The healthcare revenue cycle management (RCM) market is a crucial component of the healthcare industry, encompassing the financial processes and systems involved in managing the revenue generation and cash flow of healthcare organizations. It involves the entire cycle, starting from patient registration and insurance verification to claims processing, billing, and collection. The market for healthcare RCM solutions and services has been witnessing significant growth due to the increasing complexity of healthcare reimbursement systems, the shift from fee-for-service to value-based payment models, and the need for healthcare providers to optimize their revenue streams and improve financial performance.

Meaning

Healthcare revenue cycle management refers to the strategies, technologies, and processes employed by healthcare organizations to effectively manage the financial aspects of patient care, including patient registration, insurance eligibility verification, claims submission and processing, denial management, payment posting, and patient billing and collections. It encompasses a range of activities aimed at streamlining revenue generation, reducing costs, improving cash flow, and ensuring compliance with regulatory requirements.

Executive Summary

The healthcare revenue cycle management market has been experiencing significant growth in recent years, driven by factors such as the increasing focus on cost containment, the rising adoption of electronic health records (EHRs) and health information exchange (HIE) systems, and the need for healthcare providers to optimize their revenue streams. The market is characterized by the presence of numerous players offering a wide range of solutions and services to cater to the diverse needs of healthcare organizations. The demand for healthcare RCM solutions is expected to further increase as healthcare providers seek to improve their financial performance, enhance patient satisfaction, and navigate the complexities of reimbursement systems.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Growing Complexity of Reimbursement Systems: The healthcare reimbursement landscape is becoming increasingly complex, with the shift towards value-based payment models, the introduction of alternative payment models, and the implementation of quality-based reimbursement programs. This complexity necessitates the use of advanced RCM solutions and services to ensure accurate claims processing, maximize revenue capture, and comply with regulatory requirements.

Increasing Adoption of Technology: Healthcare organizations are adopting advanced technologies, such as cloud-based RCM solutions, predictive analytics, artificial intelligence (AI), and robotic process automation (RPA), to streamline their revenue cycle processes, improve operational efficiency, and reduce manual errors. These technologies enable real-time data analytics, automated claims processing, and proactive denial management.

Emphasis on Patient Engagement and Experience: Patient engagement is gaining prominence in healthcare RCM, with a focus on providing transparent billing information, personalized financial counseling, and convenient payment options. Healthcare organizations are leveraging patient portals, mobile applications, and online payment platforms to enhance the patient experience and improve collections.

Regulatory Compliance and Risk Mitigation: Compliance with healthcare regulations, such as the Health Insurance Portability and Accountability Act (HIPAA) and the Affordable Care Act (ACA), is crucial in healthcare RCM. Organizations are investing in solutions that ensure data security, privacy, and compliance, while also mitigating the risks associated with billing and coding errors, fraud, and revenue leakage.

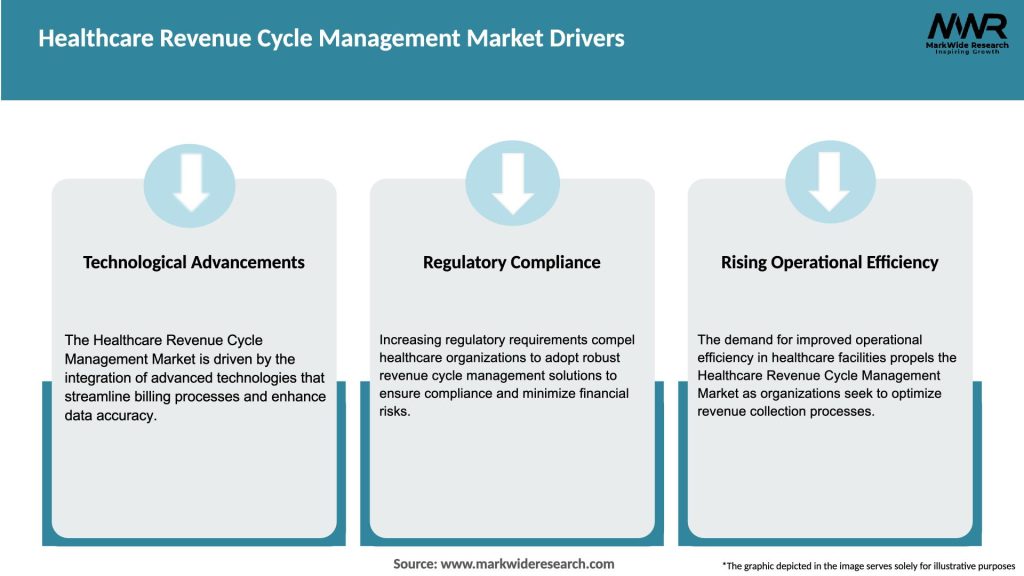

Market Drivers

Increasing Healthcare Expenditure: The continuous rise in healthcare expenditure, driven by factors such as population growth, aging demographics, and the prevalence of chronic diseases, is fueling the demand for efficient revenue cycle management solutions. Healthcare organizations are seeking to optimize their revenue streams and reduce administrative costs to sustain financial viability.

Transition to Value-based Care: The shift from fee-for-service reimbursement models to value-based care models is driving the need for sophisticated RCM solutions that can accurately capture and report quality and outcome measures. Providers are incentivized to focus on patient outcomes and deliver cost-effective care, necessitating robust RCM systems that can support value-based reimbursement models.

Increasing Adoption of Electronic Health Records (EHRs): The widespread adoption of EHRs has facilitated the digitization of patient health information, making it easier to capture, share, and analyze data throughout the revenue cycle. Integration between EHR systems and RCM solutions streamlines processes, reduces documentation errors, and improves coding accuracy.

Regulatory Changes and Compliance Requirements: The evolving regulatory landscape, including changes in reimbursement policies, coding guidelines, and billing regulations, creates a need for healthcare organizations to stay abreast of these changes and ensure compliance. RCM solutions that can adapt to regulatory updates and provide accurate coding and billing capabilities are in high demand.

Market Restraints

Cost and Return on Investment (ROI) Concerns: The implementation and maintenance costs associated with healthcare RCM solutions can be a significant barrier for healthcare organizations, especially small and medium-sized providers. Achieving a positive ROI and demonstrating the value of RCM investments can be challenging, particularly in the early stages of implementation.

Interoperability and Integration Challenges: The integration of RCM systems with existing EHRs, practice management systems, and other healthcare IT infrastructure can pose technical challenges. Lack of interoperability between different systems and data silos can hinder seamless information exchange and impact the efficiency of revenue cycle processes.

Resistance to Change and Workflow Disruption: Implementing new RCM solutions often requires changes in workflows and staff training, which can be met with resistance from healthcare providers and staff. Resistance to change and disruption to established processes can slow down adoption and impact the effectiveness of RCM initiatives.

Complexity of Healthcare Reimbursement: The complexity of healthcare reimbursement systems, including multiple payers, varying payment models, and intricate billing and coding requirements, poses challenges for accurate claims processing and revenue optimization. Healthcare organizations require sophisticated RCM solutions that can navigate this complexity and ensure compliance.

Market Opportunities

Adoption of Artificial Intelligence (AI) and Machine Learning (ML): The integration of AI and ML technologies into RCM solutions offers opportunities for automation, predictive analytics, and fraud detection. AI-powered solutions can enhance coding accuracy, identify potential billing errors, and improve revenue cycle performance.

Expansion in Emerging Markets: The healthcare RCM market offers significant growth potential in emerging markets, driven by factors such as increasing healthcare infrastructure development, rising healthcare spending, and a growing focus on healthcare quality and patient outcomes. Healthcare organizations in these regions are seeking efficient RCM solutions to address their revenue cycle challenges.

Focus on Patient Financial Responsibility: With the rise in high-deductible health plans and increased patient financial responsibility, there is a need for RCM solutions that enable transparent billing, cost estimation, and flexible payment options. Solutions that prioritize patient engagement and financial counseling can help providers improve collections and patient satisfaction.

Integration of Telehealth and Remote Patient Monitoring: The rapid adoption of telehealth and remote patient monitoring technologies presents opportunities for RCM vendors to develop solutions that streamline billing and reimbursement processes for virtual care services. Integration of RCM systems with telehealth platforms can simplify claims submission, eligibility verification, and reimbursement for remote services.

Market Dynamics

The healthcare revenue cycle management market is dynamic and influenced by various factors, including technological advancements, regulatory changes, market consolidation, and evolving patient expectations. Key dynamics shaping the market include:

Technological Advancements: Continuous advancements in healthcare IT, such as cloud computing, AI, robotic process automation, and blockchain, are transforming revenue cycle management processes. Innovative solutions that leverage these technologies provide enhanced automation, real-time data analytics, and improved efficiency.

Emphasis on Data Analytics and Predictive Insights: The ability to leverage data analytics and predictive insights is becoming crucial in revenue cycle management. RCM solutions that can analyze large volumes of data, identify patterns, predict payment behaviors, and proactively address revenue leakage are gaining traction in the market.

Mergers and Acquisitions: The healthcare RCM market has witnessed significant consolidation, with large healthcare IT companies acquiring smaller RCM solution providers to expand their product portfolios and gain a competitive edge. These mergers and acquisitions contribute to the market’s competitive landscape and drive innovation.

Partnership and Collaboration: Collaboration between healthcare providers, payers, and RCM vendors is increasing to improve interoperability, streamline processes, and enhance revenue cycle performance. Partnerships between stakeholders aim to create integrated solutions that optimize the end-to-end revenue cycle and promote financial sustainability.

Regional Analysis

The healthcare revenue cycle management market exhibits regional variations influenced by factors such as healthcare infrastructure, government regulations, reimbursement systems, and technological advancements. Key regional insights include:

North America: North America dominates the healthcare RCM market, driven by advanced healthcare systems, a well-established reimbursement framework, and a high adoption of healthcare IT solutions. The presence of major RCM vendors and a focus on cost containment further contribute to market growth in the region.

Europe: Europe represents a significant market for healthcare RCM, characterized by the presence of universal healthcare systems and government initiatives to promote interoperability and digital health. The region’s emphasis on value-based care and the adoption of advanced technologies support the growth of the RCM market.

Asia Pacific: The Asia Pacific region presents substantial growth opportunities due to the expansion of healthcare infrastructure, increasing healthcare spending, and the adoption of healthcare IT solutions. The region’s diverse market landscape, varying reimbursement systems, and the need for efficient revenue management create demand for RCM solutions.

Latin America and the Middle East & Africa: These regions are witnessing rapid advancements in healthcare infrastructure and the adoption of digital health technologies. The growing focus on improving healthcare quality, expanding insurance coverage, and enhancing operational efficiency in revenue management drive the adoption of RCM solutions.

Competitive Landscape

Leading Companies in Healthcare Revenue Cycle Management Market

Cerner Corporation

Epic Systems Corporation

McKesson Corporation

Change Healthcare

Allscripts Healthcare Solutions, Inc.

GE Healthcare

Athenahealth (Veritas Capital)

Quest Diagnostics Incorporated

nThrive Inc.

R1 RCM Inc.

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

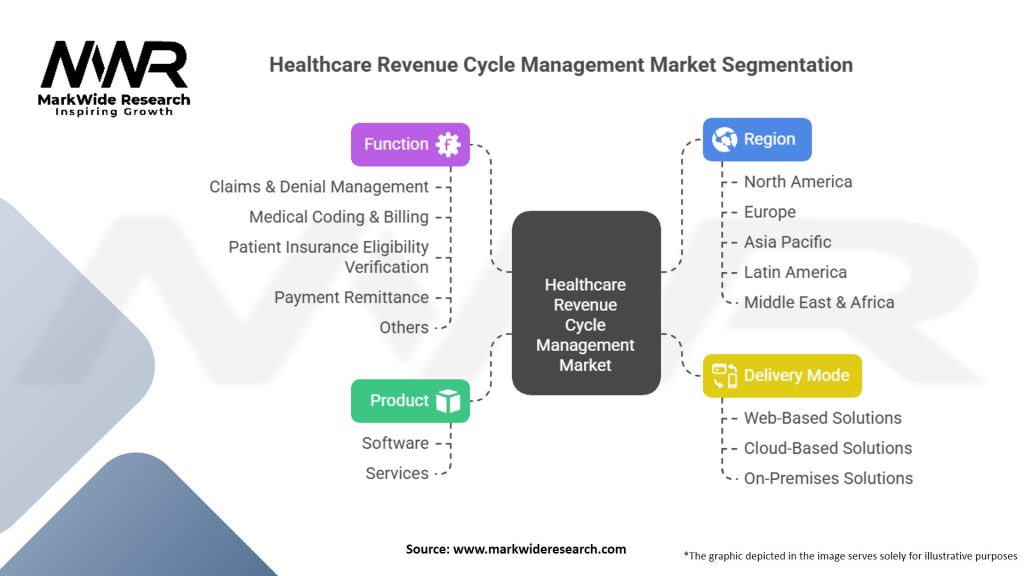

Segmentation

The healthcare RCM market can be segmented based on various factors, including component, deployment mode, end-user, and geography.

Key Benefits for Industry Participants and Stakeholders

Healthcare Providers:

Streamlined revenue cycle processes and reduced administrative burden

Improved financial performance and cash flow management

Enhanced operational efficiency and cost containment

Compliance with regulatory requirements and reduced compliance risks

Payers and Insurers:

Efficient claims processing and reduced payment delays

Accurate eligibility verification and reduced billing errors

Improved fraud detection and prevention

Enhanced provider network management and contract negotiations

Patients:

Transparent billing information and cost estimation

Convenient payment options and financial counseling

Improved patient experience and satisfaction

Reduced confusion and disputes related to healthcare billing

RCM Solution Providers:

Business growth opportunities and market expansion

Increased demand for innovative solutions and services

Long-term partnerships with healthcare organizations

Competitive advantage through technology advancements

SWOT Analysis

Strengths:

Advanced technology adoption and innovation capabilities

Established market presence and strong customer base

Extensive industry expertise and domain knowledge

Comprehensive solutions portfolio and service offerings

Weaknesses:

Cost concerns and return on investment challenges

Complex implementation and integration processes

Resistance to change and workflow disruption

Dependence on external factors, such as regulatory changes

Opportunities:

Integration of AI, ML, and predictive analytics

Expansion in emerging markets with growing healthcare infrastructure

Focus on patient financial responsibility and engagement

Collaboration and partnerships for interoperability and value-based care

Threats:

Intense market competition and pricing pressures

Security and privacy concerns related to patient data

Regulatory and compliance risks in a dynamic healthcare environment

Economic and political uncertainties impacting healthcare spending

Market Key Trends

Adoption of Blockchain Technology: The healthcare RCM market is witnessing the emergence of blockchain-based solutions that offer secure and transparent transactions, improved data interoperability, and reduced fraud and errors. Blockchain has the potential to revolutionize claims management, billing processes, and patient identity verification.

Focus on Price Transparency: Increasing emphasis on price transparency in healthcare is driving the demand for RCM solutions that facilitate accurate cost estimation, enable price comparison, and provide clear billing information to patients. RCM vendors are developing tools and platforms to support price transparency initiatives.

Shift towards Predictive Analytics: Predictive analytics is gaining traction in healthcare RCM, enabling providers to identify trends, predict revenue patterns, and optimize financial performance. Solutions that leverage predictive analytics help organizations proactively address denials, identify revenue leakage, and improve cash flow.

Integration of Telehealth and RCM: The integration of telehealth and RCM solutions is becoming crucial as telehealth services continue to grow in popularity. RCM systems that seamlessly integrate with telehealth platforms ensure accurate claims submission, eligibility verification, and reimbursement for virtual care services.

Covid-19 Impact

The Covid-19 pandemic has had a significant impact on the healthcare revenue cycle management market. Key effects of the pandemic include:

Financial Challenges for Providers: Healthcare organizations faced financial strain due to reduced patient volumes, deferred elective procedures, and increased costs related to Covid-19 response. The pandemic highlighted the need for robust RCM solutions to optimize revenue streams and mitigate financial losses.

Regulatory Changes and Telehealth Expansion: The pandemic prompted regulatory changes, such as relaxed telehealth regulations and expanded coverage for virtual care services. RCM systems had to adapt to new coding and billing requirements for telehealth visits, ensuring accurate claims processing and reimbursement.

Increased Focus on Data Analytics and Automation: The need for real-time data analytics, automated claims processing, and revenue leakage prevention became critical during the pandemic. RCM solutions that leverage AI, ML, and automation capabilities gained prominence as healthcare organizations sought to improve efficiency and reduce manual errors.

Patient Financial Responsibility and Assistance: Covid-19 led to increased financial responsibility for patients, particularly with rising unemployment rates and insurance coverage changes. RCM solutions that prioritize patient financial counseling, payment flexibility, and assistance gained importance in navigating the financial impact of the pandemic.

Key Industry Developments

Partnerships and Collaborations: RCM vendors have engaged in partnerships and collaborations with EHR providers, payers, and other stakeholders to promote interoperability, improve data exchange, and streamline revenue cycle processes. These partnerships aim to create integrated solutions that span the entire healthcare continuum.

Product Innovations: RCM solution providers continue to innovate their offerings by incorporating advanced technologies, such as AI, ML, and automation. New features and functionalities focus on improving coding accuracy, claims processing efficiency, denial management, and revenue optimization.

Enhanced Security and Compliance: With the increasing cybersecurity threats and stringent regulatory requirements, RCM vendors are investing in robust security measures, data encryption, and compliance frameworks. Solutions that prioritize data privacy and protection are gaining preference among healthcare organizations.

Expansion in Emerging Markets: RCM vendors are expanding their presence in emerging markets, such as Asia Pacific and Latin America, to capitalize on the growing healthcare infrastructure, increasing healthcare spending, and the need for efficient revenue management solutions.

Analyst Suggestions

Embrace Automation and AI: Healthcare organizations should consider adopting RCM solutions that leverage automation, AI, and predictive analytics to streamline processes, reduce manual errors, and optimize revenue cycle performance. Automation can help improve operational efficiency, accuracy, and speed in claims processing and denial management.

Focus on Patient Engagement and Financial Counseling: Healthcare providers should prioritize patient engagement and financial counseling to improve patient satisfaction and enhance collections. RCM solutions that enable transparent billing, cost estimation, and convenient payment options can contribute to positive patient experiences.

Stay Abreast of Regulatory Changes: Given the evolving healthcare landscape and changing regulatory requirements, healthcare organizations need to stay informed about reimbursement policies, coding guidelines, and compliance regulations. Regular updates to RCM systems and staff training on these changes are crucial to ensure compliance and avoid penalties.

Evaluate Total Cost of Ownership (TCO): When considering RCM solutions, healthcare organizations should conduct a thorough evaluation of the total cost of ownership, including implementation costs, maintenance fees, and potential ROI. Understanding the financial impact and benefits of RCM investments is essential for effective decision-making.

Future Outlook

The healthcare revenue cycle management market is expected to continue its growth trajectory in the coming years. Key trends and factors that will shape the future of the market include:

Continued Shift to Value-based Care: The transition to value-based care models will drive the demand for RCM solutions that can accurately capture and report quality measures, support alternative payment models, and optimize reimbursement processes.

Increasing Role of Data Analytics and AI: Data analytics, AI, and machine learning will play a crucial role in revenue cycle management, enabling predictive insights, automated processes, and proactive revenue optimization. RCM solutions that leverage these technologies will gain prominence.

Emphasis on Price Transparency and Patient Financial Responsibility: The focus on price transparency and patient financial responsibility will continue to grow, prompting healthcare organizations to invest in RCM solutions that facilitate cost estimation, transparent billing, and patient financial counseling.

Integration of Healthcare IT Systems: Seamless integration between RCM systems, EHRs, and other healthcare IT systems will be crucial to optimize revenue cycle processes, improve interoperability, and enhance data exchange between stakeholders.

Conclusion

The healthcare revenue cycle management market plays a vital role in optimizing revenue generation, improving financial performance, and ensuring compliance in healthcare organizations. The market is driven by factors such as the increasing complexity of reimbursement systems, the transition to value-based care, and the need for operational efficiency. RCM solutions that leverage advanced technologies, prioritize patient engagement, and adapt to regulatory changes will be in high demand. As the healthcare industry continues to evolve, RCM vendors and healthcare organizations must stay proactive, embrace innovation, and collaborate to navigate the dynamic revenue cycle landscape successfully.

What is Healthcare Revenue Cycle Management?

Healthcare Revenue Cycle Management refers to the financial processes that healthcare organizations use to track patient care episodes from registration and appointment scheduling to the final payment of a balance. It encompasses various functions including billing, coding, and claims management.

What are the key players in the Healthcare Revenue Cycle Management Market?

Key players in the Healthcare Revenue Cycle Management Market include companies like Cerner Corporation, McKesson Corporation, and Allscripts Healthcare Solutions, among others. These companies provide software and services that streamline revenue cycle processes for healthcare providers.

What are the main drivers of growth in the Healthcare Revenue Cycle Management Market?

The main drivers of growth in the Healthcare Revenue Cycle Management Market include the increasing complexity of healthcare billing, the rising demand for efficient revenue management solutions, and the need for compliance with regulatory requirements. Additionally, the shift towards value-based care is also contributing to market expansion.

What challenges does the Healthcare Revenue Cycle Management Market face?

The Healthcare Revenue Cycle Management Market faces challenges such as the high costs associated with implementing advanced technologies, the need for skilled personnel, and the complexities of navigating various payer regulations. These factors can hinder the efficiency of revenue cycle processes.

What opportunities exist in the Healthcare Revenue Cycle Management Market?

Opportunities in the Healthcare Revenue Cycle Management Market include the adoption of artificial intelligence and machine learning to enhance billing accuracy and efficiency. Additionally, the growing trend of telehealth services presents new avenues for revenue cycle management as patient interactions evolve.

What trends are shaping the Healthcare Revenue Cycle Management Market?

Trends shaping the Healthcare Revenue Cycle Management Market include the increasing integration of technology solutions, such as cloud-based platforms, and the focus on patient-centered billing practices. Moreover, the emphasis on data analytics for improving financial performance is becoming more prevalent.

Leading Companies in Healthcare Revenue Cycle Management Market

Cerner Corporation

Epic Systems Corporation

McKesson Corporation

Change Healthcare

Allscripts Healthcare Solutions, Inc.

GE Healthcare

Athenahealth (Veritas Capital)

Quest Diagnostics Incorporated

nThrive Inc.

R1 RCM Inc.

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.