The Global Hazardous Area Equipment market is a thriving industry that encompasses a wide range of products designed to operate safely in potentially explosive environments. These hazardous areas are typically found in industries such as oil and gas, chemical manufacturing, mining, and pharmaceuticals, where the presence of flammable gases, vapors, or combustible dusts pose a significant risk to personnel and equipment.

Meaning

Hazardous area equipment refers to devices and systems that are specifically engineered and certified to meet stringent safety standards and regulations. These products are designed to prevent ignition sources and contain potential explosions, minimizing the risk of catastrophic incidents in hazardous environments. Examples of hazardous area equipment include explosion-proof lighting fixtures, intrinsically safe instruments, flame detectors, and explosion-proof enclosures.

Executive Summary

The Global Hazardous Area Equipment market has experienced substantial growth in recent years, driven by increasing industrialization and the need for robust safety measures. The demand for hazardous area equipment is fueled by stringent government regulations and the growing awareness of workplace safety. Additionally, the expansion of key industries such as oil and gas exploration, chemical processing, and mining in emerging economies has further propelled market growth.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Product Diversity: Explosion-proof enclosures and flameproof motors account for over 30% of market revenue, with intrinsic safety and purged/pressurized systems growing fastest (CAGR ~8%) due to their flexibility and digital integration.

Regulatory Stringency: Adoption of IECEx and ATEX codes worldwide, plus NEC/CEC updates in North America, drives replacement of legacy non-certified equipment and ensures global interoperability.

Digital Transformation: Certified industrial Ethernet switches, remote I/O modules, and intrinsically safe wireless networks enable secure data collection from hazardous zones for real-time monitoring.

Aftermarket Services: Inspection, recertification, and modernization services represent ~25% of market revenues, as operators extend asset life under updated safety standards.

Regional Leadership: Asia Pacific holds the largest share (>35%), followed by North America and Europe; Middle East & Africa is the fastest growing region, fueled by petrochemical and LNG expansions.

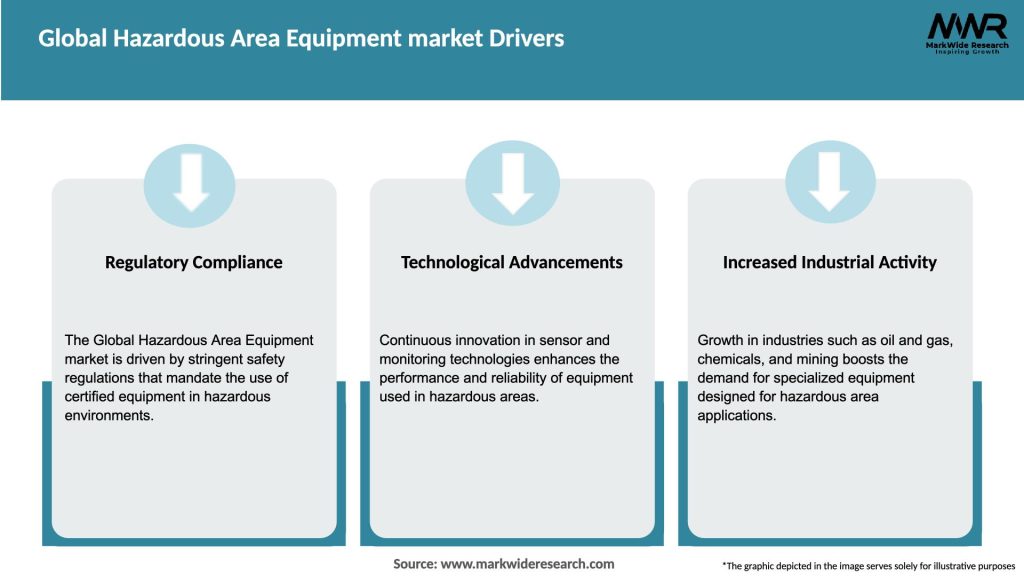

Market Drivers

Energy Sector Capital Expenditure: New offshore platforms and refinery upgrades require robust hazardous area equipment to support high-pressure, high-temperature operations.

Safety & Compliance Mandates: Regulatory enforcement and corporate safety programs mandate the use of certified equipment to protect personnel and assets, reducing downtime and liability.

Automation & IIoT Adoption: Integrating field devices into digital twins and predictive maintenance platforms necessitates explosion-protected communications and smart instrumentation.

Aging Infrastructure Modernization: Replacement of legacy assets with modern, efficient, and compliant equipment drives continuous retrofit and upgrade cycles.

Urbanization & Industrial Growth: Expansion of chemical, pharmaceutical, and battery manufacturing hubs in emerging markets increases installations of hazardous area systems.

Market Restraints

High Initial Costs:Explosion-proof and intrinsically safe solutions command price premiums over standard industrial equipment, challenging capital budgeting in cost-sensitive projects.

Certification Complexity: Lengthy and fragmented approval processes across regions (IECEx, ATEX, UL, CSA) extend lead times and development costs for new products.

Supply Chain Disruptions: Dependence on specialty enclosures, tempered glass, and certified components can cause delays when suppliers face raw material shortages.

Technical Expertise Shortage: Qualified engineers to design, install, and maintain hazardous area systems are in short supply, especially in remote or developing regions.

Obsolescence Management: Rapid digitalization of field devices leads to legacy installations that struggle to integrate with modern control architectures.

Market Opportunities

Modular & Retrofit Solutions: Compact purged/pressurized panels and explosion-proof conversion kits simplify upgrades without full system replacement.

Wireless & IIoT Devices: Intrinsically safe wireless sensor networks and Bluetooth-enabled transmitters reduce wiring costs and enable expanded monitoring.

Digital Certification Tools: Software that automates zone classification, compliance documentation, and risk assessment accelerates project timelines.

Eco-Efficient Equipment: Energy-optimized explosion-proof motors and LED lighting fixtures reduce operating costs and support sustainability goals.

Value-Added Services: Remote-monitoring subscription models for hazardous area assets deliver predictive maintenance and compliance alerts as ongoing services.

Market Dynamics

Strategic Partnerships: Alliances between process automation majors (e.g., Emerson, Honeywell) and enclosure specialists (e.g., R. Stahl, Pepperl+Fuchs) deliver integrated solutions.

Acquisitions: Consolidation among mid-tier vendors expands geographic reach and deepens certification capabilities, catering to global operator needs.

Standard Harmonization: Industry efforts to align IECEx, ATEX, NEC, and CEC requirements simplify equipment design and reduce duplication of tests.

Customer-Centric Models: Suppliers increasingly bundle products with engineering, installation, and digital support services to differentiate offerings.

Innovation Funding: Government incentives for industrial safety and energy efficiency spur R&D into next-generation hazardous area technologies.

Regional Analysis

Asia Pacific: Rapid infrastructure build-out in China, India, and Southeast Asia drives installations of certified motors, drives, and control systems in refineries, petrochemicals, and LNG terminals.

North America: Mature market with focus on modernization, safety-driven retrofit programs, and IIoT integration in upstream oil & gas and chemical complexes.

Europe: Stringent ATEX and REACH regulations promote adoption of low-VOC, flameproof devices and encourage local manufacturing under trade compliance regimes.

Middle East & Africa: Petrochemical mega-projects and desert mining operations fuel demand for robust, high-temperature hazardous area equipment and remote-service capabilities.

Latin America: Oil & gas revitalization and growing pharmaceuticals sector in Brazil, Mexico, and Argentina generate new equipment requirements and aftermarket services.

Competitive Landscape

Leading companies in the Global Hazardous Area Equipment market:

Eaton Corporation PLC

Siemens AG

ABB Ltd.

Honeywell International Inc.

Rockwell Automation, Inc.

R. Stahl AG

Emerson Electric Co.

Pepperl+Fuchs AG

Cooper Industries, Inc. (Eaton)

Bartec Group

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

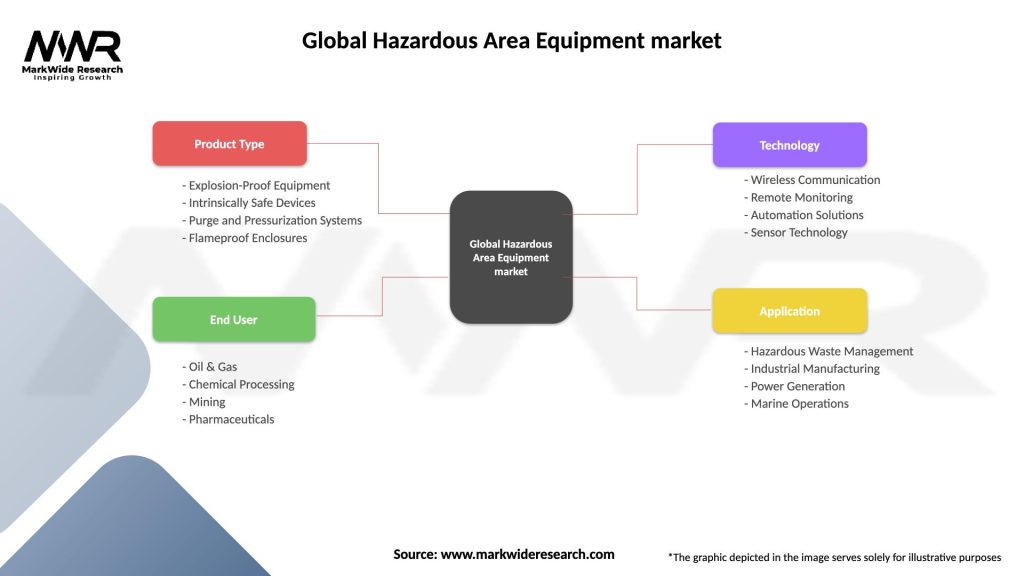

By End-Use Industry: Oil & Gas, Chemicals & Petrochemicals, Pharmaceuticals, Power Generation, Mining, Food & Beverage

By Certification: IECEx, ATEX, NEC/CEC (Class I Div 1/2), Other Regional Standards

By Region: Asia Pacific, North America, Europe, Middle East & Africa, Latin America

Category-wise Insights

Explosion-Proof Motors & Drives: Dominant segment (~35% revenue) due to widespread need for robust rotating equipment; trend toward low-voltage starter drives to reduce enclosure size.

Intrinsically Safe Instrumentation: High growth-rate segment (~9% CAGR), as wireless sensors and digital field devices expand in Zone 0/1 applications requiring minimal ignition energy.

Flameproof Enclosures & HMI: Integrated operator stations in Zone 1/2 environments growing, with touchscreen HMIs now certified for hazardous areas, enabling digital transformation at the edge.

Purged & Pressurized Panels: Offer cost-effective zone conversions and safe housing for non-certified PLCs and drives; modular skids pre-wired and certified simplify installation.

Lighting & Emergency Systems: LED-based explosion-proof luminaires and exit signs reduce maintenance and energy consumption in hazardous facilities.

Key Benefits for Industry Participants and Stakeholders

Enhanced Safety & Compliance: Certified equipment minimizes ignition risks and ensures regulatory adherence, protecting personnel and assets.

Reduced Downtime: High-integrity components and robust enclosure designs prevent unplanned outages in mission-critical processes.

Operational Efficiency: Digital-ready instruments and smart enclosures streamline data collection and control in hazardous zones, enabling remote diagnostics.

Lower TCO: Modular retrofit kits and service agreements reduce lifecycle costs by extending intervals between inspections and recertifications.

Scalability: Standardized solutions across regions simplify global roll-outs and support multi-site operation consistency.

SWOT Analysis

Strengths

Established safety standards and certification regimes ensure high performance and reliability.

Broad product portfolios spanning hardware, software, and services for end-to-end solutions.

Weaknesses

High capital expenditure and longer lead times relative to standard industrial equipment.

Complexity of maintaining multiple certification labels for different regions.

Opportunities

Expansion of wireless intrinsically safe networks and IIoT in hazardous zones.

Growth of renewable energy (hydrogen, biomass) facilities requiring classified equipment.

Threats

Emergence of alternative non-electrical monitoring (e.g., fiber-optic sensing) reducing electrical equipment footprint.

Potential supply chain disruptions for critical components and specialty materials.

Market Key Trends

IIoT & Edge Computing: Explosion-proof gateways and intrinsically safe edge controllers enable local analytics, reducing latency and cabling.

Wireless Safety: Certified wireless fieldbus and sensor networks simplify installation in remote or retrofit scenarios.

Prefabricated Skids: Factory-assembled, certified modules for pumps, compressors, and control panels accelerate deployment and ensure quality.

Predictive Maintenance: Integration of vibration, temperature, and gas-detection sensors in hazardous areas supports condition-based monitoring strategies.

Digital Twin Models: Virtual replicas of hazardous facilities and equipment inform risk analyses, maintenance planning, and training.

Covid-19 Impact

Pandemic-driven restrictions delayed installations and site access, but digital tools (remote audits, virtual inspections) gained traction. Supply-chain pressures highlighted the need for regional stocking and digital inventory management. Subsequent recovery saw accelerated investment in safety systems as operations resumed under strict health and safety protocols.

Key Industry Developments

Strategic Alliances: Partnerships between automation majors and telecommunications providers to develop explosion-proof 5G base stations for industrial campuses.

New Product Launches: Certification of intrinsically safe OPC UA gateways and APC edge devices for secure, standardized data exchange.

Facility Expansions: Investments in regional manufacturing lines for ATEX-certified enclosures and intrinsically safe components in India and Brazil.

Regulatory Updates: NEC 2023 revisions expanding definitions of hazardous areas and introducing additional equipment marking requirements.

Analyst Suggestions

Accelerate Digital Integration: Expand offerings of certified industrial routers, switches, and edge analytics to capture IIoT growth in hazardous zones.

Develop Retrofit Solutions: Innovate compact purged/pressurized modules for rapid upgrades of existing plants lacking certified power and control cabinets.

Enhance Service Ecosystems: Bundle equipment sales with digital maintenance platforms, compliance tracking, and remote-monitoring subscriptions.

Localize Capabilities: Establish calibration and recertification centers close to end-users in fastest-growing regions to reduce downtime and logistics costs.

Future Outlook

The Hazardous Area Equipment market is poised for sustained, technology-driven growth as digital transformation and safety imperatives converge. Adoption of wireless intrinsically safe devices and explosion-proof edge computing will redefine how data is collected and actioned in classified zones. Renewable energy and hydrogen processing facilities will introduce new certification challenges and growth avenues. Suppliers that combine deep domain expertise with modular, digital solutions and robust aftermarket support will lead this critical segment, safeguarding both personnel and production in the world’s most demanding environments.

Conclusion

Hazardous area equipment remains foundational to the safe operation of industries working under explosive or combustible conditions. Through continuous innovation—in certification, digital integration, and modular design—suppliers enable customers to meet evolving regulatory and operational demands. As the market shifts toward connected, smarter facilities, hazardous area devices will not only protect against ignition risks but also serve as key nodes in the Industrial Internet of Things, driving efficiency, insight, and resilience.

What is Hazardous Area Equipment?

Hazardous Area Equipment refers to specialized devices and systems designed to operate safely in environments where flammable gases, vapors, or dust may be present. These products are essential in industries such as oil and gas, chemical processing, and mining.

What are the key players in the Global Hazardous Area Equipment market?

Key players in the Global Hazardous Area Equipment market include companies like Siemens, Honeywell, and ABB, which provide a range of solutions for hazardous environments. These companies focus on innovation and compliance with safety standards, among others.

What are the growth factors driving the Global Hazardous Area Equipment market?

The Global Hazardous Area Equipment market is driven by increasing safety regulations, the growth of the oil and gas sector, and the rising demand for automation in hazardous environments. Additionally, advancements in technology are enhancing equipment efficiency and safety.

What challenges does the Global Hazardous Area Equipment market face?

The Global Hazardous Area Equipment market faces challenges such as high costs of compliance with safety standards and the complexity of integrating new technologies into existing systems. Additionally, fluctuating raw material prices can impact production costs.

What opportunities exist in the Global Hazardous Area Equipment market?

Opportunities in the Global Hazardous Area Equipment market include the expansion of renewable energy projects and the increasing adoption of smart technologies in hazardous areas. These trends are likely to drive demand for innovative equipment solutions.

What trends are shaping the Global Hazardous Area Equipment market?

Trends shaping the Global Hazardous Area Equipment market include the integration of IoT technologies for real-time monitoring and predictive maintenance, as well as a growing focus on sustainability and energy efficiency in hazardous environments. These innovations are transforming how equipment is designed and utilized.

Leading companies in the Global Hazardous Area Equipment market:

Eaton Corporation PLC

Siemens AG

ABB Ltd.

Honeywell International Inc.

Rockwell Automation, Inc.

R. Stahl AG

Emerson Electric Co.

Pepperl+Fuchs AG

Cooper Industries, Inc. (Eaton)

Bartec Group

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.