The GPS and GNSS (Global Navigation Satellite System) receivers in the aviation market have experienced significant growth in recent years. These receivers play a crucial role in providing accurate and reliable navigation and positioning information for aircraft. With the increasing demand for efficient and safe air travel, the adoption of GPS and GNSS receivers in the aviation industry has become a standard practice.

GPS and GNSS receivers are electronic devices used to receive signals from satellite systems such as the Global Positioning System (GPS) and other navigation satellite systems. These receivers utilize signals from multiple satellites to determine the precise location, velocity, and time information for aircraft. By analyzing the data received from the satellites, these receivers enable pilots and air traffic controllers to navigate accurately and efficiently.

Executive Summary:

The GPS and GNSS receivers in the aviation market have witnessed substantial growth due to the rising demand for precise navigation and positioning capabilities in the aviation industry. These receivers offer improved accuracy, reliability, and availability, ensuring enhanced flight safety and operational efficiency. As a result, aircraft manufacturers, airlines, and aviation authorities are increasingly adopting GPS and GNSS receivers to enhance their navigation systems.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights:

Growing Demand for Enhanced Navigation Systems: The aviation industry is witnessing a growing demand for advanced navigation systems that offer precise positioning, navigation, and timing information. GPS and GNSS receivers fulfill these requirements, leading to their increased adoption in the aviation market.

Technological Advancements in GPS and GNSS Receivers: The continuous advancements in GPS and GNSS receiver technology have resulted in improved accuracy, sensitivity, and signal acquisition capabilities. These advancements have contributed to the enhanced performance of navigation systems in aircraft.

Increasing Focus on Flight Safety: With the growing emphasis on flight safety, there is a heightened need for reliable navigation systems. GPS and GNSS receivers provide accurate positioning information, enabling pilots to make informed decisions during flights, thereby enhancing safety.

Integration of GPS and GNSS with Avionics Systems: The integration of GPS and GNSS receivers with avionics systems has facilitated seamless navigation and improved situational awareness for pilots. This integration has contributed to the overall efficiency and effectiveness of flight operations.

Market Drivers:

Growing Air Traffic and Need for Efficient Navigation: The increasing number of air passengers and the consequent rise in air traffic have created a demand for efficient navigation systems. GPS and GNSS receivers offer accurate and reliable navigation solutions, meeting this demand and driving their market growth.

Regulatory Mandates for Enhanced Navigation Systems: Regulatory bodies in the aviation industry are increasingly mandating the use of advanced navigation systems to improve flight safety. GPS and GNSS receivers comply with these regulations, driving their adoption in the aviation market.

Technological Advancements in Satellite Systems: The continuous advancements in satellite systems, such as the introduction of new satellite constellations and improved signal coverage, have positively impacted the performance of GPS and GNSS receivers. This, in turn, has boosted their demand in the aviation industry.

Cost Reduction and Miniaturization of GPS and GNSS Receivers: The decreasing cost of GPS and GNSS receiver components, along with their miniaturization, has made them more accessible to aircraft manufacturers and operators. This affordability has led to increased adoption in the aviation market.

Market Restraints:

Vulnerability to Signal Interference and Spoofing: GPS and GNSS signals are susceptible to interference and spoofing, which can affect the accuracy and reliability of navigation systems. The vulnerability of these systems to such threats poses a significant challenge to their widespread adoption in the aviation industry.

Limited Signal Availability in Certain Environments: GPS and GNSS signals can be affected by obstructions such as tall buildings or natural terrain, leading to signal degradation or loss. In areas with limited signal availability, the performance of GPS and GNSS receivers may be compromised, posing a restraint to their usage.

Initial Investment and Implementation Costs: The initial investment and implementation costs associated with integrating GPS and GNSS receivers into existing avionics systems can be substantial. This may act as a barrier for some aircraft operators, especially smaller players in the aviation market.

Regulatory Compliance and Certification Requirements: The stringent regulatory compliance and certification requirements for GPS and GNSS receivers in the aviation industry can pose challenges for manufacturers and operators. Meeting these requirements adds complexity and cost to the adoption process.

Market Opportunities:

Adoption of Next-Generation Satellite Systems: The ongoing development and deployment of next-generation satellite systems, such as Galileo, BeiDou, and NavIC, present significant opportunities for the GPS and GNSS receiver market in aviation. These systems offer improved accuracy, signal robustness, and increased availability, attracting potential customers from the aviation sector.

Integration of GPS and GNSS with Other Technologies: The integration of GPS and GNSS receivers with other emerging technologies, such as augmented reality (AR) and artificial intelligence (AI), can open up new possibilities in the aviation market. This integration can enhance situational awareness, navigation assistance, and predictive maintenance capabilities.

Growing Demand for Unmanned Aerial Vehicles (UAVs): The increasing use of unmanned aerial vehicles (UAVs) in various applications, including cargo delivery, surveillance, and inspection, presents a significant growth opportunity for GPS and GNSS receivers. These receivers enable precise navigation and control of UAVs, ensuring their safe and efficient operations.

Development of Advanced Antenna Technologies: The development of advanced antenna technologies, such as multi-constellation and multi-frequency antennas, can further improve the performance of GPS and GNSS receivers. These advancements can enhance signal reception, mitigate interference, and expand the application areas for GPS and GNSS receivers in aviation.

Market Dynamics:

The GPS and GNSS receiver market in aviation is characterized by dynamic factors that shape its growth and development. The market is driven by the increasing demand for enhanced navigation systems, regulatory mandates, technological advancements, and the integration of GPS and GNSS with avionics systems. However, challenges such as signal interference, limited signal availability, initial investment costs, and regulatory compliance requirements act as restraints to market growth. The market presents opportunities through the adoption of next-generation satellite systems, integration with other technologies, the growing demand for UAVs, and the development of advanced antenna technologies.

Regional Analysis:

The adoption of GPS and GNSS receivers in the aviation market varies across different regions. North America holds a significant market share due to the presence of key players and advanced aviation infrastructure. Europe is also a prominent market for GPS and GNSS receivers, driven by the region’s emphasis on flight safety and the integration of satellite systems such as Galileo. The Asia Pacific region is witnessing rapid growth in the aviation sector, leading to increased demand for GPS and GNSS receivers. Other regions, such as Latin America, the Middle East, and Africa, are also witnessing steady adoption of these receivers in their respective aviation markets.

Competitive Landscape:

Leading Companies in the GPS and GNSS Receivers in Aviation Market:

Garmin Ltd.

Honeywell International Inc.

NovAtel Inc. (Hexagon AB)

Trimble Inc.

Topcon Corporation

Rockwell Collins, Inc.

u-blox Holding AG

Advanced Navigation

Hemisphere GNSS

Spectra Precision

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

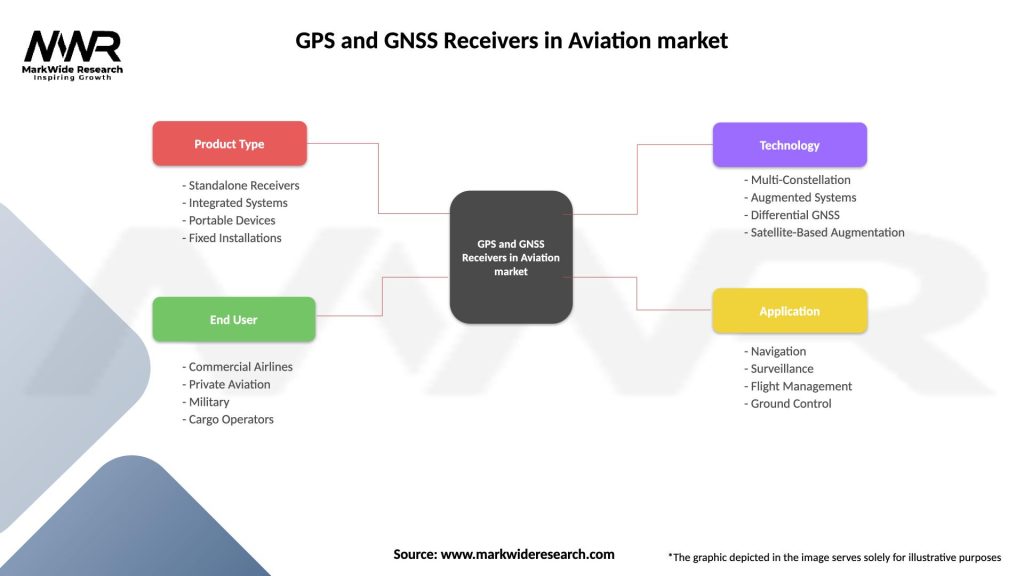

Segmentation:

The GPS and GNSS receiver market in aviation can be segmented based on receiver type, application, and end-user.

Standalone GPS/GNSS receivers are compact and portable devices used primarily by general aviation pilots and recreational aircraft operators.

These receivers offer basic navigation and positioning capabilities, providing essential information for pilots during their flights.

Standalone receivers are cost-effective solutions for smaller aircraft and serve as backup navigation devices in larger aircraft.

Integrated GPS/GNSS Receivers:

Integrated GPS/GNSS receivers are designed to be seamlessly integrated into avionics systems of aircraft.

These receivers provide advanced navigation and positioning capabilities, offering precise information to pilots and flight management systems.

Integrated receivers often support multiple satellite constellations and offer additional features such as advanced signal processing and fault tolerance.

Key Benefits for Industry Participants and Stakeholders:

Enhanced Flight Safety: GPS and GNSS receivers provide accurate and reliable positioning and navigation information, contributing to enhanced flight safety. By ensuring precise guidance and situational awareness, these receivers help pilots make informed decisions during flights.

Improved Operational Efficiency: The adoption of GPS and GNSS receivers in aviation improves operational efficiency by enabling optimized flight routes, reducing fuel consumption, and enhancing overall flight planning and management processes.

Compliance with Regulatory Standards: GPS and GNSS receivers assist aircraft manufacturers and operators in complying with regulatory standards and mandates related to navigation and positioning systems. This ensures adherence to safety guidelines and industry best practices.

Increased Situational Awareness: GPS and GNSS receivers offer pilots and air traffic controllers increased situational awareness by providing accurate real-time positioning information. This enables better decision-making and coordination during flights.

Integration with Avionics Systems: The integration of GPS and GNSS receivers with avionics systems allows for seamless data exchange and communication between different aircraft systems. This integration enhances overall system functionality and performance.

SWOT Analysis:

Strengths:

GPS and GNSS receivers provide accurate and reliable positioning and navigation information.

Continuous technological advancements enhance the performance of these receivers.

The integration of GPS and GNSS with avionics systems improves overall system efficiency.

Weaknesses:

Vulnerability to signal interference and spoofing poses a risk to the accuracy and reliability of GPS and GNSS receivers.

Limited signal availability in certain environments can impact the performance of these receivers.

Opportunities:

Adoption of next-generation satellite systems presents growth opportunities.

Integration with emerging technologies such as AR and AI offers new possibilities.

Growing demand for UAVs creates a market for GPS and GNSS receivers.

Threats:

Regulatory compliance and certification requirements add complexity and cost to the adoption process.

Competing technologies and alternative navigation systems may impact market demand.

Market Key Trends:

Increasing Integration of Multiple Satellite Constellations: GPS and GNSS receivers are now capable of receiving signals from multiple satellite constellations, including GPS, Galileo, BeiDou, and NavIC. This integration enhances receiver performance, signal availability, and overall navigation accuracy.

Advancements in Signal Processing Techniques: The continuous advancements in signal processing techniques enable GPS and GNSS receivers to mitigate signal interference, improve signal acquisition, and enhance overall performance in challenging environments.

Miniaturization and Compact Design: GPS and GNSS receivers are becoming smaller and more compact, allowing for easier integration into avionics systems and reducing the space and weight requirements. This trend enables their usage in a wider range of aircraft, including smaller and unmanned aerial vehicles (UAVs).

Increased Focus on Cybersecurity: With the growing concern of cybersecurity threats, there is an increased focus on securing GPS and GNSS receivers against potential hacking and spoofing attacks. Manufacturers are incorporating robust security features to protect the integrity of the navigation data.

Growing Demand for Real-time Data: The aviation industry is placing a greater emphasis on real-time data for improved decision-making and operational efficiency. GPS and GNSS receivers are evolving to provide enhanced real-time data, enabling pilots and operators to make informed decisions based on the most up-to-date information.

Covid-19 Impact:

The COVID-19 pandemic has significantly impacted the aviation industry, leading to a decline in air travel and a temporary reduction in the demand for GPS and GNSS receivers. The global travel restrictions and reduced flight operations have affected the installation and upgrade of navigation systems in aircraft. However, as the aviation industry recovers and air travel resumes, the demand for GPS and GNSS receivers is expected to rebound. The focus on flight safety and efficiency, along with the implementation of stringent health and safety protocols, will drive the adoption of these receivers to support the recovery and future growth of the aviation sector.

Key Industry Developments:

Introduction of Next-Generation Satellite Systems: The launch and operation of next-generation satellite systems, such as Galileo, BeiDou, and NavIC, have expanded the options for GPS and GNSS receivers in the aviation market. These systems offer improved accuracy, coverage, and signal availability, enhancing the performance of navigation systems.

Integration with Emerging Technologies: GPS and GNSS receivers are being integrated with emerging technologies such as augmented reality (AR), artificial intelligence (AI), and machine learning (ML). This integration enables advanced features such as predictive maintenance, intelligent routing, and enhanced situational awareness.

Advancements in Antenna Technology: Antenna technology plays a crucial role in the performance of GPS and GNSS receivers. Ongoing advancements in antenna design, such as multi-constellation and multi-frequency antennas, enhance signal reception, mitigate interference, and improve overall receiver performance.

Analyst Suggestions:

Embrace Next-Generation Satellite Systems: Manufacturers and operators should consider adopting and integrating next-generation satellite systems into their GPS and GNSS receivers to benefit from improved performance, accuracy, and signal availability.

Enhance Cybersecurity Measures: Given the increasing cybersecurity threats, industry participants should focus on implementing robust security measures to safeguard GPS and GNSS receivers against potential hacking and spoofing attacks.

Invest in Research and Development: Continued investment in research and development is crucial to stay at the forefront of GPS and GNSS receiver technology. This includes exploring advancements in signal processing, antenna technology, and integration with emerging technologies.

Collaborate with Stakeholders: Collaboration between manufacturers, airlines, aviation authorities, and satellite system providers is essential to drive innovation, address regulatory challenges, and develop standardized solutions that benefit the entire aviation industry.

Future Outlook:

The future of the GPS and GNSS receiver market in aviation looks promising, driven by the increasing demand for precise navigation, flight safety, and operational efficiency. The integration of next-generation satellite systems, advancements in signal processing and antenna technology, and the integration with emerging technologies will continue to shape the market. As air travel recovers from the COVID-19 pandemic, the demand for GPS and GNSS receivers is expected to rebound, further bolstering market growth.

Conclusion:

The GPS and GNSS receiver market in aviation is experiencing significant growth due to the increasing demand for precise navigation and positioning capabilities in the aviation industry. Despite challenges such as signal interference and limited signal availability, the market presents opportunities through the adoption of next-generation satellite systems, integration with emerging technologies, and the growing demand for UAVs. Manufacturers and operators should focus on enhancing flight safety, improving operational efficiency, complying with regulatory standards, and embracing advancements in receiver technology. With the future recovery and growth of the aviation industry, the demand for GPS and GNSS receivers is expected to increase, creating a favorable market outlook.

What is GPS and GNSS Receivers in Aviation?

GPS and GNSS receivers in aviation are devices that utilize Global Positioning System (GPS) and Global Navigation Satellite System (GNSS) technologies to determine the precise location and navigation of aircraft. These systems enhance flight safety, improve navigation accuracy, and support various aviation applications such as air traffic management and flight planning.

What are the key companies in the GPS and GNSS Receivers in Aviation market?

Key companies in the GPS and GNSS Receivers in Aviation market include Garmin, Honeywell, and Rockwell Collins, which are known for their advanced navigation solutions and technologies. These companies focus on developing innovative products that enhance aviation safety and efficiency, among others.

What are the growth factors driving the GPS and GNSS Receivers in Aviation market?

The growth of the GPS and GNSS Receivers in Aviation market is driven by increasing air traffic, advancements in satellite technology, and the demand for enhanced navigation systems. Additionally, the integration of these receivers in unmanned aerial vehicles (UAVs) and commercial aircraft is contributing to market expansion.

What challenges does the GPS and GNSS Receivers in Aviation market face?

Challenges in the GPS and GNSS Receivers in Aviation market include signal interference, the high cost of advanced systems, and regulatory compliance issues. These factors can hinder the adoption of new technologies and affect the overall growth of the market.

What opportunities exist in the GPS and GNSS Receivers in Aviation market?

Opportunities in the GPS and GNSS Receivers in Aviation market include the development of next-generation navigation systems and the increasing use of satellite-based augmentation systems (SBAS). Furthermore, the growing trend of automation in aviation presents significant potential for innovative GNSS solutions.

What trends are shaping the GPS and GNSS Receivers in Aviation market?

Trends shaping the GPS and GNSS Receivers in Aviation market include the integration of artificial intelligence for improved navigation accuracy and the rise of multi-constellation GNSS systems. Additionally, there is a growing focus on enhancing cybersecurity measures to protect navigation systems from potential threats.

Leading Companies in the GPS and GNSS Receivers in Aviation Market:

Garmin Ltd.

Honeywell International Inc.

NovAtel Inc. (Hexagon AB)

Trimble Inc.

Topcon Corporation

Rockwell Collins, Inc.

u-blox Holding AG

Advanced Navigation

Hemisphere GNSS

Spectra Precision

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.