444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

Market Overview

The global thin and ultra-thin films market is experiencing significant growth due to advancements in technology and the increasing demand for lightweight and flexible electronic devices. Thin and ultra-thin films are used in various applications, including semiconductors, photovoltaics, optoelectronics, and display technologies. These films, typically ranging from a few nanometers to a few micrometers in thickness, offer unique properties such as high conductivity, optical transparency, and mechanical flexibility.

Meaning

Thin films refer to a layer or coating of material with a thickness ranging from a few nanometers to a few micrometers. These films are deposited onto a substrate using techniques such as physical vapor deposition (PVD) or chemical vapor deposition (CVD). Ultra-thin films, on the other hand, are even thinner, typically less than 100 nanometers in thickness. These films are often used to enhance the performance of electronic devices by providing specific functionalities and properties.

Executive Summary

The global thin and ultra-thin films market is poised for significant growth in the coming years. The increasing demand for consumer electronics, advancements in nanotechnology, and the need for miniaturization are driving the market’s expansion. Thin and ultra-thin films find applications in various industries, including electronics, energy, healthcare, and aerospace. The market is characterized by intense competition, with key players focusing on product development and strategic collaborations to gain a competitive edge.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

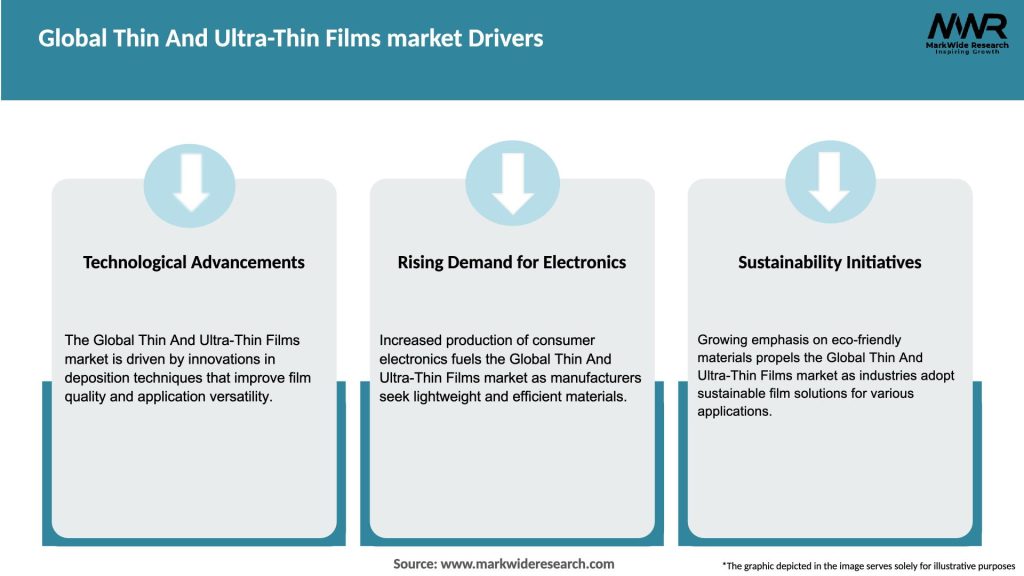

Market Drivers

Market Restraints

Market Opportunities

Market Dynamics

The global thin and ultra-thin films market is driven by various dynamics, including technological advancements, changing consumer preferences, and industry collaborations. The market is highly competitive, with key players striving to gain a competitive edge through product innovation, strategic alliances, and geographic expansion. The demand for thin and ultra-thin films is expected to grow significantly in the coming years, driven by the increasing adoption of flexible electronics, advancements in nanotechnology, and the need for sustainable energy solutions.

Regional Analysis

The Asia-Pacific region dominates the global thin and ultra-thin films market, accounting for the largest share in terms of production and consumption. Countries such as China, Japan, and South Korea are key contributors to the region’s market growth. The presence of a well-established electronics industry, strong research and development infrastructure, and favorable government policies supporting technological advancements are driving the market in this region.

North America and Europe also hold significant market shares due to the presence of major players, technological expertise, and the growing demand for advanced electronic devices. The increasing focus on renewable energy sources, such as solar power, is expected to drive the demand for thin film photovoltaic cells in these regions.

Latin America and the Middle East & Africa are witnessing steady growth in the thin and ultra-thin films market, driven by increasing investments in the electronics and energy sectors. The market in these regions is characterized by the growing adoption of advanced technologies and the emergence of local players.

Competitive Landscape

Leading companies in the Global Thin And Ultra-Thin Films Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Segmentation

The global thin and ultra-thin films market can be segmented based on material type, deposition technique, application, and region.

Category-wise Insights

Key Benefits for Industry Participants and Stakeholders

SWOT Analysis

Market Key Trends

Covid-19 Impact

The global thin and ultra-thin films market experienced temporary disruptions due to the COVID-19 pandemic. The implementation of lockdowns, supply chain disruptions, and reduced consumer spending impacted the demand and production of thin films. However, the market showed resilience and adapted to the changing dynamics.

During the pandemic, the demand for electronic devices, especially for remote working and online entertainment, increased. This trend drove the need for thin and ultra-thin films used in displays, semiconductors, and other electronic components. The market also witnessed increased focus on research and development of thin film technologies to address emerging challenges and opportunities.

Government stimulus packages, supportive policies, and investments in renewable energy infrastructure have helped in the recovery of the thin and ultra-thin films market. As economies gradually reopen and demand stabilizes, the market is expected to regain momentum and exhibit steady growth.

Key Industry Developments

Analyst Suggestions

Future Outlook

The global thin and ultra-thin films market is expected to witness substantial growth in the coming years. The increasing demand for lightweight and flexible electronic devices, advancements in nanotechnology, and the focus on renewable energy sources are key factors driving the market’s expansion.

Technological advancements in deposition techniques and material science will play a crucialrole in shaping the future of the market. New methods such as atomic layer deposition (ALD) and molecular beam epitaxy (MBE) will enable the production of thin and ultra-thin films with enhanced properties and performance.

The adoption of flexible electronics is expected to rise, driven by the demand for wearable devices, flexible displays, and bendable electronic components. This trend will create opportunities for thin and ultra-thin films, as they offer the required flexibility and functionality.

Conclusion

The global thin and ultra-thin films market is experiencing significant growth and is poised for a promising future. The demand for lightweight, flexible electronic devices, advancements in nanotechnology, and the focus on sustainable energy sources are driving the market’s expansion. Thin and ultra-thin films, with their unique properties and functionalities, play a crucial role in various industries such as electronics, energy, healthcare, and aerospace.

Key market insights indicate the dominance of the Asia-Pacific region, particularly China, Japan, and South Korea, in terms of production and consumption. However, North America and Europe also hold significant market shares due to technological expertise and the demand for advanced electronic devices. Latin America and the Middle East & Africa are witnessing steady growth, driven by investments in the electronics and energy sectors.

What is Thin And Ultra-Thin Films?

Thin and ultra-thin films are layers of material ranging from a few nanometers to several micrometers in thickness. They are used in various applications, including electronics, optics, and coatings, due to their unique properties and functionalities.

What are the key players in the Global Thin And Ultra-Thin Films market?

Key players in the Global Thin And Ultra-Thin Films market include companies like Corning Incorporated, Applied Materials, and 3M Company, which are known for their innovations in film technologies and applications across multiple industries, among others.

What are the growth factors driving the Global Thin And Ultra-Thin Films market?

The Global Thin And Ultra-Thin Films market is driven by the increasing demand for lightweight and flexible electronics, advancements in nanotechnology, and the growing need for energy-efficient solutions in solar panels and displays.

What challenges does the Global Thin And Ultra-Thin Films market face?

Challenges in the Global Thin And Ultra-Thin Films market include the high cost of production, difficulties in achieving uniform thickness, and the need for specialized equipment, which can limit accessibility for smaller manufacturers.

What opportunities exist in the Global Thin And Ultra-Thin Films market?

The Global Thin And Ultra-Thin Films market presents opportunities in emerging applications such as flexible displays, advanced photovoltaic cells, and smart coatings, driven by technological advancements and increasing consumer demand for innovative products.

What trends are shaping the Global Thin And Ultra-Thin Films market?

Trends in the Global Thin And Ultra-Thin Films market include the rise of sustainable materials, the integration of smart technologies in films, and the growing focus on miniaturization in electronic devices, which are influencing product development and market strategies.

Global Thin And Ultra-Thin Films market

| Segmentation Details | Description |

|---|---|

| Product Type | Polymer Films, Metal Films, Glass Films, Composite Films |

| End User | Electronics, Packaging, Automotive, Aerospace |

| Application | Solar Cells, Displays, Sensors, Insulation |

| Technology | Vacuum Deposition, Roll-to-Roll Processing, Coating, Laminating |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Global Thin And Ultra-Thin Films Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

North America

o US

o Canada

o Mexico

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA