain dynamics in the HSFO market.

Covid-19 Impact

The Covid-19 pandemic has had mixed effects on the HSFO market:

Demand contraction: Reduced global trade, travel restrictions, and economic slowdowns during the pandemic led to a decline in maritime transport activity, impacting demand for bunker fuels including HSFO.

Supply chain disruptions: Disruptions in crude oil production, refining operations, and logistics during the pandemic affected HSFO supply chains, leading to price volatility, inventory buildups, and storage constraints.

Regulatory delays: Implementation of IMO sulfur regulations and compliance deadlines faced challenges and delays due to the pandemic, impacting market dynamics and investment decisions for vessel owners and operators.

Key Industry Developments

Scrubber installations: Increased demand for scrubber installations as a compliance option for vessel owners and operators seeking to continue using HSFO while meeting sulfur regulations, driving investments in scrubber technology and installation capacity.

Fuel blending: Adoption of fuel blending techniques and additives to reduce sulfur content in HSFO and meet regulatory requirements while optimizing fuel properties, performance, and cost-effectiveness for vessel operators.

Alternative fuels: Growing interest and investment in alternative fuels such as LNG, biofuels, hydrogen, and ammonia as low sulfur, environmentally friendly alternatives to HSFO for maritime transport, driving innovation and infrastructure development in the energy transition.

Analyst Suggestions

Monitor regulatory developments: Stay informed about IMO sulfur regulations, regional emissions standards, and climate policies impacting the HSFO market, and assess compliance options, costs, and timelines for vessel operations.

Evaluate fuel management strategies: Assess fuel blending, scrubber installations, fuel switching, and alternative fuel options to optimize fuel procurement, consumption, and compliance for vessel fleets and operations.

Diversify market exposure: Explore new markets, applications, and industries for HSFO beyond maritime transport, such as power generation, industrial heating, and asphalt production, to mitigate risks and adapt to changing market dynamics.

Invest in technology and innovation: Explore technologies, solutions, and partnerships to enhance fuel efficiency, emissions reductions, and sustainability in HSFO applications, and position for long-term competitiveness and growth in the energy transition.

Future Outlook

The future outlook for the HSFO market is characterized by continued changes and challenges:

Regulatory compliance: Compliance with IMO sulfur regulations, regional emissions standards, and climate policies will drive market dynamics, fuel choices, and investment decisions for vessel owners and operators, shaping the transition towards cleaner, low sulfur fuels and alternative energy sources.

Technological advancements: Innovations in fuel treatment technologies, alternative fuels, and propulsion systems will continue to drive market evolution, offering opportunities for emissions reductions, cost savings, and operational efficiency improvements in HSFO applications.

Market adaptation: Vessel owners, operators, refiners, suppliers, and end-users will adapt to changing market conditions, regulatory requirements, and technological innovations, reshaping supply chains, fuel procurement strategies, and investment priorities in the HSFO market.

Conclusion

In conclusion, the High Sulfur Fuel Oil (HSFO) market is undergoing a period of transformation driven by regulatory mandates, technological advancements, and market dynamics in the global energy landscape. While HSFO continues to play a significant role in maritime transport, power generation, and industrial applications, it faces increasing scrutiny and competition from low sulfur alternatives and alternative energy sources. Vessel owners, operators, refiners, suppliers, and end-users will need to navigate regulatory compliance, market volatility, and technological changes to optimize fuel choices, reduce emissions, and ensure competitiveness and sustainability in the evolving HSFO market.

What is High Sulfur Fuel Oil (HSFO)?

High Sulfur Fuel Oil (HSFO) is a type of fuel oil that contains a higher percentage of sulfur compared to other fuel oils. It is primarily used in marine applications, power generation, and industrial processes due to its cost-effectiveness and availability.

What are the key companies in the High Sulfur Fuel Oil (HSFO) Market?

Key companies in the High Sulfur Fuel Oil (HSFO) Market include ExxonMobil, Chevron, and TotalEnergies, among others. These companies are involved in the production, distribution, and marketing of HSFO for various applications.

What are the drivers of growth in the High Sulfur Fuel Oil (HSFO) Market?

The growth of the High Sulfur Fuel Oil (HSFO) Market is driven by the increasing demand for energy in developing economies, the expansion of the shipping industry, and the need for cost-effective fuel solutions in industrial applications.

What challenges does the High Sulfur Fuel Oil (HSFO) Market face?

The High Sulfur Fuel Oil (HSFO) Market faces challenges such as stringent environmental regulations aimed at reducing sulfur emissions, competition from low-sulfur fuel alternatives, and fluctuations in crude oil prices affecting production costs.

What opportunities exist in the High Sulfur Fuel Oil (HSFO) Market?

Opportunities in the High Sulfur Fuel Oil (HSFO) Market include the potential for technological advancements in refining processes, the growth of emerging markets, and the increasing use of HSFO in power generation as countries seek to diversify their energy sources.

What trends are shaping the High Sulfur Fuel Oil (HSFO) Market?

Trends in the High Sulfur Fuel Oil (HSFO) Market include a shift towards more sustainable fuel options, the implementation of stricter emissions regulations, and innovations in fuel blending techniques to meet compliance standards.

Leading Companies in the High Sulfur Fuel Oil (HSFO) Market:

Exxon Mobil Corporation

BP plc

Royal Dutch Shell plc

TotalEnergies SE

Chevron Corporation

Saudi Arabian Oil Company (Saudi Aramco)

PetroChina Company Limited

LUKOIL

Sinopec Corp.

Valero Energy Corporation

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

Market")